Aluminum for Packaging Market Overview: Market Size, Growth, and Industry Insights

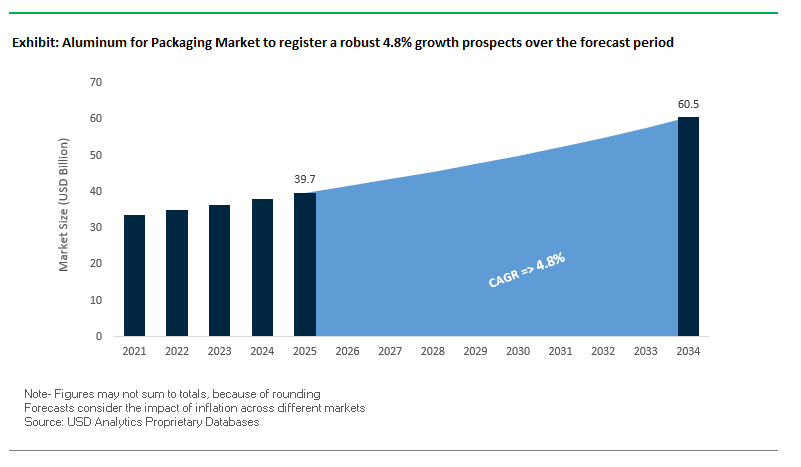

The Global Aluminum for Packaging Market is projected to reach $39.7 billion in 2025 and grow to $60.5 billion by 2034, expanding at a CAGR of 4.8%. Aluminum remains one of the most critical materials in modern packaging due to its recyclability, lightweight properties, and barrier protection. Its role spans across food, beverages, pharmaceuticals, and cosmetics, making it an indispensable material for industries that rely on product integrity and sustainability.

Aluminum’s infinite recyclability ensures it plays a pivotal role in the circular economy. With global recycling rates exceeding 75% for packaging applications, aluminum drastically reduces carbon emissions and energy consumption compared to virgin material production. Its superior barrier properties against oxygen, bacteria, moisture, and light extend product shelf life, minimizing food waste and ensuring pharmaceutical efficacy. Moreover, lightweighting aluminum beverage cans and packaging contributes to significant logistics savings and reduces the carbon footprint.

The beverage industry’s shift toward aluminum cans highlights changing consumer preferences, where sustainability and convenience converge. Cans chill faster, preserve taste longer by blocking light, and align with consumer demand for eco-friendly solutions. This shift away from plastic bottles further strengthens aluminum’s dominance in sustainable packaging strategies.

Key Insights for Industry Professionals

- Recyclability Advantage: Over 75% of aluminum packaging is recycled globally, making it central to circular economy goals.

- Barrier Protection: Aluminum provides total protection from light, moisture, oxygen, and bacteria.

- Lightweight Benefits: Reduces shipping costs and environmental impact across supply chains.

- Cans Over Plastic: Beverage companies are rapidly transitioning from plastic bottles to recyclable aluminum cans.

Market Analysis: Recent Industry Developments Driving Growth

The aluminum packaging industry is undergoing a period of rapid transition, with leading companies prioritizing sustainability and innovation. In August 2025, Crown Holdings, Inc. achieved validation from the Science Based Targets initiative (SBTi) for its updated net-zero commitments, a landmark achievement reinforcing its leadership in sustainable aluminum beverage cans. In July 2025, Crown also reported strong Q2 financial results, underscoring growing demand in beverage packaging.

In the same month, Constellium SE reported robust Q2 2025 performance and raised full-year guidance, reflecting packaging as a major growth driver. Constellium further showcased its innovation leadership at the June 2025 Paris Air Show, unveiling the world’s first aluminum ingot created from end-of-life aircraft, advancing its circular economy strategy. Similarly, Ardagh Group announced a recapitalization plan in July 2025, ensuring stability in its packaging operations.

Innovation also remains a competitive hallmark. Ball Corporation was recognized in May 2025 with four EMBANEWS Awards for sustainable packaging, including a braille-embossed lid in Brazil to improve inclusivity. Ball also expanded its market reach by acquiring Florida Can Manufacturing in February 2025 for $160 million, boosting regional capacity in North America.

Global trade dynamics also played a critical role. In March 2025, the U.S. government doubled tariffs on imported aluminum and steel, reshaping supply chains and forcing manufacturers to rethink sourcing strategies. Meanwhile, Ardagh Metal Packaging S.A. projected volume growth in February 2025, driven by rising demand in alcoholic beverages, carbonated soft drinks, and energy drinks.

Key Market Trends and Strategic Opportunities Driving Aluminum Packaging Innovation

Accelerated Investment in Low-Carbon Primary Aluminum and Advanced Recycling Infrastructure

The aluminum for packaging market is witnessing substantial transformation as producers prioritize decarbonization to meet net-zero goals and respond to emerging carbon border taxes. Corporations are making multi-billion-dollar investments to reduce the carbon footprint of primary aluminum production while scaling advanced sorting technologies for increased post-consumer recycled (PCR) content. The World Economic Forum estimates that achieving net-zero aluminum production by 2050 requires a staggering $1 trillion investment across power, smelters, and production facilities. Leading players, such as Norsk Hydro, are converting fossil-fuel-based equipment to renewable energy, natural gas, and biomass at its Alunorte alumina refinery, projected to reduce annual CO2 emissions by 1.4 million tonnes. Furthermore, North American aluminum producers benefit from a first-mover advantage, as domestic production is approximately half as carbon-intensive as global averages, positioning them favorably for low-carbon supply chains and sustainability-driven procurement decisions.

Adoption of Digital Watermarking for Enhanced Sortation and Closed-Loop Recycling

To achieve high-purity recycling and enable true circularity in aluminum packaging, digital watermarking technologies such as HolyGrail 2.0 are being piloted for automated sorting. These technologies allow packaging to be accurately identified and separated in complex waste streams, ensuring that post-consumer aluminum can re-enter production with minimal contamination. Trials at German material recovery facilities have demonstrated detection accuracy between 87.9% and 93.8% for rigid plastics, showcasing the potential for similar high-efficiency sorting of aluminum cans and trays. By enabling SKU-level sorting and differentiating food-grade from non-food-grade packaging, digital watermarking creates high-value recycling streams, reduces material loss, and supports closed-loop aluminum packaging, which is critical for sustainability compliance and corporate ESG goals.

Development of High-Strength, Thin-Wall Alloys for Lightweighting and Carbon Reduction

Significant opportunities exist in metallurgical innovation to produce high-strength, thin-wall aluminum alloys for lightweighting cans, trays, and foils. Advanced alloys such as 5000 and 7000 series allow material thickness reduction while maintaining mechanical integrity, enabling lower aluminum consumption per package. Lightweighting directly reduces material costs and embedded carbon, supporting both economic efficiency and sustainability objectives. Thinner-gauge cans and closures also help manufacturers meet global regulations targeting lower carbon footprints and resource-efficient packaging.

Strategic Positioning of Aluminum in Pharmaceutical and Battery Electrode Packaging

Beyond conventional beverage and food containers, aluminum packaging is strategically expanding into high-growth, non-cyclical sectors such as pharmaceutical blister packs and lithium-ion battery electrode components. In pharmaceuticals, aluminum provides an impermeable barrier against moisture, oxygen, and light, ensuring safety and extended shelf life for sensitive medications. Similarly, in battery applications, aluminum foil serves as the cathode current collector, offering exceptional electrical conductivity, high purity, and ultra-thin production capabilities (0.01–0.03mm). This diversification leverages aluminum’s unique barrier and conductive properties, meeting growing demand in EV batteries and advanced healthcare packaging, while reinforcing its strategic value in ESG-conscious supply chains.

Competitive Landscape: Leading Companies in Global Aluminum for Packaging

The competitive environment in the aluminum packaging market is defined by multinational leaders investing in sustainability, scaling production, and embedding innovation into product lines. These companies are addressing rising demand from beverages, food, pharmaceuticals, and personal care sectors with recyclable, lightweight, and innovative aluminum solutions.

Crown Holdings, Inc.: Advancing Sustainability with the Twentyby30™ Program

Crown Holdings is a leading producer of aluminum and steel beverage cans with a global manufacturing footprint spanning 57 facilities. Its Twentyby30™ program sets ambitious sustainability goals targeting emissions, water use, and recycling improvements. Crown’s strength lies in its ability to serve multinational brands efficiently while maintaining its focus on continuous innovation and environmental performance.

Ball Corporation: Expanding Capacity and Inclusive Packaging Solutions

Ball Corporation is a pioneer in aluminum beverage cans, bottles, and cups. In 2025, it launched a joint venture to grow its aluminum cup business, reshaping single-use product sustainability. It also became the first impact-extruded aluminum packaging supplier certified by ASI. With the acquisition of Florida Can Manufacturing in February 2025, Ball expanded North American production, meeting growing demand while reinforcing its sustainability agenda.

Amcor plc: Innovating Sustainable Packaging Alternatives

Amcor offers high-performance aluminum foil packaging solutions alongside flexible and rigid plastic packaging. In 2025, it introduced its “Bottles of the Year” program, showcasing innovative, consumer-driven designs. Its AmLite Recyclable packaging line demonstrates its commitment to replacing traditional laminates with recyclable alternatives. Amcor’s strategy focuses on achieving 100% recyclable or reusable packaging by 2025, backed by digital solutions like MaXQ Smart Packaging.

Ardagh Group S.A.: Lightweighting and Low-Carbon Packaging Leadership

Ardagh Group, through its Ardagh Metal Packaging (AMP) division, is a global leader in aluminum beverage cans and aerosol containers. Its innovations in lightweighting and advanced modeling reduce material usage and energy intensity. In addition, Ardagh is investing in fuel switching trials to lower carbon emissions in its production. Its expertise in high-quality packaging solutions makes it a reliable partner for both food and personal care industries.

Constellium SE: Circular Economy Leadership in Aluminum Packaging

Constellium leverages its scale and R&D strength to deliver rolled and extruded aluminum products for packaging, aerospace, and automotive sectors. In June 2025, it unveiled an aluminum ingot created from retired aircraft at the Paris Air Show, exemplifying its focus on circularity. Its packaging segment continues to perform strongly, as reflected in Q2 2025 results. With a focus on recycling, material innovation, and large-scale production, Constellium is positioned as a key player in the sustainable aluminum packaging value chain.

Aluminum for Packaging Market Share Insights

Foils Lead Market Share by Product Type in the Aluminum for Packaging Industry

Aluminum foils account for the largest share at 38%, underlining their status as the barrier material of choice across food, beverage, and pharmaceutical packaging. Their ability to provide absolute protection against oxygen, light, and moisture ensures product stability and extended shelf life, which is critical for categories such as dairy, confectionery, and blister-packed pharmaceuticals. This segment benefits heavily from its versatility serving both flexible laminates in pouches and rolls for household and foodservice use. Rolled aluminum, the second major segment, anchors the global beverage can industry, where demand is fueled by the surging popularity of aluminum cans for beer, soft drinks, and ready-to-drink cocktails. Continuous innovations in alloy composition and lightweighting allow producers to reduce metal use per can, improving sustainability and cost-efficiency. Containers such as trays and semi-rigid pans are gaining traction in the ready-meal and pet food sectors, leveraging recyclability and excellent heat conductivity to compete against plastic trays. Castings and extrusions, though niche, hold importance in premium cosmetics, pharmaceuticals, and aerosols, where aluminum’s malleability and premium appearance enable differentiation in high-value applications.

Cans Dominate Market Share by End-Use Industry in the Aluminum for Packaging Industry

Cans represent 65% of aluminum packaging consumption, driven primarily by the beverage sector, where they deliver unmatched recyclability, lightweight logistics benefits, and long-term preservation of taste and carbonation. The rapid rise of hard seltzers, energy drinks, and canned wines has further reinforced this dominance, supported by high-speed global production lines. Trays and containers are the second key segment, capitalizing on the global convenience food trend and consumer preference for sustainable packaging alternatives to plastics. Aluminum trays used in frozen meals, bakery items, and pet food combine recyclability with superior heating and freezing performance, making them indispensable to food manufacturers. Flexible pouches, though not fully aluminum, rely on thin foil layers for barrier protection, expanding their use in coffee, soups, and baby food. Closures and caps remain a critical safety-driven segment, providing tamper evidence and hermetic sealing for bottled beverages, dairy pots, and wine. Bottles and jars are emerging as a premium niche, particularly in spirits, personal care, and luxury beverages, where aluminum’s recyclability and modern aesthetics align with both sustainability goals and high-end branding strategies.

United States: EPR Regulations and Advanced Recycling Transform Aluminum Packaging

The U.S. aluminum for packaging market is witnessing strong growth driven by evolving state-level Extended Producer Responsibility (EPR) laws, which place the cost and responsibility of packaging waste management on producers. This regulatory push incentivizes the adoption of sustainable and recyclable materials such as aluminum, reinforcing eco-friendly packaging trends. Technological advancements are further transforming the market; a strategic partnership between Lotte Aluminium Materials USA and SMS Group in January 2024 aims to implement a logistics and digitalization package for a new greenfield aluminum cathode foil plant in Kentucky, enhancing production efficiency for electric vehicle batteries.

Corporate initiatives are also shaping the industry, with Wyda Packaging entering the U.S. market in November 2024 with a facility producing 100% recyclable aluminum foil and trays for food service, hospitality, and consumer goods sectors. Consumer demand for sustainable solutions continues to rise, prompting companies like Novelis Inc. to expand recycling capabilities and support a circular aluminum economy. Key applications are concentrated in food, pharmaceuticals, and consumer goods, where regulatory requirements demand high-barrier laminates to ensure sterility, integrity, and extended shelf life. Additionally, the Inflation Reduction Act of 2022 provides financial assistance to manufacturers adopting advanced, low-emission technologies, further supporting sustainable aluminum packaging adoption.

Germany: Circular Economy Leadership and Regulatory Compliance Fuel Growth

Germany’s aluminum for packaging market is strongly influenced by stringent regulatory frameworks and leadership in the circular economy. The EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandates that all packaging must be fully recyclable or reusable by 2030 and sets minimum recycled content targets. Complementing this, the German Packaging Act (VerpackG) ensures producers are responsible for the full lifecycle of packaging, benefiting aluminum due to its high recyclability rate.

Technological innovation is driving next-generation lightweight aluminum cans and bottles, optimizing material use while maintaining strength. Governmental mandates under PPWR establish reuse and refill targets, significantly impacting industry operations. Key applications are concentrated in the food and pharmaceutical sectors, where superior barrier properties ensure product freshness and protection. The rapid growth of e-commerce further underscores the need for durable, high-quality packaging capable of withstanding shipping challenges, while the industry continues to shift toward lightweight, recyclable materials in response to both consumer demand and regulatory pressures.

China: Dual Carbon Goals and EV Applications Propel Aluminum Packaging Market

China’s aluminum for packaging market is heavily shaped by governmental initiatives targeting carbon neutrality and peak emissions. The Action Plan for the High-Quality Development of the Aluminium Industry (2025–2027) focuses on resource security, green development, and technological innovation, including a target of 15 Mt of recycled aluminum output. Manufacturers are investing in automation, AI, and “5G plus industrial internet” integration to enhance production efficiency and flexible capacity.

Sustainability is increasingly central, with policies restricting non-degradable plastics boosting demand for recyclable alternatives. China is also a global leader in battery-grade aluminum foil for electric vehicles, producing 122,700 tons in the first half of 2023, highlighting a significant industrial application. Stricter environmental policies are driving industry consolidation, leaving larger producers with increased market share. Domestic e-commerce growth further fuels demand for sustainable, customizable packaging solutions across chemicals, food products, and industrial goods, reflecting a strong alignment between industrial growth and eco-friendly practices.

India: Government Incentives and Sustainable Solutions Drive Market Expansion

India’s aluminum for packaging market benefits from government initiatives such as “Make in India” and “Zero Effect Zero Defect,” promoting high-quality domestic production and industrial infrastructure investment. Hindalco Industries’ acquisition of Hydro’s aluminum extrusions business in December 2021 expands its capabilities in aluminum packaging solutions, supporting market growth. Regulatory policies, including the Plastic Waste Management (Amendment) Rules, promote eco-friendly alternatives, while technological advancements like QR codes and sensors enhance traceability and compliance.

The Indian market is increasingly focusing on sustainability and recycling. Companies like MMP Industries emphasize recycled aluminum in products such as powder, paste, and conductors. Growing middle-class consumption is driving demand for aluminum foil packaging in food and pharmaceuticals, encouraging premium and functional packaging solutions. Combined with rising industrial infrastructure and technological adoption, India is emerging as a hotspot for sustainable and advanced aluminum packaging solutions.

Brazil: Circular Economy Policies and Strategic Investments Boost Aluminum Packaging

Brazil’s aluminum for packaging market is propelled by the National Solid Waste Policy, which promotes a circular economy and encourages the use of reusable and durable alternatives. Technological advancements, including AI and robotics, are enhancing efficiency and quality control, from automated sorting to defect detection. Corporate initiatives, such as Ball Brazil and Açai Motion’s collaboration on an Aluminum Stewardship Initiative (ASI)-certified can in June 2025, ensure sustainable practices from raw material extraction to recycling.

Strategic investments like Novelis Inc.’s Customer Solution Center, opened in São José dos Campos in March 2023, focus on advancing aluminum packaging innovation and sustainability, reflecting Brazil’s growing market importance. The food and beverage sector is a major driver, with expanding food processing fueling demand for foil bags, totes, and containers. A robust recycling infrastructure supports circular economy principles, making aluminum a preferred material for eco-conscious packaging. HTMM is also customizing aluminum foil products for Brazil’s flexible packaging sector, producing 6–7 micron foils for food, pharmaceuticals, consumer goods, and personal care applications.

Japan: Advanced Recycling and Bio-Based Materials Transform Aluminum Packaging

Japan’s aluminum for packaging market is defined by advanced recycling systems and continuous innovation. The country’s Containers and Packaging Recycling Law assigns recycling responsibilities to businesses, creating a robust framework for collecting and repurposing aluminum packaging materials. Regulatory updates by the Ministry of Health, Labour and Welfare (MHLW) in May 2025 revised requirements for food-contact packaging, ensuring safety and compliance.

The market is embracing bio-based materials, with LyondellBasell integrating bio-based polypropylene into Shiseido’s packaging, reflecting sustainability trends. Functional innovations focus on high dimensional stability and resistance to deformation for high-performance applications. Corporate collaborations, such as UACJ’s launch of a recyclable aluminum alloy for EV battery enclosures in June 2025, address the automotive sector’s demand for lightweight, efficient thermal management solutions. These combined efforts position Japan as a leader in sustainable, high-quality aluminum packaging solutions for diverse industries.

Aluminum for Packaging Market Report Scope

Aluminum for Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$39.7 Billion

|

|

Market Size (2034)

|

$60.5 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Product Type (Rolled Aluminum, Castings & Extrusions, Foils, Containers), By Form (Rigid Packaging, Flexible Packaging), By Application (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Automotive, Industrial), By End-Use Industry (Cans, Bottles & Jars, Closures & Caps, Trays & Containers, Flexible Pouches)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ball Corporation, Crown Holdings Inc., Trivium Packaging, Amcor plc, Novelis Inc., Hindalco Industries Limited, UACJ Corporation, Ardagh Group S.A., O-I Glass, Inc., Constantia Flexibles Group GmbH, MMP Industries Ltd., Alcoa Corporation, Emirates Global Aluminium (EGA), CANPACK, DS Smith Plc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aluminum for Packaging Market Segmentation

By Product Type

- Rolled Aluminum

- Castings & Extrusions

- Foils

- Containers

By Form

- Rigid Packaging

- Flexible Packaging

By Application

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Automotive

- Industrial

By End-Use Industry

- Cans

- Bottles & Jars

- Closures & Caps

- Trays & Containers

- Flexible Pouches

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Aluminum for Packaging Market

- Ball Corporation

- Crown Holdings Inc.

- Trivium Packaging

- Amcor plc

- Novelis Inc.

- Hindalco Industries Limited

- UACJ Corporation

- Ardagh Group S.A.

- O-I Glass, Inc.

- Constantia Flexibles Group GmbH

- MMP Industries Ltd.

- Alcoa Corporation

- Emirates Global Aluminium (EGA)

- CANPACK

- DS Smith Plc

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and multi-layered research methodology to provide industry professionals with accurate and actionable insights on the global Aluminum for Packaging Market. Our approach combines extensive primary research interviews with packaging engineers, supply chain executives, sustainability managers, and R&D leaders with secondary research from corporate reports, trade publications, regulatory filings, and industry journals. Market sizing, projected to reach $39.7 billion in 2025 and $60.5 billion by 2034 at a CAGR of 4.8%, is calculated using a mix of top-down and bottom-up approaches, accounting for product types (rolled aluminum, foils, castings & extrusions, containers), packaging forms (rigid, flexible), applications (food & beverages, pharmaceuticals, cosmetics, automotive, industrial), and end-use industries (cans, bottles & jars, closures & caps, trays & containers, flexible pouches). USDAnalytics also evaluates technological innovations such as high-strength thin-wall alloys, advanced recycling streams, digital watermarking for closed-loop recovery, and aluminum’s growing adoption in pharmaceuticals and battery electrode applications. Regional analyses cover major markets including the U.S., Germany, China, India, Brazil, and Japan, incorporating regulatory trends, sustainability mandates, carbon reduction initiatives, and e-commerce-driven packaging requirements. Competitive benchmarking examines key players such as Crown Holdings, Ball Corporation, Constellium SE, Amcor, and Hindalco, highlighting capacity expansion, sustainability programs, and product innovation strategies. This integrated methodology ensures comprehensive market intelligence for informed decision-making in aluminum packaging investments, sustainability planning, and operational optimization.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.