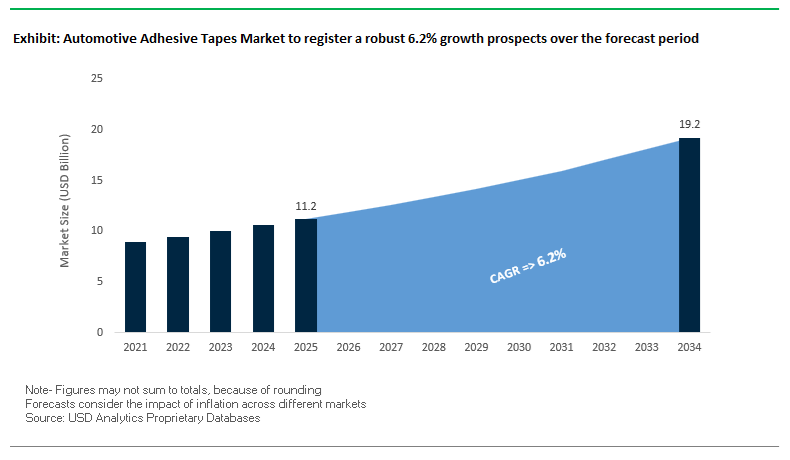

The global automotive adhesive tapes market is projected to grow from USD 11.2 billion in 2025 to USD 19.2 billion by 2034, registering a 6.2% CAGR, as vehicle OEMs accelerate the transition toward electrified powertrains, lightweight multi-material architectures, and fast, automation-ready assembly processes. Adhesive tapes have evolved from secondary fastening aids into functional engineering materials, performing roles that combine structural bonding, vibration damping, thermal management, electrical insulation, and sealing across the vehicle platform.

Leading automotive tape suppliers including 3M, tesa, Avery Dennison, Nitto Denko, Lohmann, and Saint-Gobain position pressure-sensitive adhesive (PSA) tapes as direct replacements for clips, rivets, and welds in both internal and exterior assemblies. High-performance acrylic foam and viscoelastic PSA tapes are routinely specified for body-in-white attachments, trim bonding, glazing, sensor mounting, and exterior appliqués, where they deliver consistent bond strength while absorbing differential thermal expansion between steel, aluminum, composites, and plastics.

Electrification is a primary growth catalyst. EV platforms require adhesive tapes engineered for elevated operating temperatures, dielectric insulation, and long-term durability in battery modules, power electronics, and cable management systems. Automotive-grade tapes qualified for continuous exposure above 120–150 °C, flame-retardancy (UL 94 V-0), and resistance to electrolytes and coolants are increasingly specified in battery pack assembly, cell-to-cell bonding, EMI shielding, and thermal interface applications.

Noise, vibration, and harshness (NVH) control further strengthens demand. Viscoelastic damping tapes and acrylic foam systems are widely used to reduce buzz, squeak, and rattle, replacing heavier mechanical isolators. Manufacturer data consistently shows that these tape-based NVH solutions deliver weight savings of 20–40% compared to traditional rubber or metal isolation components, directly supporting OEM lightweighting targets.

Over the forecast period, adhesive tapes enable high-speed, robot-compatible application, immediate handling strength, and cleaner assembly lines—critical for modern automotive production systems. Tape-based bonding eliminates cure ovens, reduces rework, and improves dimensional repeatability, particularly in high-volume EV and hybrid vehicle programs.

The Global Automotive Adhesive Tapes Market is undergoing a transformative phase characterized by sustainability-driven innovation, supply chain localization, and process automation. In Q4 2025, a major Tier-1 chemical supplier completed the acquisition of a European specialist in conductive and flame-retardant tapes, expanding its presence in EV battery pack shielding and thermal management applications. This acquisition marks a strategic shift toward functional adhesive tapes designed for electromagnetic interference (EMI) shielding and flame protection, which are critical for electric powertrain reliability and passenger safety.

In Q3 2025, a leading global tape manufacturer announced a $3.5 billion multi-year R&D investment plan (through 2027) to pioneer bio-based adhesive systems and PFAS-free formulations, aligning with emerging green manufacturing mandates. The investment focuses on eliminating per- and polyfluoroalkyl substances (PFAS) from production by developing sustainable acrylic and silicone chemistries, which offer high-performance bonding with minimal environmental footprint — a significant differentiator in markets governed by EU REACH and U.S. EPA regulations.

In Q2 2025, tesa SE launched its tesa® 6308 “New Bond” acrylic foam tape series, capable of primerless bonding on low surface energy (LSE) plastics, reducing process cycle times and simplifying OEM assembly lines. Around the same period, a major Asian tape producer announced an expansion in Vietnam (Q1 2025) to enhance regional supply chain resilience and meet growing demand from ASEAN automotive OEMs, highlighting Southeast Asia’s emergence as a key manufacturing hub for vehicle adhesives and tapes.

Earlier, in Q4 2024, an adhesive manufacturer collaborated with an electric vehicle OEM to develop an extrudable VHB tape system optimized for EV battery mounting, enabling automated tape application and thermal interface integration. Further, policy changes in Q3 2024 by the U.S. government accelerated the adoption of lightweight adhesive fastening solutions across federally-funded automotive programs, further reducing reliance on welding and rivets.

In Q2 2024, tesa introduced the flameXtinct™ halogen-free, double-sided acrylic tape, compliant with FMVSS 302 and UL94 standards, designed for interior bonding in transit and safety-critical applications. And in Q1 2024, a global supplier launched a digital bonding simulation platform, integrating 3D modeling and joint design optimization tools for engineers — signifying the industry’s evolution toward digitally validated adhesive integration across automotive design stages.

The global automotive sector is undergoing a paradigm shift toward multi-material lightweighting, combining steel, aluminum, plastics, and composites to reduce overall vehicle mass and comply with strict emission reduction targets. The U.S. Corporate Average Fuel Economy (CAFE) standards, which aim to achieve 54.5 mpg by 2025, have intensified the transformation—pushing manufacturers to adopt structural adhesive tapes as a lightweight, high-performance replacement for mechanical fasteners such as rivets and screws.

Structural adhesive tapes are widely used in Body-in-White (BIW) and exterior panel applications, offering not just bonding but also galvanic corrosion protection between dissimilar metals. For example, 3M’s Structural Isolation Tape (SIT2010) provides electrical insulation and abrasion resistance, effectively bonding aluminum to steel while mitigating corrosion risk—a key performance demand in multi-material vehicle assemblies.

Leading adhesive manufacturers are heavily investing in two-component acrylic and epoxy structural bonding systems for high-strength steel and Carbon Fiber Reinforced Polymer (CFRP) components. These solvent-free, fast-curing tapes allow efficient production of hang-on parts like doors, roof skins, and tailgates, contributing directly to weight reduction and enhanced assembly flexibility.

Beyond mechanical performance, the use of adhesive tapes enhances vehicle aesthetics, enabling “invisible bonding” for cleaner exterior finishes by eliminating visible fasteners. The capability is vital for premium electric vehicles (EVs), where seamless body surfaces and aerodynamic efficiency are key to achieving design differentiation and improved range.

The rise of Electric Vehicles (EVs) has revolutionized the role of adhesive tapes, transforming them from simple bonding agents into multi-functional materials integral to vehicle safety, thermal management, and electrical performance. As EV architectures evolve, the complexity of battery modules, electronics, and enclosure assemblies demands adhesives with thermal conductivity, fire resistance, and electromagnetic shielding capabilities.

One of the most critical innovations in the field is the development of thermally conductive acrylic transfer tapes that achieve conductivities up to 2 W/mK (per ASTM D5470). These tapes effectively bond battery cells to cooling plates, maintaining uniform heat distribution across modules and ensuring the optimal battery operating range of 20°C–35°C for performance stability and longevity.

Fire safety and propagation resistance are also top priorities in EV battery design. Adhesive tapes with UL94 V0 certification and ceramifiable silicone rubber formulations provide a dual function—maintaining flexibility at room temperature while transforming into a ceramic-like barrier during thermal runaway events. The innovation prevents cell-to-cell fire propagation, enhancing passenger and vehicle safety.

Additionally, Electromagnetic Interference (EMI) shielding tapes, using metallized fabric or conductive foam backings, are becoming indispensable in EV electronics integration. These tapes provide shielding effectiveness across 450 MHz to 3.8 GHz, protecting sensitive components from high-frequency disruptions, particularly in 5G-enabled vehicles.

Complementing these technologies are dielectric insulation tapes, used to isolate busbars and electrical circuits in high-voltage systems. By offering both insulation and vibration damping, these tapes replace heavier multi-layer insulation systems—simplifying design, improving energy efficiency, and enabling compact battery pack configurations.

The global acceleration of EV production represents one of the largest growth frontiers for automotive adhesive tapes. As major automakers and battery suppliers scale up manufacturing, the need for precision bonding, sealing, and insulation within cell-to-pack (CTP) and cell-to-chassis (CTC) battery designs is surging. Data indicates that the top 10 battery manufacturers account for over 75% of global adhesive tape demand in the segment—underscoring the strategic importance of the market.

Specialized adhesive tapes are being developed to manage challenges such as thermal expansion, chemical resistance, and multi-material adhesion in high-voltage assemblies. Manufacturers are also investing in “Bond & Detach” tape technologies—originally used in consumer electronics for removable battery fixation—which are being adapted for EV applications. These tapes enable reversible bonding, facilitating easier battery repair, recycling, and second-life applications, aligning perfectly with the EV industry’s circular economy objectives.

From a production standpoint, automation compatibility gives adhesive tapes a critical edge. Unlike liquid adhesives requiring curing time, tapes can be applied cleanly via automated vacuum pick-and-place systems, offering higher throughput, precision, and material efficiency. The precision application minimizes waste and ensures consistent bonding performance—a key differentiator for high-volume battery manufacturing facilities.

As automakers commit to carbon neutrality and circular design principles, adhesive tape manufacturers face growing demand for eco-friendly, recyclable, and bio-based bonding solutions that complement new sustainable interior materials. Leading automakers are targeting 50% recycled or bio-based materials in cabin interiors by the end of the decade—spurring innovation in adhesive formulations that can bond effectively to low-surface-energy (LSE) materials like recycled plastics and natural fibers.

Manufacturers are responding by launching Post-Consumer Recycled (PCR) adhesive tapes featuring up to 90% recycled PET backings paired with bio-based acrylic adhesives. These products not only meet OEM sustainability mandates but also align with global circular economy goals. Additionally, the shift to mono-material design—where entire interior assemblies are made from a single polymer type—requires adhesives that are chemically compatible with substrate materials to enable single-stream recycling without contamination.

From a regulatory perspective, low-VOC and low-odor formulations are becoming standard in interior applications to comply with VDA 278 emissions testing and other global IAQ standards. Solvent-free, low-VOC adhesive tapes enhance cabin air quality and reduce the environmental footprint of vehicle production.

Automotive Adhesive Tapes Market Share Insights, 2025-2034

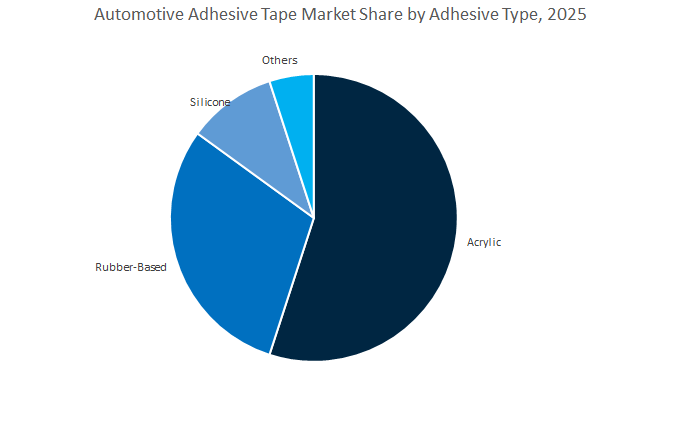

The acrylic adhesive tapes segment dominates the global Automotive Adhesive Tapes industry, accounting for approximately 54.8% of the projected 2025 market share. Acrylic-based systems, particularly Acrylic Foam Tapes (AFTs), have emerged as the industry standard due to their exceptional balance of adhesion strength, temperature stability, UV resistance, and long-term durability. These tapes are extensively used in interior and exterior automotive applications, including trim attachment, nameplates, emblems, body side moldings, and mirror mounting, where performance under stress, vibration, and weathering is critical. Acrylic chemistries outperform other formulations in resisting aging, oxidation, and discoloration, ensuring long service life even in harsh climates. The rise of Electric Vehicles (EVs) has further accelerated their adoption, as acrylic tapes enable lightweighting, vibration damping, and structural bonding without the need for mechanical fasteners, thereby improving aerodynamics and aesthetics. OEMs prefer acrylic tapes because of their compatibility with modern substrates like carbon fiber, aluminum, and high-strength plastics, which are increasingly used to meet energy efficiency and emission goals. As automotive design trends move toward cleaner lines, modular construction, and hybrid materials, the use of acrylic foam and transfer tapes is expected to expand, reaffirming acrylic’s position as the core adhesive chemistry powering the future of automotive bonding technologies.

The rubber-based adhesive tapes segment, holding around 30.4% market share in 2025, remains critical to automotive manufacturing, particularly in sealing, damping, and temporary assembly functions. These tapes—commonly formulated from natural rubber, butyl, or styrenic block copolymers (SBCs)—are prized for their high tack, quick adhesion, and excellent conformability, making them ideal for wire harnessing, NVH (Noise, Vibration, and Harshness) damping sheets, carpet fixing, and weatherstrip sealing. Rubber-based adhesives perform exceptionally well on low-surface-energy substrates, such as polyethylene and polypropylene, which are widely used in automotive interiors. Their resilience to mechanical stress and cost-effectiveness also make them a preferred choice for aftermarket applications and maintenance operations, where flexibility and reworkability are key. However, these tapes typically offer lower temperature and UV resistance compared to acrylics, limiting their use in exterior or high-temperature environments. Nevertheless, innovations such as modified butyl systems and hybrid rubber-acrylic formulations are extending their performance boundaries, enabling broader usage in door sealing, vibration isolation, and underbody protection. The segment continues to benefit from the ongoing demand for comfort enhancement, noise reduction, and sealing efficiency, which are key differentiators in both passenger and commercial vehicles.

The silicone adhesive tapes segment, though smaller in market share, plays a vital niche role in extreme temperature and high-performance applications within the automotive sector. Silicone-based tapes are unmatched when it comes to thermal stability, dielectric strength, and resistance to chemicals, oils, and high voltages, making them indispensable in engine compartments, battery packs for EVs, exhaust systems, and high-voltage electrical insulation. They maintain adhesion and flexibility across an exceptionally wide temperature range, typically from -60°C to 260°C, a property not achievable with acrylic or rubber systems. As electric and hybrid vehicles become mainstream, silicone tapes are witnessing increasing adoption for thermal management, EMI (Electromagnetic Interference) shielding, and wire harness wrapping in high-heat environments. Their use in battery module insulation and safety sealing has also surged, driven by stricter regulations on EV battery safety. Though silicone adhesives are higher in cost, their long-term performance, stability, and compatibility with sensitive electronic systems make them indispensable in premium and critical automotive systems. This segment is projected to experience steady growth through 2034, supported by the rapid expansion of the EV ecosystem, connected vehicles, and autonomous driving technologies, all of which demand advanced material solutions.

The Original Equipment Manufacturers (OEMs) segment dominates the global Automotive Adhesive Tapes market, capturing an estimated 70.6% market share in 2025. OEMs rely heavily on high-performance, pre-certified adhesive tapes that meet stringent specifications for durability, environmental resistance, and manufacturing efficiency. These tapes are integral to modern automotive assembly lines, where they replace mechanical fasteners to reduce vehicle weight, improve aerodynamics, and enhance aesthetics. OEM applications span trim attachment, body panel bonding, weatherproof sealing, noise reduction, and battery insulation. The transition toward electric and hybrid vehicles is a major catalyst for this segment, as OEMs increasingly use advanced tapes in battery pack assembly, cell wrapping, and thermal management. Furthermore, the growing demand for lightweight materials and flexible bonding solutions has led to the adoption of double-sided, acrylic foam, and pressure-sensitive tapes in lieu of welding or riveting. Automotive design evolution—favoring modular assemblies, advanced electronics, and high-performance materials—has positioned adhesive tapes as a strategic enabler of innovation and assembly line optimization. OEM partnerships with tape manufacturers have intensified, with co-development projects focusing on next-generation bonding technologies that meet the industry’s sustainability, recyclability, and emissions reduction targets.

The aftermarket segment, accounting for 29.4% of the global share, represents a dynamic and resilient channel characterized by steady replacement, repair, and customization demand. This segment includes collision repair, vehicle refurbishment, customization, and maintenance applications, making it vital for the lifecycle performance of vehicles. Aftermarket adhesive tapes are designed for ease of use, broad substrate compatibility, and quick adhesion, catering to repair technicians, body shops, and end consumers. Common uses include emblem replacement, weatherstrip repair, vibration damping, interior trim fixing, and soundproofing. The growth of the DIY automotive repair culture, particularly in North America and Europe, has further stimulated this segment, with online and retail channels expanding accessibility to premium-grade tapes. Moreover, the aging vehicle fleet and rising global car ownership ensure consistent aftermarket activity. Compared to OEMs, the aftermarket emphasizes product versatility, packaging convenience, and multi-purpose use, driving innovation in consumer-friendly formulations and pre-cut formats. Additionally, emerging EV service markets are beginning to demand thermal and insulation tape solutions for maintenance and retrofit purposes, presenting new growth avenues for adhesive tape suppliers in this segment.

The Global Automotive Adhesive Tapes Market is consolidated among a few high-innovation leaders — including 3M, tesa SE, Nitto Denko, Avery Dennison, and Scapa Group — each leveraging deep material science expertise, regional production bases, and automation-compatible product portfolios. Their collective focus centers on EV integration, sustainability compliance, high-performance acrylic systems, and digital assembly technologies.

3M remains the global benchmark for VHB™ (Very High Bond) Tapes, offering superior durability, UV resistance, and solvent stability. Its VHB acrylic foam technology provides long-term adhesion under dynamic stress, serving critical roles in sunroof, spoiler, and emblem bonding. In Q4 2025, the company reaffirmed its commitment to eliminate PFAS by 2025, signaling a strong sustainability transformation. 3M’s focus on EV battery assembly—including thermal runaway protection and structural sealing tapes—positions it as a leader in the shift toward next-generation electric vehicles. Leveraging Microreplication and Precision Coating platforms, 3M also pioneers functional tapes for display privacy and interior electronics, strengthening its dominance in automotive adhesives.

tesa SE is a key innovator in viscoelastic and structural foam tapes through its tesa® ACXplus series, providing superior load-bearing strength and viscoelastic recovery for multi-material bonding. Its tesa® 6308 line enables primerless adhesion on low surface energy substrates, improving OEM assembly efficiency and reducing cycle time. Designed for global vehicle platforms, tesa’s adhesives maintain adhesion down to −40°C, ensuring durability under harsh climatic conditions. The company also leads in fire safety compliance, with multiple product lines certified to UL94 and FMVSS 302 standards, making it a preferred partner for interior component bonding in headliners, dashboards, and control panels.

Nitto Denko dominates the automotive electrical and electronics tape segment, offering double-sided and ultra-thin vinyl tapes like its No. 2117TVH series for wiring harness bundling and component insulation. The company’s portfolio spans heat-resistant and flame-retardant tapes designed for car electronics and NEV (new energy vehicle) systems. Nitto’s focus on fluoroplastic-based NITOFLON™ films enhances chemical and thermal resistance in EV power modules, while its Fiber PSA technology introduces next-generation flexible bonding solutions for autonomous vehicle interiors and display installations. Ongoing expansion of its thermal transfer systems underscores its leadership in electrical and lightweighting applications.

Avery Dennison focuses on sustainable PSA solutions and specialty adhesive films for interior assembly, vehicle wraps, and graphic applications. Its recyclable and compostable tapes address growing global demand for end-of-life vehicle recyclability. Avery’s high-performance weather-resistant tapes are widely adopted in OEM badging and protective film applications, offering long-term UV stability and surface protection. The integration of digital printing and custom die-cutting processes allows Avery to deliver precision-engineered tape geometries for modern vehicle aesthetics and complex structural surfaces.

Scapa Group excels in technical tapes featuring foam, film, and fabric carriers designed for NVH damping, body panel sealing, and interior trim bonding. Its low-VOC formulations meet strict automotive environmental standards, while products deliver exceptional abrasion resistance and durability in harsh operating conditions. Scapa’s custom-engineered acoustic and sealing tapes are used extensively in dashboard, door panel, and headliner assemblies, optimizing both noise reduction and assembly consistency.

China continues to dominate the global Automotive Adhesive Tapes market due to its massive EV production capacity and policy-backed industrial expansion. Government initiatives promoting electric vehicle (EV) battery production and localization of material supply chains are directly fueling demand for thermal management and dielectric insulation tapes used in battery assembly.

Chinese adhesive tape manufacturers are advancing low-VOC acrylic and silicone tape formulations to comply with tightening interior air quality standards. The new products are essential for automakers aiming to meet China’s evolving environmental regulations, particularly in vehicle interiors and HVAC systems.

High-performance Acrylic Foam Tapes (AFTs) have become a standard solution for spoilers, rocker panels, and emblem attachment on SUVs and New Energy Vehicles (NEVs). Meanwhile, increasing adoption of fire-retardant and lightweight bonding tapes for cell-to-cell bonding within battery modules is transforming EV safety and thermal reliability.

Recent capacity expansions by global brands — such as tesa SE’s new Southeast Asia facility supporting China’s supply chain — demonstrate a clear regional commitment to meet local automotive adhesive demand. The country’s strategic focus on lightweighting and adhesive-based structural bonding underscores its role as a technology leader in automotive manufacturing efficiency.

Germany stands as the European hub for premium automotive adhesive innovations, with companies such as Lohmann and tesa SE spearheading R&D in multifunctional adhesive tapes. The advanced solutions integrate thermal, electrical, and mechanical bonding properties, catering to high-end EVs and autonomous vehicles.

German manufacturers are pioneering solvent-free and water-based adhesive systems in line with EU environmental policies. The systems are critical for automotive interior and NVH (Noise, Vibration, Harshness) management, replacing solvent-based tapes with sustainable yet high-performance alternatives.

A notable trend in the country is the integration of automated tape dispensing systems across OEM assembly lines, ensuring precision in structural bonding for sensor mounts, Lidar and Radar units, and LED lighting systems. Additionally, polypropylene (PP) and PET-backed tapes are being adopted for wire harness bundling and heat protection in modern powertrains and EV battery housings.

Germany’s strong regulatory compliance, combined with its material science leadership, keeps it at the forefront of innovation in aerospace-grade adhesives adapted for automotive precision manufacturing.

The United States Automotive Adhesive Tapes industry is witnessing rapid transformation, propelled by EV expansion, sustainability regulations, and factory modernization. Major adhesive giants, including 3M and Avery Dennison, are innovating thermal management and dielectric insulation tapes to meet the technical demands of large-format EV battery modules.

The U.S. government’s push for domestic EV production and energy efficiency is driving investments in localized adhesive manufacturing. For instance, substantial new plant developments across Southern states are strengthening regional supply of pressure-sensitive adhesive (PSA) tapes for truck and SUV assembly lines.

Recent product innovations include flexible circuit protection tapes designed for ADAS (Advanced Driver Assistance Systems) and high-performance acrylic foam tapes for fender flare and exterior trim bonding. Meanwhile, the Environmental Protection Agency’s (EPA) updated VOC standards (effective 2025) have accelerated the transition to low-emission adhesives.

U.S. automotive manufacturers prioritize high durability, process efficiency, and automation-ready adhesive systems, reinforcing the country’s dominance in industrial-grade automotive tape technology.

Japan remains a global leader in precision adhesive engineering, driven by its world-class automotive, robotics, and electronics manufacturing ecosystems. Companies such as Nitto Denko and Lintec Corporation continue to advance ultra-thin, high-strength non-woven and PET-backed tapes for miniaturized electronic components used in smart vehicles.

A major innovation area includes high-temperature silicone and rubber-based adhesive tapes developed for powertrain and exhaust system applications. Japan’s automakers also rely on adhesive-based gasketing solutions for battery housings, hydrogen fuel cells, and thermal insulation systems in next-generation zero-emission vehicles.

Government-backed R&D programs are encouraging the development of recyclable and eco-compliant adhesive materials to align with End-of-Life Vehicle (ELV) recycling standards. Additionally, Japanese OEMs are heavily investing in automated precision die-cutting and liner release technologies to streamline robotic tape application in modern assembly lines.

Japan’s balance of micro-level precision and macro-scale sustainability keeps its adhesive sector at the forefront of global automotive innovation.

South Korea has established itself as a technological hub for advanced automotive adhesives, supporting both its domestic automakers and global electronics industries. The country’s rapid shift toward connected, electric, and digital vehicles is driving strong demand for thermal management, vibration damping, and display mounting adhesive tapes.

Local manufacturers are leading in double-sided adhesive tape applications for curved display screens and integrated dashboards, a key differentiator in premium Korean vehicle interiors. Moreover, polyurethane (PU) and acrylic foam tapes are increasingly used in EV structural bonding and battery module assembly to improve vibration resistance and thermal stability.

Government initiatives are fostering R&D partnerships between adhesive companies and major automakers to enhance local sourcing of high-performance materials. Additionally, low-outgassing and ceramic-filled thermal tapes are being developed to prevent condensation in headlights and optimize battery cooling systems — an innovation critical for EV battery longevity and safety.

Mexico continues to expand its role in the North American Automotive Adhesive Tapes supply chain, supported by significant Foreign Direct Investment (FDI) in vehicle manufacturing. As one of the top exporters under the USMCA framework, Mexico’s automotive adhesive demand is heavily influenced by both U.S. and Canadian OEM production cycles.

The country’s focus lies in cost-effective yet performance-compliant adhesive tapes for high-volume vehicle assembly and aftermarket applications. Local converters and distributors are expanding slitting and die-cutting facilities to deliver customized adhesive components to Tier 1 suppliers.

Growing demand for anti-abrasion cloth tapes for wire harness protection and noise-dampening solutions reflects Mexico’s modernization of assembly practices. Furthermore, adoption of water-based and hot-melt adhesive technologies is increasing as the nation aligns with North American environmental standards.

India’s Automotive Adhesive Tapes market is witnessing explosive growth, fueled by the “Make in India” and Production-Linked Incentive (PLI) programs. Domestic tape producers and foreign entrants are scaling local manufacturing to meet the country’s fast-growing vehicle production demands.

The Indian market’s focus on affordability has led to cost-efficient PP and PVC masking and surface protection tapes designed for painting, assembly, and finishing in high-volume vehicle production. Meanwhile, foreign tape manufacturers are introducing high-initial-tack acrylic foam tapes for premium and export-oriented vehicle models.

Demand is rising across two-wheeler and commercial vehicle segments, where adhesive tapes are increasingly replacing fasteners in applications such as emblem bonding, mirror attachment, and wire harnessing. With automakers upgrading assembly lines for tape-based automation, India is evolving into a key global sourcing hub for automotive adhesive solutions.

Automotive Adhesive Tapes Market Report Scope

Automotive Adhesive Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.2 Billion

|

|

Market Size (2034)

|

$19.2 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Adhesive Type (Acrylic, Rubber-Based, Silicone, Others), By Backing Material (Polyvinyl Chloride, Polypropylene, Foam, Paper/Film, Cloth/Fabric, Metal Foil), By Application (Automotive Interior, Automotive Exterior, Engine & Powertrain, Electrical & Electronics / EV Battery), By End-Use Channel (OEMs, Aftermarket

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, tesa SE, Nitto Denko Corporation, Avery Dennison Corporation, Lohmann GmbH & Co.KG, Lintec Corporation, Henkel AG & Co. KGaA, Sika AG, Saint-Gobain S.A., Scapa Group PLC, Intertape Polymer Group, Adhesives Research, Inc., Coroplast Tape Corporation, Shurtape Technologies, LLC, Maxell, Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Adhesive Type

- Acrylic

- Rubber-Based

- Silicone

- Others

By Backing Material

- Polyvinyl Chloride

- Polypropylene

- Foam

- Paper/Film

- Cloth/Fabric

- Metal Foil

By Application

- Automotive Interior

- Automotive Exterior

- Engine & Powertrain

- Electrical & Electronics / EV Battery

By End-Use Channel

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- 3M Company

- tesa SE

- Nitto Denko Corporation

- Avery Dennison Corporation

- Lohmann GmbH & Co.KG

- Lintec Corporation

- Henkel AG & Co. KGaA

- Sika AG

- Saint-Gobain S.A.

- Scapa Group PLC

- Intertape Polymer Group

- Adhesives Research, Inc.

- Coroplast Tape Corporation

- Shurtape Technologies, LLC

- Maxell, Ltd.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates how electrification, NVH optimization, and lightweighting are reshaping the Automotive Adhesive Tapes value chain—linking material science to manufacturing economics and in-use reliability. Our analysis reviews thermal envelopes, primerless LSE bonding, EMI/thermal needs in EV packs, and digital bonding validation to quantify line speed, FPY, and warranty risk. It highlights acrylic foam/VHB-class structural PSAs for exterior panels, ultra-thin harness wraps, and acoustic tapes that upgrade cabin quietness while meeting RoHS2/REACH expectations. Mapping cost-to-serve and profit pools across OEM and aftermarket, we benchmark leaders on PFAS-free roadmaps, recyclability, and automation readiness. Incorporating recent technology breakthroughs in high-temperature acrylics, flame-retardant interiors, and detachable EV battery tapes, this report is an essential resource for engineering, sourcing, and operations teams seeking faster assembly, lower mass, and compliant designs.

Scope Includes

- By Adhesive Type: Acrylic; Rubber-Based; Silicone; Others

- By Backing Material: Polyvinyl Chloride; Polypropylene; Foam; Paper/Film; Cloth/Fabric; Metal Foil

- By Application: Automotive Interior; Automotive Exterior; Engine & Powertrain; Electrical & Electronics / EV Battery

- By End-Use Channel: OEMs; Aftermarket

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Horizon: Historic 2021–2024 and forecasts 2025–2034.

- Companies: 15+ company analysis/profiles.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.