Blow Molded Plastic Bottles Market Overview: Sustainability and E-commerce Driving Growth

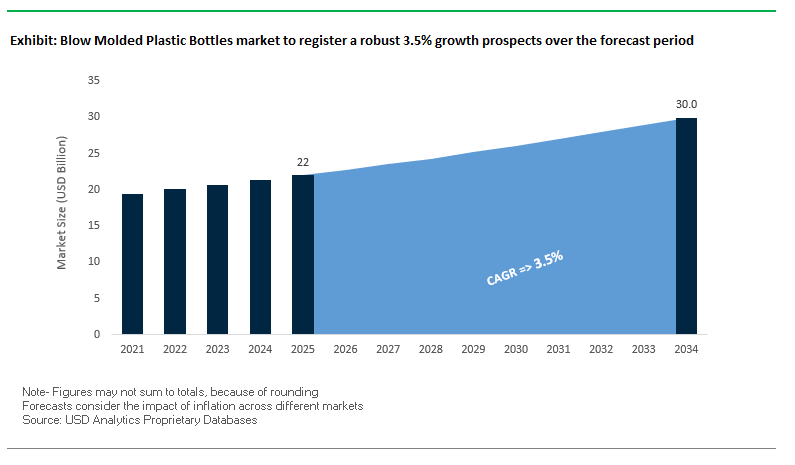

The blow molded plastic bottles market is projected to grow from USD 22 billion in 2025 to USD 30 billion by 2034, at a CAGR of 3.5%. This industry is an essential pillar of the global packaging ecosystem, known for its versatility, cost efficiency, and durability. However, the sector is undergoing a major transformation as sustainability, lightweighting, and e-commerce resilience become top priorities for manufacturers and brand owners. For buyers and industry professionals, the key questions revolve around how effectively packaging suppliers can integrate recycled content, meet global sustainability regulations, and adapt to the growing e-commerce channel without compromising durability or design versatility.

Key Insights Driving the Blow Molded Plastic Bottles Market

- Extrusion blow molding dominates as the most cost-efficient method, widely used for industrial, household, and personal care bottles.

- Over 30% reduction in material use has been achieved through lightweighting innovations, reducing both costs and carbon footprints.

- Recycled content is a priority, with companies producing bottles using up to 100% rPET to meet regulations and consumer expectations.

- E-commerce growth boosts demand for durable, tamper-evident bottles that can withstand long-distance shipping and handling.

Market Analysis: Recent Developments in the Blow Molded Plastic Bottles Industry

The blow molded plastic bottles industry has seen rapid change over the past year, marked by regulatory shifts, sustainability breakthroughs, and strategic consolidations. In August 2025, an industry journal reported rising adoption of Injection Stretch Blow Molding (ISBM), particularly in pharmaceutical and personal care segments, where smaller high-performance bottles are in demand. In July 2025, a leading beverage company announced a transition of part of its water portfolio to ultra-lightweight bottles, co-developed with a blow molding partner to reduce material usage and carbon impact.

Consolidation is also reshaping the competitive dynamics. The Amcor–Berry Global merger in June 2025 created one of the most powerful packaging giants, combining resources to accelerate innovation in sustainable and recyclable plastic bottles. On the materials side, April 2025 saw the publication of a key study in a materials science journal demonstrating the potential of bio-based resins derived from sugarcane for blow molding, positioning them as credible alternatives to petroleum-based plastics. Similarly, in March 2025, a European manufacturer invested heavily in R&D to advance tethered caps and closures, aligning with upcoming EU regulations mandating tethered closures on plastic bottles.

Technology-driven innovation remains central. Plastipak Holdings was featured in February 2025 for its G.E.M. PAK Wheel platform, enabling high-efficiency production of diverse bottle designs. Meanwhile, EU single-use plastics regulations in January 2025 created a regulatory tailwind, spurring investments in recyclable and reusable designs. On the product innovation front, in November 2024, a global food brand launched sauces in multi-layered blow molded bottles with advanced barrier properties, extending shelf life while remaining recyclable. Together, these developments signal a market that is strategically aligned with sustainability, regulatory compliance, and advanced consumer packaging needs.

Emerging Trends and Opportunities Defining the Blow Molded Plastic Bottles Market

Accelerated Integration of Post-Consumer Recycled (PCR) Content Driven by Brand Mandates

One of the most transformative shifts in the blow molded plastic bottles market is the rapid integration of post-consumer recycled (PCR) content, driven by both regulatory frameworks and bold corporate sustainability mandates. Global beverage and consumer goods companies are setting ambitious targets to reduce virgin plastic dependency and align with circular economy goals. The Coca-Cola Company, for example, has committed to using 35–40% recycled content in primary packaging, with a longer-term global objective of 30–35% recycled plastic by 2035. Such mandates force blow molding suppliers to expand resin processing capabilities and secure reliable streams of food-grade rPET and rHDPE. At the same time, smaller innovators are also shaping the market. In September 2025, Great Galleon Ventures Limited relaunched its V21 brand using 100% rPET bottles, saving 5.7 million liters of water and preventing 138.7 tonnes of CO₂ emissions per cycle. This highlights how recycled content adoption directly delivers measurable environmental and economic benefits. Regulatory pressure is equally decisive: India’s FSSAI 2025 guidelines for food-contact rPET mandate not only strict quality standards but also percentage labeling of recycled content on packaging, effectively turning recyclability into a consumer-facing metric. Together, these forces are making PCR integration not an optional initiative but a competitive necessity for bottle producers worldwide.

Lightweighting and Advanced Design Optimization to Reduce Material Use

Lightweighting has become a cornerstone strategy in the blow molded bottles market, enabling brands to simultaneously cut costs, reduce emissions, and enhance sustainability profiles. Advances in injection stretch blow molding (ISBM) technology allow manufacturers to achieve thinner wall structures and optimized material distribution while maintaining bottle durability. For instance, Coca-Cola Europacific Partners reduced the weight of its 500ml PET bottles from 28.9g to just 19.9g—a 30% reduction since 2008. More recently, the introduction of an ultra-light neck design, trimming another 1g of plastic per unit, is expected to eliminate 6,800 tonnes of plastic annually by the end of 2024. Material science also supports this trend, with the use of nucleating agents and nanocomposites improving polymer strength-to-weight ratios, enabling further material reduction. The environmental impact is equally profound: lighter bottles reduce shipping costs and lower transport emissions, which is vital for global brands distributing millions of units. Lightweighting not only aligns with corporate ESG benchmarks but also enhances competitiveness in cost-sensitive emerging markets, making it a dual advantage for bottle producers.

Development of Monomaterial and Easily Recyclable Bottle Structures

A pressing opportunity for the blow molded bottle industry lies in eliminating multi-material complexity, which currently hampers recycling efficiency. Traditional bottles often combine PET bodies with PP caps and non-removable labels, creating contamination issues in recycling streams. Researchers at IIT-Bhilai have filed a patent for a chemical recycling method capable of depolymerizing PET bottles and caps simultaneously, eliminating the need for material separation. Industry players are also prioritizing monomaterial solutions, where the cap, body, and label belong to the same polymer family. For example, an all-PET bottle with wash-off PET labels ensures higher recycling yields. This shift is reinforced by the EU Packaging and Packaging Waste Regulation (PPWR), which requires all packaging to be recyclable by 2030, compelling manufacturers to reengineer bottles for circularity. Brands adopting monomaterial structures gain competitive advantage not only by meeting compliance but also by signaling eco-consciousness to consumers. With regulatory enforcement and consumer demand converging, monomaterial bottles represent one of the most commercially viable opportunities for the future.

Adoption of Industry 4.0 and AI for Predictive Quality Control and Efficiency

The integration of Industry 4.0 technologies is redefining blow molding operations, turning factories into smart, data-driven production hubs. IoT sensors embedded in molding machines provide real-time monitoring of pressure, temperature, and cycle times, allowing predictive analytics to anticipate breakdowns before they occur. This transition from reactive to predictive maintenance reduces unplanned downtime, improves Overall Equipment Effectiveness (OEE), and extends machine lifecycles. At the same time, AI-driven vision systems are transforming quality control, inspecting every single bottle at line speed and automatically rejecting defective units a dramatic improvement over random spot checks. Energy optimization is another area where AI delivers measurable results. By dynamically adjusting machine settings, companies can reduce energy consumption, a critical advantage for an industry facing scrutiny over carbon footprints. For manufacturers, these technologies unlock efficiency gains while simultaneously meeting ESG-driven cost and sustainability goals, positioning AI-enabled factories as the new competitive benchmark in the blow molded bottle industry.

Competitive Landscape: Global Leaders in Blow Molded Plastic Bottles

The blow molded plastic bottles industry is led by a mix of global packaging giants and innovation-driven specialists. Their competitive edge lies in scale, R&D investments, and alignment with circular economy principles, as well as the ability to offer tailored, brand-centric solutions.

Amcor Rigid Packaging focuses on sustainable bottle innovations

Amcor is a global leader in rigid plastics, with a diverse portfolio spanning beverage, food, home care, and personal care bottles. The company is pioneering designs with higher PCR content and innovations such as embossed logos to replace labels, improving recyclability. Its global footprint and customer-collaborative approach allow Amcor to deliver customized, sustainable packaging at scale.

Silgan Holdings delivers customized rigid plastic packaging solutions

Silgan specializes in custom-engineered containers, widely used in food and personal care products. With 22 plants across North America, it has strong regional presence and expertise in PCR and bio-resins. Silgan’s membership in the Ellen MacArthur Foundation’s New Plastics Economy and partnerships with The Recycling Partnership underscore its commitment to building a circular economy.

Berry Global drives innovation with circular packaging technologies

Berry Global manufactures blow molded bottles across food, beverage, healthcare, and personal care markets. In a landmark collaboration, the company introduced Prevented Ocean Plastic (POP) bottles, showcasing its commitment to reducing marine plastic waste. Its B Circular Range focuses on designs that enhance recyclability, while its ISBM and blow molding expertise enables high-performance custom packaging for global brands.

Plastipak Holdings pioneers lightweighting and ePET technologies

Plastipak is a global innovator in lightweighting technologies, with its G.E.M. PAK Wheel enabling high-speed, efficient production of multiple bottle formats. Its extensive patent portfolio and R&D strength give it an edge in conversion technologies, including ePET bottles that improve performance and sustainability. Plastipak’s strategy focuses on recyclable and recycled-content packaging, aligning with global carbon reduction goals.

Alpla Group expands sustainable packaging and recycling capacity

Alpla is a leading international player with expertise in blow molding, caps, and injection-molded parts. Its standout innovation, “The Simple One,” delivers up to 60% weight reduction in HDPE bottles. With 13 recycling plants and annual investments of €50 million, Alpla is expanding its recycling operations, strengthening its role as a sustainability-focused packaging leader.

Graham Packaging advances reusable and refillable PET bottle solutions

Graham Packaging has built its reputation on co-creating sustainable packaging with customers. Recognized by the Sustainable Packaging Coalition, its REFPET refillable PET containers now achieve 25 reuse cycles, up from 17 previously. Its innovation focus extends to digital technologies like AR and VR to optimize design, maintenance, and faster time-to-market, offering clients both sustainability and efficiency.

Blow Molded Plastic Bottles market Share Insights

Market Share by Material Type in the Blow Molded Plastic Bottles Industry

Polyethylene terephthalate (PET) leads the blow molded plastic bottles market with a 48% share in 2025, underscoring its unmatched dominance in the food and beverage sector. PET’s crystal-clear transparency, superior gas barrier properties, and high strength-to-weight ratio make it the material of choice for bottled water, carbonated soft drinks, juices, and edible oils. Its position is reinforced by well-developed global recycling streams, making PET the most circular of the blow molding resins, though it continues to face scrutiny over sustainability and microplastic concerns. High-density polyethylene (HDPE) holds a substantial 35% share, positioning itself as the industry’s chemical-resistant workhorse. Its durability, opacity, and cost-effectiveness make it the standard resin for milk jugs, household chemicals, and personal care bottles. HDPE’s versatility ensures strong adoption across high-volume consumer applications where product safety and shelf stability are critical. Polypropylene (PP) serves as the specialist resin, particularly for hot-fill and thermally sensitive applications. It is widely used in medicine bottles, syrup containers, and yogurt packs, where its thermal resistance and ability to form living hinges in flip-top caps create functional advantages. Low-density polyethylene (LDPE) and other resins, including PVC, account for a minimal share of the market. LDPE’s role is confined to squeeze bottles due to its flexibility, while PVC is rapidly declining because of health and environmental concerns, surviving only in a handful of specialized technical or medical applications.

Market Share by End-Use Industry in the Blow Molded Plastic Bottles Industry

Food and beverage dominates the global blow molded plastic bottles market with 55% of demand in 2025, making it the largest and most influential end-use industry. This segment’s leadership stems from massive consumption volumes of bottled water, carbonated beverages, cooking oils, and dairy, which rely heavily on PET and HDPE. As global hydration and convenience trends continue to expand, the food and beverage sector remains the cornerstone of demand for blow molded bottles. Personal care and cosmetics account for 20% of the market, representing a high-value segment where aesthetics and brand differentiation are paramount. Bottles in this category rely on PET for premium clarity, HDPE for durability, and PP for flexible dispensing formats, with constant innovation in shapes, finishes, and decorative elements to drive shelf appeal. Household chemicals form a stable anchor segment, relying primarily on HDPE packaging for its superior chemical resistance and opacity. This category, which includes bleach, detergents, and cleaning products, emphasizes performance and safety over aesthetics, making cost and durability the key drivers. Pharmaceutical applications, while smaller in overall volume, hold significant strategic value due to strict regulatory requirements. Packaging for prescription drugs and over-the-counter medicines demands purity, stability, and features like child resistance, supporting premium adoption of PP and HDPE bottles. Other industrial applications, including automotive fluids and lubricants, round out the market. These niche uses prioritize extreme durability and chemical resistance, reinforcing HDPE’s role as the resin of choice for heavy-duty applications. Collectively, these end-use industries reflect how blow molded plastic bottles remain indispensable across diverse global sectors, balancing cost, performance, and brand-driven packaging needs.

United States: Lightweighting, Automation, and Diversification Redefining Blow Molded Plastic Bottles Market

The blow molded plastic bottles market in the United States is undergoing a major transformation driven by sustainability, advanced automation, and diversification into high-value industries. A central focus is lightweighting and the integration of recycled content, with leading beverage brands such as The Coca-Cola Company introducing ultra-lightweight PET bottle designs that cut costs, reduce environmental footprint, and enhance supply chain efficiency. This sustainability-driven innovation is complemented by rising adoption of automation and all-electric clamping systems that reduce energy consumption while ensuring precision in bottle manufacturing.

The U.S. market is also diversifying rapidly beyond food and beverages, with blow-molded plastics seeing strong adoption in automotive applications, particularly in electric vehicles (EVs), where lightweight components support efficiency standards. Additionally, the surge in demand for hand sanitizer, disinfectant, and household cleaner bottles has strengthened the market’s role in essential industries. With expansion of production facilities across the country, manufacturers are also targeting premium product packaging through advanced processes like injection stretch blow molding, which deliver high-clarity, aesthetically superior bottles for premium beverages and personal care.

China: Sustainability and Advanced Blow Molding Fueling Market Growth

China’s blow molded plastic bottles market is being shaped by a powerful combination of industrial growth, technological innovation, and government-backed sustainability initiatives. The country’s booming automotive, packaging, and construction sectors are driving robust demand, especially for lightweight blow-molded components that improve vehicle fuel efficiency. Technological advancements such as multi-layer and 3D blow molding are becoming mainstream, enabling higher material efficiency, improved barrier properties, and reduced production costs.

The Chinese government’s strong emphasis on recyclable and biodegradable plastics is accelerating the use of post-consumer recycled (PCR) content in bottle manufacturing. This aligns with the rapid expansion of e-commerce, which requires durable, lightweight, and cost-effective packaging solutions that blow-molded bottles can efficiently provide. With domestic players scaling up capacity to meet demand and reduce import dependency, China is positioning itself as a global leader in blow molding plastics innovation and mass-market adoption.

Germany: Engineering Excellence and Circular Economy Driving Market Evolution

Germany stands out as a global hub for blow molding machinery and engineering excellence, setting the benchmark for high-precision, automated production systems. German manufacturers are at the forefront of integrating IoT-enabled automation and advanced servo-electric systems, which significantly reduce energy usage while maintaining top-tier product quality. This focus on energy efficiency aligns closely with the country’s sustainability goals and its leadership in the European circular economy framework.

Germany’s strict regulations on plastic waste and recycling are fostering innovation in recyclable blow molded products and pushing companies to incorporate higher percentages of recycled content. The market is also benefiting from strong demand in packaging and automotive industries, where lightweighting and sustainable material use are top priorities. As a result, Germany’s blow molded plastic bottles sector is not only leading in production efficiency but also setting global standards for eco-friendly manufacturing and recyclability.

Brazil: Agricultural Resources Powering Bio-Based Blow Molded Plastics

Brazil’s blow molded plastic bottles market is gaining traction due to its abundant bio-based raw materials, such as sugarcane, which provide a competitive edge in producing sustainable plastics. The country’s robust agricultural sector has enabled manufacturers to explore bio-based resins, supporting the transition from fossil-based to renewable packaging solutions. Organizations such as Abiplast are leading efforts to promote circular economy principles and integrate post-consumer recycled (PCR) plastics into bottle production, making Brazil an emerging player in sustainable packaging.

The market is also witnessing increased demand from both packaging and automotive sectors, with food and beverage brands prioritizing recyclable bottles and automakers incorporating lightweight blow molded components to improve fuel efficiency. Additionally, Brazilian research institutions like EMBRAPA are pioneering innovations in agricultural waste conversion, using banana peels and other by-products to produce high-performance films and bottles with UV-blocking and antioxidant properties, suitable for food preservation and specialty packaging.

India: Government Policy, Manufacturing Expansion, and Sustainability Defining Market Growth

India’s blow molded plastic bottles market is expanding rapidly, supported by rising demand in the packaging, healthcare, and automotive industries. The food and beverage sector remains a major driver, with extensive reliance on PET and HDPE bottles for water, soft drinks, edible oils, and dairy products. The government’s “Make in India” initiative and growing foreign direct investment (FDI) are further boosting domestic manufacturing capabilities, making India an attractive hub for both local and international players.

At the same time, India is embracing modern blow molding technologies, including extrusion and injection stretch blow molding, to produce complex, high-quality bottles at scale. With increasing consumer awareness around plastic pollution, manufacturers are incorporating recycled materials and adopting energy-efficient production methods to align with sustainability mandates. The rapid adoption of biodegradable resins and recycling-friendly designs is positioning India as a fast-growing and environmentally conscious market for blow molded plastic bottles.

Japan: Precision, Lightweighting, and Advanced Manufacturing Defining the Market

Japan’s blow molded plastic bottles market is driven by its reputation for technological innovation and high-precision manufacturing. Companies like Aoki Technical Laboratory are pioneering single-stage molding technology, which significantly improves energy efficiency, reduces cycle times, and enhances production consistency. This technological edge allows Japanese manufacturers to meet the market’s demand for high-quality, precision-engineered bottles across premium beverages, pharmaceuticals, and personal care applications.

Lightweighting is a critical priority in Japan, especially for PET bottles, where manufacturers are achieving thinner walls without compromising durability or product safety. This supports both cost reduction and sustainability goals, while also reducing carbon emissions from transportation. Combined with the country’s focus on circular economy policies, Japan’s blow molded plastics industry is positioning itself as a global benchmark for eco-friendly, high-performance, and precision-driven bottle manufacturing.

Blow Molded Plastic Bottles Market Report Scope

Blow Molded Plastic Bottles market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$22 Billion

|

|

Market Size (2034)

|

$30 Billion

|

|

Market Growth Rate

|

3.5%

|

|

Segments

|

By Material Type (Polyethylene Terephthalate, High-Density Polyethylene, Low-Density Polyethylene, Polypropylene, Polyvinyl Chloride, Others), By Technology (Extrusion Blow Molding, Injection Blow Molding, Injection Stretch Blow Molding, Other Technologies), By End-Use Industry (Food & Beverage, Personal Care & Cosmetics, Household Chemicals, Automotive, Pharmaceuticals, Industrial, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Inc., Silgan Holdings Inc., Greiner Packaging International GmbH, Alpha Packaging, Resilux NV, Avery Dennison Corporation, Graham Packaging Company, Plastic Bottle Corporation, Container Corporation of Canada, Sonoco Products Company, ALPLA-Werke Alwin Lehner GmbH & Co KG, Consolidated Container Company, Plastipak Holdings, Inc., Kautex Maschinenbau GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Blow Molded Plastic Bottles Market Segmentation

By Material Type

- Polyethylene Terephthalate

- High-Density Polyethylene

- Low-Density Polyethylene

- Polypropylene

- Polyvinyl Chloride

- Others

By Technology

- Extrusion Blow Molding

- Injection Blow Molding

- Injection Stretch Blow Molding

- Other Technologies

By End-Use Industry

- Food & Beverage

- Personal Care & Cosmetics

- Household Chemicals

- Automotive

- Pharmaceuticals

- Industrial

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Blow Molded Plastic Bottles market

- Amcor plc

- Berry Global Inc.

- Silgan Holdings Inc.

- Greiner Packaging International GmbH

- Alpha Packaging

- Resilux NV

- Avery Dennison Corporation

- Graham Packaging Company

- Plastic Bottle Corporation

- Container Corporation of Canada

- Sonoco Products Company

- ALPLA-Werke Alwin Lehner GmbH & Co KG

- Consolidated Container Company

- Plastipak Holdings, Inc.

- Kautex Maschinenbau GmbH

* List Not Exhaustive

Research Coverage

This USDAnalytics report investigates the global Blow Molded Plastic Bottles market, offering a comprehensive analysis of technological advancements, sustainability-driven innovations, and evolving end-use applications. The study highlights breakthroughs in lightweighting, post-consumer recycled (PCR) integration, monomaterial designs, and Industry 4.0 adoption, providing a critical resource for manufacturers, brand owners, and investors seeking actionable insights. Through in-depth analysis reviews of market dynamics, competitive strategies, and regional developments, this report emphasizes the strategic importance of extrusion, injection, and injection stretch blow molding technologies. USDAnalytics evaluates regulatory drivers, material innovation, and the rapid growth of e-commerce packaging requirements, positioning this report as an essential resource for industry professionals aiming to align with circular economy goals and enhance operational efficiency. The coverage also extends to recent mergers and acquisitions, sustainability mandates, and product innovation trends, equipping stakeholders with a forward-looking perspective to anticipate challenges and capitalize on emerging opportunities.

Scope Highlights

- Segmentation: Material Type (Polyethylene Terephthalate, High-Density Polyethylene, Low-Density Polyethylene, Polypropylene, Polyvinyl Chloride, Others); Technology (Extrusion Blow Molding, Injection Blow Molding, Injection Stretch Blow Molding, Other Technologies); End-Use Industry (Food & Beverage, Personal Care & Cosmetics, Household Chemicals, Automotive, Pharmaceuticals, Industrial, Others).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historical & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Company Coverage: Detailed analysis and profiles of 15+ key players, including Amcor plc, Berry Global Inc., Silgan Holdings Inc., Plastipak Holdings, ALPLA-Werke, and others.

- Key Insights: Focused on sustainability, regulatory compliance, lightweighting, e-commerce resilience, AI-driven quality control, and recyclability optimization.

Methodology

The methodology employed in this USDAnalytics report combines both primary and secondary research to ensure robust, data-driven insights. Primary research includes structured interviews with industry experts, supply chain stakeholders, and leading manufacturers of blow molded plastic bottles to capture current operational practices, innovation trends, and strategic priorities. Secondary research leverages industry journals, company filings, patent databases, trade associations, and government publications to verify market developments, regulatory changes, and material advancements. Quantitative data from 2021 to 2024 is analyzed using statistical models to establish baseline trends, while predictive analytics and scenario modeling are applied to forecast growth, material adoption, and technology penetration through 2034. Competitive benchmarking examines company strategies, mergers and acquisitions, and product innovation to contextualize market positioning. All findings are cross-validated to minimize bias and ensure relevance for decision-makers in packaging, consumer goods, pharmaceuticals, and related sectors.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.