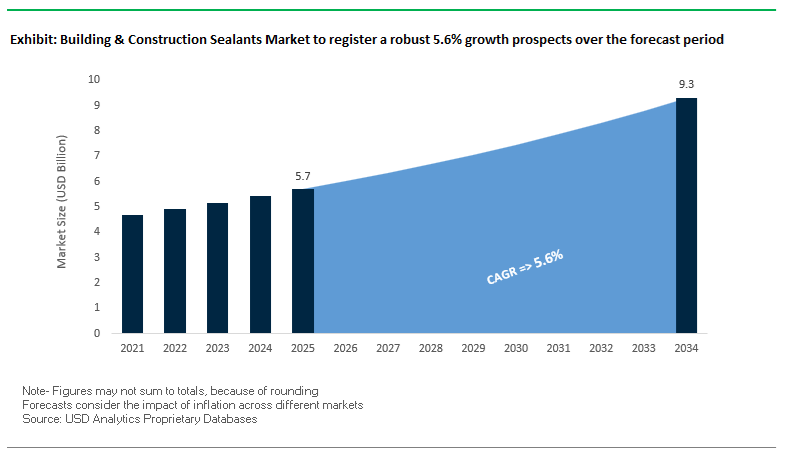

The global building and construction sealants market has become strategically critical as façade engineering, high-rise construction, and infrastructure renewal converge with stricter durability and sustainability expectations. Valued at USD 5.7 billion in 2025 and projected to reach USD 9.3 billion by 2034 at a CAGR of 5.6%, market growth reflects the industry’s dependence on long-life sealing systems that directly influence building safety, energy efficiency, and lifecycle cost. Sealants are no longer peripheral materials; they function as structural and environmental control elements within modern building envelopes, particularly in complex curtain wall, glazing, and expansion joint applications.

The core structural shift reshaping demand is the transition from legacy polysulfide and acrylic sealants toward high-performance silicones and hybrid polymer chemistries. Structural glazing sealants (SSG) based on advanced silicone formulations are routinely qualified for 20-year durability warranties in high-rise façades, reflecting OEM-tested resistance to UV exposure, ozone, moisture ingress, and long-term cyclic loading. These materials maintain elasticity under extreme conditions, accommodating seismic movement, wind-induced deflection, and blast-related strain without cohesive failure—capabilities that conventional sealants cannot sustain over comparable service lives. In parallel, elastomeric and hybrid polymer sealants compliant with ASTM C920 movement classes of ±25% to ±50% have become the design baseline for managing joint displacement caused by thermal cycling and structural settlement in tall and long-span structures.

Material substitution toward silicone and hybrid systems delivers measurable business outcomes for developers, façade contractors, and asset owners. Extended joint service life reduces remediation cycles, while high movement accommodation minimizes façade cracking, water ingress, and energy losses—directly lowering maintenance and operating costs. From a sustainability standpoint, manufacturers such as Dow, Wacker, and Sika are commercializing low-embodied-carbon silicone and hybrid sealants with PAS 2060-certified carbon neutrality, delivering up to a 20× improvement in carbon balance over a building’s operational lifespan compared to conventional alternatives. Over the forecast period, competitive differentiation in the construction sealants market will center on formulation durability, verified environmental credentials, and consistent global supply, as building codes, green certifications, and façade performance standards increasingly link material selection to long-term compliance and asset value preservation.

The building and construction sealants industry is undergoing transformative change as sustainability, automation, and energy efficiency become core priorities for global manufacturers. Strategic investments and regulatory shifts across Europe, North America, and Asia Pacific are driving rapid adoption of bio-based, solvent-free, and hybrid polymer sealants engineered for long service life and minimal environmental impact.

In August 2025, leading home improvement retailers such as Lowe’s and Home Depot executed acquisitions of major building products distributors, reshaping distribution networks and strengthening supply access to sealants, adhesives, and construction chemicals in the Professional Contractor (Pro) segment. This vertical integration strategy is set to streamline procurement for residential and light-commercial builders.

By July 2025, a leading chemical manufacturer introduced a neutral-cure hot-melt silicone sealant tailored for robotic window and door assembly, enabling high-speed, automated glazing operations that improve precision and cut cycle times in fenestration manufacturing. The European Commission (May 2025) further accelerated momentum by updating construction product regulations to prioritize life cycle assessment (LCA) and substance-of-concern phase-outs, compelling manufacturers to reformulate products with low-VOC, solvent-free chemistry.

Infrastructure modernization programs in North America and Asia (March 2025) have also spurred demand for high-modulus polyurethane and polysulfide sealants, designed for expansion joints in bridges, water facilities, and highways. Meanwhile, a January 2025 milestone introduced biomass-derived silicone polymers capable of replacing 100% fossil feedstocks—marking a significant leap toward net-zero construction chemistry.

Additional developments included fire-retardant MS polymer sealants (December 2024) tested under EN 1366-4, suitable for high-safety commercial spaces, and manufacturing capacity expansions in Southeast Asia (November 2024) to meet the surging demand from urbanization-driven housing projects. Research published in October 2024 validated that silicone adhesives’ tensile strength increases under high strain rates, offering critical data for designing blast-resistant façades in high-security architecture.

The building and construction sealants market is rapidly transitioning from traditional high-VOC and single-polymer sealants toward low-VOC, silicone-organic hybrid formulations that meet modern sustainability and regulatory standards. The shift is being catalyzed by tightening global emission regulations, particularly under the European Union’s REACH framework, which restricts the concentration of cyclic siloxanes such as D4, D5, and D6 to below 0.1% by weight for construction applications starting mid-2026. These restrictions have triggered a wave of reformulation across the sealant industry as manufacturers pivot toward environmentally superior silicone-hybrid and silyl-modified polymer (SMP) chemistries that combine the flexibility and weather resistance of silicones with the strong adhesion of polyurethanes—without the associated VOC burden.

The transition aligns with the broader trend toward carbon-neutral construction materials. Many high-performance silicone structural sealants are certified under PAS 2060 carbon neutrality standards, offering a dual advantage of long-term durability and sustainability. Notably, some next-generation silicone formulations are warranted for 20 years of structural integrity in both weatherseal and structural glazing applications, with third-party testing confirming their ability to improve façade carbon efficiency by up to 20 times compared to short-life polymeric alternatives. The demonstrates how eco-compliance and performance can coexist in modern façade engineering.

Further fueling the adoption of low-VOC technologies is the surge in green building certifications, such as LEED, BREEAM, and WELL. These certifications prioritize materials containing fewer than 50 grams per liter (g/L) of VOCs, pushing waterborne and hybrid sealants to the forefront. As governments and developers increasingly target net-zero construction goals, sealant manufacturers that can deliver long-lasting, environmentally compliant, and low-emission solutions are strategically positioned to capture the fastest-growing segment of the $10+ billion global market.

The next generation of building and construction sealants is moving beyond conventional joint sealing to incorporate smart and functional properties that contribute to energy efficiency, building automation, and fire protection. As part of the transformation, sealants are increasingly designed to act as integrated performance layers that support thermal insulation, air sealing, and even structural health monitoring.

The innovation is strongly aligned with the U.S. Department of Energy’s (DOE) research roadmap, which highlights thin insulating materials and embedded sensing systems as key R&D opportunities to enhance building efficiency. Sealants embedded with thermal and sensing functionalities can track joint movement, moisture levels, or temperature variations in real time—capabilities that can drastically improve building maintenance and reduce energy loss over time.

Fire resilience represents another major innovation frontier. Fire-rated silicone sealants are capable of providing up to four hours of certified fire resistance under EN 1366-4 testing standards, while also accommodating up to ±20% joint movement without losing integrity. These materials are crucial for maintaining compartmentalization in high-rise and critical infrastructure applications. Combined with intumescent sealant technologies, which expand to form protective barriers under heat exposure, the industry is witnessing the rise of multifunctional sealant systems designed not only to seal joints but also to protect, insulate, and monitor the structure.

The ongoing wave of energy efficiency retrofitting represents one of the largest and most sustainable growth avenues for the construction sealants market. Governments across the U.S., UK, and EU are implementing large-scale funding programs to improve the energy performance of existing building stock—most of which is over 30 years old and highly energy inefficient. In the U.S. alone, renovation and remodeling activities account for over 35% of total construction spending, creating enormous demand for air-sealing and weatherproofing sealants used in envelope restoration and thermal barrier applications.

The long-term performance of airtight seals is a major challenge for the retrofit sector. A UK government study reported that airtightness deteriorated in 7 out of 10 retrofitted homes within a decade, with average leakage rates increasing by 0.52 m³/h·m² @ 50 Pa, primarily due to seal degradation over time. The data highlights the growing importance of high-adhesion, long-life sealants capable of maintaining the integrity of air barriers under dynamic structural stresses and environmental fluctuations.

In addition, policy-driven incentives further solidify the opportunity. According to U.S. Department of Energy guidelines, air sealing remains one of the most cost-effective energy-saving measures, often providing a return on investment within one year by reducing heating and cooling costs. Consequently, high-performance elastomeric and hybrid sealants that improve building envelope durability and minimize air infiltration are becoming indispensable in all major retrofit programs. Manufacturers that can supply eco-certified, high-durability, low-VOC sealing systems will continue to dominate the long-term growth segment.

A rapidly emerging frontier in the construction sealants market lies within mass timber and Cross-Laminated Timber (CLT) construction, which demands advanced sealing technologies tailored to the hygroscopic, combustible, and flexible nature of engineered wood structures. As architects and developers increasingly turn to mass timber for sustainable and carbon-sequestering construction, the need for specialized sealants capable of addressing fire safety, moisture control, and air sealing is becoming critical.

Fire safety is the leading performance driver in the niche. Recent experimental studies on steel-to-timber joints reported that an unprotected 6 mm gap reached an internal temperature of 286°C after 80 minutes of exposure, while the use of intumescent fire-resistant sealants dramatically reduced temperature rise, protecting the connection and maintaining structural integrity. These results confirm the indispensable role of sealants in extending fire resistance in mass timber systems.

From a regulatory perspective, the International Building Code (IBC) for mass timber construction (Types IV-A, IV-B, and IV-C) explicitly mandates the use of sealants conforming to ASTM C920 at junctions of fire-rated timber elements to prevent airflow and gas transfer. Additionally, large-scale fire testing of CLT walls indicates that gaps sealed with specialized smoke-resistant sealants exhibit far lower permeability under thermal stress, enhancing both compartmentation and occupant safety.

The niche market requires sealants that combine fire expansion behavior, elastic movement capability, and aesthetic finish compatibility for exposed timber surfaces. As mass timber adoption accelerates globally—driven by sustainability goals and carbon reduction mandates—manufacturers who innovate in intumescent, elastomeric, and eco-certified wood sealants will gain early-mover advantages in one of construction’s fastest-growing material segments.

Building & Construction Sealants Market Share Insights, 2025-2034

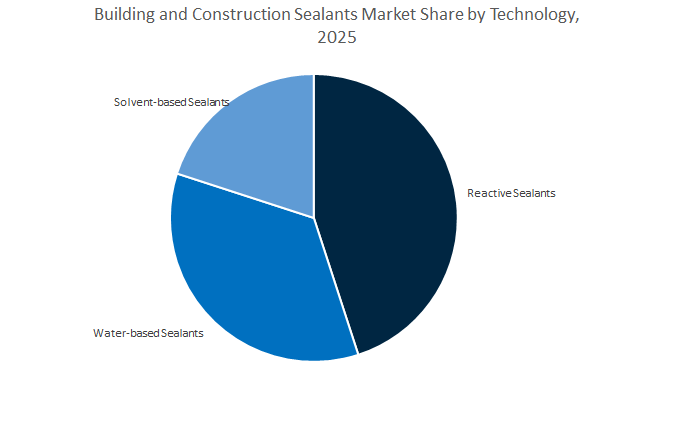

The Reactive Sealants segment dominates the global building and construction sealants industry, accounting for approximately 44.3% of the market share in 2025, owing to its unparalleled performance in structural, weatherproofing, and high-movement applications. This segment encompasses silicone, polyurethane (PU), and hybrid MS polymer-based sealants, which are the backbone of modern architectural sealing. Their superior adhesion to multiple substrates—such as glass, metal, concrete, and stone—combined with high elasticity, UV stability, and resistance to temperature extremes, makes them indispensable for critical functions like curtain wall glazing, expansion joints, roofing, and façade sealing. The dominance of reactive sealants is further fueled by their long service life and compliance with global performance standards such as ISO 11600 and ASTM C920, ensuring reliability in both commercial skyscrapers and infrastructure projects. Silicone sealants, in particular, lead within this category due to their low shrinkage, non-yellowing behavior, and extreme weather endurance, positioning them as the preferred choice for structural glazing and façade systems. The growing trend of high-rise, energy-efficient, and glass-intensive buildings continues to sustain this segment’s leadership, while hybrid polymer technologies (SMPs and STPs) are driving innovation toward low-VOC, isocyanate-free formulations, aligning with global green building goals.

The Water-based Sealants segment holds a strong secondary position, primarily due to its dominance in interior construction, renovation, and DIY applications. Predominantly composed of acrylic latex sealants, this segment is driven by ease of application, paintability, low odor, and compliance with stringent VOC emission regulations (LEED, BREEAM, and GreenGuard). Water-based systems are particularly favored in perimeter sealing, drywall finishing, flooring joints, and sanitary applications where moisture exposure is moderate. As the residential renovation market expands—especially in Europe and North America—acrylic sealants have become the material of choice for both professional contractors and homeowners seeking cost-effective, user-friendly solutions. Their compatibility with porous surfaces like concrete, plaster, and wood further strengthens their market penetration. The ongoing development of elastomerically modified water-based sealants that offer improved movement capability and durability is enhancing their competitiveness against reactive chemistries.

The Solvent-based Sealants segment, while representing a smaller portion of the market, remains relevant in specific niche applications where environmental conditions or substrate challenges demand unique performance. These sealants are prized for their fast skinning time, strong adhesion to oily or damp surfaces, and superior durability under extreme weather, making them suitable for industrial, marine, and exterior maintenance work. However, due to increasing restrictions on volatile organic compounds (VOCs) and workplace safety regulations, their use has sharply declined in favor of reactive and water-based alternatives. The segment’s current footprint is sustained in cold-climate and heavy-duty sealing operations, particularly in regions where ambient curing challenges persist. Innovations aimed at reducing solvent content and developing low-VOC hybrid alternatives are gradually transforming this category.

The Glazing segment leads the global building and construction sealants market, accounting for 25.8% of total market share, underscoring its high-value, precision-driven role in modern architecture. Sealants are vital in structural glazing, curtain wall systems, and insulated glass unit (IGU) fabrication, where they must deliver superior adhesion, movement capability, UV stability, and weather resistance. Silicone sealants dominate this application due to their excellent transparency, non-staining formulation, and long-term flexibility under high stress and extreme temperature variation. With the proliferation of glass-dominated facades, energy-efficient windows, and daylighting designs, demand for high-performance glazing sealants continues to rise globally. Moreover, the growing integration of low-E glass and smart glazing systems has increased the need for chemically compatible sealant systems that maintain clarity and structural integrity over time. This segment also benefits from ongoing advancements in neutral-cure and hybrid silicone chemistries, designed to deliver better adhesion to new-generation coated and reflective glass substrates.

The Sanitary & Kitchen segment, with a projected 20.1% market share, represents one of the largest volume-driven applications due to the ubiquitous need for sealing wet environments. These applications rely on mold-resistant, waterproof, and flexible sealants capable of withstanding constant exposure to moisture, detergents, and temperature changes. Silicone and acrylic-based formulations dominate this segment, with anti-fungal additives and high elasticity as critical performance differentiators. As hygiene standards continue to tighten globally—particularly in residential and commercial spaces such as hotels, hospitals, and restaurants—demand for long-lasting, easy-to-clean sealants is expected to accelerate. The market is also witnessing the adoption of hybrid polymer sealants that combine silicone’s durability with acrylic’s paintability, addressing consumer demand for multipurpose products. Meanwhile, the Flooring segment represents another high-volume application, where polyurethane and hybrid sealants are used for expansion joints, control joints, and substrate transitions, providing flexibility, abrasion resistance, and chemical durability. Growth in the industrial and warehouse flooring sector, particularly with epoxy and PU-based systems, continues to bolster this category.

The Global Building and Construction Sealants Market is led by top-tier players—Dow Inc., Wacker Chemie AG, Sika AG, Huntsman Corporation, and 3M Company—each driving innovation through polymer engineering, energy efficiency solutions, and sustainability-driven R&D. These companies account for a major share of the market’s growth, with their strategies emphasizing eco-compliant sealant chemistries, full-system integration, and automation-ready application systems.

Dow Construction Chemicals maintains a dominant position in silicone structural glazing (SSG), offering high-modulus, two-part sealants with 20-year performance warranties for curtain wall applications. Its DOWSIL™ 790 and 995 sealants provide industry-leading adhesion on stone, glass, and concrete, ensuring UV stability and non-staining characteristics. Dow’s sustainability focus includes low-embodied carbon silicone sealants that help projects achieve PAS 2060 carbon neutrality. Its system-compatible silicone primers and IGU sealants provide comprehensive envelope protection across façades, skylights, and glazing assemblies.

Wacker Chemie AG leverages full silicone feedstock integration, from monomer synthesis to final formulation, ensuring unmatched quality control across its ELASTOSIL® and GENIOSIL® product lines. Its bio-based alkoxy silicones utilize certified sustainable biomass, reducing carbon emissions without sacrificing UV resistance or flexibility. Wacker’s silane-modified polymer sealants (MS polymers) combine the paintability of PU with the weathering stability of silicone, supporting energy-efficient façade sealing for modern building codes.

Sika AG commands a strong presence in polyurethane and hybrid sealant systems, notably through its Sikaflex® and SikaHyflex® brands. These sealants offer high elasticity, fast curing, and exceptional cohesion, supporting critical expansion joint systems in infrastructure, parking decks, and bridges. Sika’s Sikalastic® roofing and waterproofing technologies use compatible sealants to ensure seamless building envelope performance. Its rapid-cure sealant systems, such as Sikaflex FC, are designed for faster installation cycles and improved project timelines.

Huntsman Corporation’s Polyurethanes Division provides critical raw materials (MDI) and systems for foam and elastic sealant production, ensuring vertical integration and consistent supply chain reliability. Its spray foam insulation and air sealants enhance thermal efficiency and HVAC performance in residential and commercial construction. Current R&D focuses on low-GWP blowing agents for polyurethane foam systems, aligning with global climate and sustainability targets.

3M Company applies its adhesion science expertise to deliver aerospace-grade sealants and firestop solutions adapted for construction environments. Its fire protection sealants comply with ASTM E814 and are key components in passive fire safety systems. The company’s acoustic and vibration-dampening sealants meet ASTM C919 for soundproofing in mass timber and modular interiors. 3M’s hybrid polyurethane and silicone-based sealants also serve the infrastructure repair and remedial construction market, ensuring long-term weatherability.

The U.S. construction sealants market remains at the forefront of global innovation, powered by regulatory rigor, sustainability objectives, and rapid technological integration in the built environment. The U.S. Department of Energy (DOE) continues to lead the push for advanced building envelope technologies, increasing demand for low-VOC, high-modulus silicone sealants critical for achieving airtight façades and enhancing thermal efficiency in commercial buildings.

H.B. Fuller, one of the leading global sealant manufacturers, has taken sustainability to the next level with its Millennium PG-1 EF ECO2 adhesive, which utilizes naturally occurring atmospheric gases instead of high Global Warming Potential (GWP) chemical blowing agents—demonstrating a tangible reduction in carbon footprint for roofing and insulation systems.

Meanwhile, architects and contractors are increasingly opting for STP (Silyl-Terminated Polyether) hybrid sealants that combine the durability of polyurethane with the flexibility of silicones. The solvent-free, paintable formulations are gaining traction in commercial glazing, façades, and weatherproofing applications, meeting both aesthetic and performance demands.

Additionally, the growth in modular and off-site construction has prompted manufacturers to develop factory-applied, rapid-curing sealants compatible with automated dispensing systems, improving precision and speed in large-scale assembly. Infrastructure upgrades under federal funding are further driving the use of high-movement polyurethane joint sealants for bridges and concrete expansion joints. California’s net-zero energy building codes are also accelerating the adoption of fire-rated and air barrier sealants that ensure superior safety and energy compliance.

China stands as the largest consumer and fastest-growing innovator in the global building and construction sealants market, propelled by massive urbanization and infrastructure megaprojects under the 14th Five-Year Plan. The implementation of new national standards for curtain walls and structural glazing systems has significantly increased demand for premium-grade two-part silicone sealants in high-rise façade construction.

Prefabrication continues to reshape China’s building sector. In major cities such as Shanghai, Shenzhen, and Guangzhou, government initiatives promoting modular building technologies are driving the adoption of fast-curing polyurethane and silicone sealants that can withstand dynamic stress during transport and installation.

Local manufacturers are rapidly scaling up production of silicone weatherproofing and polysulfide sealants to support mega projects like subways, tunnels, and dam construction. At the same time, there is strong policy momentum favoring low-VOC and non-solvent sealant formulations, aligning with China’s national air quality improvement goals.

The surge in green building certifications such as China Three Star and LEED equivalencies is also spurring the use of bio-based and emulsion-based sealants, providing an eco-friendly alternative for flooring and interior joints. Combined with escalating investment in R&D and manufacturing, China is poised to remain a key production and innovation hub for next-generation construction sealants.

Germany continues to lead Europe’s sealant innovation landscape, emphasizing carbon-neutral production, sustainable chemistry, and advanced façade sealing systems. Wacker Chemie AG is spearheading The transition with its ELASTOSIL® eco portfolio, a pioneering range of silicone sealants manufactured via the mass balance method, which replaces 100% of fossil raw materials with certified renewable biomass.

Driven by the European Union’s Energy Performance of Buildings Directive (EPBD), demand for high-elasticity polyurethane and foam sealants has soared, essential for achieving near-zero-energy performance through airtight joints and minimal thermal bridging. Public subsidies for energy renovation and retrofitting are further fueling demand for specialized renovation sealants, capable of adhering to aged masonry, timber, and composite surfaces found in historic European architecture.

German manufacturers are also pushing boundaries with isocyanate-free hybrid polymers to enhance worker safety and environmental compliance under REACH regulations. In the high-tech sector, advanced insulating glass (IG) manufacturing continues to rely on hot-melt butyl sealants and Ködispace 4SG warm-edge spacers—technologies that improve insulation and reduce thermal losses in energy-efficient windows.

Cutting-edge R&D collaborations between universities and private industry are exploring self-healing polymer sealants, designed to autonomously close micro-cracks and extend façade joint life cycles, marking a key step toward next-generation sustainable construction materials.

India’s building and construction sealants industry is witnessing exponential growth, supported by massive public infrastructure projects and government-led sustainability programs. A landmark development occurred in 2024 when Dow India partnered with Glass Wall Systems India to supply DOWSIL™ Facade Sealants from its Decarbia™ portfolio, marking the introduction of carbon-neutral silicone sealants into India’s façade construction sector—a first-of-its-kind initiative aimed at reducing embodied carbon in urban development.

The country’s National Infrastructure Pipeline (NIP) and smart city initiatives are generating robust demand for chemically resistant epoxy joint sealants and durable polyurethane sealants for heavy-duty flooring and parking structures. Simultaneously, affordable housing programs like Pradhan Mantri Awas Yojana are fueling large-scale use of acrylic and basic silicone sealants in residential construction.

Local leader Pidilite Industries Ltd., through its flagship brand Dr. Fixit, continues expanding its distribution network and R&D investment to deliver high-quality waterproofing and basement sealing solutions tailored for India’s tropical climate. Additionally, new Sika manufacturing facilities in Pune are strengthening domestic production capacity and enabling climate-optimized formulations.

With FDI inflows in commercial real estate and large infrastructure, the market is also seeing a surge in imported high-performance firestopping and façade sealants, helping Indian projects comply with global fire safety standards.

France’s construction sealants market is being reshaped by environmental regulations (RE 2020) that promote bio-based, low-emission materials for both new builds and heritage restorations. The mandates are spurring the use of bio-content polyurethane and acrylic sealants that combine structural integrity with recyclability, aligning with national climate goals.

Construction giants in France are increasingly utilizing PU foam sealants for prefabricated concrete and timber panels to streamline on-site assembly and reduce labor costs. The government’s investment in rail and transit infrastructure continues to create consistent demand for vibration-resistant elastomeric sealants used in tunnel gaskets and rail expansion joints.

Heritage restoration remains a distinct market niche: restoration contractors are specifying limestone-compatible, reversible sealants to preserve historic masonry façades. Moreover, French manufacturers are introducing products certified with A+ indoor air quality labels, addressing the health-conscious demands of modern commercial building occupants.

Finally, specialized silicone and fluoropolymer sealants are being developed for nuclear and defense applications, capable of resisting extreme radiation and high-temperature environments.

The UAE building and construction sealants market continues to thrive, propelled by mega projects in Dubai, Abu Dhabi, and Sharjah, where extreme weather conditions require UV-resistant and temperature-stable structural silicone sealants for façade applications. Developers of high-rise towers and mixed-use complexes are mandating premium-grade glazing and weatherproofing sealants to ensure long-term durability and energy performance.

Ongoing investment in industrial and maritime infrastructure—including ports, desalination plants, and petrochemical facilities—has increased consumption of polysulfide and epoxy sealants for chemically aggressive environments. The rapid expansion of solar energy projects across the Emirates also drives demand for specialized photovoltaic (PV) module sealants with high adhesion and thermal stability.

As the UAE pushes toward digital construction and BIM-based project validation, there is growing preference for sealant brands offering data-certified, performance-tested solutions. The trend toward fire-rated sealants exceeding international safety standards is also notable in large residential and hospitality developments.

Building & Construction Sealants Market Report Scope

Building & Construction Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.7 Billion

|

|

Market Size (2034)

|

$9.3 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Resin Type (Silicone, Polyurethane, Polysulfide, Acrylic, Butyl, Elastomeric, Others), By Technology (Water-based, Solvent-based, Reactive), By Application (Glazing, Flooring, Roofing, Sanitary & Kitchen, Expansion Joints, Interior/Exterior Perimeter Sealing, Infrastructure), By End-User (Commercial, Residential, Infrastructure

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Henkel AG & Co. KGaA, Sika AG, Wacker Chemie AG, H.B. Fuller Company, Arkema, BASF SE, 3M Company, DuPont de Nemours, Inc, Mapei S.p.A., Pidilite Industries Ltd, Illinois Tool Works Inc, Tremco CPG, KCC Corporation, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Silicone

- Polyurethane

- Polysulfide

- Acrylic

- Butyl

- Elastomeric

- Others

By Technology

- Water-based

- Solvent-based

- Reactive

By Application

- Glazing

- Flooring

- Roofing

- Sanitary & Kitchen

- Expansion Joints

- Interior/Exterior Perimeter Sealing

- Infrastructure

By End-Use Sector

- Commercial

- Residential

- Infrastructure

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Dow Inc.

- Henkel AG & Co. KGaA

- Sika AG

- Wacker Chemie AG

- H.B. Fuller Company

- Arkema

- BASF SE

- 3M Company

- DuPont de Nemours, Inc

- Mapei S.p.A.

- Pidilite Industries Ltd

- Illinois Tool Works Inc

- Tremco CPG

- KCC Corporation

- Huntsman Corporation

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates how silicone, polyurethane, polysulfide, acrylic, butyl, elastomeric, and modern hybrid sealants are reshaping façade engineering, glazing, expansion joints, and energy-efficient envelopes. Our analysis reviews durability (ASTM C920/ISO 11600), seismic/wind movement performance, EN 1366-4 fire integrity, and low-VOC compliance within LEED/BREEAM/WELL projects. It highlights carbon-neutral (PAS 2060) silicone programs, biomass-balanced chemistries, automation-ready hot-melt silicones for fenestration, and hybrid SMP/STP systems that pair silicone weatherability with polyurethane adhesion. Mapping procurement shifts, warranty practices (e.g., 20-year SSG), and retrofit demand, we spotlight material and application breakthroughs that improve airtightness, lifecycle cost, and envelope reliability—making this report an essential resource for contractors, façade consultants, QS/procurement teams, OEM fabricators, and sustainability officers planning 2025–2034 portfolios.

Scope Includes

- By Resin Type: Silicone; Polyurethane; Polysulfide; Acrylic; Butyl; Elastomeric; Others

- By Technology: Water-based; Solvent-based; Reactive

- By Application: Glazing; Flooring; Roofing; Sanitary & Kitchen; Expansion Joints; Interior/Exterior Perimeter Sealing; Infrastructure

- By End-Use Sector: Commercial; Residential; Infrastructure

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic data 2021–2024 and forecasts 2025–2034.

- Companies: 15+ company analyses/profiles included.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.