Market Overview: Chemicals Packaging Industry Strengthened by Plastics and Safety Standards

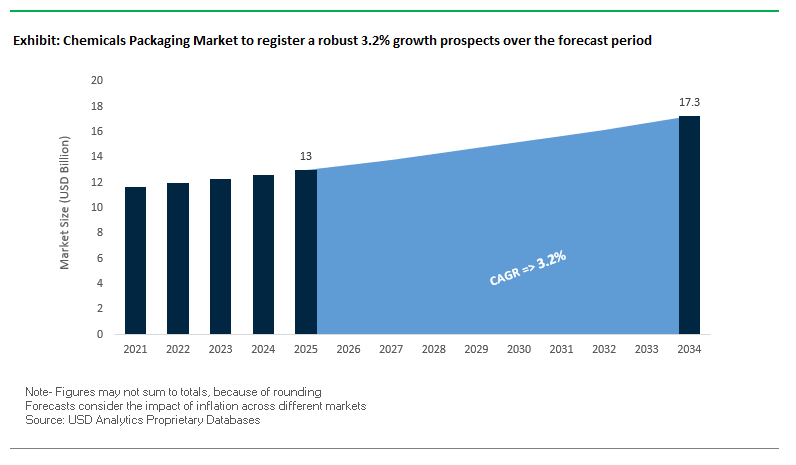

The Chemicals Packaging Market is valued at $13 billion in 2025 and is projected to reach $17.3 billion by 2034, expanding at a steady CAGR of 3.2%. Growth is supported by the rising need for durable and regulation-compliant packaging for hazardous and non-hazardous chemicals, alongside the expansion of digital distribution platforms. Industry buyers and professionals are seeking solutions that balance safety, sustainability, and efficiency, with materials and formats tailored to global chemical transport regulations.

Plastic remains the dominant material, with HDPE and PE containers widely favored for their corrosion resistance and cost-effectiveness. On the logistics side, Intermediate Bulk Containers (IBCs) and drums dominate large-volume transport, offering reusability, safety certifications, and space efficiency. The market is also shaped by stringent international standards such as GHS and ADR in Europe, driving demand for tamper-proof and leak-proof designs.

Additionally, e-commerce and digital supply chains are boosting the use of smart packaging with RFID tags and traceability features, ensuring real-time tracking and compliance. Sustainability is another critical driver, with leading players integrating recyclable plastics and circular packaging models to reduce environmental footprints.

Key Insights for Industry Professionals

- Plastics dominate packaging choice: HDPE and PE remain critical for chemical storage and transport.

- IBCs and drums lead logistics: Reusable containers dominate large-volume shipments.

- Global safety standards enforce innovation: Packaging must comply with GHS, ADR, and UN certifications.

- E-commerce drives smart packaging: RFID-enabled solutions enhance supply chain transparency.

Market Analysis: Strategic Developments Redefining Chemicals Packaging

The chemicals packaging industry has witnessed a wave of strategic moves, acquisitions, and innovations aimed at expanding capacity, advancing sustainability, and reinforcing compliance with safety regulations.

In August 2025, Constantia Flexibles earned two WorldStar Global Packaging Awards for eco-friendly solutions, reflecting the industry’s pivot toward sustainability. That same month, Mauser Packaging Solutions expanded in South Africa by acquiring a plastic drum manufacturer in Pinetown, enhancing its supply of UN-certified drums. Similarly, the $13.4 billion acquisition of Nova Chemicals by Borouge Group International (July 2025) significantly reshaped the plastics supply chain critical to chemical packaging.

In June 2025, the merger of IPL and Schoeller Allibert, two leaders in reusable packaging, strengthened industrial container portfolios across Europe and North America. Earlier in April 2025, UPM Raflatac launched its Carbon Action Plastic Films portfolio, providing packaging with reduced carbon impact. Meanwhile, Greif, Inc. inaugurated a new IBC facility in Malaysia in November 2024, boosting capacity to meet rising demand in Southeast Asia.

Innovation continues in Asia, with BASF and Nippon Paint China (August 2024) introducing eco-friendly industrial packaging for dry mortar products, marking a milestone in sustainable coatings integration. Preceding these, Berry Global’s Omni® Xtra+ cling film (November 2023) and Silgan’s Gateway Plastics acquisition (late 2023) reflect diversification and recyclability strategies across the broader industrial packaging landscape.

Key Trends and Opportunities Transforming the Chemicals Packaging Market

Strategic Shift Towards Reusable and Refillable Intermediate Bulk Container (IBC) Systems

The chemicals packaging market is witnessing a decisive transition from single-use containers to reusable and service-based IBC systems, driven by sustainability commitments, regulatory mandates, and operational efficiency goals. Lifecycle studies consistently show that reusable IBCs outperform single-use models in environmental impact, with benefits compounding over multiple reuse cycles. Beyond their ecological edge, reusable IBCs optimize supply chains: their stackable design maximizes storage density, reduces labor costs, and enables compatibility across road, rail, and maritime transport. A case study highlighted how reconditioned IBCs, with a service life of up to 10 years and bottle replacement every five years, spread costs and emissions over multiple use cycles, lowering total cost of ownership for chemical producers. This aligns with circular economy principles by preserving embedded material value while minimizing waste. As chemical producers prioritize both economic performance and ESG compliance, reusable IBC adoption is becoming an industry standard for long-term competitiveness.

Enhanced Integration of Smart Packaging Technologies for Supply Chain Integrity

Digitalization is reshaping chemicals packaging, with IoT sensors, RFID systems, and NFC tags transforming containers into data-rich assets. These technologies are enhancing safety, compliance, and efficiency across the chemical value chain. RFID-enabled drum-tracking systems, for example, have reduced container wastage by 22% for a European chemical company by improving asset recovery rates. Smart sensors monitoring temperature, shock, and humidity are critical in maintaining the stability of sensitive chemicals and ensuring regulatory compliance during transit. QR codes and NFC tags embedded on packaging provide granular traceability, from origin to handling history, which is vital for preventing counterfeiting and ensuring adherence to safety regulations. As global supply chains become more complex and risk-prone, the integration of smart packaging is evolving from a niche capability into a mainstream requirement, helping companies mitigate losses, improve compliance, and meet rising customer expectations for transparency.

Development of High-Performance Recycled Resins for Rigorous Applications

The rising demand for circularity presents a lucrative opportunity to develop new grades of post-consumer recycled (PCR) resins capable of meeting the stringent safety, durability, and regulatory requirements of chemical packaging. While PCR is widely used in consumer goods, chemical applications demand far higher chemical resistance and purity. Innovation in additives and processing aids is addressing these barriers by improving physical and chemical performance, making PCR viable for industrial-grade containers. The plastics industry is already advancing in this area, with examples such as thermoplastic vulcanizates incorporating 25% recycled content for high-performance applications. As regulatory and corporate sustainability pressures intensify, chemical producers and packaging converters will increasingly adopt PCR-based solutions to reduce reliance on virgin plastics. Success in scaling high-quality PCR for demanding chemical applications will not only advance sustainability goals but also unlock new premium revenue streams for resin and packaging manufacturers.

Standardization and Adoption of Composite IBCs for Lightweighting and Corrosion Resistance

Composite IBCs are emerging as the next-generation standard for transporting and storing chemicals, offering a powerful combination of lightweighting, corrosion resistance, and safety. By combining a durable plastic inner liner with a galvanized steel cage, composite IBCs reduce shipping weight compared to traditional steel drums, lowering fuel consumption and logistics costs while enabling higher product volumes per load. For corrosive liquids, composite IBCs deliver superior compatibility and longevity compared to metal alternatives, minimizing product degradation and container failure. Their standardized cubic shape and integrated pallet base improve handling efficiency and stacking safety, reducing risks of spills and accidents. Studies comparing IBCs with 55-gallon drums show that while drums may offer lower upfront costs, composite IBCs deliver greater long-term savings through reduced transport expenses and enhanced operational performance. As the industry prioritizes safety, cost-efficiency, and sustainability, composite IBCs are set to play a dominant role in reshaping chemical packaging supply chains.

Competitive Landscape: Leading Companies Driving Chemicals Packaging Market Growth

The global chemicals packaging industry is highly consolidated, with multinational leaders innovating across plastics, rigid packaging, and smart containers. Key companies focus on expanding global reach, investing in reconditioning networks, and embedding sustainability into their portfolios.

Mauser Packaging Solutions: Expanding with UN-Certified Drums in Africa

Mauser Packaging Solutions is a recognized leader in industrial packaging, offering IBCs, drums, and jerry cans. In August 2025, the company acquired a drum manufacturing business in South Africa, enhancing its supply of UN-certified plastic drums for petrochemicals and mining sectors. With a global reconditioning network, Mauser champions a circular model by collecting, cleaning, and reusing packaging, reducing environmental footprints for clients.

Greif, Inc.: Scaling IBC Manufacturing with Southeast Asian Expansion

Greif’s portfolio spans steel, plastic, and fiber drums alongside IBCs and corrugated products. In November 2024, it inaugurated a new IBC plant in Malaysia equipped with advanced manufacturing to meet sustainability and safety standards. Its vertical integration from forestry operations to packaging ensures control over raw materials and consistent product quality. Greif continues to strengthen its sustainable industrial packaging leadership globally.

Amcor plc: Driving Innovation with Recycle-Ready Films

Amcor, a global giant in plastic packaging, leverages sustainability as its core strategy. Its AmSky Blister System, a mono-material PE innovation, eliminates aluminum and PVC while remaining fully recyclable a breakthrough with potential in chemical packaging applications. Amcor’s global sustainability teams are embedding recycle-ready solutions across portfolios, ensuring compatibility with existing client machinery. The company targets 100% recyclability by 2025, making it a frontrunner in circular packaging innovation.

Berry Global Inc.: Innovating Lightweight and Recyclable Packaging

Berry Global provides containers, closures, and specialty films with a strong focus on circular plastics. Its Omni® Xtra+ cling film, launched in November 2023, reduces material usage by 25% while enhancing performance. Beyond films, Berry is pioneering smart packaging with digital watermarks and recyclable polypropylene bottles for healthcare and chemicals. The company’s strategy is anchored in sustainability partnerships and recycling rate improvements.

Silgan Holdings Inc.: Diversifying Rigid Packaging Portfolio

Silgan Holdings manufactures rigid plastic, metal, and composite containers for consumer and industrial markets. In late 2023, it acquired Gateway Plastics, strengthening its injection-molded closures and container portfolio for chemical and food packaging. With vertical integration from resin compounding to manufacturing, Silgan delivers customized solutions with strict quality control, positioning itself as a reliable partner for chemical packaging applications.

Chemicals Packaging Market Share Insights

Intermediate Bulk Containers (IBCs) Lead Market Share by Product Type in Chemicals Packaging

IBCs hold the leading 28% share in the chemicals packaging industry because they deliver unmatched logistics efficiency for medium-to-large volumes, particularly in petrochemicals and agrochemicals. Their standardized pallet footprint, forklift compatibility, and ability to integrate into reusable pooling systems make them the preferred solution for high-frequency shippers focused on cost optimization and sustainability. Unlike drums or sacks, IBCs reduce per-unit transport cost while improving handling safety, aligning with global chemical companies’ shift toward supply chain efficiency and circular business models. As reconditioning infrastructure expands across North America, Europe, and Asia, IBCs are increasingly viewed not just as containers but as strategic supply chain assets that support both compliance and corporate ESG targets.

Petrochemicals Dominate Market Share by Application in Chemicals Packaging

Petrochemicals account for the largest share of demand in chemicals packaging, consuming nearly a quarter of the market. The sheer volume of base chemicals, lubricants, and industrial oils produced globally ensures petrochemicals remain the volume driver, with drums and IBCs forming the backbone of distribution. The dominance of this segment reflects not only production scale but also the critical need for UN-certified, reconditionable, and reusable formats that maintain compatibility with aggressive chemical compositions. Global refiners and petrochemical majors are increasingly favoring steel drums and composite IBCs because their durability extends container life cycles while reducing total cost of ownership. In a sector where cost sensitivity is paramount and logistics efficiency determines competitiveness, petrochemicals’ packaging requirements set the performance benchmarks for the broader chemicals packaging industry.

United States: Rising Demand for Smart and Sustainable Chemical Packaging

The U.S. chemicals packaging market is being shaped by heightened consumer and corporate awareness of health, safety, and environmental responsibility. There is a growing demand for robust, tamper-evident, and secure packaging across both industrial and household chemical segments. Technological innovations such as RFID tags, IoT sensors, and smart packaging solutions are increasingly adopted to ensure traceability, supply chain transparency, and product safety, particularly for high-value or hazardous chemicals.

Sustainability is a key growth driver. Leading companies, including Amcor and NOVA Chemicals Corporation, are investing in mechanically recycled polyethylene and mono-material packaging to reduce environmental impact and enhance recyclability. Furthermore, regulatory oversight from the FDA and EPA ensures that chemical packaging complies with strict guidelines regarding material compatibility, child-resistant features, and tamper-evident seals, which not only protects consumers but also reinforces the market’s emphasis on high-quality, safe, and compliant packaging solutions.

Germany: Circular Economy and Regulatory Policies Propel Eco-Friendly Packaging

Germany’s chemicals packaging industry is strongly influenced by the EU Packaging and Packaging Waste Regulation (PPWR) 2025, which mandates eco-friendly, recyclable, and high-quality packaging solutions. The country’s focus on the circular economy encourages the development of packaging that integrates high percentages of recycled content, meeting both national and EU sustainability targets.

Technological innovation is a key market driver. Collaborations such as the June 2024 project between ExxonMobil, Hosokawa Alpine, Henkel, Nordmeccanica Group, and Univel have resulted in high-barrier, recyclable MDO-PE/PE laminates suitable for various products, including chemicals. Governmental mandates under the PPWR framework, emphasizing waste reduction and increased recyclability, continue to foster innovation and adoption of sustainable chemical packaging solutions, positioning Germany as a global leader in eco-conscious packaging practices.

China: Government Initiatives and Technological Advancements Drive Market Growth

China’s chemicals packaging market is being reshaped by the government’s dual carbon goals, which aim to achieve carbon peak and carbon neutrality, promoting a green transformation of the chemical and packaging industries. Policies encouraging eco-friendly, reduced, and reusable packaging materials, coupled with restrictions on non-degradable plastics in e-commerce by 2025, are creating significant market opportunities.

Technological advancements play a pivotal role. Chinese manufacturers are heavily investing in automation, AI, and “5G plus industrial internet” integration to optimize production efficiency, ensure flexible manufacturing, and improve operational productivity. Additionally, the growth of China’s petrochemicals sector, fueled by rising disposable incomes and increased chemical consumption, drives the need for safe, high-performance, and sustainable packaging solutions that protect chemical products while supporting environmental objectives.

India: Infrastructure Investments and Sustainability Initiatives Strengthen Chemical Packaging

India’s chemicals packaging industry is expanding rapidly, supported by the government’s Make in India and Zero Effect Zero Defect initiatives, which encourage domestic production, high-quality manufacturing, and industrial growth. The government’s development of Petroleum, Chemicals & Petrochemicals Investment Regions (PCPIRs) aims to attract investments worth approximately $420 billion by 2025, significantly benefiting the chemical packaging sector.

Sustainability and eco-friendly packaging solutions are driving market adoption. The Plastic Waste Management (Amendment) Rules are creating a demand for reusable and environmentally responsible packaging. In parallel, corporate investments such as Godrej Industries’ Rs 750 crore expansion strengthen production capabilities and position the company to become a $1 billion global player by 2030. The combination of policy support, infrastructure investment, and technological advancements underscores India’s strategic growth trajectory in chemical packaging, with a strong focus on sustainable, safe, and efficient solutions.

Chemicals Packaging Market Report Scope

Chemicals Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13 Billion

|

|

Market Size (2034)

|

$17.3 Billion

|

|

Market Growth Rate

|

3.2%

|

|

Segments

|

By Material (Plastics, Metal, Glass, Paper & Paperboard), By Product Type (Drums, IBCs, Jerrycans, Sacks & Bags, Bottles, Others), By Application (Agrochemicals, Pharmaceuticals, Dyes & Pigments, Petrochemicals, Specialty Chemicals, Adhesives & Sealants)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Greif, Inc., Mauser Packaging Solutions, Amcor plc, Berry Global Group, Inc., International Paper, Orbis Corporation, Mondi Group, RPC Group (part of Berry Global), Nippon Paper Industries Co., Ltd., Silgan Holdings Inc., Bormioli Pharma S.p.A., Gerresheimer AG, Sealed Air Corporation, SGD Pharma, Sonoco Products Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Chemicals Packaging Market Segmentation

By Material

- Plastics

- Metal

- Glass

- Paper & Paperboard

By Product Type

- Drums

- IBCs

- Jerrycans

- Sacks & Bags

- Bottles

- Others

By Application

- Agrochemicals

- Pharmaceuticals

- Dyes & Pigments

- Petrochemicals

- Specialty Chemicals

- Adhesives & Sealants

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Chemicals Packaging Market

- Greif, Inc.

- Mauser Packaging Solutions

- Amcor plc

- Berry Global Group, Inc.

- International Paper

- Orbis Corporation

- Mondi Group

- RPC Group (part of Berry Global)

- Nippon Paper Industries Co., Ltd.

- Silgan Holdings Inc.

- Bormioli Pharma S.p.A.

- Gerresheimer AG

- Sealed Air Corporation

- SGD Pharma

- Sonoco Products Company

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global Chemicals Packaging market, highlighting breakthroughs in reusable containers, smart packaging integration, high-performance recycled resins, and eco-friendly composite IBCs. The analysis reviews historical trends from 2021 to 2024 and forecasts developments from 2025 to 2034, exploring how regulatory compliance, digital supply chain adoption, and sustainability initiatives are driving market evolution. This report is an essential resource for industry professionals, investors, and chemical producers seeking actionable intelligence on materials, container designs, and technology adoption. Analysis reviews the impact of intermediate bulk containers (IBCs), drums, jerrycans, and bottles on logistics efficiency, cost optimization, and safety, while highlighting innovations in RFID-enabled tracking, IoT sensors, and temperature/humidity monitoring. Strategic developments such as mergers, acquisitions, and sustainability-driven portfolio expansions are examined across leading players. USDAnalytics also provides comprehensive profiles and competitive insights for 15+ companies, including Greif, Mauser Packaging Solutions, Amcor, Berry Global, Silgan Holdings, and Mondi Group, offering guidance for decision-making in a highly regulated, fast-evolving chemicals packaging landscape.

Scope Highlights:

- Segmentation: By Material (Plastics, Metal, Glass, Paper & Paperboard), By Product Type (Drums, IBCs, Jerrycans, Sacks & Bags, Bottles, Others), By Application (Agrochemicals, Pharmaceuticals, Dyes & Pigments, Petrochemicals, Specialty Chemicals, Adhesives & Sealants)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historic & Forecast Data: Historic data from 2021 to 2024; forecast data from 2025 to 2034

- Companies: Analysis/profiles of 15+ leading companies, including Greif, Inc., Mauser Packaging Solutions, Amcor plc, Berry Global Group, International Paper, Orbis Corporation, Mondi Group, RPC Group, Nippon Paper Industries, Silgan Holdings, Bormioli Pharma, Gerresheimer AG, Sealed Air, SGD Pharma, and Sonoco Products

Methodology

The research methodology integrates primary insights from chemical manufacturers, packaging converters, and logistics professionals with secondary research from regulatory bodies, trade reports, and corporate disclosures. USDAnalytics applies quantitative and qualitative analyses, including market sizing, CAGR estimation, material utilization studies, container type evaluation, and application-specific adoption trends. A bottom-up approach models production, reconditioning, and logistics capacity, while top-down forecasts validate global demand and growth projections. Technological innovations such as smart IBCs, RFID/NFC-enabled containers, recycled resin adoption, and composite packaging are assessed for market penetration and regulatory alignment. Scenario planning, compliance mapping, and competitive benchmarking ensure the report provides actionable intelligence for industry leaders, investors, and regulatory stakeholders navigating evolving safety, environmental, and operational requirements in the chemicals packaging market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.