Detergent Chemicals Market to Reach $109.8 Billion by 2034 at 5.2% CAGR Driven by Biosurfactants, Low-Carbon LAB, and Smart Dosing Technologies

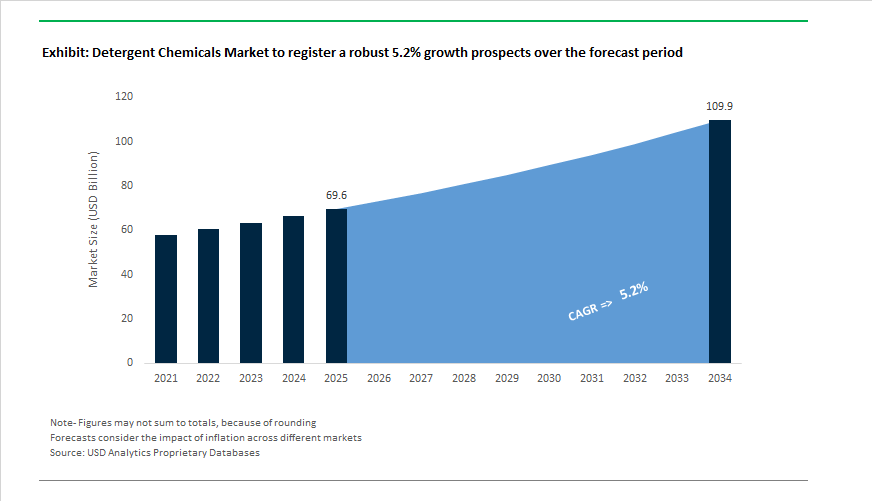

The Detergent Chemicals Market is projected to expand from $69.6 billion in 2025 to $109.8 billion by 2034, registering a CAGR of 5.2%. Growth is anchored in sustained demand for surfactants, builders, enzymes, optical brighteners, bleaching agents, and specialty additives across household, industrial, and institutional cleaning segments. Structural shifts toward bio-based surfactants, low-carbon Linear Alkylbenzene (LAB), Alkyl Polyglucosides (APGs), and concentrated formulations are redefining procurement strategies for global FMCG manufacturers and private-label producers. Regulatory pressure on carbon intensity, plastic reduction mandates, and wastewater discharge standards are accelerating innovation in mild, biodegradable, and high-efficiency detergent chemistries.

Industry transformation intensified in January 2024 when Kitten Enterprises launched a sterile alkaline detergent infused with Water for Injection for pharmaceutical cleanroom environments, targeting contamination-sensitive production facilities. In May 2024, Evonik inaugurated the world’s first industrial-scale rhamnolipid biosurfactant plant in Slovakia, introducing 100% bio-based and biodegradable surfactants produced from renewable sugar feedstocks. That same month, Tetra Pak launched its Factory Sustainable Solutions platform, incorporating nanofiltration technology capable of recovering up to 90% of Cleaning-In-Place liquids, significantly reducing industrial detergent chemical consumption. In September 2024, CEPSA Química introduced NextLab Low Carbon LAB across Asia, manufacturing Linear Alkylbenzene using renewable heat to reduce the carbon footprint of liquid and powder detergent formulations. Corporate portfolio consolidation also reshaped the sector, as Samyang Holdings completed the acquisition of Verdant Specialty Solutions in early 2024, strengthening its amphoteric and non-ionic surfactant portfolio for mild cleaning systems. In January 2025, Henkel unveiled Smartwash™ AI dosing technology at CES 2025, integrating sensor-driven cartridge systems that optimize detergent dosage per wash cycle, addressing chemical overuse and sustainability compliance in European markets.

Capacity expansion and strategic restructuring accelerated through March 2025, when Evonik signed an exclusive U.S. distribution agreement with Sea-Land Chemical Company to scale specialty surfactants and additives across the industrial and institutional cleaning sector. In November 2025, BASF inaugurated an expanded APG production line in Bangpakong, Thailand, reinforcing supply of bio-based, mild surfactants derived from renewable feedstocks. BASF also confirmed the completion trajectory of its new APG production facility in Cincinnati, Ohio, expected in 2026 to serve North American demand. In December 2025, BASF signed an agreement to divest its optical brightening agent business to Catexel, expected to close in Q1 2026, enabling the company to redirect capital toward high-growth sustainable surfactant platforms. Leadership realignment continued in January 2026, when Clariant appointed Marcelo Lu as President Designate for Care Chemicals & Americas, signaling strategic emphasis on sustainable home care ingredients. Parallel to ingredient innovation, Unilever’s April 2024 pledge to reduce virgin plastic usage by 30% by 2026 and 40% by 2028 is intensifying demand for concentrated detergent chemicals, refill systems, and packaging-efficient formulations, reshaping raw material sourcing, surfactant selection, and performance benchmarking across the global detergent value chain.

Trends and Opportunities in the Global Detergent Chemicals Market

Cold-Water Active and Short-Cycle Detergent Chemistry Redefining Wash Performance

- The convergence of household energy reduction goals and consumer preference for speed is driving a structural shift toward detergents optimized for cold water and short wash cycles. In early 2025, Unilever reported that Persil Wonder Wash™, formulated for 15-minute cycles, reached 9% of UK households within its first year. This rapid adoption underscores the scale of the speed-cleaning trend and its impact on detergent chemistry, particularly the growing reliance on protease and amylase enzymes capable of breaking down stains in under 15 minutes at temperatures as low as 20 degrees Celsius.

- Ingredient innovation is reinforcing this shift. During 2024 and 2025, IFF introduced PREFERENZ® P 400 protease, engineered for inherent stability without the need for traditional chemical stabilizers. This allows detergent manufacturers to simplify liquid formulations, lower total cost of formulation, and maintain over 90% cleaning efficacy even after extended storage under fluctuating household temperatures. As cold-water washing becomes the default in many markets, enzyme performance and stability are emerging as the primary value drivers within detergent chemical portfolios.

Regulatory Phase-Out of Microplastics and Push for Advanced Biodegradability

- Regulatory reform is accelerating the removal of persistent polymers and microplastic-forming additives from detergent formulations. On December 8, 2025, the Council of the European Union approved a comprehensive update replacing the long-standing EC No 648/2004 detergent framework. A central provision of this reform is a 3.5-year transition period requiring the industry to meet stricter biodegradability criteria for water-soluble films and fragrance encapsulation shells. This effectively ends the use of polymer systems that fragment into microplastics during or after washing.

- In response, chemical suppliers are scaling bio-based alternatives that meet both performance and eco-label standards. In April 2025, BASF launched Lamesoft® OP Plus, a wax-based opacifier dispersion with a natural origin content of up to 98.5%. This solution offers a direct replacement for synthetic acrylate opacifiers, enabling brands to maintain premium visual aesthetics while complying with emerging European and global biodegradability requirements. As enforcement tightens, bio-derived detergent chemicals are moving from niche positioning to mainstream formulation requirements.

Detergent Systems Engineered for Technical and Performance Fabrics

- The global rise of athleisure and performance apparel is creating a high-value niche for detergent chemicals tailored to synthetic and blended fabrics. These textiles trap body oils and odors more aggressively while remaining sensitive to harsh surfactants. In February 2025, Henkel’s Persil® Activewear Clean received Product of the Year USA recognition for formulations designed to remove sebum and sweat odors without degrading elastane stretch or moisture-wicking properties. This category is driving demand for surfactants with strong grease-cutting capability combined with fiber-safe performance.

- Smart appliances are amplifying this opportunity. The 2025 launch of Samsung Bespoke AI Laundry systems introduced sensors capable of monitoring detergent concentration and fabric soil levels in real time. This enables the emergence of smart detergents formulated with calibrated conductivity and viscosity profiles that support precise auto-dosing. Such systems can reduce detergent overuse and chemical waste by up to 30 %, aligning cost savings with sustainability objectives for both consumers and manufacturers.

High-Concentration Actives Enabling Waterless and Solid Detergent Formats

- Plastic reduction mandates and logistics optimization are accelerating the shift toward waterless detergent formats such as solid sheets and ultra-concentrated reloads. Industry data from 2024 and 2025 shows that an annual supply of detergent sheets for a household weighs approximately 1 kilogram, compared with around 15 kilograms for conventional liquid detergents. This weight reduction, coupled with an 80 to 90% decrease in plastic packaging, is driving strong investment in novel binder systems, bio-based matrices, and alternatives to conventional polyvinyl alcohol films that dissolve rapidly in both cold and hot water.

- Regulatory recognition is reinforcing this trend. Under the 2025 EU Detergent Regulation, refill and bulk sales models are formally encouraged, creating demand for highly concentrated detergent actives that can be diluted at home or dispensed at retail refill stations. For major global brands, these circular distribution models can reduce transportation-related emissions by an estimated 25,000 truckloads per year per brand. As a result, high-concentration detergent chemicals are emerging as a critical lever for decarbonization, cost efficiency, and regulatory compliance in the evolving detergent chemicals market.

Detergent Chemicals Market Share and Segmentation Insights

Market Share by Chemical Type : Surfactants Lead as Enzymes Accelerate Low-Temperature Washing

Surfactants account for 42% of detergent chemical consumption in 2025, reinforcing their role as the core cleaning agents across laundry detergents, household cleaners, and dishwashing formulations. Anionic systems such as linear alkylbenzene sulfonate (LAS), along with alcohol ethoxylates and alcohol sulfates, dominate due to strong soil removal, foaming, and cost efficiency. Builders including zeolites, phosphates, and citrates remain essential for water softening and alkalinity control, with phosphate-free formulations driving innovation in polymer-based builder systems. Bleaching agents such as sodium percarbonate, sodium perborate, and TAED activators support stain removal and fabric whitening, with oxygen bleaches increasingly preferred over chlorine. Enzymes are the fastest-growing segment, enabling effective cold-water washing through targeted action from proteases, lipases, amylases, and cellulases. Specialty additives including optical brighteners, fragrances, foam regulators, and soil-release polymers enhance product differentiation and premium performance.

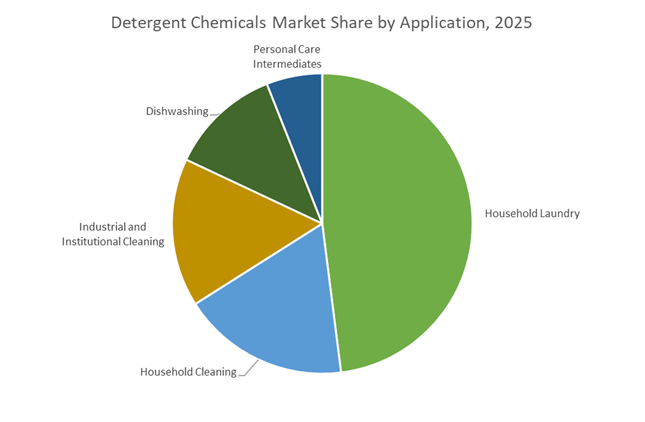

Market Share by Application : Household Laundry Dominates as I&I Cleaning Expands

Household laundry represents 48% of detergent chemical demand, driven by global consumption of powders, liquids, pods, and tablets incorporating surfactants, builders, enzymes, and bleaching agents. Market growth is shaped by concentrated formulations, multi-chamber pods, and rising adoption of cold-water washing, all influencing ingredient optimization. Household cleaning products form a substantial secondary segment, relying on surfactants and specialty additives for multi-surface performance in kitchens, bathrooms, and floors, with post-pandemic hygiene awareness sustaining volume. Industrial and institutional (I&I) cleaning continues to expand across healthcare, hospitality, food service, and manufacturing, emphasizing high-efficiency formulations delivered via automated dosing systems and aligned with sustainability targets. Dishwashing applications split between low-foaming automatic detergents and mild, foam-stable hand dish liquids. Personal care intermediates complete the landscape, utilizing gentle surfactants and conditioning additives in shampoos and body washes, fueled by demand for sulfate-free and skin-compatible products.

Competitive Landscape of the Detergent Chemicals Market

The Detergent Chemicals Market is increasingly defined by bio-based surfactants, Scope 3 decarbonization strategies, vertically integrated supply chains, and high-performance ingredients for concentrated laundry formats, as global brands accelerate their transition toward sustainable home care and industrial cleaning solutions.

BASF SE enables green transformation across the integrated detergent value chain

BASF remains a cornerstone of the global detergent chemicals market, leveraging its Verbund manufacturing network to deliver scale, cost stability, and carbon-reduction pathways across surfactants and builders. In early 2026, BASF reinforced its “Enable Green Transformation” strategy, positioning itself as a preferred partner for FMCG brands targeting lower Scope 3 emissions. The company also announced that AdBlue® GE, produced using 100% green electricity, forms part of a wider effort to decarbonize auxiliary cleaning and processing chemicals. Deep backward integration into key detergent precursors insulated BASF from 2025 raw-material volatility. With anticipated 2025 sales of approximately €59.7 billion, its Nutrition & Care segment continues to provide resilient growth amid broader industrial softness.

Nouryon accelerates renewable surfactants with FinnFix PB MAX and CMC leadership

Nouryon has emerged as a sustainability-first leader in detergent chemicals, particularly in surfactants and chelating agents. In February 2026, the company launched FinnFix® PB MAX, the industry’s first carboxymethylcellulose (CMC) featuring a 100% renewable carbon index, strengthening its position in eco-friendly laundry formulations. As the world’s largest CMC producer, Nouryon supplies high-performance anti-redeposition agents critical for modern detergent pods and ultra-concentrated liquids. Its ISCC Plus-certified Delfzijl facility ensures full traceability for bio-based ingredients, supporting clean-label requirements. With deep heritage in cellulose chemistry and strong penetration in compact detergents, Nouryon is capitalizing on the shift toward low-dosage, high-efficiency cleaning systems.

Clariant AG strengthens Care Chemicals with regional localization and glucamide technologies

Clariant plays a pivotal role in detergent formulations through its Care Chemicals portfolio, supported by strong localization in Asia-Pacific and the Americas. In January 2026, the appointment of Marcelo Lu as President-Designate of Care Chemicals marked a renewed push for growth in post-pandemic demand markets. Clariant’s Synergen™ and Dispersogen® ranges, featuring glucamide-based technologies, are increasingly adopted in bio-based detergents and agricultural cleaning applications. Despite softer Q3 2025 conditions, Care Chemicals & Americas remains Clariant’s largest business unit, generating roughly CHF 2.2 billion annually. Strategic CHF 180 million investments in Huizhou, China have lifted local production to 70%, shielding margins from currency swings while supporting regional detergent manufacturing.

Evonik Industries advances biosurfactants through precision fermentation platforms

Evonik is redefining detergent chemistry through biotechnology-driven surfactants and precision fermentation. In early 2026, it introduced TEGO® XP 32156, a sophorolipid-based biosurfactant delivering strong cleaning performance with 100% biodegradability. Under its “Advance Precision Biosolutions” strategy, Evonik is replacing hazardous surfactants with ecosystem-friendly alternatives that also enhance washing efficiency. The company continues its strategic collaboration with Unilever to scale rhamnolipid surfactants, first commercialized via the Quix home cleaning brand, establishing skin-friendly bio-detergents at scale. Evonik has also committed to evaluating all products from its 2021 to 2023 acquisitions under CMSPLUS by end-2026, reinforcing sustainability governance across its detergent chemicals portfolio.

Croda International drives premium detergent innovation with 100% bio-based surfactants

Croda is a specialty chemicals innovator focused on high-value, bio-derived detergent ingredients, aligned with its ambition to become Climate, Land, and People Positive by 2030. The company leads in 100% bio-based surfactants, with its Atlas Point facility in the USA producing ingredients from bio-ethanol instead of petrochemicals. Croda aims to exceed 75% bio-based raw material usage by 2030, with 2026 priorities centered on replacing ethylene oxide derivatives. Serving the “Smart Science” segment, Croda supplies clean-label ingredients for hand soaps, dishwashing liquids, and premium laundry care. Its five global biotechnology labs support rapid development of niche, sustainable surfactants for next-generation home care formulations.

European Union (Germany & Netherlands): Digital Traceability and Biodegradability Redefine Market Access

The European Union is reshaping the detergent chemicals market through one of the most structurally significant regulatory overhauls in its history. On December 8, 2025, the Council of the European Union approved the revised Detergents and Surfactants Regulation, modernizing Regulation (EC) No 648/2004. A cornerstone of this update is the mandatory introduction of a Digital Product Passport (DPP) from 2026–2027. This requirement obliges detergent chemical manufacturers to provide digital, component-level traceability across the value chain, covering surfactants, builders, enzymes, polymers, and encapsulation materials. For producers operating in Germany and the Netherlands, this fundamentally elevates compliance from documentation-based reporting to real-time data transparency, influencing sourcing strategies, formulation design, and downstream brand partnerships.

Equally transformative are the expanded biodegradability mandates. The revised framework extends ultimate biodegradability requirements to film-forming agents and water-soluble capsule shells, directly impacting high-volume laundry pod and unit-dose formulations. This has accelerated reformulation activity across Europe, particularly among German chemical majors such as BASF and Evonik, both of which transitioned core surfactant portfolios to ISCC PLUS-certified mass-balance feedstocks in late 2025. These shifts are not cosmetic. They target an estimated 30% reduction in Scope 3 carbon intensity for European consumer packaged goods partners by 2026. In parallel, the EU’s late-2025 inclusion of microbial cleaning products within the detergent regulatory scope has opened a new compliance frontier, forcing manufacturers to integrate biosafety protocols alongside conventional chemical risk assessments.

China: Self-Sufficiency, AI Optimization, and Circular Feedstocks at Scale

China’s detergent chemicals industry is advancing through a tightly coordinated mix of industrial policy, digitalization, and capacity expansion. Under the 2025–2026 Petrochemical Work Plan issued by seven ministries led by the Ministry of Industry and Information Technology, the country is targeting a sustained 5% annual growth in chemical value addition. Within detergents, policy emphasis is squarely on localizing high-end specialty chemicals, including bio-based surfactants and electronic-grade cleaning agents, to reduce structural dependence on imported ethoxylates and linear alkylbenzene. By 2026, China aims to lift domestic self-sufficiency for advanced chemical intermediates beyond 90 %, a goal that is already influencing capital allocation in major surfactant hubs.

Operational efficiency is being unlocked through the AI + Petrochemicals initiative. In 2025, large anionic surfactant facilities in Jiangsu integrated real-time data nodes and predictive control systems, delivering reported energy efficiency gains of around 12%. This digital layer is reducing batch variability, optimizing sulfonation reactions, and lowering unit energy consumption, which is critical in a market where margins are increasingly shaped by regulatory and environmental costs. Sustainability-driven capacity expansion is also evident. In early 2025, BASF started up the world’s first commercial loopamid facility in Caojing, Shanghai, supplying 500 metric tons of recycled-content feedstock. While developed for textiles, loopamid is gaining traction as a circular raw material input for sustainable laundry and home care formulations. China’s detergent chemicals market is therefore evolving into a high-volume, high-efficiency system where digital manufacturing and circular feedstocks coexist at industrial scale.

India: Policy-Led Localization and Green Feedstock Experimentation

India’s detergent chemicals market is being reshaped by aggressive industrial policy execution and long-term feedstock innovation. By March 2025, realized investments under the Production Linked Incentive scheme reached approximately ₹1.76 lakh crore, creating tangible momentum in domestic manufacturing of surfactants, builders, and specialty detergent intermediates that were previously import-dependent. This has strengthened the Make in India supply chain, particularly for small and mid-sized formulators supplying regional FMCG brands and institutional cleaning segments.

Capability development is being reinforced through institutional infrastructure. As of September 2025, the Department of Chemicals and Petrochemicals had operationalized 18 Centres of Excellence focused on new detergent molecules, enzyme systems, and green polymer applications. These CoEs are acting as translational bridges between academic research and industrial-scale formulation, shortening commercialization cycles for low-foam, low-temperature, and biodegradable detergent chemistries. Looking ahead, India is also experimenting with upstream decarbonization. Leading petrochemical firms are piloting methane pyrolysis in 2026 to generate low-emission hydrogen, which can be integrated into ammonia and other nitrogen-based detergent intermediates. This positions India not only as a cost-competitive producer but also as a future supplier of lower-carbon detergent chemicals aligned with global sustainability expectations.

United States: Climate Policy and PFAS Elimination Reshape Formulation Pathways

In the United States, detergent chemicals demand is being redirected by climate policy and chemical safety legislation rather than volume expansion. Under the AIM Act, the EPA’s finalized 2026 allowance allocations have accelerated the phase-down of high-GWP solvents used in industrial and institutional cleaners. This has increased adoption of hydrofluoroolefin-based and alternative low-GWP solvent systems, particularly in heavy-duty and professional cleaning formulations. The regulatory signal is clear. Climate compliance is now a core determinant of solvent and surfactant selection in the U.S. market.

Chemical safety concerns are further amplifying this shift. State-level PFAS bans in California and New York, taking effect across 2025–2026, have forced detergent chemical suppliers to re-engineer stain repellents and fluorosurfactant systems for professional cleaning and foodservice applications. This has elevated R&D intensity around PFAS-free performance chemistries that can match legacy fluorinated systems. Supply chain resilience is emerging as a parallel theme. In 2025, P&G Chemicals announced a renewed portfolio centered on decarbonization solutions, supported by TÜV Rheinland-certified carbon footprint calculations for naturally derived oleochemicals. This reflects a broader U.S. industry trend toward transparent, verifiable sustainability metrics as a competitive differentiator in detergent chemical sourcing.

Comparative Summary: Detergent Chemicals Market by Region

Detergent Chemicals Market Country level Snapshot

|

Region

|

Primary Policy Driver

|

Strategic Industry Response

|

Structural Market Impact

|

|

European Union

|

Digital Product Passport and biodegradability rules

|

Mass-balance surfactants, microbial cleaners

|

Compliance-led reformulation

|

|

China

|

Self-sufficiency and AI manufacturing

|

Localized specialty surfactants, digital plants

|

Scale with efficiency

|

|

India

|

PLI-driven localization

|

Domestic surfactant and builder production

|

Import substitution

|

|

United States

|

AIM Act and PFAS bans

|

Low-GWP solvents, PFAS-free chemistries

|

Safety and climate-led innovation

|

Detergent Chemicals Market Report Scope

Detergent Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$69.6 Billion

|

|

Market Size (2034)

|

$109.8 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Chemical Type (Surfactants, Builders, Enzymes, Bleaching Agents, Specialty Additives), By Form (Liquid Detergents, Powder Detergents, Pods and Capsules, Gels and Pastes), By Application (Household Laundry, Dishwashing, Household Cleaning, Industrial and Institutional Cleaning, Personal Care Intermediates), By Sustainability Profile (Bio-Based Surfactants, Phosphate-Free Builders, Concentrated Formulations, Probiotic Cleaners)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., Clariant AG, Nouryon, Evonik Industries AG, Huntsman International LLC, Croda International Plc, Procter & Gamble Chemicals, Stepan Company, Sasol Limited, DuPont de Nemours, Inc., Novonesis Group, Godrej Industries Limited, Kao Corporation, China Petroleum & Chemical Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Detergent Chemicals Market Segmentation

By Chemical Type

- Surfactants

- Builders

- Enzymes

- Bleaching Agents

- Specialty Additives

By Form

- Liquid Detergents

- Powder Detergents

- Pods and Capsules

- Gels and Pastes

By Application

- Household Laundry

- Dishwashing

- Household Cleaning

- Industrial and Institutional Cleaning

- Personal Care Intermediates

By Sustainability Profile

- Bio-Based Surfactants

- Phosphate-Free Builders

- Concentrated Formulations

- Probiotic Cleaners

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Detergent Chemicals Industry

- BASF SE

- Dow Inc.

- Clariant AG

- Nouryon

- Evonik Industries AG

- Huntsman International LLC

- Croda International Plc

- Procter & Gamble Chemicals

- Stepan Company

- Sasol Limited

- DuPont de Nemours, Inc.

- Novonesis Group

- Godrej Industries Limited

- Kao Corporation

- China Petroleum & Chemical Corporation

*- List not Exhaustive