Market Overview: Expandable Polystyrene Packaging to Reach $32.1 Billion by 2034 at 9.4% CAGR

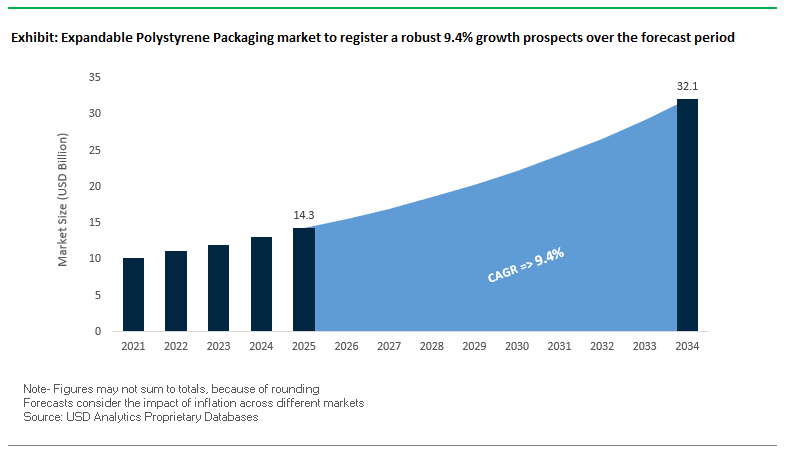

The global expandable polystyrene (EPS) packaging market is forecast to expand from $14.3 billion in 2025 to $32.1 billion by 2034, registering a robust CAGR of 9.4%. EPS packaging continues to play a vital role in logistics, food, pharmaceutical, and e-commerce sectors due to its shock absorption, insulation, and lightweight properties. For buyers and industry professionals, the market offers significant opportunities in sustainability integration, digitalized molding, and cold-chain logistics, positioning EPS as both a cost-effective and high-performance packaging solution.

Key Insights for Industry Stakeholders:

- E-commerce Growth: Rising demand for insulated packaging for perishable and fragile goods is driving strong adoption of molded EPS solutions.

- Lightweighting Focus: Manufacturers are optimizing material thickness to cut costs and reduce shipping weight while maintaining protective strength.

- Cold-Chain Applications: EPS is increasingly essential in food and pharmaceutical logistics, ensuring temperature-sensitive reliability.

- Smart Manufacturing: Digitally controlled molding technologies are improving accuracy, reducing material waste, and enabling custom EPS packaging designs.

Market Analysis: Recycling, Mergers, and Capacity Expansions Shape EPS Packaging

The EPS packaging industry is undergoing a rapid transformation, characterized by strategic mergers, recycling investments, and sustainability-driven innovations.

In June 2025, Epsilyte announced a strategic acquisition to expand capacity and strengthen its footprint in North America, underscoring the company’s ambition to scale its EPS resin supply for protective packaging. In March 2025, Versalis, the chemical arm of Eni, inaugurated a new recycled polymer production plant in Porto Marghera, Italy, with a 20,000-ton annual capacity, dedicated to producing recycled expandable polystyrene (r-EPS). That same month, NOVA Chemicals was integrated into a $13.4 billion merger led by ADNOC and OMV, forming Borouge Group International (BGI), a new global polyolefins powerhouse set to expand influence in packaging markets.

In January 2025, BASF exited its Styrodur business to concentrate on Neopor® and Styropor® EPS brands, committing to a 50,000-ton annual capacity expansion by 2027. This followed BASF’s October 2024 announcement of investment in Neopor expansion at its Ludwigshafen site. In September 2024, Versalis confirmed the launch of a Hoop® demonstration plant for advanced chemical recycling of mixed plastic waste, strengthening its circular economy portfolio. Earlier in April 2024, Versalis partnered with Crocco to introduce sustainable food packaging films incorporating recycled plastics, reflecting the industry’s drive toward food-grade circular applications.

Other significant moves include NOVA Chemicals’ March 2024 launch of a Plastics Circularity Centre of Excellence, a hub for developing advanced recycling technologies, and Sonoco’s December 2024 divestiture of its thermoformed packaging business for $1.8 billion, refocusing on industrial paper and molded pulp packaging, including EPS-related segments.

Trends and Opportunities Transforming the Expandable Polystyrene (EPS) Packaging Market

Regulatory Pressure and Material Substitution in Key Applications

The expandable polystyrene (EPS) packaging market is undergoing a regulatory-driven transformation, as global bans and restrictions on single-use plastics reshape material choices in packaging. Unlike voluntary sustainability initiatives, this shift is primarily compliance-based, compelling manufacturers to re-engineer their product portfolios.

Across the United States, by late 2024, at least 12 states, including New York and Maryland, enacted legislation restricting or banning EPS foodservice containers and loose-fill packaging. Washington State’s ban, which took effect in June 2024, further illustrates the momentum of anti-EPS regulation. In Europe, the Single-Use Plastics Directive (SUPD) and broader Packaging and Packaging Waste Regulation (PPWR) are accelerating the phaseout of EPS in foodservice applications, while allowing limited exemptions for fish packaging and pharmaceutical uses due to EPS’s unmatched protective and insulation properties.

Corporate initiatives amplify these regulatory trends. New York City’s 2019 EPS ban reduced foam waste by more than 50%, showing how municipal-level action directly alters waste streams. Major foodservice and retail brands are also proactively eliminating EPS packaging to meet 2030 recyclability and sustainability pledges, intensifying the transition toward molded fiber, paper-based, and other alternatives. This dual push from regulators and corporations is restructuring the global EPS demand landscape.

Innovation in Advanced Recycling and Chemical Repurposing Technologies

While bans present challenges, the EPS packaging industry is countering with significant investment in advanced recycling technologies to transform EPS waste into valuable raw materials. Unlike mechanical recycling, which struggles with contaminated EPS, chemical depolymerization and solvent-based technologies are unlocking closed-loop solutions.

A landmark example is Versalis’s Porto Marghera plant in Italy, operational since March 2025, with capacity to recycle 20,000 tonnes per year of post-consumer EPS and crystal polystyrene, focusing on fish boxes. Similarly, the PolyStyreneLoop project in the Netherlands, involving over 70 partners, has successfully demonstrated a solvent-based process to dissolve EPS, remove impurities such as flame retardants, and produce purified feedstock for new applications. Academic research is also broadening horizons one study showed EPS waste converted into nonwoven fabrics through melt jet spinning, presenting new value streams for sectors like filtration and construction.

These breakthroughs are building the foundation of a circular economy for EPS packaging, where waste is no longer a liability but a renewable feedstock for virgin-equivalent polymers or new materials. For stakeholders, these innovations not only mitigate regulatory risk but also reposition EPS as a sustainable and technologically advanced packaging option.

Development of High-Performance, Sustainable Protective Packaging

Despite headwinds in consumer packaging and foodservice, the industrial, medical, and e-commerce sectors provide a major opportunity for EPS to reinforce its market position as a lightweight, high-performance protective packaging material. Its superior cushioning, shock absorption, and insulation properties make it indispensable for safeguarding fragile electronics, medical devices, and temperature-sensitive products.

Life Cycle Assessment (LCA) studies validate EPS’s environmental efficiency compared to paper-based or molded pulp alternatives. One study demonstrated that an EPS wine shipper used 5.67 times less water than a molded pulp equivalent, while also requiring less energy and producing a lower carbon footprint. Given that EPS is 98% air, its lightweight structure minimizes transportation emissions by reducing fuel use per shipment a direct advantage in global logistics and e-commerce operations.

As sustainability narratives dominate boardroom agendas, promoting EPS as a carbon-efficient protective packaging solution rather than a waste challenge could reposition the material favorably. By coupling LCA-backed data with innovation in design, EPS can remain a competitive option for industries that prioritize both performance and environmental accountability.

Expansion into Circular Economy Models via Take-Back and Repurposing

Another major growth avenue lies in establishing closed-loop EPS recycling systems, particularly in B2B channels where packaging volumes are high and logistics networks can be centralized. Dedicated take-back programs, densification technologies, and advanced recycling alliances are making circular models both technically and economically feasible.

In Europe, the European Expanded Polystyrene Group (EUMEPS) reports that more than 30% of EPS waste is already recycled, with fish boxes in some regions achieving recycling rates of up to 90% due to efficient collection systems. To overcome EPS’s traditionally high transportation costs, companies are deploying on-site densifiers and compactors capable of reducing material volume by up to 90%. This densification makes reverse logistics viable and lowers recycling costs.

Competitive Landscape: Key EPS Packaging Companies Driving Innovation and Circularity

The expandable polystyrene packaging market is led by global chemical companies and specialized EPS producers who differentiate through sustainable innovations, recycling investments, and product performance.

BASF SE Strengthening Core EPS Brands with Neopor Expansion

BASF remains a global leader in EPS with flagship brands Styropor® and Neopor®, including graphite-infused Neopor for superior insulation. The company recently exited its Styrodur business to focus on core EPS growth and announced a 50,000-ton Neopor capacity boost by 2027 at Ludwigshafen. BASF also introduced Neopor F 5 Mcycled™, containing 10% recycled content, aligning with its circular economy strategy. Its innovation-driven approach positions it as a key enabler of sustainable EPS packaging.

Versalis S.p.A. Advancing Chemical Recycling and r-EPS for Food Applications

Versalis, Eni’s chemical subsidiary, is expanding EPS packaging sustainability with its Versalis Revive® product line, including food-grade EPS with 75% recycled content. In March 2025, it opened a 20,000-ton r-EPS facility in Italy, reinforcing its recycling leadership. Its Hoop® technology for chemical recycling of mixed plastics and its partnership with Crocco for sustainable food packaging highlight Versalis’ strong positioning in closed-loop EPS solutions.

NOVA Chemicals Corporation Expanding Recycling and Merging into Borouge Group International

NOVA Chemicals plays a central role in polyolefins and EPS-related packaging, with a growing emphasis on circularity. In March 2025, it was integrated into Borouge Group International through a $13.4 billion merger, giving it expanded reach in polyolefins and EPS packaging markets. NOVA is actively developing advanced recycling plants in Canada and launched a Centre of Excellence for Plastics Circularity in March 2024, underscoring its long-term strategy to lead in sustainable EPS packaging.

StyroChem (Epsilyte Holdings) Strengthening North American EPS Leadership

StyroChem, acquired by Epsilyte Holdings in 2021, has been integrated into one of the largest EPS producers in North America. With three production sites, StyroChem brings high-quality resins for protective packaging and expertise in efficiency-driven manufacturing. The June 2025 acquisition announcement by Epsilyte further strengthens its market position, making the combined entity a dominant player in sustainable, high-R value EPS packaging solutions.

Alpek S.A.B. de C.V. Circular Economy Initiatives Driving EPS Growth

Alpek is a major Latin American chemical company with a diverse plastics portfolio including EPS. Its Circular Economy program focuses on expanding mechanical and chemical recycling capacities and introducing biodegradable EPS alternatives. In 2025, Alpek announced the closure of its PET facility in North Carolina as part of portfolio optimization, redirecting focus toward core materials like EPS. With strong recycling initiatives and partnerships, Alpek is positioning itself as a sustainability-forward EPS producer.

Expandable Polystyrene Packaging market Share Insights

Shapes and Molded Products Lead Market Share by Product Type in EPS Packaging

In 2025, shapes and molded products account for 45% of the expandable polystyrene (EPS) packaging market, making them the largest product type, followed by blocks at 30%, with loose fill and sheets contributing smaller shares. Molded EPS maintains leadership as a precision-fit solution for electronics, appliances, and medical devices, where its cushioning properties prevent costly damage during shipping. Blocks continue to play a significant role in construction insulation and industrial packaging, while loose fill has entered a managed decline due to regulatory bans and consumer backlash against single-use plastics. Boards and sheets remain niche but persist in protective layers for flat-pack goods. Overall, product segmentation reflects EPS’s ability to defend share in industrial protective niches despite regulatory headwinds affecting consumer-facing formats.

Protective Packaging Dominates Market Share by Application in EPS Packaging

By application, protective packaging commands 40% of the EPS packaging market in 2025, solidifying its position as the material’s core strength. Electronics, appliances, and fragile goods rely on EPS’s unmatched shock absorption, ensuring its continued use where performance outweighs environmental criticism. Food and beverage packaging, which holds around 25%, faces steep regulatory decline, particularly in single-use items like coffee cups and meat trays, though functional demand persists in certain supply chains. EPS also retains relevance in electronics, automotive, and medical shipments, where insulation and performance under pressure are critical. While EPS is under growing replacement pressure from molded fiber and paper-based alternatives, its protective packaging applications highlight why it continues to secure share in performance-driven markets even amid a long-term transition.

United States: State-Level Bans and Advanced Recycling Driving EPS Packaging Innovation

The U.S. expandable polystyrene (EPS) packaging market is undergoing significant transformation due to state-level bans and municipal regulations. As of mid-2025, over 12 states and numerous cities have prohibited EPS foodware and packaging, driving companies to invest in lightweight, cost-effective, and recyclable alternatives.

To complement regulatory compliance, manufacturers are increasingly investing in advanced recycling infrastructure and circular economy initiatives. Companies like BASF have expanded offerings such as Neopor F 5 Mcycled, a recycled-content EPS granulate incorporating post-consumer waste. The e-commerce boom is a major application driver, as EPS is widely used for protective and temperature-sensitive packaging for electronics, pharmaceuticals, and fragile goods. Additionally, government initiatives like the United States Innovation and Competition Act support EPS applications in high-value protective packaging, particularly for sensitive semiconductor components.

Germany: Pioneering Circular Economy and Energy-Efficient EPS Solutions

Germany’s EPS packaging industry leads Europe’s transition toward a circular economy, emphasizing high recycling rates and post-consumer recycled (PCR) content in products. Companies are innovating to improve mechanical performance and barrier properties of EPS sheets and films, aligning with European Green Deal objectives.

A notable technological advancement is graphitic or "grey" EPS, enhanced with graphite additives for superior thermal insulation. This material is widely used in construction applications and temperature-controlled food and beverage packaging. Heavy investment in research and development allows German firms to optimize production processes and develop sustainable EPS solutions that balance performance with environmental responsibility.

China: Scaling Production and Recycling Infrastructure for Global Demand

China’s EPS packaging market is driven by its vast production and export capacity, serving both domestic needs and international markets. As a global manufacturing hub, China produces a wide range of EPS products at competitive prices, making it a key player in the global EPS industry.

Government policies targeting plastic pollution and waste reduction are accelerating the development of recycling infrastructure. Advanced technologies, including AI-powered sorting systems, are being adopted to enhance efficiency and accuracy in EPS recycling. This integration of automation and high-tech solutions ensures compliance with regulations while meeting the growing demand from domestic and export markets.

Japan: High-Quality, Reusable, and Sustainable EPS Packaging

The Japanese EPS packaging market emphasizes reusability and sustainable design, with R&D focused on material optimization to reduce waste and carbon footprint. Innovative designs for EPS cushions and packaging components allow multiple uses while maintaining product protection.

Precision and high-quality manufacturing are essential, particularly for electronics and automotive sectors, where EPS packaging must provide shock and vibration protection for high-value components. Japanese manufacturers combine sustainability with performance, creating solutions that are both eco-friendly and reliable.

United Kingdom: Policy-Driven Sustainability and Recycling Awareness

The UK EPS packaging market is addressing public misconceptions regarding EPS recyclability. Initiatives by the British Plastics Federation (BPF), such as interactive maps of recycling facilities, aim to improve awareness and encourage investment in standardized recycling infrastructure.

Policy drivers like the Plastic Packaging Tax (PPT) incentivize the use of post-consumer recycled content (PCR), pushing EPS manufacturers toward more sustainable production practices. These developments highlight the UK market’s emphasis on regulatory compliance, recycling optimization, and environmental responsibility.

Expandable Polystyrene Packaging Market Report Scope

Expandable Polystyrene Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.3 Billion

|

|

Market Size (2034)

|

$32.1 Billion

|

|

Market Growth Rate

|

9.4%

|

|

Segments

|

By Material Type (White EPS, Grey EPS), By Product Type (Blocks, Shapes & Molded Products, Boards & Sheets, Loose Fill), By Application (Protective Packaging, Food & Beverage Packaging, Automotive, Electronics & Electricals, Medical & Pharmaceuticals, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Alpek S.A.B. de C.V., TotalEnergies SE, SABIC, Synthos S.A., NOVA Chemicals Corporation, Versalis S.p.A., Ineos Group, Kaneka Corporation, SIBUR, EPSILON EPS, Atlas Roofing Corporation, Plasti-Fab Ltd., ACH Foam Technologies (A brand of Atlas Roofing Corporation), BEWi ASA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Expandable Polystyrene Packaging Market Segmentation

By Material Type

By Product Type

- Blocks

- Shapes & Molded Products

- Boards & Sheets

- Loose Fill

By Application

- Protective Packaging

- Food & Beverage Packaging

- Automotive

- Electronics & Electricals

- Medical & Pharmaceuticals

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Expandable Polystyrene Packaging market

- BASF SE

- Alpek S.A.B. de C.V.

- TotalEnergies SE

- SABIC

- Synthos S.A.

- NOVA Chemicals Corporation

- Versalis S.p.A.

- Ineos Group

- Kaneka Corporation

- SIBUR

- EPSILON EPS

- Atlas Roofing Corporation

- Plasti-Fab Ltd.

- ACH Foam Technologies (A brand of Atlas Roofing Corporation)

- BEWi ASA

*List not Exhaustive

Research Coverage

This report investigates the global expandable polystyrene (EPS) packaging market, analyzing breakthroughs in digitalized molding, high-performance protective solutions, and sustainable recycling technologies. USDAnalytics’ analysis reviews market transformations driven by mergers, capacity expansions, regulatory shifts, and circular economy initiatives, highlighting opportunities for manufacturers, logistics operators, and e-commerce stakeholders to optimize cost efficiency and product protection. This report is an essential resource for packaging engineers, supply chain professionals, sustainability managers, and investors seeking actionable insights into emerging EPS applications, innovative recycling techniques, and material substitution strategies. It provides a comprehensive view of historical trends from 2021–2024 and forecasts through 2034, emphasizing adoption of white and grey EPS, molded products, blocks, and loose-fill solutions across protective, food & beverage, medical, and electronics applications. The study also highlights competitive dynamics among leading global players driving technological advancement, circularity initiatives, and performance improvements, ensuring readers gain clarity on investment priorities, regulatory compliance, and high-growth opportunities in the evolving EPS packaging landscape.

Scope Highlights:

- Segmentation: By Material Type (White EPS, Grey EPS); By Product Type (Blocks, Shapes & Molded Products, Boards & Sheets, Loose Fill); By Application (Protective Packaging, Food & Beverage Packaging, Automotive, Electronics & Electricals, Medical & Pharmaceuticals, Other Applications)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historical & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies Covered: Profiles and analysis of 15+ companies, including BASF SE, Alpek S.A.B. de C.V., TotalEnergies SE, SABIC, Synthos S.A., NOVA Chemicals Corporation, Versalis S.p.A., Ineos Group, Kaneka Corporation, SIBUR, EPSILON EPS, Atlas Roofing Corporation, Plasti-Fab Ltd., ACH Foam Technologies, BEWi ASA

Methodology

The report employs a structured methodology combining primary and secondary research to deliver an authoritative perspective on the EPS packaging market. Primary research included interviews with packaging engineers, operations managers, sustainability specialists, and supply chain directors to validate trends in recycling, circularity adoption, and material innovation. Secondary research leveraged corporate annual reports, regulatory filings, industry whitepapers, patent databases, and academic studies to assess advances in EPS molding technologies, chemical recycling, and protective packaging performance. Market sizing and forecasts were generated using top-down and bottom-up approaches, integrating factors such as material production capacity, sector-specific adoption rates, and regional demand trends. Competitive benchmarking examined mergers, acquisitions, sustainability initiatives, and product innovation. USDAnalytics ensured cross-verification and triangulation of data, providing industry professionals with insights to optimize operational efficiency, mitigate regulatory risk, and implement advanced, sustainable EPS packaging solutions.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.