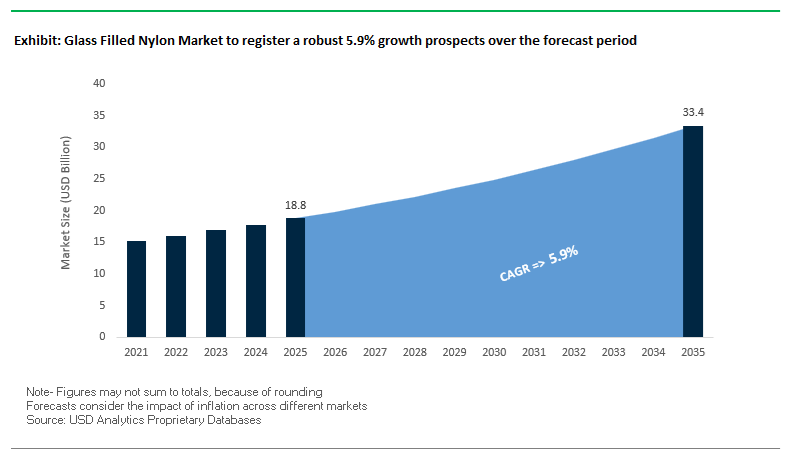

The Glass Filled Nylon Market, valued at USD 18.8 billion in 2025, is forecast to reach USD 33.4 billion by 2035, expanding at a strong CAGR of 5.9%. The market’s rapid acceleration is rooted in the increasing adoption of glass-fiber-reinforced polyamides across automotive, electrical & electronics, industrial machinery, and e-mobility systems—driven by the need for lightweighting, thermal stability, dimensional accuracy, and cost-efficient metal replacement.

Industry developments show a decisive shift toward circular materials, new PA chemistries, and high-performance composite solutions that support complex structural and thermal challenges. In November 2025, Envalior introduced Durethan® ECO and Durethan® BLUE PA6 grades with up to 90% ISCC PLUS-certified recycled/bio-based content, setting a new benchmark in sustainable glass-filled polyamides for automotive, consumer and E&E components. The aligns with OEM sustainability mandates and emerging lifecycle carbon regulations. Similarly, September 2025 saw BASF launch Ultramid® H, a specialty PA grade with high water permeability, showcasing the industry’s expansion into niche, functional applications beyond structural uses.

Sustainability initiatives strengthened further in March 2025, when BASF confirmed commercial-scale production of bio-based Ultramid® grades replacing 100% fossil resources via mass-balance methods. The shift toward biologically derived PA feedstock is directly aligned with global decarbonization and net-zero manufacturing targets. In parallel, application-oriented innovations continued: November 2024 saw Celanese validate its reinforced PA66 coolant hub that achieved a 50% assembly space reduction, proving the role of glass-filled PA in thermal management miniaturization. September 2024 highlighted Syensqo’s launch of Omnix® ECHO—PA grades with up to 98% recycled content, aimed at high-performance consumer goods and electronics.

Performance advancements persisted into early 2024. LyondellBasell introduced Schulamid ET100 in July 2024, engineered to deliver superior surface aesthetics, reducing fiber visibility—a breakthrough for visible automotive interior parts. In April 2024, Celanese unveiled Zytel XMP70G50, a 50% GF PA66 compound tailored for high-heat EV structural applications, dramatically enhancing operational durability. The industry continues to focus on collaborative innovation, demonstrated by Syensqo and ZF’s ongoing partnership to develop structural steering components for the Volvo EX90, incorporating recycled-content HPPA compounds for sustainable metal substitution.

For industry buyers, the central strategic questions involve identifying which PA6/PA66 GF grades offer the right balance of strength, processability, long-term heat aging resistance, and sustainability credentials for next-generation high-load and high-temperature components.

Technical performance remains the core differentiator in procurement, with GF-reinforced nylon grades easily achieving 245 MPa tensile strength, 250°C HDT, and up to 80% stiffness enhancements compared to unfilled nylon resins. The makes glass-filled PA an essential choice for OEMs designing engine components, structural EV brackets, battery housings, cooling systems, e-motor modules, and high-voltage connectors. Additionally, the industry’s move toward ISCC PLUS-certified recycled and bio-based feedstock is reshaping sourcing strategies, pushing compounders to deliver sustainable GF nylon offerings without compromising mechanical integrity.

- Structural strength leadership: PA66 GF50 compounds deliver up to 245 MPa tensile strength, enabling replacement of aluminum in high-load components.

- Automotive lightweighting: Switching from die-cast aluminum to GF50 PA66 achieves ≈45% weight reduction with equal durability—critical for EV range optimization.

- High-heat suitability: GF-reinforced PA66 maintains HDT up to 250°C at 1.8 MPa, supporting continuous use in under-hood and thermal management systems.

- Dimensional accuracy: Glass fiber reinforcement limits mold shrinkage to 0.1%–0.5%, essential for precision housings and multi-component assemblies.

- Structural stiffness boost: GF loading increases flexural modulus by up to 80%, enabling thinner-walled parts and high-flow injection molding of complex geometries.

High-Temperature Electrification Demands and Precision Robotics Fuel Advanced Formulations in the Glass Filled Nylon Market

The Glass Filled Nylon Market is entering a new phase of accelerated innovation as electrified mobility, industrial robotics, hydrogen infrastructure, and premium consumer electronics push performance requirements far beyond the capabilities of conventional engineering plastics. As OEMs transition to lightweight composite solutions with superior thermal, mechanical, and functional properties, glass-fiber-reinforced nylons-particularly long-glass-fiber (LGF) and high-glass-content grades-are becoming essential for structural, chemical-resistant, and electrically functional applications. The following trends and opportunities deliver a deeply analytical, fact-rich, SEO-optimized evaluation tailored for high-level industry stakeholders.

Trend 1 - Long-Glass-Fiber and High-Temperature Glass Filled Nylon Grades Become Essential for EV Powertrain and Thermal-Load Components

The electrification of automobiles is redefining the material requirements for under-the-hood components. Electric drive units (EDUs), battery mounting structures, inverter housings, and high-voltage architectural systems demand elevated thermal stability, creep resistance, and fatigue performance-conditions ideally suited for advanced glass-filled nylon solutions.

High-performance PA66 GF30+ formulations and specialty nylon blends maintain mechanical integrity at continuous-use temperatures of 120–150°C, ensuring parts retain dimensional stability in high-heat zones of the EV drivetrain. Long-glass-fiber (LGF) technology further enhances durability by creating a robust internal fiber skeleton that withstands 20× more flexural cycles than short-fiber grades, enabling components to survive sustained vibration and mechanical loading.

OEMs increasingly specify PA66 GF50 grades, which deliver exceptional rigidity and tensile strengths approaching 180 MPa, unlocking applications historically restricted to metals. Thermal Gravimetric Analysis (TGA) confirms that 30% GF-reinforced Nylon 6/6 exhibits degradation onset between 440–490°C, providing ample safety margin above EV operating conditions.

As EV architectures evolve toward higher power densities and compact thermal zones, LGF nylon materials are replacing aluminum and die-cast metals across battery frames, structural brackets, clutch housings, and power electronics enclosures-anchoring the material’s strategic role in automotive electrification.

Trend 2 - Glass Filled Nylon Replaces Metals in Industrial Robotics and Automation End-Effectors for Weight and Performance Gains

Industrial automation systems increasingly rely on lightweight, high-stiffness materials to achieve faster cycle times, reduced energy consumption, and enhanced precision. Glass Filled Nylon-especially 30–40% GF grades and LGF variants-is becoming a preferred metal replacement material in robotic end-effectors, grippers, and precision tooling.

With densities of 1.3–1.5 g/cm³, GF Nylon weighs roughly half as much as aluminum (2.7 g/cm³), enabling 40–50% mass reduction when replacing machined metal components. This reduction in inertia significantly improves robot acceleration, deceleration, and throughput.

GF nylon grades reach flexural strengths of up to 190 MPa, providing excellent stiffness-to-weight ratios essential for rapid, repetitive motion. Superior creep resistance ensures that dimensional accuracy-often required within micron-level tolerances-is preserved over long operational cycles in factory automation systems.

Injection molding enables part consolidation, eliminating multi-part assemblies, fasteners, and secondary machining steps. This not only reduces manufacturing cost but also enhances geometric repeatability-critical for high-performance robotics. As smart factories expand globally, the shift from metal to engineered polymer composites in automation tooling is accelerating unmet demand for Glass Filled Nylon.

Opportunity 1 - Chemically Resistant Glass Filled Nylon Grades for Hydrogen and Concentrated Solar Power (CSP) Infrastructure

The global shift toward hydrogen and renewable energy infrastructure is creating highly technical performance requirements that standard nylon grades cannot meet. This is opening a substantial market opportunity for chemically resistant, reinforced polyamide composites.

Hydrogen storage and transport systems require materials with low gas permeability. Enhanced PA6 composites containing 2.0 wt% graphene have demonstrated a 33.2% reduction in helium permeability, making them strong candidates for valves, liners, and fittings in hydrogen fuel systems and Type IV pressure vessels.

For concentrated solar power (CSP) plants, components must withstand corrosive heat transfer fluids, molten salts, and solar-driven oxidation. Specialty grades such as PA12-GF and semi-aromatic polyamides (PPAs) deliver superior chemical resistance and long-term dimensional stability under harsh environmental conditions.

Graphene-modified PA6 compounds also show dramatic improvements in toughness-130.6% increase in normal-temperature impact strength and 111.7% increase at low temperatures-supporting the demanding operational envelope of hydrogen infrastructure ranging from −40°C to +85°C.

With clean energy markets scaling quickly, the development of chemically robust Glass Filled Nylon formulations represents one of the most commercially strategic pathways for polymer producers.

Opportunity 2 - Electrically Conductive & Aesthetically Enhanced GF Nylon Grades for Consumer Electronics and Smart Devices

The premium consumer electronics sector is driving significant innovation in both surface aesthetics and electrical functionality of Glass Filled Nylon formulations, opening new opportunities in device housings, wearable products, and compact smart hardware.

Traditional GF nylon surfaces reveal visible fibers (“fiber prominence”), often requiring secondary finishing. New formulations using specialized glass fibers, optimized coupling agents, and advanced injection-molding techniques can deliver smooth, high-gloss, metallic-like finishes directly from the mold, eliminating costly painting steps and producing a premium, OEM-grade appearance.

Electrically conductive GF Nylon compounds incorporating nickel-coated carbon fibers, stainless-steel fibers, or carbon nanotubes are also gaining momentum. These materials provide:

- EMI shielding effectiveness >50 dB across 30 MHz–1 GHz

- Weight reductions up to 40% compared to aluminum

- Stable surface resistivity suitable for static dissipation and circuit protection

These engineered composites are increasingly used in ADAS components, IoT enclosures, drones, high-strength electronic housings, and medical devices requiring integrated structural and electromagnetic performance.

As device miniaturization and functional integration accelerate, the demand for advanced GF Nylon with premium finishes and built-in conductivity is projected to grow rapidly-particularly in the markets for wearables, consumer robotics, smart home equipment, and next-generation connected devices.

Glass Filled Nylon Market Share Analysis

Market Share by Polyamide Type: PA6 Leads Through Cost Efficiency, Superior Processability, and Robust Mechanical Toughness

Polyamide 6 (PA6) captures the largest 48% share in the Glass Filled Nylon Market, driven by its optimal balance of cost, processing efficiency, and mechanical performance, which makes it the preferred polyamide for high-volume and general-purpose engineering applications. PA6’s material economics play a decisive role in its dominance: it is inherently more cost-effective than PA66 due to lower raw material costs and reduced energy requirements during molding. Its lower melting point (~220°C vs. ~260°C for PA66) enables faster cycle times in injection molding, reducing electricity use and improving throughput—key advantages for large-scale manufacturers in consumer goods, power tools, electronics, and industrial components. From a mechanical standpoint, unreinforced PA6 offers greater impact resistance (toughness) than PA66, and while glass reinforcement narrows the performance gap, glass-filled PA6 retains sufficient toughness for parts subjected to dynamic loading and shock absorption. These properties make PA6 a workhorse material for housings, brackets, gears, and furniture components where strength, durability, and cost efficiency must align. Its robust global supply chain and versatility across glass loadings further support its widespread adoption. Collectively, these attributes position PA6 as the dominant nylon type in glass-filled formulations, solidifying its leadership in markets prioritizing manufacturability and cost-effective structural performance.

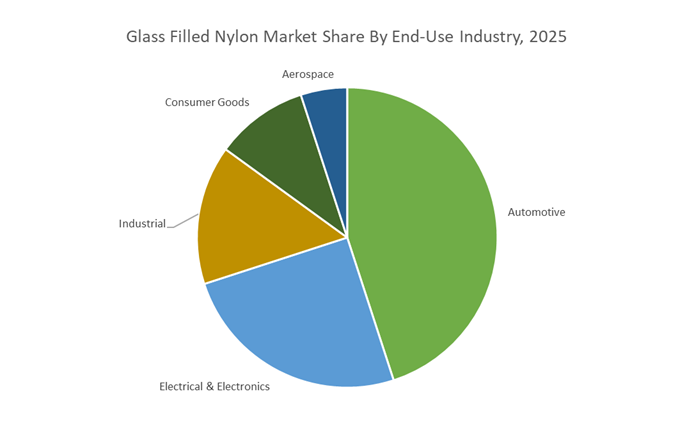

Market Share by End-Use Industry: Automotive Dominates Through Aggressive Lightweighting and High-Temperature Performance Requirements

The Automotive sector commands a leading 45% share of the Glass Filled Nylon Market, reflecting the industry’s deep reliance on high-strength, lightweight polymers to meet modern efficiency, emissions, and electrification targets. Automakers increasingly replace metal components with glass-filled nylon due to its ability to provide up to 50% weight reduction in critical parts such as intake manifolds, engine covers, cooling fan shrouds, and radiator end tanks—weight savings that directly translate into improved fuel economy for internal combustion engine vehicles and extended driving range for electric vehicles. Glass-filled nylon also excels in thermal environments, with automotive-grade PA6-GF and PA66-GF materials capable of sustaining 100°C–150°C continuous operating temperatures, while high-performance grades withstand up to 250°C for short durations, making them ideal for under-the-hood components exposed to thermal cycling and chemical exposure.

Equally important is the material’s structural capability: 30% glass-filled nylon grades exceed 200 MPa in tensile strength, enabling load-bearing brackets, oil pans, and structural housings to meet OEM durability standards while maintaining low weight and corrosion resistance. As vehicle platforms continue shifting toward electrification, the need for thermally stable, electrically insulating, flame-retardant, and dimensionally stable materials further accelerates demand for glass-filled nylon across battery enclosures, high-voltage connectors, and EV thermal management assemblies. With automotive OEMs pursuing long-term lightweighting strategies and modular polymer-intensive design architectures, the sector’s dominance in glass-filled nylon consumption remains firmly anchored and continues to expand.

Country Analysis: Global Glass Filled Nylon Development Hubs

Germany / European Union: Sustainability Mandates and High-Heat PA66 Driving Advanced Glass-Filled Nylon Adoption

The European Union continues to serve as a global frontrunner in Glass Filled Nylon (PA GF) innovation, driven by stringent emissions regulations, aggressive decarbonization strategies, and the region’s strong industrial commitment to circular materials. Major polymer producers such as BASF are spearheading the commercialization of bio-based polyamide grades, with the company confirming in its 2024 Report that specific Ultramid® PA66 materials now replace 100% of fossil feedstocks via mass balance certification. This directly aligns with the automotive industry’s transition toward net-zero vehicle manufacturing, enabling OEMs to achieve lightweighting targets without compromising mechanical performance.

Component consolidation and lightweight structural engineering are becoming defining trends across the EU’s automotive ecosystem. In August 2024, Syensqo, in collaboration with ZF, secured an innovation award for a specialized polyamide steering system component used in the Volvo EX90 EV, demonstrating how glass-filled polyamides replace complex multi-material assemblies while improving design precision. Regulatory pressure from the EU Green Deal further accelerates the replacement of heavy metals across sectors, strengthening long-term demand for high-strength PA66 GF composites in industrial machinery, transportation, and energy-efficient equipment. European producers are also advancing specialized high-fiber formulations: Ensinger’s TECAMID 66/X GF50, featuring 50% glass fiber reinforcement and aromatic stabilizers, can withstand temperatures up to 130°C (266°F)—meeting the needs of demanding mechanical and thermal environments across automotive, robotics, and heavy-duty industrial systems.

China: EV Manufacturing Scale and Rapid Localization of Long Glass Fiber (LGF) Reinforced PA66

China is the largest and fastest-growing global hub for Long Glass Fiber (LGF) reinforced nylon, fueled by the explosive expansion of domestic EV production and supply-chain localization strategies. The country’s dominant EV manufacturers—spanning EV battery platforms, high-voltage architectures, and structural modules—are increasingly specifying LGF-reinforced PA6 and PA66 for critical components such as battery mounting brackets, underbody crash structures, front-end modules, and high-voltage connector housings. Chinese EV makers require materials with superior dimensional stability, impact resistance, long-term fatigue behavior, and heat-aging durability, making LGF nylon a preferred choice over short-fiber and metal alternatives.

Domestic composite suppliers, including Xiamen LFT Composite Plastic Co., Ltd. (LFT-G®), continue to expand capacity for Long Carbon Fiber (LCF) and Long Glass Fiber (LGF) reinforced nylon compounds optimized for injection molding of complex automotive geometries. This supports China’s ambition to reduce reliance on imported engineering resins. Local R&D is heavily focused on fiber–matrix interface optimization, utilizing advanced sizing agents and coupling chemistries to enhance tensile strength, flexural modulus, and fatigue resistance. These innovations help Chinese-produced LGF nylon compete with international engineering polymers, strengthening China’s position as a global technology center for lightweight EV-ready composite materials.

United States: Metal Replacement and High-Load Structural Adoption Accelerating PA66 GF Market Penetration

The United States market emphasizes structural, high-load-bearing applications where Glass Filled Nylon’s strength-to-weight ratio enables extensive metal replacement in automotive, industrial, and infrastructure components. A strong example is Celanese Corporation’s high-performance PA66 grade, showcased at Chinaplas 2024, which enabled the 2025 Ford Mustang Mach-E to replace a multi-part metal-and-plastic coolant distribution system with a single consolidated polyamide component. This redesign achieved a 50% reduction in packaging space, simplified assembly, and improved fluid management—highlighting the U.S. automotive sector’s strategic shift toward modular plastic architectures supporting electrification.

In addition to EV cooling and structural modules, safety-critical components are increasingly being redesigned using glass-filled nylon. U.S. manufacturers are producing nylon-based brake pedals that reduce component weight by roughly 27% compared to metal, while maintaining high-impact performance and mechanical reliability. Industrial demand is rising as well: in 2023, the U.S. recorded a 7.3% increase in glass-filled nylon consumption within automated manufacturing systems, robotics, and fluid-handling equipment. These applications depend on PA GF materials for gear wheels, pump impellers, housings, and load-bearing mechanical elements where durability, fatigue resistance, and chemical stability are essential. With continued investment in design integration and electrification-driven lightweighting, the U.S. remains a core driver of advanced PA66 GF composite adoption.

Japan: High-Precision Electrical Components and Flame-Retardant PA Grades for Electronics Manufacturing

Japan maintains a specialized leadership position in precision-engineered Glass Filled Nylon for electronics, miniature machinery, and high-spec industrial systems requiring superior dielectric and thermal performance. Japanese manufacturers rely heavily on PA GF materials with high dielectric strength (>20 kV/mm) and UL V-0 flame retardancy, making them indispensable for connectors, relay housings, circuit breakers, and power distribution modules. These components demand exceptional dimensional stability, low warpage, high heat deflection temperature (HDT), and controlled moisture absorption, making high-performance PA12 and PA66 GF grades central to Japanese electronics manufacturing.

Material customization capabilities are particularly advanced in Japan. Leading suppliers produce tailored PA12/PA66 GF formulations with optimized fiber reinforcement, flame retardants, and impact modifiers to meet the stringent tolerances required for precision tooling and miniature electromechanical assemblies. Japanese OEMs also prioritize materials with low water absorption, vital for maintaining tight tolerances in humid environments and ensuring long-term electrical reliability. This specialization solidifies Japan's role as a premium hub for glass-filled nylon materials used in high-reliability electronics, robotics, automation components, and miniature mechanical assemblies.

Competitive Landscape: High-Performance Glass-Filled Nylon Suppliers Strengthening Global Market Position

The competitive environment for Glass Filled Nylon is defined by vertically integrated chemical producers, advanced compounders, and specialty PA innovators that differentiate through polymer chemistry, reinforcement technology, and application engineering. The advantage derives from the ability to deliver high-flow, high-strength, thermally stabilized, flame-retardant, and recycled-content GF nylon compounds tailored for modern E&E and EV platforms.

BASF leverages complete vertical integration across PA6 and PA66 production, ensuring full control over monomer quality, polymerization, and compounding. Its Ultramid® portfolio includes high-flow and heat-stabilized GF grades optimized for e-motor housings, battery modules, integrated cooling systems, and connector blocks. BASF is aggressively advancing sustainable materials through ChemCycling® and mass balance methods, producing PA grades that replace 100% fossil-based feedstocks. The Ultramid Advanced 6/4T series further strengthens BASF’s reach into high-temperature and chemically aggressive environments, supporting metal replacement in harsh automotive and industrial applications.

Celanese has consolidated the Zytel® business, strengthening its leadership in high-performance polyamides and glass-filled PA66 compounds. Its GF50 reinforced materials target EV chassis parts, structural brackets, cooling modules, and oil-contact systems, where long-term thermal aging and chemical resistance are critical. Zytel PLUS formulations deliver outstanding mechanical retention after exposure to hot oils and coolants. The company’s strategic focus includes thermal management innovations, validated by its PA66 coolant hub demonstrating significant packaging space reduction—a key differentiator for compact EV architectures.

Formed through the merger of LANXESS HPM and DSM Engineering Materials, Envalior commands an extensive global footprint in GF-reinforced PA6 and PA66. Its sustainability-driven product families—Durethan® ECO and BLUE—feature up to 90% recycled or bio-attributed content, aligning with European environmental regulations. Envalior’s strength lies in FR-engineered GF PA grades for high-voltage EV components, offering UL V-0 compliance and low tracking (CTI) without mechanical compromise. Its compounding expertise extends to hybrid systems combining glass fibers with minerals to balance surface finish, strength, and shrinkage control.

Syensqo (formerly Solvay’s specialty polymers division) dominates long glass fiber (LGF) polyamide technology with its Technyl brand. Technyl LITE unidirectional tapes and LGF PA compounds are widely adopted for load-bearing EV components, including brackets, housings, and steering systems. The company excels in hydrolysis-resistant and high-flow PA66 chemistries suitable for coolant circuits, humid environments, and continuous heat exposure. Its move toward high-recycled-content HPPA compounds reinforces its commitment to circularity in automotive and electronics sectors.

Ascend remains one of the world’s most significant fully integrated PA66 producers, ensuring stable resin and compound supply—critical during global PA66 shortage cycles. Its Vydyne® R series comprises GF-reinforced, heat-stabilized formulations used in radiator tanks, engine covers, transmission components, and E&E housings. The company’s increasing focus on halogen-free flame retardant (HFFR) GF nylon supports the rising demand for safer electrical enclosures and high-voltage modules in EVs.

RTP Company specializes in Long Glass Fiber (LGF) PA6/PA66/PPA compounds, where its proprietary pultrusion method maximizes fiber–resin bonding, enabling exceptional impact resistance and stiffness. These materials are widely used as metal substitutes in industrial tools, structural brackets, and machinery components. RTP also integrates PTFE, MoS₂, and wear-resistant additives to produce friction-optimized structural GF Nylon, supporting dynamic load and movement applications.

Glass Filled Nylon Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18.8 Billion

|

|

Market Size (2035)

|

$33.4 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Polyamide Type (PA6, PA66, PA46, PA12), By Fiber Type/Length (Short Glass Fiber, Long Glass Fiber, Glass Bead Filled, Continuous Fiber Reinforced Thermoplastics), By Glass Content (10%, 20%, 30%, 40–60%), By End-Use Industry (Automotive, Electrical & Electronics, Industrial, Consumer Goods, Aerospace), By Manufacturing Process (Injection Molding, Extrusion, Additive Manufacturing, Compression Molding)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Solvay S.A. (Syensqo), Celanese Corporation, DuPont de Nemours Inc., LANXESS AG, Asahi Kasei Corporation, Arkema Group, Evonik Industries AG, Ascend Performance Materials, Toray Industries Inc., SABIC, Envalior

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glass Filled Nylon Market Segmentation

By Polyamide (Nylon) Type

- Polyamide 6 (PA6)

- Polyamide 66 (PA66)

- Polyamide 46 (PA46)

- Polyamide 12 (PA12)

By Fiber Type / Length

- Short Glass Fiber (SGF)

- Long Glass Fiber (LGF)

- Glass Bead Filled

- Continuous Fiber Reinforced (CFR-TP)

By Glass Content (%)

- 10% Glass Filled

- 20% Glass Filled

- 30% Glass Filled

- 40%–60% Glass Filled

By End-Use Industry

- Automotive

- Electrical & Electronics

- Industrial

- Consumer Goods

- Aerospace

By Manufacturing Process

- Injection Molding

- Extrusion

- 3D Printing / Additive Manufacturing

- Compression Molding

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Glass Filled Nylon Manufacturers

- BASF SE

- Solvay S.A. (Syensqo)

- Celanese Corporation

- DuPont de Nemours, Inc.

- LANXESS AG

- Asahi Kasei Corporation

- Arkema Group

- Evonik Industries AG

- Ascend Performance Materials

- Toray Industries, Inc.

- SABIC

- DSM Engineering Materials (Envalior)

*- List not Exhaustive