Market Overview: Healthcare and Laboratory Labels Market to Reach $17.8 Billion by 2034 on Compliance and Smart Label Innovation

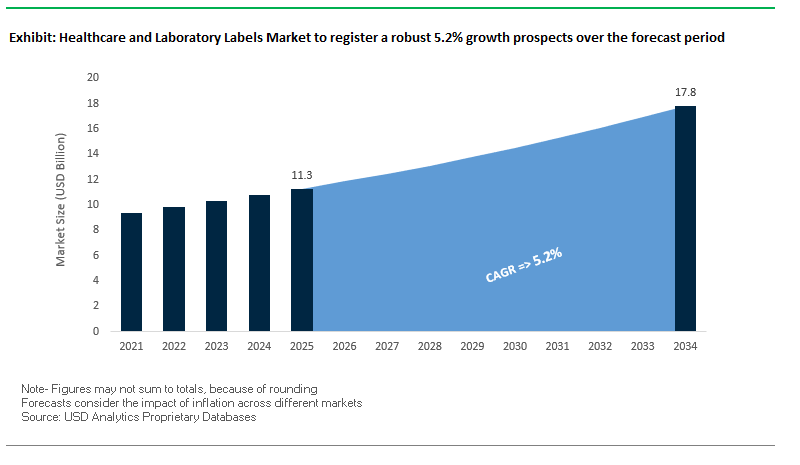

The global healthcare and laboratory labels market is valued at $11.3 billion in 2025 and is projected to reach $17.8 billion by 2034, growing at a CAGR of 5.2%. Unlike conventional labels, healthcare and laboratory labels must meet stringent regulatory, environmental, and security requirements, while ensuring precision in patient safety, specimen tracking, and pharmaceutical packaging integrity. With the rise of clinical trials, biologics, and personalized medicine, demand for RFID-enabled smart labels, tamper-evident solutions, and cryogenic durability is accelerating across hospitals, labs, and pharmaceutical supply chains.

Key Insights for industry professionals

- Regulatory alignment is critical: Labels must comply with FDA, EMA, and GMP standards to ensure authenticity and traceability.

- Durability under extreme conditions: Laboratory labels must survive cryogenic storage, sterilization, and harsh chemicals without losing adhesion or legibility.

- Smart technology adoption: RFID, barcodes, and digital ID labels are driving automation, enabling real-time specimen and inventory tracking.

- Anti-counterfeiting in focus: Tamper-evident seals and holographic features safeguard pharmaceutical products and clinical trial supplies.

Market Analysis: Recent Developments Highlight Sustainability, Acquisitions, and Advanced Materials

The healthcare and laboratory labels industry has witnessed sustainability breakthroughs, acquisitions, and material innovations over the past two years. In August 2025, UPM Adhesive Materials received a Platinum EcoVadis sustainability rating, ranking in the top 1% globally for its efforts in procurement, labor, and environmental practices. Similarly, Lintec’s China subsidiary (April 2025) achieved Global Recycled Standard (GRS) certification, reinforcing circular economy credentials in label production.

Innovation in life sciences is also shaping the sector. Ahlstrom (February 2025) secured FDA Class 1 listing for its biological sample collection cards, improving traceability in diagnostics. Earlier, in November 2024, Ahlstrom acquired ErtelAlsop, expanding into advanced filtration for pharmaceutical and laboratory applications. Technology-led product launches are reshaping competitive dynamics Avery Dennison (October 2024) unveiled RFID-enabled healthcare labels and sustainable digital ID solutions at Labelexpo, while CCL Industries (September 2024) completed a strategic acquisition to strengthen its healthcare packaging footprint.

Strategic manufacturing investments are also driving capacity expansion. Gerresheimer (August 2024) opened a new German plant for pharma vials, while UPM and Ahlstrom reinforced their role in supplying label substrates built for compliance, sustainability, and high performance. Together, these developments reflect a market focused on green materials, automation integration, and product authenticity in healthcare labeling.

Trends and Opportunities Reshaping the Healthcare and Laboratory Labels Market

Strategic Expansion of Production Capacity for High-Performance Materials

The healthcare and laboratory labels market is undergoing rapid transformation as leading manufacturers strategically expand production capacity to meet the rising demand for high-performance materials. Labels used in biopharma, clinical diagnostics, and research laboratories must endure extreme conditions such as deep-freeze storage, sterilization in autoclaves, or exposure to harsh chemicals. To address this, companies are investing heavily in specialized manufacturing facilities equipped with advanced presses and certified for quality and compliance.

In 2025, R.R. Donnelley & Sons Company (RRD) announced a major expansion of its U.S.-based ISO 9001:2015-certified facilities, enabling greater output of compliant, high-quality label solutions specifically designed for healthcare and pharmaceutical applications. Meanwhile, innovators like Schreiner MediPharm are setting new performance benchmarks with advanced solutions such as its Freeze-Light-Protect label, engineered to withstand both cryogenic temperatures and light exposure two critical challenges for biopharma storage and transport. Material innovation is also accelerating, with polyolefin labels gaining traction for their chemical resistance and durability in high-stress laboratory environments. These investments highlight how manufacturers are shifting focus from commodity labels to high-performance, application-specific materials that ensure compliance, safety, and reliability in clinical and laboratory settings.

Integration of Digital Technology for Track-and-Trace and Patient Safety

Digitalization is reshaping the healthcare and laboratory labels industry, transforming labels into multifunctional tools that extend far beyond basic identification. Labels embedded with QR codes, RFID chips, and unique identifiers (UIDs) are increasingly being adopted to meet strict global regulations for serialization, traceability, and patient safety. Governments and agencies such as the FDA in the U.S. and the EMA in Europe mandate serialization and aggregation standards for pharmaceuticals, making digitally integrated labels essential to ensure compliance.

This trend also addresses the growing problem of counterfeit medical products. According to the World Health Organization (WHO), one in ten medical products in low- and middle-income countries is falsified or substandard. Serialized smart labels enable real-time authentication throughout the supply chain, mitigating this risk and enhancing patient safety. Additionally, companies like Identiv are expanding digital integration with BLE-enabled smart labels that provide end-to-end visibility in high-value logistics and cold chain tracking. This technological shift transforms labels into intelligent assets, enabling predictive supply chain monitoring, anti-counterfeiting protection, and enhanced patient trust, making them central to the healthcare sector’s digital transformation.

Capitalizing on the Rapid Growth of At-Home Diagnostic Tests

The surge in at-home diagnostic testing represents one of the most dynamic opportunities in the healthcare and laboratory labels market. As consumers increasingly adopt direct-to-consumer testing kits for conditions such as COVID-19, diabetes, fertility, and cholesterol, the demand for specialized label solutions is accelerating. Labels play a crucial role in these kits, providing clear user instructions, unique identifiers for online result access, and brand differentiation in a highly competitive market.

A study of consumer behavior emphasizes that the convenience and privacy of at-home testing are primary drivers of adoption, creating direct demand for labels that are both user-friendly and durable. Label formats must balance functionality with space constraints, often requiring high-resolution printing on compact surfaces. As the market expands into infectious disease, genetic, and cardiovascular diagnostics, new generations of labels must perform reliably across varied substrates and environmental conditions. This opportunity allows manufacturers to deliver precision-engineered, instruction-rich labels that directly enhance usability, accuracy, and consumer trust, positioning labels as a value-adding component of the at-home diagnostic ecosystem.

Development of Sustainable Label Solutions for Life Sciences

Sustainability is emerging as a critical innovation frontier for healthcare and laboratory labels. The industry faces growing pressure from corporate ESG commitments and global regulations to reduce environmental impact while maintaining stringent performance and compliance standards. Traditional labels often contaminate recycling streams, limiting container recyclability and undermining circular economy goals. This creates a major opportunity for companies to pioneer eco-friendly label substrates, adhesives, and films that align with life sciences performance requirements.

Manufacturers are already responding with recycled-content and bio-based films designed for infusion bottles and pharmaceutical applications, offering durability while reducing virgin material use. Innovation is also advancing in wash-off adhesives, which allow labels to be cleanly separated during recycling, ensuring plastic containers can re-enter the material stream without contamination. At the same time, bio-based adhesives and renewable films are being scaled to meet the rigorous standards of healthcare, where chemical resistance, sterilization tolerance, and regulatory compliance are non-negotiable. By delivering sustainable yet high-performance label solutions, producers can not only meet customer ESG targets but also secure a differentiated competitive position in a market where sustainability is becoming a purchasing criterion.

Competitive Landscape: Global Leaders Driving Compliance, RFID Adoption, and Sustainable Label Materials

The healthcare and laboratory labels market is highly specialized, with competition centered on regulatory compliance, material durability, and smart technology integration. Global leaders and niche specialists are investing in RFID innovation, cryogenic materials, and sustainability programs to differentiate in this compliance-heavy sector.

Avery Dennison: Leading RFID and sustainable label innovation

Avery Dennison offers pressure-sensitive label materials for healthcare and pharmaceuticals, including blood bag and cryogenic vial labels. Its RFID-enabled smart labels enhance traceability, while CleanFlake™ adhesive technology boosts recyclability. The AD Circular program reinforces its sustainability focus, and its portfolio ensures durability across extreme environments.

CCL Industries: Expanding healthcare packaging through acquisitions

CCL Industries, the world’s largest label manufacturer, provides booklet labels for clinical trials, security solutions, and RFID labels. In September 2024, it completed a strategic healthcare acquisition, reinforcing its global dominance. CCL Healthcare specializes in multi-language clinical trial labels and expanded content labels (ECLs), meeting GMP standards for complex drug packaging.

UPM Adhesive Materials: Sustainability leader with Platinum EcoVadis rating

Formerly UPM Raflatac, UPM offers pressure-sensitive label stock tailored for healthcare and pharmaceuticals. In August 2025, it received a Platinum EcoVadis rating, ranking in the top 1% globally. UPM is embedding environmental footprint data into customer quotes, enhancing transparency. Its investments in North Carolina and Malaysia coating facilities highlight its global expansion.

3M Company: Material science expertise in medical labels

3M brings deep adhesive and material science expertise to healthcare labeling. Its portfolio includes medical tapes, lab labels, and surgical adhesives that withstand sterilization and diagnostics workflows. Its innovation pipeline supports high-performance films and medical tapes, critical in blood banks, diagnostics labs, and device packaging.

Lintec Corporation: Traceability and sustainable label systems

Lintec provides high-resolution adhesive papers and films for barcode and traceability labels in healthcare. In April 2025, its China subsidiary achieved GRS certification, reinforcing its sustainable materials strategy. Its innovation in removable hot-melt adhesive labelstock and label machinery systems positions Lintec as a full-service provider.

Gernep GmbH: Precision labeling machinery for healthcare production

Gernep specializes in rotary labeling machines for pharmaceuticals, vials, and healthcare packaging. Its systems cover pressure-sensitive, hot melt, and cold glue applications, ensuring speed and precision in regulated environments. By focusing on low downtime and tailored integration, Gernep supports high-volume pharmaceutical producers.

Healthcare and Laboratory Labels Market Share Insights

Market Share by Technology: Thermal Transfer Leads Healthcare and Laboratory Labeling

By technology, thermal transfer printing dominates the healthcare and laboratory labels market, projected to hold 48% of the 2025 share. Its leadership is driven by unmatched durability, chemical resistance, and long-term reliability, making it indispensable for sterilization, cryogenic storage, and harsh laboratory environments. Direct thermal technology also captures a notable portion due to its efficiency in short-term clinical workflows such as patient wristbands and point-of-care specimen labeling. Meanwhile, laser printing continues to strengthen its presence in pharmaceutical packaging where precision, compliance, and serialization are non-negotiable. Inkjet printing holds a smaller niche, serving specialized needs like color-coded laboratory labeling and inventory management where visual cues enhance workflow efficiency. The dominance of thermal transfer underscores the market’s prioritization of safety, compliance, and resilience across critical healthcare applications.

Market Share by Application: Pharmaceutical and Patient Safety Labels Drive Growth

By application, pharmaceutical and nutraceutical labels account for the largest share of the market, representing 30% of projected demand in 2025. This segment’s growth is sustained by stringent global regulations requiring serialization, barcoding, and traceability across every drug package. Patient identification and specimen labels follow closely, forming the backbone of clinical safety by ensuring accurate diagnostics and reducing medical errors through reliable tracking systems. Laboratory labels remain a vital segment, supporting scientific research and biotechnology with products engineered to withstand cryogenic temperatures, solvents, and sterilization. Niche but critical segments such as blood bag labeling highlight the industry’s technical rigor, requiring flawless barcode performance to safeguard patient outcomes. Asset and inventory labeling, though smaller in share, is growing steadily as hospitals prioritize operational efficiency and digital asset management. Collectively, these applications emphasize the sector’s dual focus on regulatory compliance and patient safety, reinforcing labeling as an indispensable pillar of modern healthcare operations.

United States: Digitalization and Sustainability Driving Healthcare Label Innovation

The U.S. healthcare and laboratory labels market is witnessing significant growth, driven by the rapid adoption of digitalization and automation in hospitals, laboratories, and pharmaceutical companies. Integration with electronic health records (EHRs) and laboratory information management systems (LIMS) has increased demand for barcode labels and RFID tags, which enhance specimen tracking, patient safety, and operational efficiency. Innovations in label materials and adhesives, such as ultra-durable, chemical- and temperature-resistant labels introduced by Avery Dennison, are ensuring the integrity of critical healthcare data. Regulatory compliance with FDA guidelines remains a cornerstone, while sustainability trends push the adoption of biodegradable labels printed with soy-based inks. Advanced printing technologies, including direct thermal and thermal transfer methods, are enabling on-demand production of high-quality, durable labels.

Germany: Government Support and Advanced Healthcare Infrastructure Accelerating Label Demand

Germany’s healthcare and laboratory labels market benefits from robust governmental support and a highly developed medical infrastructure. Initiatives like Horizon Europe are funding smart health, AI, and digital care projects, creating opportunities for innovative labeling solutions. The Digital Care Act (DVG) facilitates reimbursement for digital health applications, driving demand for labels compatible with smart medical devices. Germany’s focus on collaboration and R&D within healthcare clusters fosters the development of new materials and technologies, while high spending on medical devices and in vitro diagnostics (IVDs) ensures a steady demand for reliable, high-quality labels that meet stringent European standards.

China: Automation, AI, and Smart Packaging Transforming Label Applications

China’s healthcare and laboratory labels market is rapidly evolving, driven by intelligent, multi-functional, and highly automated manufacturing equipment. The integration of IoT, AI-enabled quality inspection, and 5G remote monitoring enhances production efficiency and operational stability. National standards such as GB 4806.15-2024 for food packaging adhesives are pushing manufacturers to ensure safety and compliance. Rapid urbanization and the growth of processed and ready-to-eat foods are increasing demand for secure, convenient, and informative packaging solutions. Smart packaging innovations, including time-temperature indicators and gas sensors, are being integrated into labels to monitor product freshness and quality across the supply chain.

India: Make in India and Regulatory Compliance Boosting Label Market Growth

India’s healthcare and laboratory labels market is being propelled by the Make in India initiative, which has attracted foreign investment and expanded domestic production capabilities. The country’s regulatory framework, governed by CDSCO and the Medical Devices Rules, 2017, mandates detailed labeling requirements, ensuring traceability and patient safety. Technological adoption, including QR codes and other smart label solutions, enhances transparency and consumer confidence. The government’s emphasis on drug traceability through barcodes and unique identifiers is a critical development to combat counterfeit drugs and maintain the integrity of the pharmaceutical supply chain.

Brazil: Digitalization and Pharmaceutical Growth Supporting Label Demand

Brazil’s healthcare and laboratory labels market is experiencing growth due to increased governmental investment in digital health. The Brazilian Ministry of Health’s $200 million investment for digitalizing the public healthcare system (SUS) opens opportunities for labels compatible with smart medical devices and digital applications. Brazil’s pharmaceutical sector, the largest in Latin America and ninth globally, drives demand for labels for medicines and related products. Regulatory updates by Anvisa ensure adherence to international quality and safety standards, further enhancing the market for high-quality healthcare labels.

Japan: AI, Data Utilization, and Regulatory Support Enhancing Label Innovation

Japan’s healthcare and laboratory labels market is benefiting from strong governmental support, including initiatives under Healthcare Policy Phase III (April 2025), which promote practical applications of pharmaceuticals, medical devices, and novel therapies. The government encourages the use of medical data and AI in healthcare, driving demand for smart labels capable of providing real-time patient and device information. Japan’s emphasis on quality and safety ensures that the market produces reliable, high-performance labels for diverse healthcare and laboratory applications, positioning the country as a leader in advanced medical labeling solutions.

Healthcare and Laboratory Labels Market Report Scope

Healthcare and Laboratory Labels Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.3 Billion

|

|

Market Size (2034)

|

$17.8 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Material Type (Paper, Vinyl, Polyolefin, Polyester, Nylon, Other Materials), By Technology (Thermal Transfer, Direct Thermal, Laser, Inkjet), By Application (Patient Identification Labels, Specimen Labels, Blood Bag Labels, Pharmaceutical & Nutraceutical Labels, Laboratory Labels, Asset & Inventory Labels, Other Applications), By End-Use (Hospitals & Clinics, Laboratories, Blood Banks, Research & Diagnostic Centers, Pharmaceutical Companies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avery Dennison Corporation, CCL Industries Inc., 3M Company, Honeywell International Inc., Brady Corporation, Zebra Technologies Corporation, Lintec Corporation, UPM Raflatac Oyj, Schreiner Group GmbH & Co. KG, SATO Holdings Corporation, WS Packaging Group, Inc., Checkpoint Systems, Inc., R.R. Donnelley & Sons Company (RRD), L.N. International Co., Ltd., Technicote Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Healthcare and Laboratory Labels Market Segmentation

By Material Type

- Paper

- Vinyl

- Polyolefin

- Polyester

- Nylon

- Other Materials

By Technology

- Thermal Transfer

- Direct Thermal

- Laser

- Inkjet

By Application

- Patient Identification Labels

- Specimen Labels

- Blood Bag Labels

- Pharmaceutical & Nutraceutical Labels

- Laboratory Labels

- Asset & Inventory Labels

- Other Applications

By End-Use

- Hospitals & Clinics

- Laboratories

- Blood Banks

- Research & Diagnostic Centers

- Pharmaceutical Companies

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Healthcare and Laboratory Labels Market

- Avery Dennison Corporation

- CCL Industries Inc.

- 3M Company

- Honeywell International Inc.

- Brady Corporation

- Zebra Technologies Corporation

- Lintec Corporation

- UPM Raflatac Oyj

- Schreiner Group GmbH & Co. KG

- SATO Holdings Corporation

- WS Packaging Group, Inc.

- Checkpoint Systems, Inc.

- R.R. Donnelley & Sons Company (RRD)

- L.N. International Co., Ltd.

- Technicote Inc.

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global healthcare and laboratory labels market, highlighting breakthroughs in smart label technology, compliance-driven innovations, and sustainable material development. The analysis reviews recent strategic acquisitions, automation integration, and material advancements that are reshaping labeling solutions across hospitals, laboratories, blood banks, and pharmaceutical supply chains. The report highlights how manufacturers are leveraging RFID-enabled and tamper-evident labels, cryogenic-resistant substrates, and bio-based adhesives to meet the stringent regulatory, environmental, and safety requirements of healthcare operations. Additionally, this report examines competitive dynamics, capacity expansion, and digital traceability initiatives that ensure patient safety, improve supply chain efficiency, and mitigate counterfeiting risks. With historic data from 2021 to 2024 and forecast data spanning 2025 to 2034, this report is an essential resource for executives, procurement specialists, R&D managers, and compliance officers seeking actionable insights into market growth, material performance, and technological adoption. USDAnalytics delivers in-depth company profiles, market share insights, and country-specific analyses to guide strategic investment, operational optimization, and innovation planning in the healthcare and laboratory labels market.

Scope Highlights:

- Segmentation: By Material Type (Paper, Vinyl, Polyolefin, Polyester, Nylon, Other Materials), By Technology (Thermal Transfer, Direct Thermal, Laser, Inkjet), By Application (Patient Identification Labels, Specimen Labels, Blood Bag Labels, Pharmaceutical & Nutraceutical Labels, Laboratory Labels, Asset & Inventory Labels, Other Applications), By End-Use (Hospitals & Clinics, Laboratories, Blood Banks, Research & Diagnostic Centers, Pharmaceutical Companies)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historic Data: 2021–2024; Forecast Period: 2025–2034

- Companies Covered: Profiles and analysis of 15+ companies including Avery Dennison, CCL Industries, 3M, Honeywell, Brady Corporation, Zebra Technologies, Lintec, UPM Raflatac, Schreiner Group, SATO Holdings, and others

Methodology

The methodology combines primary research, secondary data collection, and quantitative modeling to deliver robust market insights. USDAnalytics conducted interviews with key stakeholders, including label manufacturers, distributors, end-users, and healthcare compliance experts, to capture supply- and demand-side dynamics. Secondary sources such as regulatory documents, sustainability reports, corporate filings, trade publications, and patent databases were analyzed to validate technological and material trends. Historic market data (2021–2024) was consolidated using statistical techniques, while forecasts (2025–2034) were derived based on adoption rates, healthcare infrastructure growth, and technological integration scenarios. Segmentation analysis, competitive benchmarking, and country-level insights were incorporated to identify investment hotspots, capacity expansion opportunities, and innovation pathways. The methodology ensures that the report provides actionable intelligence for executives, R&D teams, and procurement specialists seeking to optimize operations, ensure compliance, and leverage sustainable, high-performance labeling solutions in healthcare and laboratory environments.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.