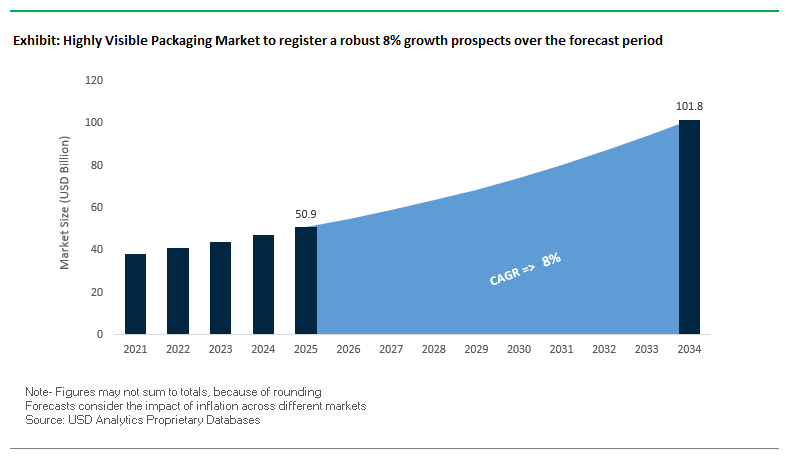

Highly Visible Packaging Market Overview (2025–2034): $50.9B to $101.7B at 8% CAGR, driven by transparency and sustainability

The Global Highly Visible Packaging Market is a fast-growing segment within the packaging industry, enabling brands to showcase product authenticity and drive consumer trust through transparent, windowed, and clear formats. The demand is expanding rapidly as consumers seek visual confirmation of product quality, particularly in categories such as food, beverages, cosmetics, luxury goods, and electronics.

The market is shaped by two major forces sustainability and digitalization. Companies are innovating with Post-Consumer Recycled (PCR) PET, compostable transparent materials, and biodegradable fiber-based packaging, reducing reliance on virgin plastics. Simultaneously, the integration of intelligent packaging technologies such as QR codes, RFID, and IoT sensors is creating interactive consumer experiences and real-time traceability.

Key Insights for Industry Professionals:

- Transparency as a growth driver: More than half of global consumers prioritize brands that enable visibility and authenticity through packaging.

- Sustainability imperative: Growing adoption of PCR PET, transparent paper, and compostable bio-materials in blister packs, clamshells, and windowed cartons.

- Premiumization: Luxury, cosmetics, and gourmet segments leverage aesthetic clarity to differentiate and justify higher price points.

- Smart packaging adoption: Brands are adding QR, RFID, and freshness sensors to highly visible packaging to meet traceability, safety, and engagement goals.

- EPR regulations: New legislation such as Hawaii’s EPR law (May 2025) is shaping material choice and accelerating the shift to recyclable designs.

Market Analysis: Recent Developments in Highly Visible Packaging (2024–2025)

The market is experiencing a wave of sustainability-focused innovation and strategic investment as companies adapt to consumer expectations and regulatory frameworks.

In September 2025, APP Group showcased Foopak Bio Natura at FACHPACK 2025, a compostable, recyclable, PFAS-free paperboard for food packaging, highlighting the shift toward fiber-based visible alternatives. In the same month, Schott expanded syringe and cartridge tubing production in India, strengthening its footprint in healthcare-related transparent packaging.

In August 2025, a report confirmed the growing demand for smart packaging technologies (QR, NFC, RFID), signaling the industry's pivot toward traceability and consumer interaction. Earlier, in July 2025, the Amcor–Berry Global merger created a new powerhouse in rigid and flexible visible packaging, enabling expanded scale and innovation.

Regulatory momentum also shapes market direction. In May 2025, Hawaii signed a pre-EPR bill into law, compelling producers to rethink packaging design for recyclability. At the innovation front, Wiliot (January 2025) launched an IoT-based packaging solution delivering end-to-end supply chain visibility.

Longer-term sustainability trends are reinforced by corporate investment. Unilever (December 2024) doubled its packaging R&D budget under its “Future Flexibles” program, aiming to develop recyclable and compostable materials. The PlantBottle prototype (October 2024) introduced a 100% plant-based clear PET bottle, while Pakka (September 2024) launched compostable flexible packaging, further proving the momentum toward eco-friendly highly visible formats.

Pioneering Trends and Strategic Opportunities in the Highly Visible Packaging Market

Strategic Shift to Monomaterial Polyolefin Structures for Recyclability

The highly visible packaging market is experiencing a major shift toward mono-material polyethylene (PE) and polypropylene (PP) pouches, moving away from traditional multi-material laminates that are difficult to recycle. This trend is primarily driven by brand sustainability commitments and Extended Producer Responsibility (EPR) regulations, which increasingly mandate that all packaging be recyclable. Companies such as Nestlé and Unilever are actively piloting mono-material flexible packaging solutions for baby food, personal care products, and consumer goods, aiming to streamline recycling processes and enhance environmental compliance. Collaborative innovations, including ExxonMobil’s high-barrier MDO-PE//PE laminate, ensure that these pouches maintain oxygen, moisture, and light barrier properties while remaining compatible with existing production lines. This transition is reshaping the flexible packaging supply chain, encouraging close collaboration between resin manufacturers, converters, and brand owners to implement cost-effective, sustainable packaging solutions.

Integration of Transparent High-Barrier EVOH Layers for Product Visibility

Increasing consumer demand for product transparency without compromising barrier performance is accelerating the adoption of EVOH-integrated high-barrier pouches. These structures use thin, transparent EVOH layers coextruded with polyolefin sealants, replacing traditional opaque aluminum laminates while maintaining exceptional oxygen and aroma barrier properties. EVOH acts as a “fortress” against oxygen ingress, protecting food and beverage quality, and is often shielded from moisture by adjacent polyolefin layers to maintain stability. This innovation not only enhances on-shelf appeal but also provides a lighter, more flexible alternative to rigid packaging, offering a significant growth avenue for premium products such as coffee, snacks, and dried fruits. Collaborations between film manufacturers and pouch converters are optimizing coextrusion technologies to integrate EVOH efficiently and cost-effectively.

Development of Bio-Based and Compostable High-Barrier Solutions

A substantial opportunity lies in the development of high-barrier pouches from bio-based and certified compostable materials, particularly for organic, natural, and premium product segments. Materials such as PLA, PHA, and cellulose derivatives can be engineered to provide barrier performance on par with conventional plastics while supporting industrial composting standards. Academic research, including work from Bhabha Atomic Research Centre (BARC), has demonstrated that biopolymers like guar gum can achieve comparable mechanical and barrier properties to traditional plastics. Companies such as Nestlé and Unilever are increasingly adopting these materials as part of their sustainability strategies, targeting environmentally conscious consumers willing to pay a premium. This innovation requires a robust industrial composting infrastructure and encourages partnerships between film manufacturers, renewable material suppliers, and converters, fostering a circular economy and reducing environmental impact.

Incorporation of Digital Watermarking for Intelligent Recycling

The integration of digital watermarking technologies, exemplified by the HolyGrail 2.0 initiative, presents a transformative opportunity to overcome sorting challenges in flexible packaging recycling. These imperceptible watermarks can be scanned at high-resolution sorting facilities to automate separation of packaging by material type or food category, creating clean streams of recyclable material. Industrial trials have demonstrated the ability to significantly enhance recycling precision, improving the quality and quantity of recycled output. This trend is supported by organizations such as the Ellen MacArthur Foundation and companies like Digimarc, promoting the creation of a circular economy for flexible packaging. By embedding “smart” capabilities into pouches, manufacturers can increase recycling rates, reduce environmental footprint, and add value for brand owners. Successful implementation requires collaboration across the entire packaging ecosystem, including technology providers, converters, and recycling facilities, ensuring scalability and efficiency.

Competitive Landscape: Global Leaders Driving Sustainable, Transparent, and Intelligent Packaging

The competitive environment is defined by multinational corporations scaling recyclable clear plastics and specialists pioneering fiber-based transparency. Players are differentiating through material science innovation, partnerships, and acquisitions.

Amcor strengthens clear packaging through Berry merger

Amcor’s global network enables leadership in highly visible packaging with sustainable rigid and flexible formats. In July 2025, it merged with Berry Global, expanding its clear and recyclable portfolio. Amcor’s offerings include 50% PCR paint containers and recyclable closures. Its strategy centers on achieving 100% recyclable/reusable packaging by 2025, balancing visual clarity and sustainability.

Berry Global expands circular polymers and recyclable visibility solutions

Berry Global, now combined with Amcor, continues to focus on sustainable highly visible packaging. In February 2025, it collaborated with Kraft Heinz to introduce a fully recyclable ketchup cap, showcasing innovation in visible closures. With a focus on circular polymers, Berry is positioned to supply clear packaging across food, beverage, and personal care markets while aligning with low-carbon footprints.

Printex Transparent Packaging pioneers custom PCR-based designs

Printex specializes in transparent folding boxes, clamshells, and window cartons. Its Eco-PET series offers up to 100% PCR PET, aligning visibility with circularity. Innovative designs, like a three-sided windowed coffee sachet carton, have boosted retail sales. Printex’s strategy is to support brand marketing and sustainability goals by scaling domestic PCR production in North America.

Ahlstrom advances fiber-based transparent paper as plastic alternative

Ahlstrom is redefining visible packaging with biodegradable transparent paper a compostable and recyclable substitute for plastic windows and films. Applications span toys, cosmetics, and pharma. Its certified bio-based transparent materials meet home and industrial compost standards. Recent partnerships, such as with Maped for flowpack eraser packaging, highlight versatility. Ahlstrom aims to commercialize next-gen sustainable visibility solutions across industries.

Eastman Chemical Company integrates recycled content into visible resins

Eastman leverages its Cristal™ One Renew resin (RIC1) with 100% certified recycled content to supply cosmetic compacts and blister packaging. Collaborating with ICONS (late 2023), Eastman demonstrated monomaterial designs that combine clarity, durability, and recyclability. Its PETG and copolyester resins enable applications ranging from beverage bottles to healthcare blister packs, supporting customers’ circular economy goals.

Highly Visible Packaging Market Share Insights

Blister Packs Lead Market Share by Packaging Type in Highly Visible Packaging

Blister packs hold the largest share of the highly visible packaging market at 35% in 2025, driven by their unique combination of product visibility, tamper evidence, and adaptability across industries. They are indispensable for pharmaceuticals, where unit-dose packs ensure patient compliance and safety, and for consumer goods such as batteries, razors, and electronics accessories, where the clear dome showcases the product while deterring theft. Clamshells follow closely with 30% share, providing rigid protection for premium and high-value products like electronics, hardware, and personal care items, and their recyclability (often using rPET) is increasingly valued in sustainability-focused retail environments. Windowed packaging continues to grow in food, cosmetics, and gift sectors, balancing cost-effectiveness with high-impact branding by combining die-cut visibility with full graphic coverage. Shrink wrap and skin packaging remain specialized solutions: shrink wrap dominates in bundling multi-packs with high shelf impact, while skin packaging offers secure visibility for irregular hardware and tools. This segmentation underscores how blisters dominate through versatility and compliance, clamshells anchor security-driven markets, and windowed packaging captures cost-sensitive yet visibility-focused applications.

Consumer Goods Dominate Market Share by Application in Highly Visible Packaging

Consumer goods account for 40% of the highly visible packaging market in 2025, reflecting their reliance on packaging as both a protective and marketing tool at retail. From stationery and toys to small appliances and grooming products, clear packaging directly influences purchase decisions by letting shoppers see the product while ensuring theft deterrence. Food and beverages follow with 25% share, where windowed boxes, clamshells, and blister packs are widely used for pastries, confectionery, cheeses, and premium produce leveraging visibility to drive impulse purchases and assure freshness. Healthcare applications, though smaller in volume, remain non-negotiable in value, as blister packaging for unit-dose medications is mandated for compliance, dosage accuracy, and tamper evidence. Electronics and industrial goods also rely heavily on clamshells, blisters, and skin packs, balancing theft prevention with durability and point-of-sale visibility for items such as cables, headphones, and tools. This segmentation demonstrates how consumer goods drive scale, food leverages visibility for impulse sales, and healthcare and electronics sustain compliance- and protection-driven adoption.

United States Highly Visible Packaging Market Driven by Sustainability and Consumer Transparency

The U.S. highly visible packaging market is shaped by a fragmented regulatory environment, notably California's SB-54 Extended Producer Responsibility (EPR) law, which mandates a 25% plastic reduction by 2032. This regulation is accelerating the shift toward recyclable and mono-material packaging designs that are both environmentally friendly and consumer-centric. Technological advancements are driving innovation, with direct digital printing and smart packaging features like QR codes and RFID becoming essential for providing real-time product information and enhancing consumer engagement.

Corporate investments are significant, with Amcor’s planned acquisition of Berry Global Group consolidating R&D efforts to develop sustainable packaging solutions. Demand is robust across the food and beverage, healthcare, and consumer goods sectors, where highly visible formats such as clamshells and blister packs play a key role in product differentiation and consumer trust. Sustainability remains a critical focus, with eco-friendly materials like recycled PET (rPET) and biodegradable options being increasingly adopted to reduce environmental impact and meet evolving consumer preferences.

Germany Highly Visible Packaging Market Strengthened by Regulatory Compliance and Circular Economy Initiatives

Germany’s highly visible packaging market is regulated by the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandating fully recyclable or reusable packaging by 2030 and phasing out certain hazardous chemicals. Technological innovation is at the forefront, with companies like Amcor showcasing lightweight containers using recycled plastics and mono-material solutions that simplify recycling processes, as highlighted at Fachpack 2025.

The country’s Packaging Act (VerpackG) fosters leadership in the circular economy by incentivizing recycling-friendly designs through modulated fees. Pilot projects such as “Mehrweg Modell Stadt” demonstrate Germany’s commitment to reusable systems. The market is particularly strong in food, beverage, and medical sectors, driven by a robust manufacturing base and high export activities that demand reliable, high-performance packaging solutions ensuring product integrity and consumer trust.

China Highly Visible Packaging Market Expands Through Sustainability and Domestic Manufacturing

China’s highly visible packaging market is influenced by government initiatives, including the “dual carbon” goal and the March 2024 Action Plan promoting sustainable materials and recycling. Regulatory reforms like GB/T 31268, effective November 2024, address excessive packaging, particularly in e-commerce, directly affecting packaging design and material usage.

Technological advancements, including AI and “5G plus industrial internet,” are enhancing production efficiency and flexibility. Corporate collaborations, such as Dow and Mengniu’s mono-material PE yogurt pouch introduced in August 2023, focus on recyclability and visual appeal. A strong emphasis on domestic manufacturing is supporting local substitution of imported technologies and meeting growing demand for high-quality, sustainable packaging in consumer goods, particularly in the food and beverage sector.

India Highly Visible Packaging Market Accelerates with Circular Economy Policies and Smart Packaging

India’s highly visible packaging market is benefiting from circular economy initiatives and the Make in India program, promoting local manufacturing and technological advancement. Adoption of automated printing systems and smart packaging technologies is growing, with industry events like Fi India and ProPak India 2025 highlighting AI-driven automation as a key trend.

Corporate investments are expanding production capacity, led by companies like UFlex, which is pioneering aluminum-free laminates and bio-based films. Key applications include food processing, personal care, and e-commerce sectors, where demand for transparent, high-performance packaging is rising. Regulatory focus by the Food Safety and Standards Authority of India (FSSAI) in 2025 on labeling and organic food standards is further boosting demand for highly visible, informative packaging solutions.

Japan Highly Visible Packaging Market Focuses on High-Performance and Functional Films

Japan’s highly visible packaging market is anchored in advanced precision manufacturing, with the Plastic Resource Circulation Act, effective April 2022, promoting sustainable materials and reducing single-use plastics. The market is moving toward high-performance and value-added packaging, incorporating features like IoT sensors, easy-open tear notches, and resealable closures to cater to aging populations and single-person households.

Companies such as Toppan Inc., in collaboration with RM Tohcello and Mitsui Chemicals, are producing recycled BOPP films suitable for mass production. Japan’s focus on functional and visually appealing packaging aligns with its commitment to sustainability, innovation, and maintaining a competitive edge in the global highly visible packaging industry.

Brazil Highly Visible Packaging Market Driven by Sustainable Innovations and Strategic Partnerships

Brazil’s highly visible packaging market is influenced by government policies promoting sustainable waste management, including amendments to the National Solid Waste Policy. Partnerships such as iFood and XPRIZE’s $20 million competition for flexible, biodegradable packaging are encouraging eco-friendly innovations in the packaging industry.

Technological advancements are driving the adoption of premium and digital packaging solutions, extending product shelf life while maintaining quality. The food and beverage sector, particularly processed and ready-to-eat foods, is a key application area. Strategic corporate collaborations, such as SIG Group’s partnership with DPA Brazil to introduce spouted pouches for Chamyto yogurt, reinforce the country’s position in sustainable, high-performance highly visible packaging solutions.

Highly Visible Packaging Market Report Scope

Highly Visible Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$50.9 Billion

|

|

Market Size (2034)

|

$101.7 Billion

|

|

Market Growth Rate

|

8%

|

|

Segments

|

By Packaging Type (Blister Packs, Clamshells, Windowed Packaging, Skin Packaging, Shrink Wrap), By Material (Plastics, Paper & Paperboard), By Application (Consumer Goods, Food & Beverages, Healthcare, Electronics, Industrial Goods), By Technology (Digital Printing, Smart Packaging, Anti-counterfeiting Features)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Huhtamaki Oyj, Berry Global Group, Inc., Sealed Air Corporation, Sonoco Products Company, ProAmpac, Constantia Flexibles Group, Klöckner Pentaplast, Toppan Inc., WestRock Company, DS Smith Plc, UFlex Ltd., Novolex Holdings, LLC, TC Transcontinental

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Highly Visible Packaging Market Segmentation

By Packaging Type

- Blister Packs

- Clamshells

- Windowed Packaging

- Skin Packaging

- Shrink Wrap

By Material

- Plastics

- Paper & Paperboard

By Application

- Consumer Goods

- Food & Beverages

- Healthcare

- Electronics

- Industrial Goods

By Technology

- Digital Printing

- Smart Packaging

- Anti-counterfeiting Features

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Highly Visible Packaging Market

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- Berry Global Group, Inc.

- Sealed Air Corporation

- Sonoco Products Company

- ProAmpac

- Constantia Flexibles Group

- Klöckner Pentaplast

- Toppan Inc.

- WestRock Company

- DS Smith Plc

- UFlex Ltd.

- Novolex Holdings, LLC

- TC Transcontinental

* List Not Exhaustive

Methodology

The research methodology for the Highly Visible Packaging Market report by USDAnalytics integrates a robust combination of primary and secondary research to deliver precise, actionable insights for industry professionals. Primary research involved in-depth interviews with packaging engineers, sustainability experts, brand managers, supply chain stakeholders, and regulatory authorities across North America, Europe, and Asia-Pacific. Secondary research encompassed analysis of corporate annual reports, industry white papers, patent filings, trade publications, sustainability reports, and regulatory frameworks such as EPR and PPWR. Advanced data triangulation techniques were employed to validate market sizing, CAGR projections, and technology adoption trends, incorporating macroeconomic indicators, raw material pricing, and consumer preference shifts. Market forecasts were developed using both top-down and bottom-up approaches, with regional analysis contextualized against policy initiatives, emerging sustainability mandates, and digital packaging innovations. This rigorous, multi-layered methodology ensures that USDAnalytics’ report provides highly accurate, data-driven insights aligned with current and future market dynamics in highly visible packaging.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.