Low Migration Inks Market Overview: Key Industry Statistics and Insights

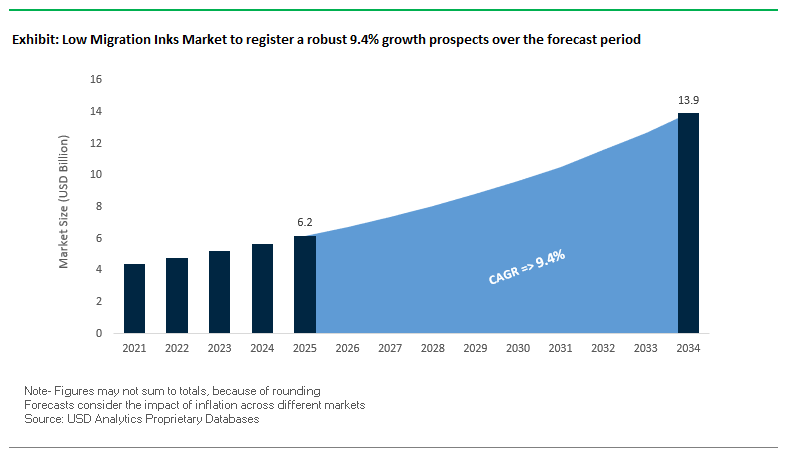

The global Low Migration Inks Market is projected to reach $6.2 billion in 2025 and is expected to grow to $13.9 billion by 2034, registering a robust CAGR of 9.4%. This growth trajectory is underpinned by the combined impact of regulatory compliance, rising consumer demand for food safety, and sustainability imperatives shaping the packaging industry. Low migration inks (LMI) have become indispensable in ensuring compliance with stringent food-contact packaging laws while simultaneously meeting the needs of evolving printing technologies and eco-friendly solutions.

For industry professionals and buyers, the central question is no longer whether LMIs are necessary, but how fast adoption can scale while balancing performance, sustainability, and compliance. With food and beverage accounting for more than 70% of the market’s demand, the sector is increasingly driven by consumer safety expectations and innovation in packaging solutions. In addition, digital printing and bio-based ink formulations are transforming cost efficiency, customization, and environmental performance, marking a pivotal point in the market’s evolution.

Key Insights for Decision Makers

- Regulatory Impact: EU’s Framework Regulation (EC) No 1935/2004 sets the benchmark, limiting NIAS migration to 10 ppb, compelling global adoption of LMI.

- Dominant Application: Over 70% of new product launches in sensitive food categories now use low migration ink solutions.

- Printing Innovation: Digital UV and water-based inks are enabling safe, customized, short-run packaging for high-value segments.

- Sustainability Push: Growing integration of bio-based raw materials reduces fossil fuel reliance, aligning with global brand sustainability goals.

Market Analysis: Recent Developments Shaping the Low Migration Inks Industry

The Low Migration Inks Market is being redefined by a wave of technological and strategic advancements between late 2024 and 2025, signaling heightened investments in sustainable innovation and regional expansion. In August 2025, Toyo Ink Europe launched Steraflex GIO, a low migration flexographic ink free from photoinitiator 379, aligning with EU’s evolving food safety standards. The same month, INX International introduced INXJet MDLM UV Curable Inkjet Ink for beverage cans, reinforcing LMI’s growing role in direct-to-object printing for sensitive applications.

Sustainability and compliance are also shaping corporate R&D priorities. In May 2025, INX International unveiled Innova Plus NCF, a nitrocellulose-free ink line developed to reduce environmental impact without compromising performance. Meanwhile, Elopak’s launch of its first U.S. carton plant in Little Rock (May 2025) further amplified demand for LMIs in North America. Likewise, in April 2025, Billerud introduced recyclable, heat-sealable paper packaging requiring specialized LMI integration, reflecting the symbiosis between packaging innovation and ink technology.

Regional expansion is another defining trend. SIG’s entry into India in February 2025 with its first aseptic carton plant highlights Asia’s strategic importance as a growth hub for food-safe packaging. Complementing this, Sun Chemical’s parent company, DIC Corporation, invested in a new European R&D center in January 2025, dedicated to high-performance, low-migration coatings and inks. Market consolidation also continues to play a role, with INX Group’s November 2024 acquisition of Coatings & Adhesives Corporation (C&A) broadening its portfolio and reinforcing synergies in the packaging ink sector.

Key Market Trends and Strategic Opportunities in the Low Migration Inks Market

Heightened Regulatory Scrutiny and Global Standardization Driving Low Migration Inks

The low migration (LM) inks market is witnessing a significant uptick in demand due to increasingly stringent regulatory frameworks and harmonized international standards for food contact materials. The European Commission’s Regulation (EU) 2025/351, adopted in February 2025, exemplifies this trend by emphasizing the purity of substances and the control of non-intentionally added substances (NIAS), reinforcing mandatory compliance across the EU. Major brands, including Nestlé, are setting internal standards that often exceed legal requirements, creating a de facto global benchmark for safety, quality, and sustainability. In addition, harmonization of regulations, such as the Swiss Ordinance on Food Contact Materials and Germany’s new Ink Ordinance (GIO), is compelling ink manufacturers to innovate and ensure products meet global safety and compliance standards. The focus on NIAS and trace impurities necessitates advanced formulations and rigorous testing, driving demand for LM inks that offer exceptional purity and performance. This regulatory-driven push is a key market force, positioning LM inks as essential for food-safe, high-quality packaging globally.

Strategic Industry Consolidation and Capacity Expansion by Major Chemical Firms

The LM inks market is evolving from a niche specialty segment to a strategic core business for leading chemical firms, driven by acquisitions and targeted capacity expansion. For example, Siegwerk’s acquisition of Allinova in August 2025 added expertise in water-based dispersions and strengthened its “Circular Economy Coatings” business unit, enabling delivery of sustainable LM ink solutions at scale. In parallel, Flint Group has invested in a dedicated facility in India for energy-curable inks serving the label and narrow web sector, ensuring separate production lines to prevent contamination and meet growing demand in emerging markets. These moves reflect a strategic commitment to capturing market share, enhancing technical capabilities, and scaling production of specialized, sustainable LM inks. Industry consolidation also accelerates innovation, enabling companies to integrate advanced, bio-based, and circular formulations into their product portfolios.

Development of High-Performance Bio-Based and Circular Low Migration Inks

Sustainability and circular economy initiatives present a high-value opportunity for LM ink manufacturers to develop bio-based and recyclable formulations. The cosmetics and personal care sector exemplifies this demand, with companies like L’Oréal targeting 100% reusable, refillable, recyclable, or compostable packaging by 2025. Meeting these sustainability goals requires LM inks that do not compromise recyclability or compostability of the substrate, creating a premium market for high-performance formulations. Innovative solutions are emerging that enable efficient recycling by allowing inks to be easily washed off, ensuring clean recovery of paper or plastic. This convergence of regulatory compliance, environmental responsibility, and brand sustainability creates a robust market for bio-based LM inks with superior technical performance.

Expansion into Non-Food Sensitive Segments with High-Growth Potential

Beyond food packaging, LM inks are increasingly finding applications in pharmaceutical, nutraceutical, and personal care sectors, where chemical migration poses significant safety risks. Pharmaceutical packaging, including drug containers, supplements, and medical devices, requires inks that comply with strict safety standards, mirroring those in the food industry. Similarly, personal care products such as lotions, shampoos, and liquid creams demand LM inks to prevent contamination from ink components, ensuring consumer safety and regulatory compliance. Brands are proactively implementing internal standards that exceed legal requirements, positioning LM inks as a differentiator in these high-value markets. Expansion into these adjacent segments provides ink manufacturers with near-term growth opportunities while reinforcing the critical importance of product safety and compliance.

Competitive Landscape: Leading Companies Driving the Low Migration Inks Market

The competitive landscape of the global Low Migration Inks Industry is shaped by five key players—Sun Chemical, Siegwerk, Flint Group, Hubergroup, and Toyo Ink—each leveraging innovation, sustainability, and compliance as their competitive levers. These companies are investing in advanced ink technologies, expanding global footprints, and developing circular economy solutions to meet the fast-rising demand for food-safe packaging inks.

Sun Chemical: Investing in Next-Generation Low Migration Inks

Sun Chemical, part of the DIC Group, offers a broad range of low migration inks under its SunCure and SunLit series, tailored for food, pharmaceutical, and personal care packaging. The company’s European R&D center (January 2025) is pivotal in advancing high-performance, eco-friendly ink technologies. Sun Chemical’s focus on UV LED and water-based inks positions it at the forefront of sustainable, energy-efficient printing solutions. With specialized offerings such as DigiStrato and DigiSpectro, the company underscores its leadership in odor-free, minimal-migration inks that adhere to global safety benchmarks.

Siegwerk: Circular Economy Leadership in Safe Packaging

Siegwerk has established itself as a pioneer in safe packaging inks with its SICURA product line, covering flexo, gravure, and offset printing applications. The company’s SICURA NutriJet UV inkjet inks are designed specifically for sensitive packaging, while innovations in bio-renewable water-based inks reinforce its sustainability agenda. Siegwerk’s strategy emphasizes its role in the circular economy, ensuring inks contribute to recyclability and compostability of packaging. Its strong technical support and integration expertise give it a distinctive edge in partnering with converters and brand owners to streamline compliance and efficiency.

Flint Group: Expanding Sustainable Low Migration Portfolios

Flint Group is recognized for its Novasens® low migration ink series for sheetfed and web offset applications in sensitive food and luxury packaging. The company is expanding its sustainable offerings, including Hydrofast® AFS 359, a low-odor offset ink certified by ISEGA. Its strategic focus is on high-performance, mineral oil-free inks aligned with evolving safety and sustainability norms. Flint Group’s deep expertise across multiple printing technologies and consumables makes it a comprehensive solutions provider, supporting customers with inks, coatings, and chemicals under one umbrella.

Hubergroup: Backward Integration Strengthens Market Position

Hubergroup has long been a pioneer in LMIs with its MGA ink series, trusted by food packaging brands worldwide. The company’s MGA Natura inks, built on innovative binder technology, ensure reduced migration risk while protecting food’s organoleptic properties. Its backward integration, producing raw materials in-house, enhances quality control and sustainability. Showcased in early 2025 at a major industry event in India, Hubergroup’s focus on eco-friendly and efficient printing solutions reinforces its leadership in aligning safety with sustainability in offset and board printing.

Toyo Ink: Innovating with Advanced Flexographic Solutions

Toyo Ink brings deep chemical expertise to its STERAFLEX series, designed for flexographic and gravure printing in sensitive packaging. In August 2025, the company launched a new low migration UV flexo ink in Europe, directly addressing rising regulatory scrutiny and customer demand for high-quality, food-safe inks. With a strong focus on bio-based and digital printing technologies, Toyo Ink is strategically positioning itself as a partner of choice for brands seeking both compliance and print excellence. Its ability to deliver across inks, coatings, and adhesives highlights its integrated approach to packaging solutions.

Low Migration Inks Market Share Insights

UV-Curable Inks Dominate Market Share by Ink Type in the Low Migration Inks Industry

UV-curable inks command the largest 45% share of the low migration inks market, reflecting their unmatched performance in preventing contamination of sensitive products. Their instant curing into a highly cross-linked polymer matrix under UV light locks in ink components, virtually eliminating migration risks while providing scratch resistance, high print quality, and fast production speeds. These attributes make them indispensable in flexible packaging films and food labels where regulatory compliance and consumer safety are paramount. Water-based inks secure a strong second position, driven by low VOC emissions, recyclability, and safety advantages that align with global sustainability mandates, particularly in paperboard-based packaging. Solvent-based inks, once the industry standard, are steadily declining under regulatory and environmental pressure, while oil-based inks retain a niche presence in specialized sheet-fed offset applications. Together, this landscape underscores how UV-curable inks dominate compliance-driven applications, while water-based inks expand as the sustainable growth driver in low migration printing technologies.

Food and Beverage Packaging Drives Market Share by Application in the Low Migration Inks Industry

Food and beverage packaging accounts for 60% of the global low migration inks industry, making it the overwhelmingly dominant application segment. The sheer scale of packaged food production, combined with stringent regulations such as EU 10/2011 and FDA standards, drives demand for inks that safeguard against harmful migration into consumables. Flexible packaging films, multilayer laminates, and paperboard cartons all rely heavily on UV-curable and water-based low migration inks to ensure product safety, stability, and compliance in high-speed packaging operations. Pharmaceutical packaging represents the second most critical end-use, where even microscopic ink transfer could compromise drug efficacy or safety, resulting in the strictest quality verification protocols. Cosmetics and personal care applications continue to expand, with “clean label” and safety-conscious beauty products adopting low migration inks to meet consumer trust expectations. Other niches such as baby food, pet food, and tobacco packaging extend this focus, often adopting pharmaceutical-grade standards. This segmentation demonstrates how food and beverage packaging anchors market volume, while pharmaceuticals and cosmetics drive regulatory intensity and high-value adoption of low migration inks.

United States Low Migration Inks Market Fueled by Regulatory Compliance and Sustainable Innovations

The U.S. low migration inks market is primarily driven by stringent FDA regulations for food and pharmaceutical packaging, which mandate inks that do not transfer harmful substances to packaged products. This regulatory environment is a key driver for the adoption of low-migration ink formulations. Companies are also focusing on sustainable innovations, exemplified by INX International Ink Co.’s DuraInx HRC, a new ink launched in April 2023 containing up to 40% renewable content. Additionally, the growing adoption of UV-curable and LED-curable inks offers instant drying, enhanced durability, and minimal VOC emissions, aligning with environmental sustainability goals.

Corporate investments are further strengthening market capabilities. Sun Chemical Corporation opened an advanced testing facility in late 2022 to ensure compliance with evolving regulations, enhancing trust among brand owners and consumers. The market sees strong demand across food and beverage, pharmaceutical, and e-commerce packaging sectors, with increasing requirements for corrugated packaging, where safety and product integrity are crucial. The U.S. government’s focus on infrastructure upgrades and manufacturing reshoring complements the push for bio-based inks, further accelerating market growth.

Germany’s Low Migration Inks Market Leading Through Stringent Regulations and Circular Economy Initiatives

Germany’s low migration inks industry is shaped by one of the world’s strictest regulatory frameworks, including the German Ink Ordinance and EU Food Contact Materials regulations. These regulations drive the adoption of high-performance, low-migration ink formulations to meet safety standards in food packaging. Technological innovations from companies like Siegwerk Druckfarben and hubergroup Deutschland focus on UV and water-based inks offering rapid curing and high chemical resistance, while cost-effective low-migration offset inks cater specifically to food packaging applications.

Germany also emphasizes sustainability and the circular economy, leading to the development of easily de-inkable systems for efficient paper and board recycling. Strategic corporate investments by Ardex and Sun Chemical are enhancing production capabilities and supporting the growing demand for eco-friendly and high-performance inks, positioning Germany as a global leader in sustainable printing technologies.

China Expands Low Migration Inks Market Through Regulatory Reforms and Green Initiatives

China’s low migration inks market is benefiting from the government’s dual carbon goal and initiatives such as the Action Plan for Large-Scale Equipment Updates and Consumer Goods Replacement, which promote sustainable materials and reduce excessive packaging. Regulatory reforms, including GB 4806.14-2023, set specific requirements for inks used in food packaging and mandate shared safety responsibility between ink manufacturers and printing enterprises, significantly boosting demand for low-migration inks.

Technological advancements in automation and AI-driven production are improving efficiency, while large-scale infrastructure projects like the Belt and Road Initiative are driving demand for durable and reliable packaging inks. The focus on domestic manufacturing to replace imported technologies supports local capacity expansion, especially in the booming e-commerce, electronics, and food and beverage sectors, creating substantial opportunities for specialized low-migration inks in China.

India’s Low Migration Inks Market Strengthens With Regulatory Reforms and Advanced Manufacturing

India’s low migration inks industry is gaining momentum following the BIS prohibition of toluene-based inks under IS15495, a regulatory step strongly promoted by companies like DIC India. This initiative is driving the adoption of toluene-free and ketone-free ink formulations, particularly in food and pharmaceutical packaging, enhancing product safety and compliance.

Technological adoption is increasing to meet the needs of India’s growing industrial and urban sectors. Investments like DIC India’s state-of-the-art manufacturing facility in Gujarat highlight the commitment to producing high-performance, low-migration inks that align with international standards. The market sees strong demand across food, beverage, and pharmaceutical sectors, with rising exports fueling the need for modern and safe packaging inks.

Japan’s Low Migration Inks Market Focuses on Advanced Materials and Specialty Applications

Japan is a global leader in precision manufacturing, and its low migration inks market is pivotal in the country’s advanced production ecosystem. Manufacturers like Toyo Ink and Sakata INX are innovating in UV, LED, and specialty inks. Regulatory changes effective June 1, 2025, introduced a positive list for synthetic materials in food packaging, driving the development of safer and compliant low-migration inks.

Japanese players are focusing on high-performance, specialty inks with enhanced barrier properties, self-sealing capabilities, and aesthetic improvements. Examples include Toyo Ink Europe’s Steraflex GIO UV, a flexographic printing ink fully compliant with EU and German regulations, demonstrating the country’s focus on functional, high-quality, and regulatory-compliant printing solutions.

Brazil’s Low Migration Inks Market Accelerates Through Sustainable Practices and Strategic Investments

Brazil’s low migration inks industry is supported by the National Solid Waste Policy, which encourages sustainable packaging and inks. Technological advancements are driving innovation in biodegradable, recyclable, and compostable inks, reducing environmental impact and supporting carbon-neutral initiatives.

Corporate investments are significant, with Toyo Ink Brazil maintaining two modern factories and R&D laboratories to meet growing demand, and INX International opening a new facility in March 2025 to enhance regional service capabilities. Strong demand from food, beverage, and agricultural sectors, coupled with increasing consumption of processed and ready-to-eat foods, is fueling market growth. This positions Brazil as a key player in the sustainable low migration inks market in Latin America.

Low Migration Inks Market Report Scope

Low Migration Inks Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.2 Billion

|

|

Market Size (2034)

|

$13.9 Billion

|

|

Market Growth Rate

|

9.4%

|

|

Segments

|

By Ink Type (UV-Curable Inks, Water-based Inks, Solvent-based Inks, Oil-based Inks), By Printing Process (Flexographic Printing, Gravure Printing, Lithographic Printing, Digital Printing), By Application (Food & Beverage Packaging, Pharmaceutical Packaging, Cosmetics & Personal Care Packaging, Other Applications), By Substrate (Paper & Paperboard, Flexible Packaging, Metal, Plastic)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sun Chemical Corporation (a DIC Company), Siegwerk Druckfarben AG & Co. KGaA, Flint Group, hubergroup Deutschland GmbH, TOYO INK CO., LTD. (artience Group), INX International Ink Co., DIC Corporation, Sakata INX Corporation, T&K Toka Co., Ltd., Marabu GmbH & Co. KG, ACTEGA GmbH, Kao Chimigraf S.A., Epple Druckfarben AG, Zeller+Gmelin GmbH & Co. KG, Doneck Euroflex S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Low Migration Inks Market Segmentation

By Ink Type

- UV-Curable Inks

- Water-based Inks

- Solvent-based Inks

- Oil-based Inks

By Printing Process

- Flexographic Printing

- Gravure Printing

- Lithographic Printing

- Digital Printing

By Application

- Food & Beverage Packaging

- Pharmaceutical Packaging

- Cosmetics & Personal Care Packaging

- Other Applications

By Substrate

- Paper & Paperboard

- Flexible Packaging

- Metal

- Plastic

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Low Migration Inks Market

- Sun Chemical Corporation (a DIC Company)

- Siegwerk Druckfarben AG & Co. KGaA

- Flint Group

- hubergroup Deutschland GmbH

- TOYO INK CO., LTD. (artience Group)

- INX International Ink Co.

- DIC Corporation

- Sakata INX Corporation

- T&K Toka Co., Ltd.

- Marabu GmbH & Co. KG

- ACTEGA GmbH

- Kao Chimigraf S.A.

- Epple Druckfarben AG

- Zeller+Gmelin GmbH & Co. KG

- Doneck Euroflex S.A.

* List Not Exhaustive

Methodology

The research methodology for the Low Migration Inks Market combines comprehensive primary and secondary approaches to ensure accurate, actionable insights for industry professionals. Primary research involved in-depth interviews with packaging engineers, ink formulators, regulatory experts, and senior executives across multiple regions, capturing firsthand perspectives on technological adoption, sustainability initiatives, and regulatory compliance. Secondary research included rigorous analysis of annual reports, patents, regulatory frameworks, verified industry journals, and sustainability disclosures to validate market trends, competitive dynamics, and growth projections. Advanced data triangulation was applied to confirm market sizing, CAGR, and regional expansion patterns, factoring in innovations in UV-curable, water-based, and bio-based ink technologies, as well as the increasing role of digital and specialty printing processes. Both top-down and bottom-up forecasting methods were utilized, while regional insights were contextualized against food contact regulations, consumer safety trends, and packaging innovation adoption. This multi-layered, systematic methodology ensures USDAnalytics delivers precise, fact-based, and strategically relevant intelligence on the global Low Migration Inks Market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.