Market Overview: Expanding Role of Flexographic Printing in Packaging

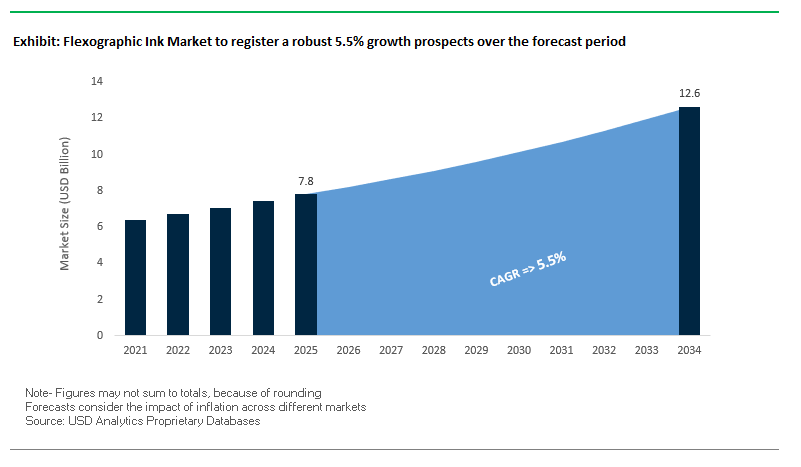

The Global Flexographic Ink Market is projected to grow from USD 7.8 billion in 2025 to USD 12.6 billion by 2034, registering a steady CAGR of 5.5%. Flexographic inks are the backbone of the flexographic printing process, which dominates high-volume applications across flexible packaging, labels, corrugated boards, and folding cartons. The industry is being shaped by sustainability imperatives, technological innovations, and the rising demand for high-definition printing that can rival offset and rotogravure quality.

A defining trend is the shift toward water-based and UV-curable inks, aligning with global VOC regulations and helping brands achieve their carbon reduction goals. The demand for low-migration inks is surging, particularly in food and beverage packaging, where consumer health and regulatory compliance are paramount. At the same time, HD flexo inks combined with advanced plate technology are improving print vibrancy and accuracy, enabling flexo printing to penetrate markets traditionally dominated by gravure.

The boom in e-commerce and short-run packaging is pushing converters to adopt inks compatible with hybrid digital-flexo presses, ensuring faster turnaround and personalization. Collectively, these trends make flexographic inks indispensable for industries seeking cost efficiency, premium print quality, and sustainable packaging.

Key Insights for industry professionals and buyers:

- Market to reach USD 12.6B by 2034 at CAGR 5.5%.

- Water-based and UV-curable inks gaining share due to VOC restrictions.

- Low-migration inks are essential for food & beverage compliance.

- HD flexo inks elevate flexography to compete with gravure.

- E-commerce growth drives demand for hybrid ink systems and shorter print runs.

Market Analysis: Recent Developments in the Flexographic Ink Industry

The Flexographic Ink Market is seeing strong innovation momentum, with recent product launches and strategic acquisitions highlighting the industry’s focus on sustainability, technology integration, and global consolidation.

In September 2025, Siegwerk showcased its circular economy-driven inks and coatings at the 12th Specialty Films and Flexible Packaging Summit in Mumbai, underlining its expanded functional coatings business. A month earlier, in August 2025, Flint Group launched its Flexocure® LEAP UV flexo inks at Labelexpo Europe, engineered to minimize migration and address the needs of food-grade applications.

In July 2025, DIC Corporation (through Sun Chemical) acquired Luminescence, a leading producer of security inks, strengthening its foothold in brand protection and government applications. Earlier in June 2025, a global study highlighted consumer demand for recyclable and compostable packaging, creating opportunities for compatible ink formulations that do not compromise recyclability.

Ink producers are also focusing on digital integration and smart packaging. Reports from April 2025 noted the rise of QR, NFC, and RFID-enabled packaging, with inks playing a vital role in enabling traceability and interactive consumer engagement. Cost pressures remain a challenge: February 2025 reports confirmed that fluctuations in petrochemical markets reduced adhesive and ink production by about 6% in 2024, prompting manufacturers to rethink procurement strategies.

In December 2024, Hubergroup introduced its Hydro-X range of water-based inks, designed for corrugated board, with improved drying times and optimized printability for difficult substrates.

Key Trends and Strategic Opportunities Shaping the Flexographic Ink Market

Accelerated Adoption of Water-Based Inks for Sustainable Packaging

The flexographic ink market is witnessing a rapid shift toward water-based inks, driven by sustainability commitments from brand owners and regulatory mandates to reduce Volatile Organic Compound (VOC) emissions. Converters are increasingly moving away from solvent-based inks to high-performance water-based systems, which require investment in new drying infrastructure and reformulation to meet performance standards. Water-based inks provide a safer working environment for press operators and comply with stringent environmental regulations. Companies like Follmann are offering water-based inks for flexible plastic and aluminum packaging, while DIC Corporation, in collaboration with the Suntory Group, developed the “Marine Flex LM-R” water-based flexo ink with significantly lower VOC and CO2 emissions compared to traditional solvent-based inks. This trend creates a high-value growth avenue, particularly as ongoing R&D addresses historical challenges in drying time and adhesion, making water-based inks a compliant, safe, and performance-ready solution. The adoption of these inks is reshaping the supply chain, requiring closer collaboration between ink manufacturers and packaging converters.

Development of Advanced Inks for Monomaterial Plastic Packaging

With the global push toward recyclable monomaterial packaging (e.g., all-polyethylene or polypropylene structures), ink manufacturers are innovating to ensure strong adhesion on polyolefins without compromising recyclability. Traditional nitrocellulose-based inks can cause odor, discoloration, and mechanical degradation in recycled streams, limiting circularity. Companies such as Siegwerk have launched NC-free ink series for PE and PP packaging, while Flint Group offers polyurethane-based inks compatible with recycling guidelines. Regulatory developments like the EU Packaging and Packaging Waste Regulation (PPWR) are further propelling demand for these advanced inks. This trend strengthens the interconnected value chain, fostering partnerships between ink manufacturers, packaging converters, and recycling organizations such as RecyClass and CEFLEX, ensuring seamless adoption of circular economy-compliant ink solutions.

Formulation of Energy-Curable LED Inks for Efficiency and Performance

The development of UV-LED curable flexographic inks represents a major growth opportunity, offering energy savings, longer lamp life, and compatibility with heat-sensitive substrates. UV-LED lamps consume up to 70% less energy than traditional mercury lamps and have service lives up to 20,000 hours, dramatically lowering operational costs. This technology enables short-run production and rapid design testing, making it especially appealing for D2C brands. Studies confirm that instant curing allows printing on thin films and shrink sleeves without deformation. Companies providing LED-optimized inks are creating a more innovative value chain, collaborating with lamp system providers to deliver energy-efficient, cost-effective, and high-performance flexographic solutions.

Expansion of Functional and Smart Inks for Enhanced Packaging

Beyond color, functional and smart inks are emerging to provide oxygen barriers, antimicrobial properties, or printed electronics for smart packaging. Conductive inks can enable RFID/NFC circuits on packaging, giving consumers interactive experiences while maintaining recyclability. Oxygen-scavenging inks extend food shelf life, reducing spoilage and food waste. Academic studies on silver nanoparticle-based conductive inks and oxygen-scavenging formulations confirm these developments. This opportunity allows ink manufacturers to tap into higher-value segments, supporting sustainability and supply chain transparency. Collaboration between ink producers, technology firms, and food scientists is creating a more interconnected and innovative ecosystem, positioning flexographic inks as critical enablers of circular, smart, and sustainable packaging solutions.

Competitive Landscape: Leading Innovators in the Flexographic Ink Market

The Global Flexographic Ink Market is highly competitive, with leading players expanding their portfolios, strengthening global footprints, and aligning innovation pipelines with sustainability and regulatory needs.

Siegwerk strengthens circular economy-focused coatings

Siegwerk is recognized globally for its packaging inks and coatings, with a strong focus on safety and sustainability. In September 2025, it showcased new circular ink solutions in Mumbai, following its acquisition of Allinova. With dedicated business units like Circular Economy Coatings (CEC), Siegwerk is enabling recyclability in packaging design. Its portfolio spans solvent-based, water-based, and UV flexo inks tailored for flexible packaging, corrugated, and labels.

Sun Chemical expands through DIC and Luminescence acquisition

As part of DIC Corporation, Sun Chemical is the largest global producer of printing inks. It has a strong innovation pipeline in bio-renewable inks, UV-LED curables, and low-migration formulations. In July 2025, it acquired Luminescence, expanding into security inks. Its flagship SunSpectro® and SunVisto® inks are widely adopted in flexible films, corrugated board, and high-speed label printing.

Flint Group launches Flexocure® LEAP UV flexo inks

Flint Group has reinforced its innovation credentials with the launch of Flexocure® LEAP inks in August 2025, designed to minimize migration risks for food-grade applications. Its portfolio also includes TerraCode® water-based inks and ZenCode® solvent-based inks, all aligned with circular economy requirements. Flint also leads in UV LED curing systems through its EkoCure® inks, enabling high efficiency and reduced energy consumption.

DIC Corporation leverages AI-driven product development

DIC Corporation, the parent of Sun Chemical, is a global powerhouse in inks, pigments, and specialty chemicals. Beyond acquisitions, it is investing in AI and materials informatics to accelerate ink formulation and sustainability. In 2024, it introduced an NC-free toolbox for flexible packaging inks, targeting future regulatory compliance. Its flexographic portfolio spans solvent, water-based, and UV inks, catering to high-definition printing needs across packaging formats.

Hubergroup launches Hydro-X and Gecko Platinum Flexo series

Hubergroup, with its long-standing expertise, remains a leading supplier of tailor-made flexographic inks. In December 2024, it launched Hydro-X inks for corrugated board, optimized for fast drying and difficult substrates. Its Gecko Platinum Flexo series, a pure PU-based ink system, is free from monomeric plasticizers and designed for high-performance lamination and high-temperature applications. With modular ink families, Hubergroup enables reliability and flexibility for diverse packaging segments.

Flexographic Ink Market Share Insights

Flexible Packaging Commands Market Share in Flexographic Ink Applications

In the flexographic ink market, flexible packaging accounts for 45% of global application share by 2025, cementing its leadership as the most demanding and technically complex printing segment. Inks for flexible packaging must adhere to diverse substrates like PE, PP, PET, and foils, deliver strong chemical and heat resistance, and meet strict global regulations for food contact safety, making them the benchmark for high-performance ink innovation. Corrugated containers follow with 25% share, boosted by the explosive rise of e-commerce, which demands fast-drying, durable, and cost-effective inks that can withstand logistics stress while delivering sufficient print quality for branding. Tags, labels, and folding cartons collectively represent a growing premium niche, requiring inks with high gloss, abrasion resistance, and advanced features like metallic finishes and scratch-off properties to enhance shelf appeal. Conversely, paper printing continues its decline, pressured by digitalization and media shifts, leaving it as a legacy but shrinking application for flexographic inks. This segmentation highlights how flexible packaging drives technical advancement, corrugated containers anchor volume, and premium labels and cartons fuel high-value ink innovation.

Polyurethane Resins Hold Market Leadership in Flexographic Inks

Polyurethane resins dominate the flexographic ink market with a 40% share in 2025, driven by their unmatched versatility, chemical resistance, and adhesion across a wide range of substrates, particularly in flexible packaging and premium labels. They provide the durability required for high-performance laminates while ensuring compliance with food packaging regulations, making them the top choice for converters worldwide. Acrylic resins follow with 25% share, offering cost-effective versatility and strong performance for corrugated, paper, and certain flexible packaging applications, though they lack the superior chemical and heat resistance of polyurethanes. Polyamide resins maintain a specialized role in untreated PE applications like bread bags, while nitrocellulose resins retain share in surface printing due to their fast-drying properties and high gloss, albeit gradually losing ground to more advanced formulations. The “Others” category, including vinyl, ketone, and polyester resins, contributes to niche high-performance needs, particularly for adhesion or resistance in specialty packaging. Collectively, this segmentation illustrates how polyurethane resins set the performance standard for modern flexographic inks, while acrylics balance cost and versatility, and legacy resin types fade into specialized or declining roles.

United States Flexographic Ink Market Driven by Low-VOC and UV-LED Innovations

The U.S. flexographic ink market is influenced by a complex regulatory environment, with the Environmental Protection Agency (EPA) issuing control technique guidelines to reduce VOC emissions in flexible packaging printing. This regulatory push is driving manufacturers toward low-VOC, water-based, and UV-curable ink systems that enhance sustainability while maintaining print performance. Technological advancements such as UV-LED dual cure flexographic inks for shrink sleeves are meeting the growing demand for high-quality, distinctive labels.

Corporate investments are further strengthening the market. INX International Ink Co., for instance, is expanding its sustainable ink portfolio to align with consumer expectations and regulatory mandates. Key applications are concentrated in food and beverage, pharmaceuticals, and consumer goods packaging, where durability, brand appeal, and e-commerce readiness are critical. Sustainability remains a central business imperative, with bio-based and low-migration inks increasingly preferred for food contact applications, supporting environmental compliance and corporate responsibility goals.

Germany Flexographic Ink Market Advances Through Water-Based Innovations and Circular Economy Leadership

Germany’s flexographic ink market operates under stringent regulations, including the EU Packaging and Packaging Waste Regulation (PPWR), which encourages reuse, recycling, and the reduction of harmful chemicals like PFAS. This regulatory framework has driven innovations in water-based inks for flexible packaging, exemplified by Siegwerk’s fully automated production facility producing next-generation inks aligned with Germany’s sustainable manufacturing focus.

Leadership in the circular economy is further bolstered by Germany’s Extended Producer Responsibility (EPR) system, incentivizing packaging designs that are easier to recycle. The food and personal care packaging sectors are key markets, requiring low-migration and food-safe ink formulations to meet rigorous safety and environmental standards. Germany’s focus on sustainability and high-quality production is reinforcing its position as a leading market for advanced flexographic inks in Europe.

China Flexographic Ink Market Expands with Dual Carbon Goals and Domestic Innovation

China’s flexographic ink industry is strongly influenced by the government’s “dual carbon” objectives, which drive a green transformation across manufacturing sectors. Regulatory reforms, including the National Food Safety Standard for Adhesives in Food Contact Materials (GB 4806.15-2024), enforce strict migration limits to ensure safety and quality in packaging inks. These regulations are accelerating the adoption of water-based and environmentally friendly inks.

Technological advancements are reshaping production, with AI and “5G plus industrial internet” integration enhancing efficiency and capacity. Domestic manufacturers, such as StarColor, are expanding production to meet growing local demand with FDA-compliant inks. Strategic collaborations, like the Hanghua Harima Ink joint venture with T&K Toka, are producing high-quality water-based flexographic inks for both domestic and export markets. Rapid growth in e-commerce, food and beverage, and chemical industries continues to fuel demand for reliable, sustainable flexographic ink solutions.

India Flexographic Ink Market Fueled by Circular Economy Policies and Advanced Flexo Presses

India’s flexographic ink market is benefiting from government initiatives promoting a circular economy, including the draft Environment Protection (Extended Producer Responsibility for Packaging) Rules, 2024. These measures create opportunities for sustainable ink solutions that meet stringent environmental and food-grade standards. Technological adoption is rising, with automated flexo presses like Echaar’s FlexoDelight CI Flexo Press enabling simplified operations, automated ink management, and cleaning efficiencies.

Corporate investments are expanding production capacity under the “Make in India” initiative, boosting the domestic market for high-performance inks. Key applications include food and beverage and personal care packaging, particularly driven by e-commerce demand. The growing domestic food processing industry and emphasis on sustainable, modern packaging technologies are pivotal in shaping India’s flexographic ink market, fostering both innovation and local manufacturing capabilities.

Japan Flexographic Ink Market Leads in Sustainable Water-Based and High-Performance Formulations

Japan’s flexographic ink market is anchored in precision manufacturing and advanced material development. Companies like DIC Corporation are pioneering high-density water-based inks that achieve gravure-like print quality, supporting sustainable printing practices. Regulatory guidance under the Plastic Resource Circulation Act (April 2022) promotes environmentally friendly designs and supports the reduction of single-use plastics, influencing the development of inks compatible with bio-based packaging.

Sustainability is further emphasized by collaborations, such as Asahi Photoproducts with the Flexo Technical Association Japan (FTAJ), demonstrating a 65% reduction in GHG emissions using water-based flexo inks compared to solvent-based gravure inks. Innovation in functionality includes nanoparticle-enhanced formulations for improved print quality and anti-counterfeiting features. Japan’s focus on high-performance, eco-friendly inks ensures continued leadership in the Asia-Pacific flexographic ink market.

Brazil Flexographic Ink Market Strengthens Through Strategic Investments and Premium Packaging Solutions

Brazil’s flexographic ink industry is seeing substantial corporate investments, exemplified by INX International’s new 65,000 sq. ft. facility in Cabreuva (February 2025), capable of producing 2,000 tons of solvent-based inks per month for South America. This investment highlights the country’s commitment to supporting packaging demand, particularly in food consumption and exports.

Technological advancements include premium and hybrid digital printing solutions requiring high-performance flexographic inks, reinforcing the country’s position in innovative packaging applications. Domestic market performance remains closely tied to internal economic activity, with strong packaging demand driven by food and beverage consumption. Brazil’s emphasis on specialized, high-quality ink solutions and sustainable practices positions it as a key growth market in Latin America.

Flexographic Ink Market Report Scope

Flexographic Ink Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.8 Billion

|

|

Market Size (2034)

|

$12.6 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Technology (Water-Based Inks, Solvent-Based Inks, UV-Curable Inks), By Application (Flexible Packaging, Corrugated Containers, Folding Cartons, Tags & Labels, Paper Printing), By Resin Type (Acrylic, Polyurethane, Polyamide, Nitrocellulose, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sun Chemical Corporation, Flint Group, Siegwerk Druckfarben AG & Co. KGaA, DIC Corporation, Hubergroup Holding SE, INX International Ink Co., Toyo Ink SC Holdings Co., Ltd., T&K Toka Co., Ltd., Zeller+Gmelin GmbH & Co. KG, Wikoff Color Corporation, Fujifilm Corporation, SAKATA INX Corporation, DuPont de Nemours, Inc., ALTANA AG, Suminco S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flexographic Ink Market Segmentation

By Technology

- Water-Based Inks

- Solvent-Based Inks

- UV-Curable Inks

By Application

- Flexible Packaging

- Corrugated Containers

- Folding Cartons

- Tags & Labels

- Paper Printing

By Resin Type

- Acrylic

- Polyurethane

- Polyamide

- Nitrocellulose

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Flexographic Ink Market

- Sun Chemical Corporation

- Flint Group

- Siegwerk Druckfarben AG & Co. KGaA

- DIC Corporation

- Hubergroup Holding SE

- INX International Ink Co.

- Toyo Ink SC Holdings Co., Ltd.

- T&K Toka Co., Ltd.

- Zeller+Gmelin GmbH & Co. KG

- Wikoff Color Corporation

- Fujifilm Corporation

- SAKATA INX Corporation

- DuPont de Nemours, Inc.

- ALTANA AG

- Suminco S.A.

* List Not Exhaustive

Methodology

USDAnalytics employed a rigorous, integrated research methodology to deliver a comprehensive analysis of the Global Flexographic Ink Market. This approach combined extensive primary research through interviews with industry stakeholders, including ink manufacturers, packaging converters, technology providers, and sustainability experts, with secondary research from regulatory reports, corporate filings, trade associations, and industry publications. Market sizing, growth projections, and trend identification were assessed across key parameters such as ink technology (water-based, solvent-based, UV-curable), resin types (polyurethane, acrylic, polyamide, nitrocellulose), and applications (flexible packaging, corrugated, folding cartons, labels). Regional dynamics, including the U.S., Germany, China, India, Japan, and Brazil, were evaluated to understand regulatory frameworks, sustainability initiatives, and technological adoption. Special emphasis was placed on innovations like low-migration inks, LED-UV curing, smart and functional inks, and circular economy solutions. Key corporate developments, M&A activities, and strategic partnerships were also analyzed to provide insights into competitive positioning, operational efficiency, and high-value growth opportunities. The resulting research equips industry professionals, converters, and decision-makers with actionable intelligence to navigate market expansion, regulatory compliance, and technological evolution in flexographic ink applications.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.