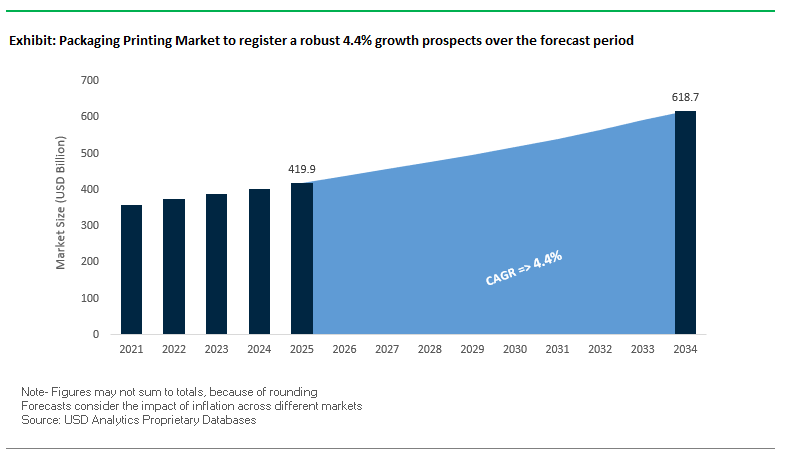

Packaging Printing Market Set to Surge from $419.9 Billion in 2025 to $618.7 Billion by 2034 Amid Digitalization and Sustainability Trends

The Global Packaging Printing Market is expected to grow from $419.9 billion in 2025 to $618.7 billion by 2034, registering a CAGR of 4.4%. The market is witnessing robust demand driven by e-commerce, D2C brands, and high-value consumer goods, which increasingly rely on customized, functional, and sustainable packaging solutions. Packaging printing ensures brand visibility, product safety, and regulatory compliance, while integrating advanced technologies like digital printing, smart packaging, and automation.

Key Insights for Industry Professionals:

- E-commerce and Personalization Driving Short-Run Printing: Digital technologies enable brands to produce on-demand, personalized packaging, enhancing consumer engagement and brand loyalty.

- Sustainability as a Core Industry Focus: Adoption of water-based, UV-cured inks, and recyclable substrates addresses environmental regulations and consumer expectations.

- Smart Packaging for Security and Functionality: Integration of QR codes, RFID tags, and other identifiers enables anti-counterfeiting, real-time tracking, and interactive brand communication.

- Automation and AI Enhancing Production Efficiency: Advanced software and AI-based color calibration systems ensure consistency, speed, and reduced human error in high-volume operations.

- Rising Demand for High-Quality Visual and Tactile Effects: Innovations in inks and coatings provide superior gloss, color fidelity, and haptic experiences, crucial for premium products.

The market is evolving rapidly, driven by the intersection of digital innovation, sustainability, and consumer-centric packaging solutions, positioning it as a strategic enabler of brand differentiation and regulatory compliance.

Recent Technological Advancements and Strategic Moves Reshaping Global Packaging Printing

The Packaging Printing Industry is highly dynamic, with strategic acquisitions, product launches, and technology innovations driving transformation. In August 2025, Siegwerk acquired Allinova, strengthening its capabilities in functional coatings for sustainable packaging. In July 2025, Sun Chemical introduced SunCure Advance ECO UV inks with 25–30% bio-renewable content, certified by the American Soybean Association, while Xerox completed its acquisition of Lexmark, expanding its portfolio and hybrid workplace solutions.

In June 2025, Hubergroup launched the HYDRO-X CONTACT water-based inks for direct food contact applications, addressing safety and regulatory needs. May 2025 saw Durst Group acquire callas software, enabling integrated and open digital printing workflows, and in April 2025, the Amcor-Berry Global merger created a new leader in consumer packaging, increasing demand for printing services across their portfolios.

Earlier in March 2025, XSYS completed the acquisition of MacDermid Graphics Solutions, reinforcing its position in flexographic and pre-press markets, while in January 2025, HP showcased its HP Indigo presses and solutions at Labelexpo India 2024, targeting in-mold labels and flexible packaging.

Trends and Opportunities Transforming the Packaging Printing Market

Accelerated Adoption of Digital Printing for Short-Run and Versioned Packaging

The packaging printing market is witnessing unprecedented momentum toward digital printing technologies, fueled by demand for agility, customization, and sustainability. Traditional flexographic and gravure methods, while efficient at scale, are being disrupted by digital printing’s ability to serve short-run, versioned, and customized packaging needs. Research indicates that for production runs under 4,000–8,000 units, digital printing is substantially more cost-effective, with the highest savings for runs under 2,000 packages. This makes digital printing the preferred choice for seasonal promotions, limited-edition packaging, and hyper-local marketing campaigns.

Another crucial advantage is speed-to-market. By eliminating plate production, digital printing reduces lead times drastically. Comparative studies show that packaging can move from concept to shelf in just 7–10 days with digital technology, versus weeks with flexography. This rapid turnaround empowers FMCG, personal care, and beverage brands to respond to evolving consumer trends almost in real time.

The market is further supported by heavy capital investment in digital infrastructure. HP’s launch of the Indigo 120K HD press in 2025, designed for high-volume and AI-driven digital printing, signals that digital is now capable of competing at scale. Simultaneously, digital printing reduces waste—studies estimate up to 30% material savings on short-run jobs—positioning it as a key enabler of sustainable packaging strategies.

Mandated Shift to Low-VOC and UV-LED Curable Inks for Compliance

A second transformative trend is the regulatory-driven shift to low-VOC and UV-LED curable inks. Governments worldwide are phasing out solvent-based inks due to their volatile organic compound (VOC) emissions, which contribute significantly to air pollution. For example, China’s packaging industry alone accounts for 30% of global VOC emissions, making it a central target of its 14th Five-Year Plan. Similarly, the EU’s Carbon Border Adjustment Mechanism (CBAM) reinforces the push toward low-emission packaging processes.

UV-LED curing technology is at the forefront of compliance and sustainability. These systems use just 20–25% of the energy of mercury lamps, with lifespans exceeding 20,000 hours—ten times longer than conventional lamps—leading to 70% cost savings in operations. Beyond efficiency, the low heat output (around 60°C) allows printing on heat-sensitive substrates like thin plastic films, critical for food and electronics packaging.

Leading equipment manufacturers are embedding this technology. EFI’s VUTEk LED printers, for example, deliver energy efficiency, improved workplace safety, and compatibility with a wide range of materials. Combined, these factors make UV-LED inks the new industry standard, ensuring regulatory compliance while enhancing print quality and sustainability.

Expansion of Digital Watermarking for Smart Packaging and Recycling

One of the most significant opportunities in the global packaging printing market is the commercialization of digital watermarking. Industrial trials under the HolyGrail 2.0 initiative have demonstrated 99% detection accuracy and 95% ejection efficiency, even on soiled or crushed packaging. These results validate digital watermarking as a scalable, industrial-ready recycling solution.

This technology allows for intelligent packaging sortation, distinguishing materials at SKU-level precision. For example, PET bottles can be sorted into separate streams for food-grade and non-food-grade recycling, unlocking higher-value secondary materials. Beyond waste management, digital watermarks transform packaging into a consumer engagement channel. With a simple smartphone scan, consumers can access product traceability, sustainability disclosures, or AR experiences, amplifying brand transparency and loyalty.

Accessibility is also improving. Digimarc’s licensing model enables brands and converters to integrate watermarks into existing printing workflows without specialized inks or substrates. This makes smart, digitally enabled packaging achievable at scale, bridging the gap between compliance, sustainability, and marketing innovation.

Development of Functional and Smart Inks for Active Packaging

The second major opportunity lies in the adoption of functional and smart inks, which elevate packaging from a passive medium to an active enabler of safety, authenticity, and interaction. Invisible phosphorescent or magnetic inks provide brand owners with advanced anti-counterfeiting tools, particularly vital in pharmaceuticals, luxury goods, and premium food products.

Smart inks further enhance product quality and safety. Thermochromic inks change color when exposed to certain temperatures, giving consumers visible confirmation of proper storage conditions. This is highly relevant for beverages, dairy, and pharma cold chains. Meanwhile, conductive inks are unlocking interactive packaging. Projects such as OET’s NFC-enabled feta cheese packaging show how packaging can provide real-time traceability by connecting directly to a smartphone.

Equipment innovation is supporting adoption. HP’s new presses are designed to support specialty inks, allowing converters to integrate anti-counterfeiting and interactive features without disrupting production efficiency. This creates new revenue streams for converters while offering brands value-added packaging solutions that combine protection, engagement, and compliance.

Competitive Landscape Highlighting Leaders Driving Innovation, Sustainability, and Digital Transformation

The Packaging Printing Market is dominated by global leaders leveraging materials science, digital technology, and sustainability initiatives. These companies focus on high-performance solutions, short-run customization, and integrated packaging workflows, positioning themselves as key partners for brands seeking innovation and regulatory compliance.

HP Inc.: Pioneering Digital Printing Solutions for Flexible and On-Demand Packaging

HP Inc. is a global leader in digital printing technologies, offering HP Indigo and HP PageWide presses for high-quality, short-run, and customized packaging. In January 2025, HP showcased innovations for in-mold labels, flexible packaging, and folding cartons at Labelexpo India 2024. Its portfolio includes HP Indigo 6K, HP Indigo 200K presses, and PrintOS software for workflow automation. HP’s strategy emphasizes sustainable, on-demand printing that reduces environmental impact and generates new revenue streams.

Bobst Group SA: Integrating Printing and Converting Solutions for a Fully Connected Packaging Ecosystem

Bobst Group SA is a leading global provider of printing, converting, and folding solutions. In August 2025, it launched its first barrier paper metallizer using iMA technology, advancing sustainable packaging. Bobst offers gravure, flexo, and digital presses, including the MASTER M6 inline flexo press with oneECG technology. Its Vision 2025 strategy focuses on creating a digitized, automated, and sustainable packaging ecosystem, integrating machines, services, and digital tools.

Konica Minolta Inc.: Enabling Agile, High-Quality Digital Label Printing for Short-Run Applications

Konica Minolta provides digital printing solutions for labels and packaging, specializing in short-run, flexible, and cost-effective applications. Recent developments emphasize carbon footprint reduction and responsive supply chains, with success stories using the AccurioLabel series. Its portfolio includes AccurioJet KM-1e inkjet presses, delivering high-quality, sustainable, and customizable packaging solutions. Konica Minolta’s strategy focuses on helping manufacturers compete in fast-moving industrial markets with superior digital printing technology.

Siegwerk Druckfarben AG & Co. KGaA: Leading Functional and Sustainable Ink Solutions for Circular Packaging

Siegwerk is a global provider of printing inks and coatings for packaging and labels, known for product safety and sustainability via its HorizonNOW program. In August 2025, the company acquired Allinova, enhancing functional coatings expertise. Its offerings include water-based, solvent-based, and UV-curing inks, with emphasis on low-migration solutions for food packaging. Siegwerk focuses on circular packaging, mono-material solutions, and reducing environmental impact through strategic innovation.

Flint Group: Delivering Comprehensive Inks and Coatings Portfolio with Sustainability at the Core

Flint Group supplies inks and coatings for printing and packaging, offering solutions for flexo, gravure, and offset applications. In August 2025, Flint showcased Flexocure® LEAP UV flexo ink at Labelexpo Europe, highlighting its sustainable innovation. The company provides coatings, blankets, and pressroom consumables, with a strategy centered on enhancing efficiency, reducing costs, and supporting customers’ sustainability goals through continuous R&D investment.

Packaging Printing Market Share Insights, 2025-2034

Flexography Leads Market Share by Printing Technology in the Packaging Printing Industry

Flexography accounts for 44% of the global packaging printing market, making it the undisputed leader among printing technologies. Its dominance is built on unmatched versatility across substrates—including corrugated, labels, flexible films, and folding cartons combined with cost efficiency for medium-to-long production runs. Technological innovations in water-based and UV-curable flexographic inks have significantly improved print resolution and compliance with environmental regulations, reinforcing its role as the industry’s workhorse. While gravure and offset maintain strongholds in specific niches such as premium folding cartons and long-run snack packaging, their inflexibility and higher setup costs are eroding share. Digital printing, however, is the fastest-growing challenger, driven by short-run economics, variable data printing, and e-commerce personalization needs. Despite this shift, flexography continues to dominate as it strikes the optimal balance between high-speed mass production, quality consistency, and regulatory compliance, cementing its leadership across the global packaging sector.

Food and Beverage Dominates Market Share by End-Use Industry in the Packaging Printing Sector

The food and beverage industry accounts for 50% of packaging printing demand, making it the single largest and most influential segment. This dominance reflects both sheer production volume and strict compliance requirements, where low-migration inks and coatings are mandatory to ensure food safety. Printing in this segment must balance high-speed output for mass-market products with premium-quality graphics that enhance shelf visibility in competitive retail environments. Beverage shrink sleeves, flexo-printed flexible snack pouches, and offset folding cartons for frozen foods exemplify the diverse formats consumed by this sector. Household and cosmetics drive demand for aesthetic innovation with metallic and tactile finishes, while pharmaceuticals require precision, serialization, and sterilization-resistant inks. Electronics and industrial sectors emphasize functional durability, such as abrasion resistance and static control. Yet, the overwhelming share held by food and beverage ensures that this sector remains the anchor of global packaging printing innovation, setting quality, compliance, and sustainability benchmarks that ripple through every other industry.

United States Packaging Printing Market Driven by Digital Printing and Stringent VOC Regulations

The United States packaging printing market is increasingly defined by digital printing technologies and personalization trends, particularly in e-commerce. A 2024 consumer survey highlighted that 79% of shoppers are more likely to purchase products with scannable codes like QR codes, underscoring the role of digital printing in enabling smart packaging and interactive consumer engagement. The rise of short-run customization for consumer packaged goods (CPG) and food packaging is also boosting demand for flexible, cost-efficient digital print solutions.

The U.S. Environmental Protection Agency (EPA), alongside local air quality agencies such as California’s regulators, enforces some of the strictest limits on VOC emissions worldwide. This is accelerating the transition toward water-based, UV-curable, and low-VOC inks. Additionally, the Inflation Reduction Act is channeling investment into sustainable manufacturing processes, encouraging companies to adopt climate-friendly inks and materials. The FDA’s oversight of food-contact packaging inks ensures ongoing innovation in safe, food-grade formulations. Together, these factors make the U.S. a leader in both regulatory compliance and digital packaging printing innovation.

European Union Packaging Printing Market Shaped by PPWR and Stricter Labeling Rules

The European Union packaging printing market is strongly shaped by the Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025. This regulation mandates standardized labeling across all EU member states by 2028, requiring clear guidance on material composition, disposal methods, and recyclability. Such harmonization is pushing printers and converters to adopt eco-friendly inks, recyclable substrates, and de-inkable adhesives to meet circular economy targets.

In addition, the Regulation (EU) 2024/2865 amending the CLP Regulation for classification, labeling, and packaging of chemicals has raised compliance requirements for the industry, particularly for laboratory and industrial packaging. The ECHA’s REACH framework continues to restrict hazardous substances, fostering demand for compliant, safe, and sustainable printing materials. Furthermore, Denmark’s introduction of Extended Producer Responsibility (EPR) in October 2025 highlights the region’s shift toward producer accountability. Food, pharmaceuticals, and cosmetics sectors remain the largest adopters, making the EU a benchmark region for sustainable packaging printing innovation.

China Packaging Printing Market Accelerated by Green Policies and High-Volume Demand

China’s packaging printing market is evolving rapidly under the government’s 14th Five-Year Plan, which emphasizes controlling plastic pollution and expanding the remanufacturing sector. New policies and tax incentives for green technologies are encouraging companies to adopt sustainable printing solutions while expanding the domestic production of packaging substrates.

A strong trend is the development of lightweight, high-performance packaging with barrier properties and security features to combat counterfeiting, especially in consumer goods and pharmaceuticals. China’s massive scale plays a pivotal role: with over 175 billion parcel deliveries in 2024, demand for high-quality printed packaging is unprecedented. Domestic manufacturers are scaling up capacity to serve the consumer, agricultural, and chemical markets, positioning China as both a global hub for packaging printing production and a testbed for sustainable innovation.

India Packaging Printing Market Supported by FSSAI Standards and Eco-Friendly Regulations

India’s packaging printing market is governed by strict safety and sustainability standards. The Food Safety and Standards Authority of India (FSSAI) enforces packaging standards to ensure hygiene and product safety. The Food Safety and Standards (Packaging) Regulations, 2018 require inks for food packaging to comply with IS 15495, banning harmful substances such as phthalates, toluene, and non-food-grade pigments. These regulations are pushing manufacturers toward eco-friendly, food-grade inks.

The ban on single-use plastics in 2022 has created opportunities for water-soluble and biodegradable packaging, which demand new compliant printing techniques. Coupled with the Make in India initiative, the sector is seeing strong growth in domestic printing and converting operations across industries including food, beverages, automotive, electronics, and FMCG. The combination of rising e-commerce penetration, growing packaged food consumption, and government incentives makes India one of the fastest-growing packaging printing markets worldwide.

Japan Packaging Printing Market Advancing with Plastic Resource Law and Value-Added Labeling

Japan’s packaging printing market is undergoing transformation under the Plastic Resource Circulation Promotion Law, which took effect in 2025. This law mandates reduction or redesign of 12 types of single-use plastic products, fostering demand for compostable and reusable packaging formats that require advanced printing solutions. The industry is also shifting from a volume-driven to a profit-oriented model, with companies focusing on adding value to labels through functionality, design, and services.

The Japanese label industry reached USD 4.3 billion in shipments in 2024, marking a 2.4% annual growth, the highest in five years. This growth is driven by strong adoption of pressure-sensitive labels in food and shrink labels in beverages and alcohol. The food and beverage industry remains the largest consumer of packaging printing, supported by consumer preferences for aesthetically appealing, functional, and sustainable designs. Japan’s focus on innovation and sustainability ensures its position as a leading market for premium packaging printing solutions.

Brazil Packaging Printing Market Strengthened by PNRS and Food Labeling Mandates

Brazil’s packaging printing market is heavily influenced by the National Solid Waste Policy (PNRS), which sets comprehensive guidelines for waste reduction, reuse, and recycling. This has encouraged the adoption of sustainable packaging printing solutions and pushed companies to align with the circular economy. Additionally, the National Food and Nutrition Policy (PNAN) and Resolution No. 429/2020 mandate new front-of-pack warning labels on foods high in sugar, sodium, and saturated fats, driving fresh demand for innovative label printing.

A notable trend is the growing use of unit-dose packaging for household cleaning products, which reduces reliance on bulk plastic containers and requires efficient, high-quality printing. The food and beverage industry remains the largest consumer of packaging printing services, supported by Brazil’s position as a major producer of canned goods and processed foods. With sustainability regulations tightening and demand for advanced packaging formats rising, Brazil is becoming an important emerging market for eco-friendly and compliant packaging printing solutions.

Packaging Printing Market Report Scope

Packaging Printing Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$419.9 Billion

|

|

Market Size (2034)

|

$618.7 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Printing Technology (Flexography, Gravure, Offset, Digital, Screen Printing, Other Technologies), By Printing Ink (Aqueous, Solvent-Based, UV-Curable, Latex, Dye Sublimation, Other Inks), By Type (Corrugated, Flexible, Folding Cartons, Labels & Tags, Other Types), By End-Use Industry (Food & Beverage, Household & Cosmetics, Pharmaceutical, Consumer Electronics, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, WestRock Company, Smurfit Kappa Group Plc, DS Smith Plc, International Paper Company, Graphic Packaging Holding Company, Mondi Group, Huhtamaki Oyj, Sealed Air Corporation, Avery Dennison Corporation, CCL Industries Inc., Ball Corporation, Sonoco Products Company, R.R. Donnelley & Sons Company, Oji Holdings Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Printing Market Segmentation

By Printing Technology

- Flexography

- Gravure

- Offset

- Digital

- Screen Printing

- Other Technologies

By Printing Ink

- Aqueous

- Solvent-Based

- UV-Curable

- Latex

- Dye Sublimation

- Other Inks

By Type

- Corrugated

- Flexible

- Folding Cartons

- Labels & Tags

- Other Types

By End-Use Industry

- Food & Beverage

- Household & Cosmetics

- Pharmaceutical

- Consumer Electronics

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Printing Market

- Amcor plc

- WestRock Company

- Smurfit Kappa Group Plc

- DS Smith Plc

- International Paper Company

- Graphic Packaging Holding Company

- Mondi Group

- Huhtamaki Oyj

- Sealed Air Corporation

- Avery Dennison Corporation

- CCL Industries Inc.

- Ball Corporation

- Sonoco Products Company

- R.R. Donnelley & Sons Company

- Oji Holdings Corporation

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and multi-faceted research methodology to deliver actionable insights into the global Packaging Printing Market. Our approach integrates primary and secondary research, leveraging authoritative sources such as company reports, regulatory filings, industry journals, and interviews with key stakeholders including manufacturers, converters, and technology providers. Secondary research is used to identify macroeconomic indicators, regulatory frameworks, technological trends, and sustainability drivers affecting market dynamics. USDAnalytics then validates these findings through quantitative analysis, including CAGR calculations, market sizing, and share estimates segmented by printing technology, ink type, packaging format, and end-use industries. Advanced analytical tools, combined with insights from regional markets such as the United States, European Union, China, India, Japan, and Brazil, allow for accurate forecasting from 2025 to 2034. Emphasis is placed on emerging trends such as digital printing adoption, UV-LED curable inks, smart packaging, and eco-friendly formulations. The methodology ensures a robust understanding of competitive strategies, technological innovation, regulatory compliance, and sustainability initiatives shaping the packaging printing landscape, enabling industry professionals to make informed strategic decisions and optimize growth opportunities.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.