Mobile Phone Packaging Market Growth Forecast: $5.6 Billion in 2025 to $9.3 Billion by 2034 at 5.8% CAGR

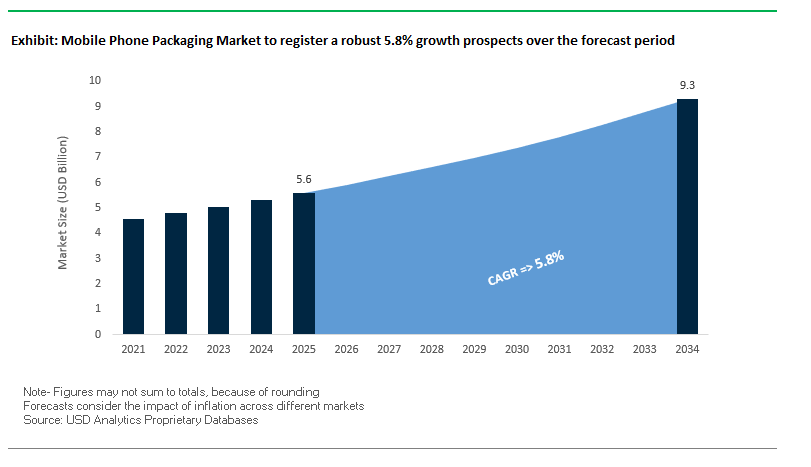

The global mobile phone packaging market is projected to grow from $5.6 billion in 2025 to $9.3 billion by 2034, exhibiting a CAGR of 5.8%. Growth is primarily driven by sustainability initiatives, the premiumization of unboxing experiences, and e-commerce protective packaging innovations. Packaging manufacturers are increasingly adopting eco-friendly materials, interactive technologies, and lightweight composites to meet consumer and regulatory demands.

Key Insights for Industry Stakeholders

- Elimination of single-use plastics: Companies like Samsung aim to remove plastics from mobile packaging entirely by 2025, reflecting a broader trend toward sustainable packaging solutions.

- Luxury and consumer engagement: Innovative designs using magnetic closures, pull-tabs, and premium finishes enhance the unboxing experience, driving brand differentiation.

- E-commerce resilience: Packaging must be durable, lightweight, and shock-resistant, supporting safe delivery in global online retail channels.

- Smart technology integration: QR codes and NFC tags are increasingly embedded into packaging, enabling product verification, consumer interaction, and enhanced brand loyalty.

- Material innovation and lightweighting: Adoption of metallized films, composite inserts, and biodegradable materials is reshaping mobile packaging to improve efficiency and environmental performance.

Market Analysis: Material Innovations Driving Mobile Phone Packaging

Recent developments highlight significant material, sustainability, and technology trends shaping the global mobile phone packaging landscape. In August 2025, the rapid substitution of aluminum foil with lightweight metallized films demonstrated cost-effective, durable alternatives for interior trays and inserts, potentially enhancing packaging protection for high-value devices. Simultaneously, a liquid-metal printing process enabling ultra-thin indium tin oxide (ITO) films may influence how devices are secured inside packaging while improving flexibility and transparency.

July 2025 marked a critical consolidation event with WestRock and Smurfit Kappa merging to form Smurfit WestRock, strengthening their capacity to serve global mobile phone packaging demands. Sustainability remains a priority, as recyclable plastics show 34% adoption, and biodegradable materials reach 28%, particularly appealing to environmentally conscious consumers. By June 2025, copper adoption in metallic films surged, driven by high-power battery packs and 5G device requirements, highlighting the intersection of packaging with emerging electronics technology.

Earlier innovations include April 2025 studies emphasizing the rising demand for protective and sustainable packaging that prolongs product shelf life, and February 2025 launches of paper-based stand-up pouches by Mondi and Proquimia, demonstrating the potential of paper alternatives for electronics packaging. In February 2024, companies such as Corplex, Packeta, and Slovak Telekom successfully implemented reusable e-commerce boxes featuring QR-based product tracking, proving the feasibility of circular economy packaging solutions.

Trends and Opportunities Transforming the Mobile Phone Packaging Market

Elimination of Plastic and Shift to Fiber-Based Monomaterial Structures

The mobile phone packaging market is undergoing a decisive shift away from plastic laminates and inserts toward 100% fiber-based monomaterial systems, driven by Extended Producer Responsibility (EPR) regulations, corporate sustainability goals, and circular economy principles. Major OEMs are leading this transition. Google announced in August 2024 that all Pixel hardware packaging is now 100% plastic-free, using stretchable paper and molded pulp from recycled newspapers. Apple has also accelerated its transformation, with the iPhone 15 Pro series reaching 99% fiber-based packaging, ahead of its 2025 target. Samsung has followed suit, cutting plastic in its Galaxy smartphone packaging from 51% in 2017 to just 4% in 2024, and committing to complete elimination by 2025.

The EU Packaging and Packaging Waste Regulation (PPWR), approved in late 2024, has intensified this momentum by enforcing mandatory recyclability and recycled content targets. These regulations are compelling brands to adopt simplified monomaterial packaging to ensure clean recovery streams. The combination of regulatory pressure, corporate commitments, and consumer demand for sustainable packaging positions fiber-based designs as the dominant trend in the next phase of the mobile phone packaging industry.

Supply Chain-Led Packaging Miniaturization and Logistics Optimization

Another powerful trend shaping the mobile phone packaging market is packaging miniaturization, which directly contributes to lower Scope 3 emissions, optimized logistics, and reduced material usage. OEMs are redesigning boxes to be smaller and lighter, while maintaining protective performance. Apple’s redesign of the iPhone 16 Pro and Pro Max packaging resulted in a 6% reduction in box volume, translating into a 3% drop in transportation-related carbon emissions by allowing more units per pallet.

This shift is not new—Apple’s packaging strategy as far back as the iPhone 7 reduced plastic by 84% compared to the iPhone 6s, using compact fiber-based trays. Google’s sustainability reports similarly highlight packaging optimization as a critical tool to lower its device supply chain footprint, even when overall product emissions fluctuate. By combining smaller box sizes, reduced weight, and fiber-based inserts, manufacturers achieve both economic efficiency and sustainability alignment, making miniaturization a long-term packaging trend across the mobile phone industry.

Integration of Digital Watermarking for Enhanced Recycling and Consumer Engagement

The integration of digital watermarking technologies—pioneered through the HolyGrail 2.0 initiative—presents a transformative opportunity for mobile phone packaging. These nearly invisible codes, printed directly on fiber-based mobile phone boxes, can be detected by high-resolution scanners in recycling facilities, enabling high-purity paper stream sorting and significantly improving recyclability outcomes.

Beyond recycling, digital watermarks open new avenues for interactive consumer engagement. By scanning the code with a smartphone, users can access digital manuals, sustainability credentials, warranty information, or exclusive multimedia content. Brands can leverage this to enhance the unboxing experience, personalize communication, and strengthen customer loyalty. This dual function—closing recycling loops and building digital engagement platforms—positions digital watermarking as one of the most impactful near-term opportunities in mobile phone packaging.

Development of Protective Bio-Based and Molded Fiber Cushioning

The global phase-out of plastic foams (EPS inserts) has created a critical opening for bio-based cushioning solutions that combine product protection with compostability. Companies are investing in molded pulp made from sugarcane bagasse, bamboo, and recycled newspaper, as well as mycelium-based composites, to provide sustainable alternatives to plastic trays and holders. Samsung has already replaced many plastic accessory trays with recycled pulp molds, ensuring comparable strength with reduced environmental impact.

Bio-based cushioning not only aligns with corporate zero-plastic goals but also diverts agricultural waste streams from landfills, creating renewable raw materials for packaging. Research on agricultural waste utilization demonstrates the dual benefit of reducing reliance on virgin resources while providing consumers with home-compostable inserts. As circular economy frameworks expand, protective bio-based cushioning will play a pivotal role in ensuring mobile phone packaging achieves both sustainability and product protection targets.

Competitive Landscape of Global Mobile Phone Packaging: Leading Innovators

The mobile phone packaging industry is increasingly shaped by sustainability-driven innovation, e-commerce resilience, and premium design capabilities. Market leaders differentiate through advanced materials, smart packaging technologies, and strategic mergers.

Amcor plc: Championing Recyclable and High-Performance Packaging

Amcor is a global leader in flexible and rigid packaging, providing folding cartons, rigid boxes, and flexible films for mobile phones and accessories. In July 2025, Amcor upgraded its Heanor, UK recycling facility to strengthen high-performance recycling capabilities in Europe. The company focuses on sustainability, lightweighting, and material innovation, aiming for all packaging to be recyclable or reusable by 2025. Its products are used in primary mobile phone packaging and protective accessory packaging, balancing durability with premium presentation.

Sonoco Products Company: Sustainable Paperboard and Molded Fiber Expertise

Sonoco specializes in paperboard and molded fiber packaging critical for mobile phone boxes and custom-fit inserts. In November 2024, the acquisition of Eviosys enhanced its global footprint and capabilities in innovative packaging solutions. Sonoco focuses on lightweight, recyclable materials and serves as a key supplier for brands requiring durable, environmentally responsible packaging for smartphones and accessories.

Smurfit WestRock: Merging Scale with Eco-Friendly Paper-Based Packaging

Following the July 2025 merger of WestRock and Smurfit Kappa, Smurfit WestRock offers an extensive portfolio of folding cartons and corrugated containers for mobile phones. The merger enhances global supply capabilities, while its strategy emphasizes recycled and renewable materials to reduce environmental footprint. The company provides premium-quality packaging for retail display and secure e-commerce delivery.

Mondi Group: Advancing Fiber-Based Packaging Solutions

Mondi delivers innovative paper and flexible packaging solutions for mobile phones, combining sustainability with aesthetic appeal. In May 2025, the company commissioned a €400 million paper machine at its Štětí mill, expanding production of high-quality, recyclable materials. Mondi’s offerings include fiber-based pouches and functional barrier papers, supporting both premium unboxing experiences and environmental goals.

Pragati Pack (India) Pvt. Ltd.: Customized Premium Packaging Solutions

Pragati Pack specializes in high-end, consumer-facing packaging, including rigid boxes and folding cartons for mobile phones and tablets. Its core strength is in producing highly customized packaging that enhances brand image and the unboxing experience, leveraging advanced printing and finishing technologies. Pragati Pack emphasizes sustainability, quality, and innovation, making it a preferred partner for global electronics brands seeking differentiated packaging solutions.

Mobile Phone Packaging Market Share Insights

Folding Cartons Retain the Largest Market Share by Packaging Type in the Mobile Phone Packaging Industry

Folding cartons dominate the mobile phone packaging market with 45% share in 2025, owing to their unmatched balance of cost-efficiency, sustainability, and brand presentation. They are the go-to solution for mid-range and budget smartphones, as well as accessories, because they ship flat, reduce logistics costs, and support high-speed automated filling. Their printability enables vibrant branding, regulatory labeling, and anti-counterfeiting features, which are critical in a fiercely competitive smartphone market. While rigid boxes remain indispensable for premium flagships and flexible films are rapidly expanding in accessory packaging, folding cartons maintain leadership by addressing the industry’s need for high-volume, eco-friendly, and versatile packaging. Insert trays and thermoformed blisters serve more specialized roles, but their shares remain secondary compared to cartons, which have become the backbone of smartphone packaging strategies worldwide.

Smartphones Drive the Largest Market Share by Application in the Mobile Phone Packaging Industry

Smartphones account for 65% of the application share in 2025, making them the single largest consumer of packaging in this industry. This dominance is driven by the enormous global shipment volumes of smartphones, which demand both premium packaging for flagships and cost-effective folding cartons for mass-market models. Packaging here is not merely protective but a core part of brand strategy, with unboxing experiences shaping consumer perception and loyalty. Accessories, while commanding a strong 25% share, rely more on flexible, lightweight formats, particularly as e-commerce accelerates. Refurbished phones are a fast-growing application, leaning heavily on sustainable, no-frills recycled cartons to align with the circular economy. Feature phones continue to shrink into a niche, relying on the lowest-cost blisters. Collectively, smartphones remain the centerpiece of packaging innovation, sustainability adaptation, and supply chain efficiency in this market.

United States: EPR Laws and Smart Packaging Technologies Reshape Consumer Experiences

The United States mobile phone packaging market is rapidly adapting to Extended Producer Responsibility (EPR) laws, with California’s SB 54 standing out as a landmark regulation. By requiring producers to fund end-of-life packaging management, this regulation is accelerating the transition toward recyclable, plastic-free, and sustainable phone boxes. Leading companies are also exploring smart packaging technologies that integrate NFC tags and QR codes to provide augmented reality experiences, product authentication, and real-time supply chain traceability. A notable example is Google’s Pixel 8 series, launched in late 2024 with 100% plastic-free packaging, reflecting a broader industry trend toward sustainability. With premium and mid-tier smartphones both demanding unique unboxing experiences, features such as magnetic closures, embossed logos, and sustainable rigid boxes are becoming mainstream. The U.S. market is also witnessing investments in localized production facilities to reduce exposure to global trade disruptions while capitalizing on high consumer expectations for innovative and eco-friendly mobile phone packaging.

Germany: EU Packaging Regulations and Circular Economy Leadership Drive Innovation

Germany is at the forefront of the European Union’s Packaging and Packaging Waste Regulation (PPWR), which came into effect in January 2025. This framework prioritizes recyclability and recycled content, putting pressure on packaging manufacturers to replace plastics with fiber-based alternatives and recycled paperboard. German companies, recognized globally for their strength in material science, are investing in high-performance, lightweight packaging solutions that balance durability with sustainability. With one of the world’s most advanced recycling infrastructures, Germany also leads the adoption of mono-material and circular packaging designs for smartphones. Corporate investments in R&D are creating next-generation packaging with advanced adhesive formulations and protective designs, ensuring compliance with EU mandates while serving the premium smartphone packaging market. This makes Germany a role model for the integration of circular economy principles in mobile phone packaging.

China: Domestic Innovation and Automation Fuel High-Volume Smartphone Packaging

China’s mobile phone packaging market is benefiting from strong government support for high-end manufacturing. Fast-tracked approval processes and new standards for packaging technologies are fostering rapid innovation. Domestic producers are leading in automation and digital printing, enabling cost-efficient, on-demand, and highly customized mobile phone packaging that caters to the branding needs of both global giants and local smartphone companies. Multinational brands are also expanding production facilities in China to shorten supply chains, boosting demand for local packaging suppliers. With China’s rapidly growing consumer electronics industry, the demand for premium packaging that combines aesthetics, durability, and sustainability is surging. The increasing use of digital printing and smart customization is ensuring that Chinese mobile phone packaging can deliver both functionality and visual appeal, particularly in the competitive premium smartphone market.

India: Make in India and PLI Scheme Boost Domestic Mobile Phone Packaging Manufacturing

India is emerging as a major hub for mobile phone packaging production, strongly driven by the government’s Make in India initiative and the Production Linked Incentive (PLI) scheme. In 2024, India inaugurated its first tempered glass manufacturing facility for mobile devices, expanding the local ecosystem of phone packaging and components. The Central Pollution Control Board’s (CPCB) EPR regulations on plastic packaging are also reshaping the industry by encouraging manufacturers to invest in sustainable alternatives and register compliance for imports. The Indian market is experiencing rapid adoption of advanced packaging solutions to meet the demands of its booming e-commerce and smartphone industries, with a focus on lightweight, durable, and visually appealing designs. Major investments, such as Samsung’s world’s largest mobile phone factory in India, reinforce the country’s role in both domestic and export-oriented smartphone packaging. As branding becomes critical for online sales, demand is accelerating for cost-effective yet high-quality unboxing experiences across the Indian mobile phone packaging sector.

United Kingdom: Premium Smartphone Packaging Strengthened by Sustainability Initiatives

The United Kingdom mobile phone packaging market is strongly influenced by the Smart Sustainable Plastic Packaging (SSPP) challenge, which funds over 70 innovation projects to drive the development of eco-friendly alternatives to single-use plastics. The UK is aligning with the EU’s plastic waste reduction goals while promoting biodegradable films and bio-based materials. Local companies are focusing on advanced extrusion technologies and innovative film solutions to improve packaging sustainability. Recent corporate moves, such as Berry Global’s 2025 launch of bio-based polyethylene packaging, reflect the broader commitment to the circular economy. The UK market is particularly strong in the premium mobile phone and accessories segment, where unboxing experience is seen as part of brand identity. Brands are increasingly investing in luxury rigid boxes, high-quality finishing, and custom branding elements to appeal to premium consumers while maintaining eco-friendly practices.

Japan: Precision Manufacturing and Premium Graphics Strengthen Mobile Phone Packaging

Japan’s mobile phone packaging industry is driven by its precision manufacturing expertise, with companies such as Toppan and Dai Nippon Printing setting high standards in sustainable and high-performance packaging solutions. Regulatory oversight from the Pharmaceuticals and Medical Devices Agency (PMDA) enforces strict safety and quality measures, indirectly influencing the wider packaging supply chain. Japanese packaging firms are focusing on thin-walled, high-finish packaging designs that meet the growing demand for premium unboxing experiences across smartphones, cosmetics, and electronics. Innovations include advanced paper-based alternatives and multifunctional packaging with enhanced optical properties, durability, and aesthetic appeal. With a national focus on reducing plastics and ensuring sustainable design, Japan is becoming a leader in premium, eco-friendly mobile phone packaging that balances elegance, functionality, and sustainability.

Mobile Phone Packaging Market Report Scope

Mobile Phone Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.6 Billion

|

|

Market Size (2034)

|

$9.3 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Packaging Type (Rigid Boxes, Folding Cartons, Flexible Films, Insert Trays, Thermoformed Blisters), By Material (Paper & Paperboard, Plastic, Molded Fiber, Others), By Application (Smartphones, Feature Phones, Refurbished Phones, Accessories), By End-User (Mobile Phone Manufacturers, Accessory Manufacturers, E-commerce Platforms, Retailers)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, WestRock Company, Berry Global Inc., Amcor Plc, Smurfit Kappa Group, Mondi Group, DS Smith, Sealed Air Corporation, Sonoco Products Company, Pragati Pack (India) Pvt. Ltd., Graphic Packaging Holding Company, Huhtamaki Oyj, AR Packaging Group AB, Crown Holdings, Inc., Avery Dennison Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Mobile Phone Packaging Market Segmentation

By Packaging Type

- Rigid Boxes

- Folding Cartons

- Flexible Films

- Insert Trays

- Thermoformed Blisters

By Material

- Paper & Paperboard

- Plastic

- Molded Fiber

- Others

By Application

- Smartphones

- Feature Phones

- Refurbished Phones

- Accessories

By End-User

- Mobile Phone Manufacturers

- Accessory Manufacturers

- E-commerce Platforms

- Retailers

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Mobile Phone Packaging Market

- International Paper Company

- WestRock Company

- Berry Global Inc.

- Amcor Plc

- Smurfit Kappa Group

- Mondi Group

- DS Smith

- Sealed Air Corporation

- Sonoco Products Company

- Pragati Pack (India) Pvt. Ltd.

- Graphic Packaging Holding Company

- Huhtamaki Oyj

- AR Packaging Group AB

- Crown Holdings, Inc.

- Avery Dennison Corporation

* List Not Exhaustive

Methodology

USDAnalytics employs a robust and systematic methodology to deliver accurate insights into the global Mobile Phone Packaging Market. Our approach integrates primary research, including interviews with packaging engineers, supply chain specialists, mobile device OEMs, and sustainability consultants, alongside secondary research sourced from corporate reports, regulatory filings, patent databases, scientific publications, and trade journals. We analyze key market drivers such as the shift to fiber-based monomaterial packaging, eco-friendly cushioning materials, e-commerce protective solutions, and smart technology integration like NFC and QR codes. Quantitative analysis incorporates historical data, market sizing, CAGR forecasts, and regional adoption trends across North America, Europe, and Asia-Pacific. Competitive intelligence evaluates innovations, mergers, and sustainability initiatives by leading players such as Amcor, Smurfit WestRock, Mondi, Sonoco, and Pragati Pack, highlighting premium unboxing experiences, digital engagement, and material optimization. This methodology ensures that USDAnalytics provides industry professionals with actionable, data-driven insights to support strategic planning, sustainability adoption, and supply chain optimization in the evolving mobile phone packaging sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.