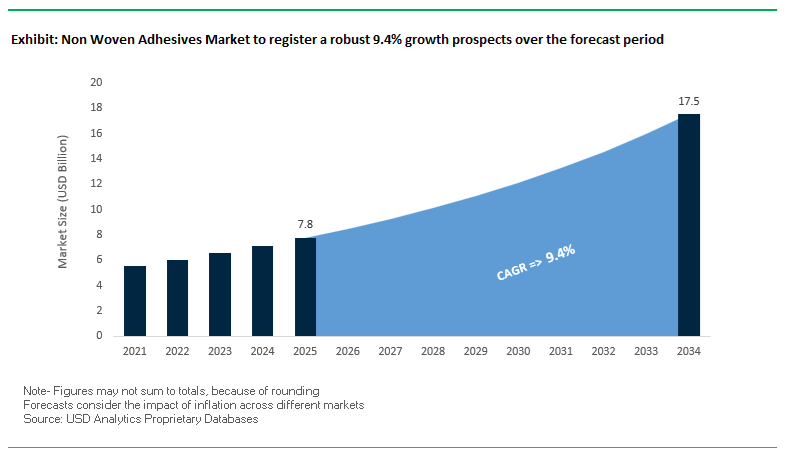

The Global Nonwoven Adhesives Market is projected to expand from USD 7.8 billion in 2025 to USD 17.5 billion by 2034, advancing at a CAGR of 9.4%, as hygiene and medical product manufacturers continue to scale high-speed production while tightening requirements around softness, durability, and environmental impact. Market momentum is closely linked to the sustained growth of baby diapers, adult incontinence, and feminine hygiene products, where adhesive performance directly influences line speed, product integrity, and consumer perception. In this context, nonwoven adhesives are treated as process-critical materials that determine manufacturing efficiency and brand-level quality outcomes.

Across hygiene and medical nonwovens, adhesives are increasingly engineered to balance fiber integrity, wet tensile strength, and low odor, particularly in environments where converting lines operate at speeds exceeding 800 units per minute. At these throughputs, even marginal variability in adhesive rheology or thermal stability can translate into downtime or reject rates. As a result, metallocene polyolefin (mPO) hot melt adhesives are becoming the preferred technology platform, offering tighter molecular weight distribution, improved thermal stability, and lower coating weights. More than 70% of global high-speed diaper lines have already transitioned to mPO-based systems, reflecting a structural shift away from conventional EVA formulations in premium hygiene applications.

Sustainability considerations are increasingly shaping formulation roadmaps. Leading adhesive producers are integrating renewable feedstocks, with many targeting a minimum of 25% bio-based content in future nonwoven adhesive portfolios to align with brand owner commitments for 2030. This transition is occurring alongside continued demands for softness and skin comfort, particularly in adult incontinence and feminine hygiene products, where prolonged skin contact heightens sensitivity to odor and residue. In medical nonwovens, demand is accelerating for breathable, skin-friendly, and residue-free adhesives, supporting applications such as surgical drapes, wound care materials, and disposable medical textiles; this segment is expanding at approximately 15% annually, outpacing traditional hygiene growth.

Operational performance benchmarks are tightening in parallel. Premium nonwoven adhesives are now expected to retain at least 85% wet tensile strength after saturation, ensuring product durability under real-use conditions. From a manufacturing standpoint, adhesives delivering ≥95% fiber tear at line speeds above 800 units per minute are increasingly viewed as baseline requirements rather than differentiators, as converters prioritize uptime optimization and consistent bonding quality.

The nonwoven adhesives industry is undergoing a phase of significant transformation driven by sustainability initiatives, advanced polymer chemistry innovations, and capacity expansions across major markets.

In October 2025, Henkel Adhesive Technologies strengthened its global sustainability agenda by expanding its partnership with Dow Chemical Company to introduce low-carbon feedstocks into hot melt adhesive manufacturing. This initiative targets a 20–40% reduction in Product Carbon Footprint (PCF) across select adhesive product lines, marking a critical step toward the decarbonization of adhesive production. In the same month, Henkel also expanded its portfolio of Environmental Product Declarations (EPDs), providing greater transparency to construction and industrial customers on the environmental lifecycle impact of its adhesive solutions.

In May 2025, Bostik (Arkema Group) launched a new series of bio-based nonwoven adhesives tailored for the hygiene industry, reinforcing its leadership in sustainable product innovation. These formulations are engineered to deliver softness, elasticity, and secure bonding without compromising environmental performance—key differentiators in high-end diaper and incontinence products. Around the same time, a leading specialty chemical company unveiled an $18 million investment to upgrade its European production plant, implementing water-based dispersion technologies for high-performance nonwoven lamination adhesives, targeting filtration and industrial applications.

Earlier, in February 2025, Dow Chemical Company and Sika AG announced a strategic partnership to co-develop nonwoven adhesives for construction applications, emphasizing energy-efficient, eco-friendly building materials. Meanwhile, H.B. Fuller Company, in January 2024, expanded its nonwoven adhesive capacity in Asia, aiming to meet the rising demand for hygiene products in rapidly urbanizing economies. The same month, 3M introduced its QX-200 hot-melt adhesive, designed specifically for medical nonwovens, offering superior skin-friendliness and controlled adhesion for surgical tapes and drapes.

In the patent and regulatory landscape, ExxonMobil Chemical received a patent in November 2024 for a new polyolefin adhesive composition optimized for improved elasticity and thin-core bonding in modern disposable products. Additionally, the European Union’s August 2024 voluntary guidelines for disposable product manufacturers promote the use of biodegradable and compostable adhesives, accelerating industry adoption of eco-compliant nonwoven bonding solutions.

Market Trend 1: Shift Toward Bio-Based and Renewable Hot Melt Adhesives in Hygiene Applications

The most transformative trend in the non-woven adhesives market is the rapid adoption of bio-based and renewable hot melt adhesives (HMAs) designed for diapers, femcare, and hygiene product assembly. The shift is driven by both regulatory frameworks focused on carbon neutrality and brand-owner sustainability mandates requiring lower environmental impact across the supply chain.

Leading global manufacturers are actively reformulating adhesive chemistries to integrate renewable feedstocks while maintaining processability, cohesive strength, and thermal stability. One major chemical company, for instance, introduced a bio-based HMA portfolio that enables hygiene manufacturers to reduce cradle-to-gate carbon emissions by up to 50%, verified through comprehensive Life Cycle Assessment (LCA) analysis. These products achieve performance parity with conventional petroleum-based adhesives while supporting circular economy objectives in disposable hygiene manufacturing.

Simultaneously, innovations are being validated by certification bodies. A specialty adhesive producer received DIN CERTCO certification for its bio-based non-woven adhesive range, featuring 50%–85% renewable carbon content. The certification enhances product transparency and assures compliance with green procurement policies adopted by major hygiene brands worldwide.

The market outlook for green HMAs in hygiene is robust—analysts project double-digit annual growth in the coming decade as bio-based raw material supply chains mature and cost differentials narrow. By combining sustainability performance with regulatory compliance (such as EU Green Deal targets and China’s environmental labeling standards), bio-based non-woven adhesives are quickly emerging as a core pillar of the sustainable hygiene materials ecosystem.

Market Trend 2: Rise of Ultra-Low VOC and Odorless Formulations for Premium Hygiene Products

Growing consumer sensitivity to product safety and comfort—especially in baby diapers, feminine hygiene, and adult incontinence products—is accelerating the development of ultra-low VOC and odorless adhesives. These formulations are designed to eliminate residual volatiles and chemical odors while ensuring long-term adhesion and flexibility.

Traditional adhesive formulations relied on rosin esters and volatile tackifiers, which are being phased out in favor of advanced styrenic block copolymers (SBCs) and metallocene polyolefins. These polymers enable high thermal stability, enhanced cohesive strength, and virtually odor-free performance, aligning with consumer preferences for skin-safe and hypoallergenic products.

Regulatory action reinforces the shift. China, one of the largest global producers of hygiene goods, has implemented stringent indoor air quality and VOC content regulations for adhesives used in hygiene product assembly, compelling manufacturers to adopt cleaner, low-emission production processes. The has created a direct incentive for multinational adhesive suppliers to reformulate product lines around low-odor, solvent-free, and isocyanate-free technologies.

The result is a new class of premium non-woven adhesives engineered for superior user comfort and compliance with global air-quality standards. As consumers increasingly associate low odor with product purity and safety, these high-purity adhesives are redefining brand differentiation in hygiene product innovation.

Market Opportunity 1: Reusable and Wash-Resistant Hygiene Product Assembly

The global shift toward sustainable and reusable hygiene solutions—including washable diapers, reusable feminine care pads, and protective apparel—creates a fast-growing niche for durable, wash-resistant adhesives capable of surviving repeated laundering and sterilization.

Technical textile studies show that washable laminates used in hospital gowns and reusable hygiene products must withstand up to 100 wash and sterilization cycles without delamination or adhesive degradation. To meet the challenge, manufacturers are adapting Hot Melt Moisture Cure (HMMC) systems originally developed for outdoor performance textiles and protective workwear, offering high water resistance, flexibility, and mechanical stability at minimal coating weights.

The evolution represents a fundamental redefinition of performance expectations for non-woven adhesives. The adhesive must not only deliver initial bond strength but also maintain long-term adhesion reliability that outlasts the textile’s service life. These requirements elevate reusable non-woven assemblies to a premium product category, where the adhesive serves as a key value driver in determining both durability and cost efficiency.

As sustainability-driven business models gain momentum in the hygiene sector, long-life bonding adhesives will become essential for achieving economical cost-per-use ratios. The transition marks one of the most compelling growth avenues for non-woven adhesive suppliers, enabling them to serve a new generation of high-value, environmentally responsible hygiene products.

Market Opportunity 2: Advanced Medical Non-Wovens for Wound Care and Single-Use Devices

The expansion of medical-grade non-wovens—particularly for advanced wound care dressings, surgical fabrics, and single-use medical devices—is creating a high-value market for adhesives with precise functional control, biocompatibility, and active material compatibility.

Adhesives in the sector must achieve a balanced Moisture Vapor Transmission Rate (MVTR) between 800–1000 g/m²/24h, allowing the wound to remain moist for healing while preventing maceration. The development of breathable yet water-resistant adhesive layers is therefore critical for next-generation wound dressing technologies, where controlled vapor permeability ensures optimal patient recovery outcomes.

In addition, the integration of Active Pharmaceutical Ingredients (APIs) into drug-eluting non-woven dressings has introduced a new chemical compatibility requirement. Adhesives must remain chemically inert, avoiding migration or reactivity that could alter drug efficacy. Leading manufacturers of medical-grade silicone and acrylic adhesives are expanding into the domain, offering API-compatible solutions designed for transdermal patches and skin-contact devices.

Additionally, ISO 10993 biocompatibility compliance is becoming a prerequisite for all medical non-woven adhesives. These standards ensure safety and stability for patient-worn devices like sensors, catheters, and surgical drapes, where secure adhesion and hypoallergenic performance are essential.

Non Woven Adhesives Market Share Insights, 2025-2034

Market Share by Technology

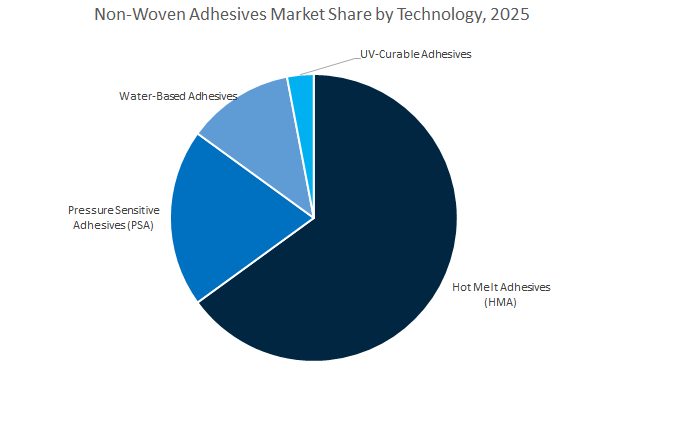

The hot melt adhesive (HMA) segment dominates the global non-woven adhesives market, accounting for a projected 63.5% share in 2025, owing to its fast setting time, superior bonding strength, and seamless integration into high-speed manufacturing lines. HMAs are the adhesive backbone of the hygiene and personal care industry, particularly in baby diapers, adult incontinence, and feminine hygiene products, where thermal stability, flexibility, and non-toxicity are critical. Their solvent-free and low-VOC nature aligns with stringent environmental regulations, making them the most sustainable and process-efficient choice. Furthermore, the continuous innovation in reactive polyolefin and metallocene-based HMA formulations is enhancing product performance, allowing better adhesion to low-surface-energy substrates like polyethylene and polypropylene. The expansion of automated assembly systems across hygiene and medical manufacturing further strengthens the dominance of hot melt technologies.

Pressure-sensitive adhesives (PSAs) maintain a significant share, catering to applications that require gentle yet durable adhesion—particularly in medical tapes, hygiene fastening systems, and protective dressings. Their repositionable and skin-friendly characteristics have driven strong adoption in healthcare and wearable device applications. Meanwhile, water-based adhesives are preferred in specific segments demanding softness, breathability, and low odor, such as premium diapers and sanitary pads, though they face competition from HMAs due to slower drying times and limited temperature resistance. UV-curable adhesives, while representing a smaller portion of the market, are expanding rapidly in technical non-wovens and filtration applications, where instant curing, high precision, and strong bond strength are required.

Market Share by Application

The baby diaper segment leads the global non-woven adhesives market, projected to hold a 38.2% share in 2025, reflecting the immense volume demand and innovation intensity in the hygiene sector. The surge in infant population across emerging economies, coupled with rising disposable incomes and improved hygiene awareness, continues to drive diaper production globally. Non-woven adhesives play a critical role in core construction, elastic attachment, and positioning systems, offering softness, flexibility, and secure bonding under high-speed production conditions. Manufacturers are increasingly using hot melt and PSA formulations to improve comfort, absorbency, and product durability, ensuring optimal performance even under moisture and stress conditions. The growing shift toward eco-friendly and bio-based hygiene products is also shaping adhesive selection, pushing demand for low-VOC and recyclable non-woven bonding systems.

The feminine hygiene and adult incontinence segments represent major growth drivers, supported by aging populations, gender health awareness, and increased consumer spending on premium personal care products. Adhesives used in these applications must maintain skin compatibility, odor control, and consistent adhesion even in humid conditions, driving R&D toward hypoallergenic and breathable adhesive technologies. The medical and healthcare sector also holds a crucial role, utilizing non-woven adhesives in surgical drapes, wound dressings, and medical textiles, where biocompatibility and sterilization resistance are essential. Beyond hygiene, filtration and automotive applications are gaining prominence as non-woven adhesives provide thermal stability, vibration resistance, and air permeability for air filters, cabin filters, and insulation systems.

The nonwoven adhesives market is moderately consolidated, with Henkel AG & Co. KGaA, H.B. Fuller, Bostik (Arkema Group), 3M Company, and Savare Specialty Adhesives among the top players. These companies are actively expanding production capacity, enhancing sustainable formulations, and integrating R&D with end-user innovation centers to maintain a competitive edge in a rapidly evolving market.

Henkel remains the global market leader in nonwoven adhesive innovation through its Adhesive Technologies business unit, which reported €10.4 billion in H1 2025 sales. The company’s commitment to environmental transparency and low-carbon manufacturing continues to set industry benchmarks. In October 2025, Henkel expanded its strategic alliance with Dow Chemical to incorporate low-carbon feedstocks into its hot melt adhesive production, achieving up to 40% lower emissions. Its metallocene polyolefin (mPO) hot melts are widely used in high-speed hygiene applications, offering exceptional cohesion, low odor, and long-term thermal stability.

H.B. Fuller announced a major production capacity expansion in Asia-Pacific in January 2024, positioning itself to capitalize on soaring regional demand for disposable hygiene and healthcare products. Its innovation model is centered on customer collaboration, integrating product development with client engineering teams through global Technology Centers of Excellence. Fuller’s nonwoven adhesive portfolio spans hot melts and water-based systems, providing superior fiber adhesion, elasticity, and line-speed performance. The company continues to invest in smart manufacturing processes that enhance efficiency and reliability in high-speed hygiene production.

Bostik, a division of Arkema Group, is at the forefront of bio-based nonwoven adhesive development, launching a new eco-friendly product line in May 2025 targeting the hygiene sector. These adhesives combine renewable feedstocks with soft-feel and high-elasticity properties, ideal for premium diaper and incontinence products. Leveraging Arkema’s expertise in specialty materials, Bostik develops high-performance formulations with optimized polymer chemistry that enhance comfort, bonding strength, and process flexibility. Its commitment to sustainability continues to shape the next wave of circular, high-comfort hygiene solutions globally.

3M’s expertise in Pressure-Sensitive Adhesives (PSAs) and medical-grade hot melts drives its leadership in nonwoven applications for healthcare and hygiene. The launch of 3M QX-200 in December 2023 underscores its focus on skin-compatible and low-trauma bonding solutions for medical drapes, surgical tapes, and wearables. 3M’s R&D strategy centers on high-shear and high-peel adhesives that ensure secure adhesion even under stress. With its robust low-VOC portfolio, 3M addresses stringent global standards for indoor air quality and manufacturing safety while delivering reliable bonding performance for critical healthcare products.

Savare Specialty Adhesives has carved a strong niche in the global hygiene adhesives market, specializing in tailored polymer systems for baby care, feminine hygiene, and adult incontinence applications. Its product portfolio includes both Styrenic Block Copolymer (SBC) and polyolefin-based hot melts, providing manufacturers with flexibility in optimizing for elasticity, softness, or cost efficiency. Savare’s close collaboration with machinery manufacturers ensures perfect integration between adhesive behavior and high-speed application performance, achieving 95% fiber tear consistency. The company’s technical service centers across Europe and Asia deliver responsive, localized support, reinforcing its position as a customer-focused adhesive partner.

Country Analysis: Global Non-Woven Adhesives Industry

United States: Innovation in Sustainable and Medical-Grade Non-Woven Adhesives

The United States remains a dominant force in the global non-woven adhesives market, supported by strong R&D infrastructure, advanced healthcare applications, and expanding automation in packaging and hygiene manufacturing. In early 2024, H.B. Fuller Company expanded its domestic capacity to strengthen the supply of high-performance hot melt non-woven adhesives, particularly for medical devices and hygiene applications such as baby diapers, adult incontinence, and surgical drapes. The expansion aligns with the U.S. government’s push to reinforce domestic healthcare supply chain resilience post-pandemic, boosting the production of hospital-grade non-woven materials and PPE.

At the forefront of innovation, 3M’s Specialty Adhesives and Tapes Division is developing next-generation skin-contact pressure-sensitive adhesives (PSAs) designed for advanced wound care and wearable medical sensors. The formulations emphasize biocompatibility and gentle removal without compromising adhesion strength. Simultaneously, major producers are investing heavily in compostable and bio-based elastic adhesives to meet rising sustainability demands from major brands and consumers in the hygiene sector. Beyond healthcare, the booming e-commerce packaging sector is also a key growth driver, where polyolefin (PO) hot melts are increasingly used for automated, right-sized packaging systems—underscoring the versatility of non-woven adhesive applications across industries.

China: Expanding Production and Premiumization in the Non-Woven Adhesives Sector

China has firmly positioned itself as the Asia-Pacific powerhouse in the non-woven adhesives industry, leveraging its vast manufacturing base, cost-efficient raw material supply, and government-backed innovation programs. The country’s production of Styrenic Block Copolymers (SBC) and Amorphous Poly Alpha Olefin (APAO) polymers has surged since 2023, enabling large-scale production of disposable hygiene and medical non-woven products for both domestic and export markets. Local manufacturers are increasingly shifting toward metallocene polyolefin (mPO)-based adhesives, which allow thinner, softer, and more elastic non-woven structures—ideal for premium baby and adult hygiene products.

Environmental policies from the Ministry of Ecology and Environment are accelerating the transition to solvent-free and low-VOC adhesives, prompting smaller players to upgrade production technology or consolidate. Global leaders such as Bostik (Arkema) and Henkel are entering strategic joint ventures with domestic non-woven fabric producers, co-developing customized formulations for high-speed application in local diaper and hygiene factories. The blend of localization, technological integration, and regulatory compliance is transforming China into a global benchmark for sustainable and performance-oriented non-woven adhesive manufacturing.

Germany: European Leader in Low-Monomer PUR and Bio-Based Non-Woven Adhesives

Germany stands as the technology epicenter of Europe’s non-woven adhesives market, championing sustainability, safety, and digital manufacturing integration. Jowat SE, a leading German adhesive manufacturer, introduced a new generation of reactive PUR hot melt adhesives with ultra-low monomer content in late 2023, anticipating stricter EU worker safety standards under the updated REACH framework. Concurrently, Henkel AG & Co. KGaA is expanding its bio-based adhesive portfolio for the hygiene industry, aligning with the EU Circular Economy Action Plan and sustainability-driven procurement trends among European hygiene brands.

German manufacturers are integrating Industry 4.0 technologies—including digital dispensing systems and real-time quality monitoring—to optimize adhesive application precision in high-speed production lines for non-woven hygiene and filtration materials. Moreover, compliance with the EU Policy Framework on Biobased and Compostable Plastics is pushing adhesive producers to certify their products for industrial compostability. Germany’s advanced R&D ecosystem and regulatory foresight continue to drive its leadership in eco-efficient, low-VOC, and high-performance non-woven adhesives across Europe.

India: Fastest-Growing Market for Hygiene and Infrastructure-Based Non-Woven Adhesives

India is emerging as one of the fastest-growing markets in the global non-woven adhesives industry, propelled by strong policy support, rising consumer hygiene awareness, and a surge in foreign investment. Under the “Make in India” initiative, significant foreign direct investment (FDI) has been channeled into localized manufacturing of hot melt adhesives and non-woven fabrics, reducing dependence on imports. The investment momentum is complemented by large-scale government hygiene campaigns, such as the National Sanitary Protection and Swachh Bharat initiatives, which are boosting demand for cost-effective high-tack positioning adhesives used in feminine hygiene and baby diaper products.

Rising disposable income and urbanization are driving a shift toward premium branded hygiene products, increasing demand for adhesives with better bond strength, reduced odor, and superior performance in humid climates. Local and multinational players, including Pidilite and Sika, are expanding technical centers and production lines dedicated to non-woven applications. India’s focus on infrastructure and healthcare manufacturing positions it as a key emerging hub for high-volume, cost-efficient non-woven adhesive production in the Asia-Pacific region.

Japan: Precision Engineering and Advanced Non-Reactive Hot Melt Adhesives

Japan’s non-woven adhesives market is characterized by technological precision, quality control, and innovation in low-add-on formulations. With one of the world’s most rapidly aging populations, Japan’s demand for high-end adult incontinence products continues to rise, driving advancements in ultra-thin, highly elastic polyolefin-based adhesives that prioritize comfort, breathability, and skin safety. The nation’s expertise in precision coating and lamination technology enables the production of multi-layer non-woven composites for medical, filtration, and hygiene applications.

Moresco Corporation is leading R&D efforts in non-reactive hot melt adhesives designed for ultra-thin, lightweight hygiene products, showcasing breakthroughs in thermal stability and odor control. Furthermore, Japan’s electronics and filtration industries rely heavily on low-add-on SMP and PO adhesives for consistent bonding in high-speed assembly lines. The combination of aging demographics, strict quality standards, and world-class manufacturing systems ensures Japan’s continued dominance in the premium segment of the non-woven adhesives industry.

France: Specialty Hybrid Adhesives and Bio-Based Innovation Hub

France remains a key European center for specialty non-woven adhesives, driven by robust R&D, sustainability initiatives, and the influence of major domestic players like Arkema’s Bostik division. Under its “Smart Adhesives” strategy, Bostik continues to develop high-performance, safe non-woven specialty adhesives tailored for medical and hygiene applications, where precision, durability, and regulatory compliance are paramount. The French government’s Bio-Economy and Green Chemistry programs have further catalyzed innovation in bio-sourced tackifiers and polymers, core components in sustainable hot melt non-woven adhesives.

France also plays a strategic role in developing flame-retardant and recyclable formulations that cater to stringent European safety and sustainability standards. Continuous investments in R&D for polymer science and advanced material performance position France as a leader in bio-circular and performance-optimized non-woven adhesives, reinforcing Europe’s transition toward greener material solutions in healthcare, hygiene, and industrial manufacturing.

Non Woven Adhesives Market Report Scope

Non Woven Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.8 Billion

|

|

Market Size (2034)

|

$17.5 Billion

|

|

Market Growth Rate

|

9.4%

|

|

Segments

|

By Technology (Hot Melt Adhesives, Pressure Sensitive Adhesives, Water-Based Adhesives, UV-Curable Adhesives), By Product Type (Construction/Core-Fixation, Positioning/Attachment, Elastic/Strand, Laminating), By Base Polymer (Styrenic Block Copolymers, Amorphous Poly Alpha Olefin, Metallocene Polyolefin, Ethylene Vinyl Acetate, Polyurethane), By Application (Baby Diapers, Adult Incontinence Products, Feminine Hygiene Products, Medical & Healthcare, Filtration, Automotive & Transportation

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Arkema Group (Bostik), 3M Company, Dow Inc., Sika AG, Jowat SE, ExxonMobil Chemical Company, Texyear Industries Inc., Lohmann-Koester GmbH & Co. KG, Moresco Corporation, Eastman Chemical Company, Wacker Chemie AG, Mitsubishi Chemical Group, Avery Dennison Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Technology

- Hot Melt Adhesives

- Pressure Sensitive Adhesives

- Water-Based Adhesives

- UV-Curable Adhesives

By Product Type

- Construction/Core-Fixation

- Positioning/Attachment

- Elastic/Strand

- Laminating

By Base Polymer

- Styrenic Block Copolymers

- Amorphous Poly Alpha Olefin

- Metallocene Polyolefin

- Ethylene Vinyl Acetate

- Polyurethane

By Application

- Baby Diapers

- Adult Incontinence Products

- Feminine Hygiene Products

- Medical & Healthcare

- Filtration

- Automotive & Transportation

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Non Woven Adhesives Market

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Arkema Group (Bostik)

- 3M Company

- Dow Inc.

- Sika AG

- Jowat SE

- ExxonMobil Chemical Company

- Texyear Industries Inc.

- Lohmann-Koester GmbH & Co. KG

- Moresco Corporation

- Eastman Chemical Company

- Wacker Chemie AG

- Mitsubishi Chemical Group

- Avery Dennison Corporation

*- List not Exhaustive

Research Coverage

This report investigates the Non Woven Adhesives Market with a focus on high-speed hygiene converting, mPO-driven efficiency, and bio-based innovation; it delivers analysis reviews of adoption drivers across baby care, femcare, adult incontinence, medical nonwovens, filtration, and automotive interiors, curates breakthroughs in metallocene polyolefin hot melts, ultra-low-odor PSA systems, and wash-durable lamination chemistries, and highlights manufacturing levers such as thermal stability windows, low add-on weights, fiber-tear consistency, and EPD/PCF transparency that enhance uptime and cost-in-use; produced by USDAnalytics, this report is an essential resource for product managers, operations leaders, sourcing teams, and investors seeking defensible forecasts, compliance alignment, and clear routes to sustainability-led differentiation.

Scope Highlights

Segmentation:

- By Technology: Hot Melt Adhesives; Pressure Sensitive Adhesives; Water-Based Adhesives; UV-Curable Adhesives.

- By Product Type: Construction/Core-Fixation; Positioning/Attachment; Elastic/Strand; Laminating.

- By Base Polymer: Styrenic Block Copolymers; Amorphous Poly Alpha Olefin; Metallocene Polyolefin; Ethylene Vinyl Acetate; Polyurethane.

- By Application: Baby Diapers; Adult Incontinence Products; Feminine Hygiene Products; Medical & Healthcare; Filtration; Automotive & Transportation.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies covering strategies, portfolios, sustainability moves, and recent capacity/product actions.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.