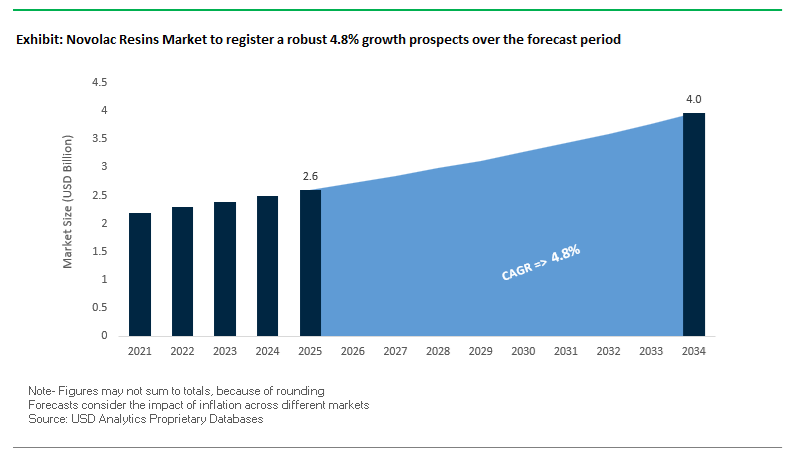

The Global Novolac Resins Market is projected to expand from USD 2.6 billion in 2025 to USD 4 billion by 2034, advancing at a CAGR of 4.8%, as demand consolidates around applications where thermal endurance, dimensional stability, and controlled cross-linking density are non-negotiable. Growth is anchored in automotive, electrical & electronics, and industrial composite systems, where novolac phenolic chemistry continues to outperform conventional phenolics and standard epoxies under sustained thermal and mechanical stress.

Novolac resins—produced via acid-catalyzed polymerization of phenol and formaldehyde—retain a structural advantage in applications that require high heat deflection temperatures, chemical resistance, and predictable curing behavior. These attributes underpin their continued use in friction materials, electrical laminates, encapsulants, coatings, and structural adhesives, where failure modes are often driven by long-term thermal exposure rather than peak loads. In automotive systems, this is reinforcing demand from under-the-hood components and braking materials, particularly as the industry continues its transition toward heat-resistant, copper-free friction formulations.

Electronics and semiconductor manufacturing are increasingly influencing novolac resin specifications. The expansion of electric vehicle power electronics and advanced semiconductor fabrication is driving uptake of high-purity, linear novolac formulations, where impurity control and molecular uniformity directly affect yield and reliability. In lithography, sub-10 nm photoresist processes rely on linear novolac phenolic resins to achieve tight line-edge roughness control and pattern fidelity, while in electronics encapsulation, epoxy novolac systems delivering glass transition temperatures above 200°C are becoming standard for high-power modules exposed to continuous thermal cycling.

The industry is undergoing a critical phase of technological innovation, capacity expansion, and sustainability advancement in the global Novolac Resins industry. Market leaders have prioritized strategic acquisitions, collaborative partnerships, and process digitization to meet rising demand from automotive, semiconductor, and sustainable materials segments.

In June 2025, Sumitomo Bakelite Co., Ltd. achieved a major industry milestone with the commercialization of the world’s first lignin-modified solid Novolac phenolic resin, utilizing non-edible biomass as feedstock. This sustainable breakthrough offers high heat resistance for automotive casting and molding applications, aligning with the broader decarbonization goals across the materials industry. Earlier, in January 2024, the company also expanded its phenolic molding compound capacity in Asia by 28% to meet growing demand from EV and semiconductor manufacturing sectors.

Hexion Inc., one of the global leaders in phenolic chemistry, took a dual approach—combining digital transformation and product innovation. In December 2024, it completed the acquisition of Smartech, an AI-driven process optimization platform, followed by the launch of SmartQuality in May 2025—integrating AI analytics into Novolac-based adhesive and composite production. The same year, Hexion partnered with Kadant Carmanah Design to modernize wood panel manufacturing, reinforcing its position in industrial adhesive systems. Furthermore, Hexion’s July 2024 collaboration with Clariant to co-develop intumescent coatings leveraged Novolac’s intrinsic flame-retardant and charring characteristics, expanding its footprint into fire protection materials.

The electronics and specialty chemicals sector also witnessed major developments. DIC Corporation advanced its bio-phenol derived Novolac resins in December 2023, which quickly achieved 25% higher market adoption for sustainable insulation and coating materials. In October 2024, DIC further enhanced its portfolio by acquiring a German additive formulator, integrating new chemistries into its DICPHEN™ Novolac resin line for coatings, composites, and electrical laminates.

The competitive momentum intensified as Prefere Resins finalized its acquisition of Ingevity’s phenolic resins business in March 2024, strengthening its North American manufacturing and customer network. Meanwhile, Kolon Industries unveiled in January 2025 a new phenolic composite for EV battery housings, leveraging Novolac’s high-heat structural performance to deliver lightweight, flame-resistant vehicle components.

In parallel, SI Group doubled its Nanjing, China production capacity to address surging regional demand for industrial Novolac grades used in rubber tackifiers, friction materials, and coatings. These expansions, combined with digital manufacturing initiatives and bio-based innovation, reflect a dynamic and technology-driven trajectory for the Novolac resins industry—one firmly positioned at the intersection of performance engineering and sustainable chemistry.

Market Trend 1: Development of High-Purity, Low-Ion Novolac Resins for Advanced Electronics Encapsulation

The miniaturization and integration of next-generation semiconductor and microelectronic devices demand encapsulants that meet exceptional purity and thermal reliability standards. Ionic contaminants, particularly chloride ions, can accelerate corrosion and premature circuit failure under bias, heat, and humidity, making low-ion novolac resins indispensable in modern packaging materials.

Advanced manufacturing processes have reduced ionic chloride content in epoxy novolac resins (EPN, ECN) to below 1 part per million (ppm)—a 100× improvement over traditional specifications. The purity benchmark is crucial for ensuring long-term electrical stability in semiconductor encapsulation and molding compounds, directly impacting the reliability of high-density surface-mount (SMT) packages such as QFPs and SOPs used in high-frequency applications like 5G infrastructure and autonomous driving systems.

Studies involving high-humidity bias testing (Bias-PCT) have shown that these ultra-low-ion novolac systems dramatically reduce moisture-induced corrosion and electrical leakage, significantly enhancing mean time to failure (MTTF). To further mitigate stress during curing and post-reflow processes, researchers have developed modified novolac-type epoxy resins through aliphatic alcohol addition reactions, reducing shrinkage and improving thermal-mechanical resilience—key attributes for high-integration chips with increased power density.

In addition, the automotive electronics segment, guided by the AEC-Q100 reliability standard, has become a major growth driver for high-purity novolac systems. Automotive-grade components must withstand operating temperatures exceeding 150°C for up to 15 years, a performance threshold achievable only through high-purity, thermally stable novolac-based epoxy curing systems. The intersection of automotive reliability and semiconductor-grade material performance drives the strategic importance of novolac resin innovation in high-stress electronic environments.

Market Trend 2: Reformulation for Enhanced Thermal and Mechanical Performance in Carbon Composite Friction Materials

The second defining trend in the novolac resins market is the reformulation of phenolic novolac systems for high-performance carbon composite friction materials used in automotive, aerospace, and industrial braking systems. As braking technologies evolve to support higher loads, temperatures, and environmental durability, the demand for heat-resistant, high-char-yield novolac binders is accelerating.

Laboratory data confirms that boron-modified novolac phenolic resins (B-novolacs) enhance char yield at 800°C by up to 26.3%, compared to conventional novolac systems. The increased char formation provides a protective barrier during high-friction events, minimizing mass loss, oxidation, and structural ablation. Further, specialized thermoset formulations like Novolac-4-HMPBA exhibit decomposition temperatures (T₅) exceeding 369°C, a 41% improvement over standard resins, thereby offering enhanced longevity under extreme braking cycles.

Studies also show a direct correlation between thermal decomposition temperature and friction stability, confirming that high-temperature-resistant novolac matrices translate into superior tribological performance and extended service life for disc brake pads, clutch facings, and heavy-duty industrial friction composites. The technical progress not only enhances mechanical performance but also aligns with regulatory goals for low dust and reduced brake emissions, further strengthening the adoption of advanced novolac-based binders in sustainable mobility solutions.

Market Opportunity 1: High-Density PCB Laminates for AI and High-Performance Computing (HPC)

The exponential rise of AI computing, data centers, and supercomputing infrastructure is driving robust demand for high-Tg (Glass Transition Temperature) novolac-cured epoxy laminates in high-density printed circuit boards (HDI PCBs). These materials must withstand lead-free solder reflow temperatures (260°C+) while maintaining structural integrity and signal fidelity in multilayer configurations.

High-performance novolac-cured epoxy systems have achieved Tg values exceeding 210°C (compared to 135°C for traditional FR-4 systems), ensuring dimensional stability and preventing delamination under thermal cycling. Such stability is vital in high-layer-count PCBs used for AI processors and HPC motherboards, where prolonged exposure to heat can compromise board integrity.

Simultaneously, incorporating specialized inorganic fillers into novolac epoxy matrices reduces the dielectric loss tangent (tan δ) from 0.04 to as low as 0.01 across GHz frequencies—crucial for maintaining signal integrity in high-speed data transmission. These performance gains position high-Tg, low-loss novolac-epoxy systems as essential materials for copper-clad laminates (CCLs) used in next-generation networking, AI acceleration cards, and HPC server boards.

Given that the global lead-free PCB manufacturing segment continues to expand in alignment with RoHS and WEEE directives, novolac resin suppliers offering thermally stable, low-dielectric epoxy systems are well-positioned to capitalize on the rapidly growing electronics materials market.

Market Opportunity 2: Aerospace Ablative and Refractory Composite Applications

The increasing pace of aerospace innovation, including hypersonic vehicles, reusable spacecraft, and missile systems, presents a high-margin growth frontier for novolac-based carbonizable and ablative materials. These applications demand exceptional thermal resistance, low thermal conductivity, and high carbon char retention for components such as nozzles, leading edges, and re-entry heat shields.

Experimental studies on novolac-phenolic composites have demonstrated reductions in ablation rates of up to 26% and significant mass loss reduction (≈21%) when compared with unmodified polymer matrices. The improved char structure forms a dense carbonized layer, protecting underlying materials from direct plasma exposure during re-entry or propulsion events.

Further development of low-density ablative composites (e.g., SPQ systems) using novolac phenolic matrices has achieved density reductions up to 43% and thermal conductivity drops by 50%, aligning with aerospace industry requirements for lightweight, high-insulation materials. Such advances directly contribute to improving payload efficiency and structural safety in both defense and space exploration missions.

Novolac resins are also essential precursors in the fabrication of Carbon/Carbon (C/C) composites, where they act as the binder and carbon source during pyrolysis. The resulting high-yield carbon matrices sustain functionality at temperatures exceeding 1,500°C, a necessity for rocket nozzle throats and hypersonic vehicle components. The capability makes high-carbon-yield novolac resins indispensable for next-generation refractory systems, where material failure tolerance is near zero.

Novolac Resins Market Share Insights, 2025-2034

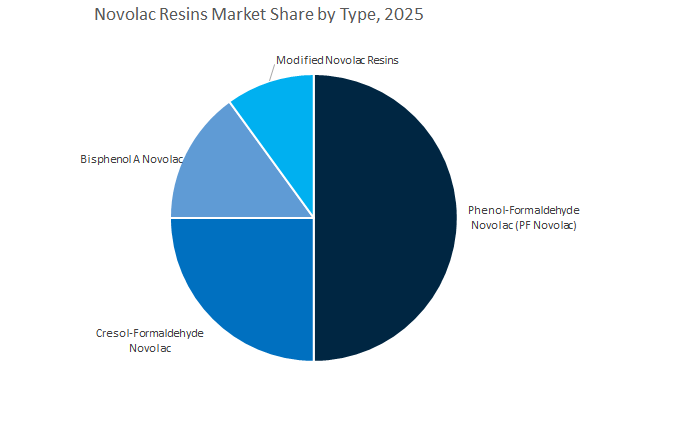

Market Share by Type

The Phenol-Formaldehyde (PF) Novolac segment dominates the global Novolac resins market, accounting for a projected 48.9% share in 2025, owing to its exceptional versatility, cost-efficiency, and robust performance across multiple industrial applications. PF Novolac resins offer excellent thermal stability, mechanical strength, and chemical resistance, making them the material of choice for friction materials, adhesives, coatings, insulation, and molding compounds. Their adaptability in powder coating binders, electrical insulation, and brake pads has solidified their leading role in both automotive and electronics industries. Furthermore, their ability to be easily modified with curing agents like hexamethylenetetramine (HMTA) enhances crosslinking performance, providing durability even in extreme thermal or chemical environments. As industries pursue high-performance thermosetting polymers that balance cost and reliability, PF Novolac resins continue to outperform alternative phenolic and epoxy systems.

Cresol-Formaldehyde Novolac resins hold a significant market share due to their superior thermal endurance, electrical insulation, and high purity levels, which are crucial for applications in semiconductor encapsulation, photoresists, and advanced composite materials. Their use in electronic packaging materials and copper-clad laminates continues to expand with the miniaturization of semiconductor components. Meanwhile, Bisphenol A Novolac resins are gaining traction in composite resins and corrosion-resistant coatings, offering improved toughness, rigidity, and thermal strength. These properties make them ideal for aerospace, industrial coatings, and high-performance structural adhesives. The Modified Novolac Resin segment—including variants modified with epoxy, rubber, or silicone—represents the innovation frontier, responding to market needs for eco-friendly, low-emission, and high-strength phenolic systems.

Market Share by End-Use Industry

The electrical and electronics industry leads the global Novolac resins market, commanding an estimated 33.6% share in 2025, due to extensive utilization in semiconductor encapsulation, printed circuit boards (PCBs), and electronic insulation systems. Novolac resins’ thermal stability, dielectric strength, and flame retardancy make them indispensable in protecting delicate electronic components from heat and chemical exposure. The surge in consumer electronics, 5G infrastructure, and miniaturized semiconductor devices has intensified demand for high-purity phenolic and cresol-based Novolacs used in encapsulants, solder resists, and epoxy modifiers. Their contribution to high-performance laminates, potting compounds, and heat shields reinforces their critical position in next-generation electronics manufacturing.

The automotive and transportation segment is another major market for Novolac resins, driven by their use in brake linings, clutch facings, friction materials, and under-the-hood components where thermal stability and mechanical strength are vital. With the rapid adoption of electric vehicles (EVs) and the need for lightweight, thermally resistant materials, Novolac resins are increasingly integrated into battery insulation systems, adhesives, and protective coatings. The construction and infrastructure sector maintains a steady share, primarily through the use of Novolac resins in structural adhesives, wood composites, and waterproof coatings, valued for their resistance to moisture and environmental degradation. In industrial and machinery applications, Novolac resins are essential for producing abrasives, composites, and high-temperature-resistant molded parts used in heavy equipment and manufacturing tools.

The global Novolac resins market is moderately consolidated, led by companies such as Hexion Inc., Sumitomo Bakelite Co., DIC Corporation, Kolon Industries Inc., and SI Group, each leveraging unique strengths in phenolic chemistry, process automation, and sustainability innovation. These firms are increasingly focused on supply chain optimization, digital manufacturing systems, and next-generation resin formulations to cater to high-performance industrial applications.

Hexion Inc., a global leader in phenolic thermosets and Novolac resins, continues to dominate with its Bakelite™ and Varcum™ brands. The company’s new 65-kiloton production reactor in Ohio has significantly enhanced its supply capacity for the automotive and industrial sectors. Through partnerships with Kadant Carmanah Design and Clariant, Hexion is integrating AI-driven production systems and fire-retardant material innovation into its Novolac resin portfolio. Its joint venture with Ravago underscores a commitment to circular economy models, enabling recycled phenol feedstock integration and reduced carbon intensity in resin manufacturing.

Sumitomo Bakelite remains a global pioneer in high-purity Novolac resins, with flagship products under the PHENOREZ™ and SUMILITERESIN brands. The company’s 6.1% R&D investment ratio reflects its dedication to innovation in semiconductor encapsulation and microelectronics applications. Its Singapore formulation lab focuses on developing low-VOC encapsulants for sub-10 nm chip packaging, while its Shizuoka plant features VOC capture and abatement systems for clean production. The June 2025 launch of lignin-modified Novolac resins cements Sumitomo’s leadership in bio-based phenolic chemistry for sustainable industrial materials.

DIC Corporation leverages deep expertise in color science and specialty formulations to expand its DICPHEN™ and FIBERLEN™ Novolac resin series. Following its October 2024 acquisition of a German additive company, DIC has integrated advanced chemistries to enhance resin adhesion, flexibility, and durability in coatings and laminates. The company’s bio-phenol pilot line, launched in December 2023, aligns with its long-term sustainability roadmap, targeting large-scale adoption of plant-derived phenols. With a strong foothold in electrical laminates and high-performance coatings, DIC continues to be a key innovator in eco-compliant Novolac resin systems.

Kolon Industries combines its Kolon Novolac and KOTEX™ product lines to serve critical friction, molding, and composite applications across the automotive industry. In collaboration with Hyundai, the company has been developing copper-free brake pad formulations to comply with new European dust emission standards, utilizing Novolac binders for superior heat resistance and wear performance. Its EV-focused phenolic composites, launched in January 2025, provide lightweight, flame-retardant battery housing solutions. With 63% of revenue derived from exports, Kolon’s strong OEM relationships and carbon-neutral manufacturing initiatives highlight its strategic commitment to sustainable industrial growth.

SI Group has positioned itself as a dynamic player in specialty Novolac resin markets, doubling capacity at its Nanjing facility to serve Asia-Pacific demand for industrial adhesives, tire tackifiers, and coating applications. Following a strategic divestment of its rubber business, the company is sharpening focus on phenolic and specialty resin portfolios. SI Group’s agile production framework enables fast customization for niche markets such as foundry binders and high-performance composites. Additionally, its European and Asian distribution partnerships have improved logistics efficiency by 22%, reinforcing its ability to meet localized customer requirements with precision.

Country Analysis: Global Novolac Resins Industry

Japan: Pioneering Bio-Based Novolac Resins and High-Performance Electronic Materials

Japan remains a global leader in advanced novolac resin innovation, particularly in sustainable thermoset materials and electronics-grade phenolic systems. In June 2025, Sumitomo Bakelite Co., Ltd. achieved a major technological milestone by commercializing the world’s first biomass-derived solid Novolac-type lignin-modified phenolic resin (PR-L-0002). The next-generation product—containing a 15% biomass ratio and offering an 11% reduction in carbon footprint (CFP)—marks a crucial step toward Japan’s broader carbon neutrality goals. The material’s application extends to high-strength friction and casting components in the automotive industry, demonstrating strong commercial viability in performance-critical environments.

In line with the country’s sustainability and digital transformation agenda, Sumitomo Bakelite has expanded its global manufacturing footprint, including a new Phenolic Molding Compounds plant at its Nantong, China subsidiary (April 2024) and a Liquid Phenolic Resin supply expansion at SNC Industrial Laminates in Malaysia (October 2024). The investments reinforce Japan’s regional supply network for printed circuit boards (PCBs), semiconductors, and electric vehicle (EV) components. Furthermore, the launch of a new facility at Sumitomo Bakelite (Suzhou) Co., Ltd. dedicated to epoxy resin molding compounds for semiconductor encapsulation reflects Japan’s strategic commitment to advanced electronic materials. The nation’s ongoing focus on fire-resistant phenolic molding compounds for EV batteries also highlights its contribution to the global e-mobility and green materials ecosystem.

United States: Regulatory Reforms and AI-Driven Innovation Define Market Direction

The United States novolac resins market is characterized by regulatory evolution, sustainability certifications, and AI-enabled process optimization. In December 2024, the U.S. Environmental Protection Agency (EPA) released its final risk evaluation for formaldehyde under the Toxic Substances Control Act (TSCA)—a pivotal regulation directly influencing novolac resin production and usage across adhesives, coatings, and composite wood applications. Concurrently, in April 2024, the EPA finalized amendments to the National Emissions Standards for Hazardous Air Pollutants (NESHAP), enforcing stricter control technology standards on emissions from resin manufacturing plants. The policies are expected to elevate compliance costs but will accelerate the transition toward low-emission, sustainable production lines for phenolic resins.

Hexion Inc., one of the country’s leading resin manufacturers, is actively redefining its novolac resin strategy through innovation and sustainability. Its acquisition of Smartech (May 2025) integrates artificial intelligence (AI) into process optimization, enabling energy-efficient production and predictive maintenance across its specialty chemicals operations. In addition, Hexion’s ISCC PLUS certification (Baytown, Texas site, 2023) validates the company’s use of renewable feedstocks under the mass balance approach, signaling the U.S. industry’s growing commitment to bio-attributed novolac systems. Collaborations like the Hexion-Clariant partnership (December 2024) for high-performance intumescent coatings also exemplify how novolac-epoxy hybrid systems are becoming central to fire protection and construction markets, reflecting the U.S.’s focus on high-value specialty resin applications.

South Korea: Driving EV Safety and Advanced Composites with Novolac-Based Technologies

South Korea’s novolac resin market is rapidly aligning with its mobility innovation agenda, leveraging its strong industrial base in electric vehicles (EVs), hydrogen energy, and advanced composites. In July 2024, Kolon Group launched Kolon Spaceworks, a dedicated advanced materials company designed to consolidate and expand its composite materials business. The strategic move positions South Korea as a key producer of high-performance novolac-based composite prepregs for use in battery covers, hydrogen storage tanks, and lightweight automotive components.

Kolon Spaceworks is at the forefront of developing flame-retardant unidirectional (UD) tapes using phenolic and novolac matrix systems—critical for mitigating thermal runaway risks in EV batteries. The innovations reflect South Korea’s national focus on EV safety, performance, and energy efficiency. The country's expertise in carbon-fiber reinforced and novolac-modified thermosets is extending into aerospace and defense applications, signaling the broader industrial potential of high-temperature-resistant novolac resins. As the Korean government increases R&D incentives for advanced materials, local manufacturers are expected to lead the next generation of composite-grade novolac resins, reinforcing South Korea’s status as a global innovation hub for advanced mobility materials.

Germany and Europe: Consolidation and Bio-Based Value Chain Leadership

Germany—and the broader European Union—continue to dominate the bio-based and circular economy transition within the novolac resins landscape. In July 2022, Prefere Resins Group, one of Europe’s largest producers of phenolic and amino resins, was acquired by One Rock Capital Partners, marking a strategic consolidation aimed at expanding product diversity, geographic reach, and R&D intensity. Under The ownership, Prefere has accelerated its bio-based resin transition, aligning with EU Green Deal objectives to minimize environmental impact in construction, automotive, and industrial adhesive applications.

German and European chemical majors are also leading the charge toward sustainable chemical intermediates. For instance, BASF’s biomass-balanced (BMB) ammonia and urea products (May 2024)—certified under ISCC PLUS standards—illustrate a systemic shift toward renewable feedstocks that influence the entire resin value chain, including novolac production. The European market’s heavy regulatory framework, encompassing REACH and EU Taxonomy, ensures that novolac resin manufacturers prioritize eco-certified, low-emission, and circular formulations. Furthermore, ongoing research in bio-based phenol substitutes and lignin-derived aromatic compounds is establishing Europe as the global leader in sustainable resin chemistry, setting benchmarks for other regions to follow.

Novolac Resins Market Report Scope

Novolac Resins Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.6 Billion

|

|

Market Size (2034)

|

$4 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Type (Phenol-Formaldehyde Novolac, Cresol-Formaldehyde Novolac, Bisphenol A Novolac, Modified Novolac), By Form (Solid, Liquid), By Application (Molding Compounds, Coatings & Adhesives, Friction Materials, Tire and Rubber Products, Electronics & Semiconductor Materials, Refractories & Foundry, Advanced Composites), By End-use Industry (Automotive & Transportation, Construction & Infrastructure, Electrical & Electronics, Aerospace & Defense, Industrial & Machinery

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sumitomo Bakelite Co., Ltd., Hexion Inc., BASF SE, Prefere Resins Group, DIC Corporation, Showa Denko Materials Co., Ltd., Huntsman Corporation, Kolon Industries, Inc., Georgia-Pacific Chemicals LLC, Sinopec Corporation, Chang Chun Group, Shandong Laiwu Runda Chemical Co., Ltd., Aica Kogyo Co., Ltd., Atul Ltd., Kukdo Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Type

- Phenol-Formaldehyde Novolac

- Cresol-Formaldehyde Novolac

- Bisphenol A Novolac

- Modified Novolac

By Form

By Key Application

- Molding Compounds

- Coatings & Adhesives

- Friction Materials

- Tire and Rubber Products

- Electronics & Semiconductor Materials

- Refractories & Foundry

- Advanced Composites

By End-use Industry

- Automotive & Transportation

- Construction & Infrastructure

- Electrical & Electronics

- Aerospace & Defense

- Industrial & Machinery

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Novolac Resins Market

- Sumitomo Bakelite Co., Ltd.

- Hexion Inc.

- BASF SE

- Prefere Resins Group

- DIC Corporation

- Showa Denko Materials Co., Ltd.

- Huntsman Corporation

- Kolon Industries, Inc.

- Georgia-Pacific Chemicals LLC

- Sinopec Corporation

- Chang Chun Group

- Shandong Laiwu Runda Chemical Co., Ltd.

- Aica Kogyo Co., Ltd.

- Atul Ltd.

- Kukdo Chemical Co., Ltd.

*- List not Exhaustive

Research Coverage

This report investigates the Novolac Resins Market through end-use mapping and technology benchmarking, delivers analysis reviews on demand inflection points across automotive friction systems, high-density electronics, refractories, and advanced composites, curates breakthroughs in low-ion/semiconductor-grade novolacs, boron-modified high-char binders, and bio-attributed phenolic feedstocks, and highlights processing windows, cross-link density control, and reliability metrics that underpin next-generation performance; developed by USDAnalytics, this report is an essential resource for product managers, procurement leaders, application engineers, and investors seeking defensible forecasts, compliance alignment, and clear routes to commercialization in phenolic thermoset value chains.

Scope Highlights

Segmentation:

- By Type: Phenol-Formaldehyde Novolac; Cresol-Formaldehyde Novolac; Bisphenol A Novolac; Modified Novolac.

- By Form: Solid; Liquid.

- By Key Application: Molding Compounds; Coatings & Adhesives; Friction Materials; Tire & Rubber Products; Electronics & Semiconductor Materials; Refractories & Foundry; Advanced Composites.

- By End-use Industry: Automotive & Transportation; Construction & Infrastructure; Electrical & Electronics; Aerospace & Defense; Industrial & Machinery.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies covering strategies, portfolios, capacity moves, partnerships, and innovation pipelines.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.