Explosive Growth in the Packaged Water Treatment System Market Driven by Industrialization and Sustainability Goals

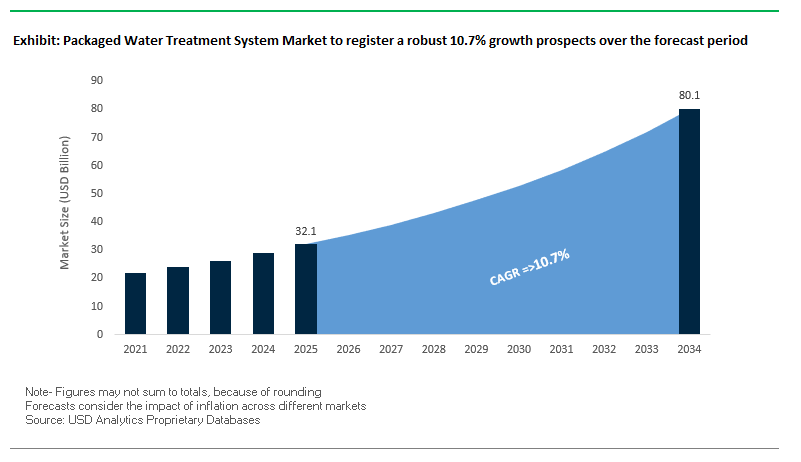

The global packaged water treatment system market is projected to surge from $32.1 billion in 2025 to $80.1 billion by 2034, reflecting an impressive CAGR of 10.7%. The rapid expansion is fueled by the growing need for decentralized water purification, industrial effluent management, and cost-efficient, easily deployable solutions in both developed and emerging markets.

Such systems, especially skid-mounted packaged units, have become popular because they are truly "plug-and-play" systems, thereby cutting down on-site construction time and expenditure. Membrane filtration technology like reverse osmosis (RO) and ultrafiltration (UF) lead the technology scene, as they serve these high purity waters to industries and municipal users.

Water treatment stands out as the largest application area due to increasing environmental regulations, urbanization across developing nations, and a need to treat sewage effectively in hinterlands. Asia Pacific continues to be ahead in terms of adoption, with fast-paced growth in manufacturing bases, urbanization, and water shortages driving demand for scalable and modular solutions to treat waters.

Key Insights:

- Dominance of Skid-Mounted Systems for rapid, low-cost deployment.

- Membrane Filtration Leads Technology Adoption, particularly RO and UF.

- Wastewater Treatment as Core Application, especially for decentralized solutions.

- Asia Pacific as Growth Engine due to urbanization and industrialization trends.

Market Analysis: Strategic Projects, Partnerships, and Technological Innovation Redefine the Competitive Landscape

Strategic partnerships, mergers and innovation propel market growth both in municipal and industrial applications. Veolia was awarded a contract to provide France's largest wastewater reuse scheme in Argelès-sur-Mer during July 2025, consistent with ongoing priorities around water reuse and compliance with environmental mandates. A. O. Smith reported a 19% organic growth in Indian and MEA water conservation operations in July that shows satisfactory uptake of packaged systems for commercial and institutional applications in high-growth economies.

Also in July 2025, SUEZ, together with SIAAP, launched a production unit combining wastewater treatment and energy recovery choosing the trend of circular economy. Thermax and Tata Projects forged a strategic alliance in India to provide large-capacity packaged water and wastewater treatment solutions reinforcing turnkey project capabilities in competitive advantage.

More recent developments between late 2024 and mid-2025 further signal sector technological strength. Xylem advanced further into the anaerobic membrane bioreactor (AnMBR) market in September 2024, while Pentair expanded its membrane filtration capabilities by acquiring Porous Media in October 2024 in a $225 million transaction. Veolia in June 2025 commissioned America's largest PFAS treatment plant, a $35 million facility demonstrating its capacity to address emerging contaminants. Before this was Smart Ops' May 2024 rollout of India's Smart Ops SCR System, a packaged water treatment solution utilizing biotechnology-based technology meant to address localized water concerns.

Trends and Opportunities in Packaged Water Treatment System Market

Trend 1: Rapid Deployment of Modular Systems for Disaster Response

The packaged water treatment systems market is experiencing significant growth driven by the urgent need for rapidly deployable, modular water treatment solutions in disaster-stricken and infrastructure-challenged regions. Climate change-induced disasters, including floods, hurricanes, and extreme weather events, have exposed vulnerabilities in centralized water networks, driving demand for portable, plug-and-play treatment units. The U.S. Environmental Protection Agency (EPA), in collaboration with non-profits, has developed mobile systems such as the "Water-on-Wheels Mobile Water Treatment System (WOW Cart)," which integrates multiple treatment technologies with alternative power sources to provide safe drinking water during emergencies. Organizations like Veolia maintain fleets of mobile membrane bioreactors, reverse osmosis trailers, and carbon filters, which can be deployed to municipal and industrial sites within hours, ensuring continuity of critical water services. The United Nations Office for Disaster Risk Reduction (UNDRR) emphasizes that building resilience into infrastructure through such modular systems can increase investment costs by as little as 3% while substantially mitigating disaster impacts. Market trends indicate that demand for mobile packaged systems is projected to grow at a CAGR of over 11% in North America and Europe, fueled by government initiatives, public-private partnerships, and increasing frequency of natural disasters.

Trend 2: Decentralized Treatment for Small Communities

Decentralized water treatment is becoming a primary trend among rural, peri-urban, and underserved communities without accessible centralized infrastructure. Packaged water treatment systems provide a low-cost, scalable solution to these areas, allowing communities to reach clean water access without a high upfront investment typical of traditional plants. Due to their modular nature, these systems can be expanded incrementally in capacity increments starting with small units (<50 m³/day) and scaling to accommodate population growth or industrial demand. Pilot programs have shown that decentralized systems can reach greater than 99% pathogen reduction and 90% total suspended solids removal while meeting rigorous environmental discharge levels and enhancing public heath metrics. Economically, these systems remove the need for long-haul pipelines and centralized facilities and become most attractive in low-density or geography-tough locations. Adoption rates continue to increase internationally, emerging Asian and Latin American markets investing aggressively in decentralized packaged systems to close gaps in available water access and sanitation services, experiencing market growth rates between 10–12% per annum.

Opportunity 1: Industrial Zero Liquid Discharge (ZLD) in Emerging Markets

Growing enforcement of environmental regulations and corporate sustainability initiatives across emerging markets is driving demand for packaged, small-footprint Zero Liquid Discharge (ZLD) technology. Textile, mining, and food & beverage manufacturing companies are challenged to minimize or eliminate wastewater effluent while optimizing resource recovery. Rules mandated by India's Central Pollution Control Board (CPCB) and state pollution control boards demand compliance with ZLD within textile clusters such as Surat, driving mass migration to cutting-edge packaged systems. Modern membrane filtration, evaporation, and crystallization allow state-of-the-art ZLD facilities to recover salts of commercial value and recycle waters while facilitating operational cost recovery and new streams of revenue. Business cases such as those within Chennai provide evidence of how revenues generated from treating and reclaiming effluent waters for process applications can recover operational costs and capital investments within a timeframe of five years or less. Adoption of ZLD technology within packaged solutions not only facilitates compliance with rules but further bolsters concepts of a circular economy while reinforcing sustainability strategies within industrial firms.

Opportunity 2: Offshore and Remote Site Applications

Packaged water treatment systems continue to be installed in offshore, isolated, and remote locations such as oil rigs, military camps, and island communities where centralized water supply is not economically feasible. Such applications demand compact, energy-efficient, and rugged systems producing potable and process-quality water in difficult operating conditions. Advanced reverse osmosis (RO) packaged units designed to be offshore-capable achieve high recovery ratios, low power consumption, and multi-stage treatment to achieve World Health Organization (WHO) drinking water quality. Hundreds of Pure Aqua seawater RO systems have been installed worldwide by companies such as Pure Aqua to prove demand for the market for such reliable, stand-alone units. Such units often have other features such as corrosion resistance, light weight, and ability to be easily installed and maintained to provide continued operation in extreme marine or isolated locations. The segment growth is powered by rising offshore oil exploration activity, installation of distant infrastructures, and global standards compliance. Adoption levels will increase at a projected 9–10% CAGR in the coming five years.

Packaged Water Treatment System Market Share Insights

Membrane Bioreactor Systems Driving Premium Growth

Membrane Bioreactor (MBR) systems are projected to capture nearly 30% of the packaged water treatment system market by 2025, making them the premium growth leader. Their dominance stems from their ability to deliver high-quality effluent in compact footprints, a critical advantage for decentralized treatment where space and discharge standards are strict. MBR adoption is accelerating in industrial clusters and rapidly urbanizing regions, where water reuse is no longer optional but a regulatory and cost-driven necessity. The technology’s position as the benchmark for quality effluent and modular deployment ensures continued preference across both developed and emerging economies.

.png)

Reverse Osmosis and SBR Systems Shaping Market Core

Reverse Osmosis (RO) systems, with a projected 25% market share, remain the industry standard for desalination and high-purity process water generation. Their role in Zero Liquid Discharge (ZLD) and industrial recycling streams positions them as an indispensable component of modern water treatment infrastructure. In parallel, Sequencing Batch Reactors (SBR) account for nearly 20%, acting as the proven biological treatment workhorse. Favored for their operational flexibility and reliability under variable loads, SBRs continue to find application in smaller municipalities and industrial operations seeking a balance between cost and performance. Together, RO and SBR systems form the backbone of the sector’s mainstream adoption curve.

Niche Opportunities in Extended Aeration and Electrocoagulation

Extended Aeration systems secure approximately 15% of the market, valued for their cost-effectiveness in treating less complex wastewaters for smaller communities and light industrial users. Their lower energy efficiency is offset by reduced capital requirements, which sustains demand in budget-sensitive projects. Meanwhile, Electrocoagulation systems, though holding a modest 10% share, are emerging as a niche technology for industries such as mining, textiles, and metal finishing. Their ability to handle challenging effluents with emulsified oils and heavy metals without the use of added chemicals makes them an attractive option where environmental compliance and footprint reduction are priorities.

Treatment Capacity Trends: Decentralization Sweet Spot at 50–200 m³/day

In terms of treatment capacity, systems handling 50–200 m³/day command the largest share at 35%, reflecting the global shift toward decentralized wastewater treatment. These units strike a balance between scalability and modularity, making them the go-to choice for medium industrial facilities, large commercial complexes, and small communities. Smaller systems (<50 m³/day), with a 25% share, are crucial for remote resorts, construction camps, and isolated industrial sites where ease of operation and portability matter most. The 200–500 m³/day range, also at 25%, caters to large industrial plants and small towns, while systems above 500 m³/day, at 15%, represent high-value project-based contracts for rapid municipal expansions and temporary treatment during upgrades.

Industrial End-Use Leading with Compliance-Driven Demand

The industrial sector dominates with 50% of global demand, reflecting its need for compliance, water reuse, and operational independence. Industries such as food and beverage rely heavily on packaged MBR and SBR systems to treat high-organic wastewater before discharge or reuse. In oil & gas, packaged systems address both produced water treatment and camp sanitation in remote sites, while in mining, electrocoagulation and biological systems manage metal-laden effluents and acidic mine drainage. The breadth and diversity of industrial applications make the sector the largest and most resilient revenue stream in the market.

Municipal Sector as a Strategic Growth Engine

Municipal adoption, accounting for nearly 30% of the market, is expanding as cities and towns look for satellite treatment solutions in suburban growth corridors. Packaged systems provide municipalities with a cost-effective alternative to large centralized plants, particularly for rural communities and overloaded urban infrastructure. Their modularity and rapid deployment capability make them essential for bridging infrastructure gaps and meeting tightening environmental discharge norms. As governments globally push for water reuse and decentralized treatment models, municipal demand is set to accelerate significantly.

Commercial Applications Expanding with Tourism and Infrastructure Projects

The commercial sector contributes around 20%, led by high-value users such as resorts, construction sites, and institutional facilities. Resorts and hotels, especially those in coastal and alpine environments, adopt packaged MBR and SBR systems to meet strict environmental discharge standards and support reuse in irrigation. Construction sites demand temporary and mobile packaged systems to manage both camp sewage and turbid runoff, while hospitals and military installations prioritize highly reliable, independent operations. The segment’s growth is directly tied to global tourism expansion, infrastructure development, and the increasing need for localized, compliant wastewater solutions.

Country Analysis of the Packaged Water Treatment System Market

United States: Federal Infrastructure Spending Drives Packaged System Adoption

The United States packaged water treatment systems market is being propelled by substantial government funding and rising demand for decentralized solutions. The Bipartisan Infrastructure Law has allocated over $50 billion to upgrade drinking water and wastewater systems, directly stimulating the deployment of both centralized and packaged treatment solutions. The U.S. Environmental Protection Agency (EPA) is actively addressing PFAS contamination, increasing demand for packaged systems equipped with advanced filtration technologies capable of removing these contaminants. Xylem Inc.’s acquisition of Evoqua expands its portfolio in packaged water treatment technologies across North America and Europe. Ecolab’s acquisition of Barclay Water Management in 2024 further strengthens offerings in municipal and industrial packaged treatment systems. DuPont Water Solutions has been recognized for its sustainable membranes and ion exchange resins, highlighting the role of packaged treatment technologies in water purification, reuse, and conservation. The EPA is also promoting alternative drinking water delivery solutions, including packaged treatment devices in homes and small communities where conventional infrastructure is unaffordable or infeasible.

China: Rural Water Safety Initiatives and Industrial Packaged Systems

China's packaged water treatment system market is driven by lofty state targets for treating wastewater and a new focus on water security in the hinterlands and in the industrial sector. An aim of a 95% coverage of wastewater at the level of county-level cities creates a demand for packaged treatment technology that is extremely high. SUEZ has partnered with Shandong Public to build and operate an industrial wastewater treatment plant within Jining New Materials Industrial Park that utilizes packaged systems to achieve 100% recycling of water. The H2O Solution program is a data-driven packaged solution tailored to efficiently address rural villagers' water pollution challenges. Stringent regulations targeting key polluters like chemical oxygen demand (COD), ammonia nitrogen (NH4), and total phosphorus keep demand for advanced packaged water and wastewater treatment systems going.

India: Rapid Deployment and Government-Led Packaged Solutions

Indian packaged water treatment systems market is gathering pace owing to large-scale governmental programs and rapid deployment initiatives. Namami Gange has cleared a total 488 projects valued at more than ₹39,730 crore, out of which a large proportion use pre-engineered or packaged systems for rehabilitation and sewage treatment. Enviro Infra Engineers has won a Maharashtra ₹395.5 crore ZLD project involving packaged treatment phases. Jal Jeevan Mission focuses on household tap quality in water and depends upon innovative packaged purification systems both in urban and rural India. Government financial aid guarantees infra development and technology deployment. Large companies like VA Tech Wabag and Thermax are currently implementing large-scale water supply and wastewater management initiatives, which reflect a concentration within market on modular rapid-deployment solutions.

Japan: Portable and Disaster-Ready Packaged Systems

Japan’s packaged water treatment systems market emphasizes disaster preparedness and portable water solutions. WOTA Corp. developed a small-scale, portable water recycling system capable of reclaiming over 98% of wastewater, deployed after the 2024 Noto Peninsula Earthquake. NIHON GENRYO Co., Ltd. offers the Mobile SIPHON TANK, a compact, unified packaged water treatment system designed for disaster relief and regions with limited infrastructure. Kurita Water Industries’ partnership with ispace to transport a water purification system to the moon after 2027 reflects the focus on advanced, specialized packaged systems for extreme environments. The Japanese government’s emphasis on decentralized water treatment and emergency preparedness encourages innovation in portable, modular water treatment solutions.

Saudi Arabia: National Water Strategy Boosts Packaged System Demand

Saudi Arabia is investing heavily in wastewater infrastructure through its National Water Strategy 2030, creating opportunities for packaged treatment systems that allow rapid deployment and operational flexibility. The Jeddah Airport 2 Independent Sewage Treatment Project (ISTP) will implement Nereda technology in a modular setup, while the Madinah-3 Wastewater Treatment Plant serves over 1.1 million residents with an expandable packaged solution. The Taif Independent Sewage Treatment Plant employs Waterleau’s LUCAS® Cyclic Activated Sludge technology, integrating key treatment phases in a compact, energy-efficient packaged design. These projects demonstrate the growing role of modular and pre-engineered treatment units in large-scale municipal applications.

Germany: Modular Systems Align with Sustainability and EU Regulations

Germany’s packaged water treatment systems market is shaped by EU water quality regulations and a strong sustainability focus. Compliance with the European Union Water Framework Directive drives adoption of packaged and modular systems that improve water quality and optimize energy use. Advanced technologies such as membrane filtration and energy-efficient treatment processes are increasingly available in self-contained, pre-engineered forms. Germany’s ambitious climate targets, aligned with the Paris Agreement, further fuel investments in sustainable water treatment solutions. Companies like BWT AG are developing innovative filter ranges and modular units that offer efficient, easy-to-install packaged treatment solutions for residential, industrial, and municipal applications.

Competitive Landscape: Global Leaders Driving Technological and Market Advancements

The packaged water treatment system market is defined by multinational corporations leveraging innovation, sustainability, and modular design to strengthen their positions. Competitors are increasingly integrating digital monitoring, energy recovery, and customized configurations to meet regulatory, operational, and cost-efficiency demands.

Xylem Inc.: Delivering Smart, Integrated Packaged Water Treatment Solutions

Xylem's product portfolio comprises state-of-the-art disinfection systems through Wedeco, biological treatment through Sanitaire, and filtration through Leopold integrated in modular units to facilitate deployment. Its Xylem Vue digital platform supports predictive maintenance and real-time monitoring to minimize operational downtime and manpower use. With effective integration across the entire water cycle, Xylem provides end-to-end packaged solutions to municipal and industrial customers across the globe.

Veolia Environnement S.A.: Modular Water Reuse and Resource Recovery Leader

Veolia offers package and containerized treatment plants in a packaged and module format featuring Actiflo® clarification technology, Biobed®, AnoxKaldnes™ biological technology, and membrane solutions. Its acquisition of full ownership of its Water Technologies and Solutions (WTS) business allows a streamlined product range. Its system for recuperation of biogas from effluent is distinct within the fast-emerging resource recoveries market.

SUEZ S.A.: Flexible, High-Performance Packaged Water Treatment Systems

It has expertise in mobile and containerized solutions for drinking water and municipal and industrial wastewater treatment and applies MBR, RO, UF, and disinfection technology. Its use of AI-based digital centers makes operations most efficient and compliant. It has a global reach and a capability to tailor deployments to suit users' requirements, making it a good partner both to municipal and industrial users.

Pentair plc: Sustainable, High-Efficiency Packaged Systems for Industry

Pentair's pre-engineered packaged systems serve light commercial and industrial applications and possesses a distinct strength in advanced filtration thanks to its own acquisition of Porous Media. It has active solutions available to treat PFAS contamination and has pre-engineered energy-efficient filtration units that can be readily integrated within large treatment configurations.

Thermax Limited: Customized Industrial Packaged Water Solutions

Thermax supplies containerized, RO, UF, and biological solutions along with a strong zero liquid discharge (ZLD) solution orientation. With its alliance with Tata Projects, Thermax can provide large turnkey Indian water treatment projects. With extensive process know-how, Thermax customizes systems to provide site-specific solutions ranging from boiler water softening to effluent treatment in industry.

Packaged Water Treatment System Market Report Scope

Packaged Water Treatment System Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$32.1 Billion

|

|

Market Size (2034)

|

$80.1 Billion

|

|

Market Growth Rate

|

10.7%

|

|

Segments

|

By System Type (Extended Aeration Systems, Membrane Bioreactor (MBR) Systems, Reverse Osmosis Systems, Electrocoagulation Systems, Sequencing Batch Reactors (SBR)), By Treatment Capacity (<50 m³/day, 50-200 m³/day, 200-500 m³/day, >500 m³/day), By End-Use Industry (Municipal Sector, Industrial Sector, Oil & gas, Food & beverage, Mining camps, Power plants, Commercial Sector, Resorts/hotels, Schools, Hospitals, Construction sites, Military bases)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Xylem Inc., SUEZ, Pentair, Evoqua Water Technologies (now part of Xylem), Fluence Corporation, Sustainable Biosolutions Private Limited (SUSBIO), VA Tech Wabag Ltd., Thermax Limited, Ion Exchange India Ltd., Larsen & Toubro (L&T) - Water & Effluent Treatment, Toshiba Water Solutions, Corix Water System, RWL Water

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaged Water Treatment System Market Segmentation

By System Type

- Extended Aeration Systems

- Membrane Bioreactor (MBR) Systems

- Reverse Osmosis Systems

- Electrocoagulation Systems

- Sequencing Batch Reactors (SBR)

By Treatment Capacity

- <50 m³/day

- 50-200 m³/day

- 200-500 m³/day

- >500 m³/day

By End-Use Industry

- Municipal Sector

- Industrial Sector

- Oil & gas

- Food & beverage

- Mining camps

- Power plants

- Commercial Sector

- Resorts/hotels

- Schools

- Hospitals

- Construction sites

- Military bases

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaged Water Treatment System Market

- Veolia

- Xylem Inc.

- SUEZ

- Pentair

- Evoqua Water Technologies (now part of Xylem)

- Fluence Corporation

- Sustainable Biosolutions Private Limited (SUSBIO)

- VA Tech Wabag Ltd.

- Thermax Limited

- Ion Exchange India Ltd.

- Larsen & Toubro (L&T) - Water & Effluent Treatment

- Toshiba Water Solutions

- Corix Water System

- RWL Water

* List Not Exhaustive

Research Coverage

This report investigates the Global Packaged Water Treatment System Market, delivering analysis reviews of key growth drivers, technological breakthroughs, and corporate strategies shaping the industry’s evolution. Published by USDAnalytics, the study highlights how industrialization, sustainability targets, and decentralized water management are accelerating adoption of modular and skid-mounted systems worldwide. It emphasizes the rising importance of membrane filtration (RO, UF), membrane bioreactors (MBRs), and zero liquid discharge (ZLD) solutions, alongside strategic partnerships, acquisitions, and government-led initiatives. With insights into technological advances, regulatory compliance, and regional adoption dynamics, this report highlights competitive positioning, tracks strategic collaborations, and provides actionable forecasts. This report is an essential resource for water technology providers, project developers, policymakers, and investors seeking to capitalize on long-term opportunities in modular water and wastewater treatment.

Scope Includes:

- Segmentation: By Product (Skid-Mounted, Extended Aeration, Electrocoagulation, Others), Technology (RO, UF, MBR, SBR, Hybrid Systems), Capacity (<50 m³/day, 50–200 m³/day, 200–500 m³/day, >500 m³/day), and End-Use (Industrial, Municipal, Commercial).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe: Historic data from 2021–2024 and forecast data from 2025–2034.

- Companies: Analysis and profiles of 15+ leading companies active in the global packaged water treatment system market.

Methodology

The research methodology applied by USDAnalytics combines primary and secondary approaches to deliver robust and credible market intelligence. Primary research included interviews with technology providers, EPC contractors, regulators, and end-users across industrial, municipal, and commercial sectors. Secondary research leveraged government publications, corporate filings, peer-reviewed journals, and industry databases to validate findings. Market size estimates were developed using top-down and bottom-up models, cross-verified through data triangulation and scenario analysis. Expert validation further ensured accuracy, making this study a reliable reference for corporate strategy, policy planning, and investment decisions in the packaged water treatment system market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Packaged Water Treatment System Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights

1.3. Global Market Snapshot

2. Packaged Water Treatment System Market Outlook (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $32.1 Billion

2.2.2. Forecasted Market Size (2034): $80.1 Billion at 10.7% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Dominance of Skid-Mounted Systems

2.3.2. Membrane Filtration Technology Adoption

2.3.3. Wastewater Treatment as a Core Application

2.3.4. Asia Pacific as a Growth Engine

3. Market Analysis: Strategic Projects, Partnerships, and Technological Innovation

3.1. Overview of Market Trends

3.2. Recent Strategic Partnerships and Acquisitions

3.2.1. Veolia's Argelès-sur-Mer Contract and WTS Acquisition

3.2.2. A. O. Smith's Growth in India and MEA

3.2.3. SUEZ and SIAAP's Wastewater-to-Energy Project

3.2.4. Thermax and Tata Projects Alliance

3.3. Key Technological Developments (2024–2025)

3.3.1. Xylem's Anaerobic Membrane Bioreactor (AnMBR)

3.3.2. Pentair's Acquisition of Porous Media

3.3.3. Veolia's PFAS Treatment Plant Commissioning

3.3.4. Smart Ops' SCR System Rollout

4. Trends and Opportunities in Packaged Water Treatment System Market

4.1. Trend 1: Rapid Deployment of Modular Systems for Disaster Response

4.1.1. Role in Climate Change-Induced Disasters

4.1.2. Examples of Mobile Systems (e.g., "WOW Cart")

4.2. Trend 2: Decentralized Treatment for Small Communities

4.2.1. Addressing Infrastructure Gaps in Rural and Peri-Urban Areas

4.2.2. Economic and Health Benefits of Decentralized Systems

4.3. Opportunity 1: Industrial Zero Liquid Discharge (ZLD) in Emerging Markets

4.3.1. Regulatory Drivers and Corporate Sustainability

4.3.2. Economic Benefits and Resource Recovery

4.4. Opportunity 2: Offshore and Remote Site Applications

4.4.1. Demand from Oil Rigs, Military Camps, and Remote Communities

4.4.2. Technological Requirements for Extreme Environments

5. Packaged Water Treatment System Market Share Insights

5.1. By System Type

5.1.1. Membrane Bioreactor (MBR) Systems

5.1.2. Reverse Osmosis (RO) Systems and Sequencing Batch Reactors (SBR)

5.1.3. Extended Aeration and Electrocoagulation Systems

5.2. By Treatment Capacity

5.2.1. Decentralization Sweet Spot: 50–200 m³/day

5.2.2. Smaller and Larger Capacity Segments

5.3. By End-Use Industry

5.3.1. Industrial Sector

5.3.2. Municipal Sector

5.3.3. Commercial Sector

6. Country Analysis of the Packaged Water Treatment System Market

6.1. United States: Federal Infrastructure Spending and PFAS

6.2. China: Rural Water Safety Initiatives and Industrial Systems

6.3. India: Government-Led Packaged Solutions and Rapid Deployment

6.4. Japan: Portable and Disaster-Ready Systems

6.5. Saudi Arabia: National Water Strategy Boosts Demand

6.6. Germany: Modular Systems and Sustainability

6.7. Other Country Analysis (e.g., UK, France, UAE)

7. Packaged Water Treatment System Market Size Outlook by Region (2025–2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By System Type, Capacity, and End-Use

7.2. Europe Market Size Outlook to 2034

7.2.1. By System Type, Capacity, and End-Use

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By System Type, Capacity, and End-Use

7.4. South America Market Size Outlook to 2034

7.4.1. By System Type, Capacity, and End-Use

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By System Type, Capacity, and End-Use

8. Company Profiles: Top Companies in Packaged Water Treatment System Market

8.1. Veolia

8.2. Xylem Inc.

8.3. SUEZ

8.4. Pentair

8.5. Evoqua Water Technologies (now part of Xylem)

8.6. Fluence Corporation

8.7. Sustainable Biosolutions Private Limited (SUSBIO)

8.8. VA Tech Wabag Ltd.

8.9. Thermax Limited

8.10. Ion Exchange India Ltd.

8.11. Larsen & Toubro (L&T)

8.12. Toshiba Water Solutions

8.13. Corix Water System

8.14. RWL Water

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations