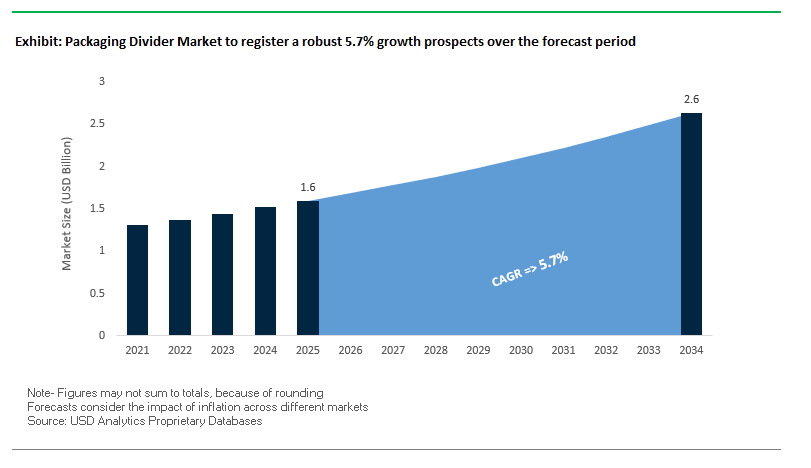

Packaging Divider Market to Reach $2.6 Billion by 2034 at a CAGR of 5.7%

The global packaging divider market is expected to grow from $1.6 billion in 2025 to $2.6 billion by 2034, representing a CAGR of 5.7%. Packaging dividers are a vital component of modern supply chains, providing protective, organizational, and structural solutions for a variety of industries. They are made from corrugated paper, molded pulp, plastic, and foam, and are crucial in reducing product damage, enhancing logistics efficiency, and improving the consumer experience.

Key Insights for Industry Professionals:

- E-commerce growth driving demand: Dividers secure products during transit, reducing returns and improving customer satisfaction.

- Sustainability trends: Shift toward fiber-based, molded pulp, and recycled plastic dividers aligns with ESG goals and regulatory requirements.

- Enhanced product protection: Critical for pharmaceuticals, automotive components, and sensitive electronics.

- Customization and design optimization: Use of digital design and automation minimizes material use, reduces package size, and enhances unboxing experiences.

- Innovation in food packaging: Dividers enable mess-free, convenient consumption in on-the-go product formats.

Market Analysis: Recent Developments Highlight Consolidation, Sustainability, and Advanced Manufacturing

The packaging divider industry is highly dynamic, with a strong focus on sustainability, advanced manufacturing, and strategic mergers. In July 2025, the all-stock merger of Amcor and Berry Global Group created a dominant force in flexible and rigid packaging, directly influencing the demand for dividers. In May 2025, Mondi started up a new €400 million paper machine at its Štětí mill, strengthening its leadership in sustainable paper and packaging materials, including those used for dividers. April 2025 saw International Paper complete its $9.9 billion acquisition of DS Smith, expanding corrugated box and divider offerings across North America and Europe.

In January 2025, Dordan Manufacturing Company installed a new prototyping press, enhancing its capabilities in custom thermoformed dividers for medical devices and electronics. December 2024 featured the launch of Belgian Boys’ Breakfast All Day boxes and Pancakes & Go cups, highlighting the role of dividers in convenient food packaging. November 2024 marked the completion of the WestRock acquisition by Smurfit Kappa, forming Smurfit WestRock, a global leader in paper and divider solutions. Additionally, September 2024 saw increased adoption of mono-material packaging and recyclable fiber-based dividers, while Sabert launched its Hot2Go pack, demonstrating eco-friendly innovation in on-the-move food solutions.

Trends and Opportunities Transforming the Packaging Divider Market

Rapid Adoption of Automated, Right-Sized On-Demand Partition Systems

The packaging divider market is undergoing a major transformation with the shift toward automated, on-demand partitioning systems. E-commerce and 3PL providers, managing high order complexity and diverse product dimensions, are increasingly investing in automation platforms that design and manufacture customized dividers in real time. This eliminates the inefficiencies of pre-manufactured, generic inventories while reducing packaging waste. Automation systems now integrate robotics, AI-driven software, and high-speed corrugated cutting technology to produce right-sized boxes and partitions for single or multi-SKU orders, significantly minimizing void fill and protecting products with precision-fit solutions. Capital inflows into automation are accelerating this trend, with providers developing turnkey solutions capable of handling packaging requirements across consumer electronics, retail goods, and industrial components. By reducing material use and optimizing fulfillment efficiency, automated partitioning is emerging as a cost-saving, sustainability-driven innovation that aligns with the growth of omnichannel and direct-to-consumer supply chains.

Regulatory and Consumer Pressure Driving Shift to 100% Recycled and Plastic-Free Divider Materials

Global regulatory and market forces are compelling companies to abandon plastics in divider manufacturing, replacing them with recycled paperboard, corrugated cardboard, and molded fiber alternatives. The European Union’s Plastic Levy, in place since January 2021, imposes a €0.80/kg charge on non-recycled plastic packaging waste, directly incentivizing brands to adopt curbside recyclable divider formats. Similarly, in the U.S., states like California and Washington are enforcing escalating PCR content mandates, reaching 50% by 2030, underscoring a broader push toward circular packaging models. Parallel to regulation, ESG commitments and consumer preferences are accelerating the move toward fiber-based and plastic-free dividers, particularly in food, e-commerce, and electronics packaging. Molded fiber dividers—produced from bagasse, recycled paper, or other natural fibers—are gaining traction for being biodegradable and cost-competitive, offering companies an environmentally responsible way to meet both legislative mandates and consumer expectations for sustainable packaging.

Development of High-Performance Molded Fiber Composites for Heavy/Industrial Goods

A key opportunity lies in the development of molded fiber composites with superior strength-to-weight ratios, enabling dividers to penetrate heavy-duty applications such as automotive, aerospace, and industrial equipment packaging. Current molded fiber solutions are primarily used for lightweight consumer goods, but advanced processing methods such as additive manufacturing-compression molding (AM-CM) are producing fiber composites with 35% higher tensile modulus compared to conventional molding techniques. These enhanced materials can compete with wood, foam, and plastics, offering lightweight yet durable protection for sensitive, high-value industrial goods. In sectors like automotive and electronics, where weight reduction is linked to lower logistics costs and improved sustainability, next-generation molded fiber dividers present both functional and ecological advantages. This opportunity is further reinforced by industry interest in carbon and glass fiber-reinforced composites, signaling a strong appetite for innovative, high-performance packaging substrates that align with industrial sustainability targets.

Integration of Smart and Connected Dividers for Asset Tracking and Authentication

The convergence of IoT and packaging introduces a high-value opportunity for dividers to evolve beyond protection into connected platforms for supply chain intelligence and brand protection. By embedding RFID tags, NFC chips, or serialized QR codes directly into paperboard or molded fiber dividers, companies can create smart partitions that deliver real-time asset tracking, interactive unboxing, and consumer authentication. Studies on RFID integration in logistics show improvements in inventory accuracy and shipment visibility, helping prevent losses and misrouting. For premium sectors such as luxury goods, consumer electronics, and pharmaceuticals, dividers enhanced with serialized QR codes provide an anti-counterfeiting mechanism, enabling consumers to verify authenticity instantly via mobile scan. This innovation elevates dividers from commodity packaging to data-rich, value-adding components, creating new revenue opportunities for packaging suppliers while aligning with digital transformation trends in global supply chains.

Competitive Landscape: Leading Players Shaping the Packaging Divider Market

The global packaging divider market is dominated by key players leveraging materials expertise, sustainable practices, and innovative design to deliver high-performance solutions for industrial, consumer, and food packaging applications.

Smurfit WestRock Leads with Integrated, Sustainable Divider Solutions

Smurfit WestRock, formed through the merger of Smurfit Kappa and WestRock in November 2024, is a global leader in paper-based packaging. The company’s vertically integrated model ensures a consistent supply of high-quality materials for corrugated, solid board, and molded pulp dividers. Key offerings include Lokfast partitions in the UK market. Its strategy focuses on circular business models, sustainable materials, and global scale to deliver innovative packaging solutions.

Mondi Group Focuses on Sustainable Paper-Based Dividers

Mondi is recognized for its sustainable packaging and paper solutions, with a strong presence in the divider market. In May 2025, Mondi commissioned a new €400 million paper machine at Štětí, enhancing its eco-friendly product portfolio. Recent innovations include paper-based stand-up pouches in collaboration with Proquimia. Key offerings include corrugated dividers for e-commerce and industrial applications, supported by the Mondi Action Plan 2030 (MAP2030) for circular-driven, recyclable solutions.

International Paper Expands Divider Portfolio Through Strategic Acquisition

International Paper is a leader in fiber-based packaging, providing a wide range of corrugated dividers and inserts for industrial and consumer goods. The April 2025 acquisition of DS Smith expanded its offerings in Europe and North America. The company’s products protect fragile goods and enhance e-commerce shipping efficiency. International Paper focuses on sustainability, operational excellence, and innovative fiber-based solutions aligned with its Vision 2030 goals.

Dordan Manufacturing Co. Specializes in Custom Thermoformed Dividers

Dordan Manufacturing, a US-based family-owned company, excels in precision-engineered, custom thermoformed dividers. Its vertically integrated process includes in-house design, tooling, and manufacturing, enabling rapid prototyping. In January 2025, Dordan emphasized its ISO 9001:2015 and ISO 13485:2016 certifications. Key offerings include custom insert trays for medical, automotive, and electronics industries, ensuring product safety during transport.

Sonoco Products Company Delivers Protective and Temperature-Assurance Solutions

Sonoco provides a diverse portfolio of protective packaging products, including dividers and inserts for temperature-sensitive applications. In April 2025, it divested its thermoformed and flexible packaging business to Toppan Holdings, optimizing its portfolio. The company’s offerings include insulated shippers and temperature-controlled containers, designed for healthcare and industrial logistics. Sonoco focuses on sustainable, high-performance solutions to meet evolving customer needs.

Packaging Divider Market Share Insights

Consumer Electronics Lead Market Share by Application in Packaging Dividers

Consumer electronics command the largest share at 30% of the packaging divider industry in 2025, reflecting the premium placed on protection, precision, and brand presentation for high-value devices such as smartphones, laptops, and wearables. Dividers in this segment are engineered from molded pulp, foams, and corrugated board to deliver shock absorption, ESD protection, and an elevated unboxing experience, which is increasingly used as a branding tool by global electronics leaders. Food and beverages (25%) follow closely, with dividers used extensively in glass bottle transport for wines, spirits, and premium beverages, as well as in multi-pack formats for retail. The sustainability trend is catalyzing a shift to molded pulp and recycled board solutions, replacing plastic inserts without compromising protection. Automotive and industrial goods (15%) utilize heavy-duty dividers designed for reusability and durability, safeguarding parts and components across extended logistics chains. Healthcare and pharmaceuticals (12%) represent a high-specification segment where dividers must meet cleanroom, sterility, and regulatory requirements for packaging syringes, vials, and diagnostics. Glass and ceramics (10%) maintain steady demand, with dividers ensuring safe shipment of fragile consumer and laboratory products. Personal care and cosmetics (8%) represent a niche but premium application, where luxury dividers enhance aesthetics and reinforce brand equity in gift sets and retail displays. This distribution underscores how consumer electronics and food & beverage drive scale, while healthcare and cosmetics maintain value-added demand for premium and regulated divider solutions.

E-commerce & Logistics Drive Market Share by End-User in Packaging Dividers

E-commerce and logistics providers dominate end-user demand for packaging dividers with a 35% share in 2025, reflecting the sector’s explosive growth fueled by omnichannel retail and direct-to-consumer shipping. Dividers are essential in this channel to minimize product damage, reduce return rates, and optimize shipping costs, particularly for multi-item orders. Electronics manufacturers (25%) form the second-largest end-user base, where global brands invest in custom-engineered divider systems that enhance both protection and luxury brand perception while meeting corporate sustainability commitments. Food and beverage companies (20%) continue to drive large-scale adoption, particularly in wine, spirits, and premium food packaging, where dividers are essential for breakage prevention and sustainable brand positioning. Retailers (12%) are important specifiers of divider packaging, balancing cost efficiency for bulk shipping with aesthetics for in-store displays, particularly in luxury retail. Automotive manufacturers (8%) round out the end-user base, relying on durable, reusable dividers in just-in-time supply chains for components and aftermarket parts. Collectively, this segmentation highlights how e-commerce anchors volume demand, while electronics and food & beverage drive specialized, value-added innovations in divider packaging solutions.

United States: Automation-Ready and Eco-Friendly Packaging Dividers Gain Momentum

The U.S. packaging divider market is being reshaped by a complex regulatory environment and rapid technological adoption. New 2025 laws in Delaware and New York banning single-use plastic rings and polystyrene foam containers have forced companies to pivot toward eco-friendly divider materials. In addition, state-level sustainability mandates are accelerating the replacement of traditional plastics with recyclable and biodegradable solutions, reinforcing the U.S. role as a pioneer in sustainable protective packaging.

Technological advancements are driving this shift, as consumer packaged goods (CPG) companies embrace robotics and automation to streamline packaging processes. Some firms report up to an 85% reduction in line labor after adopting automated systems, creating strong demand for dividers that are durable, lightweight, and compatible with smart packaging lines. With e-commerce booming and healthy snacks and fortified smoothies emerging as the fastest-growing segments, U.S. brands are also investing in innovation labs to design stackable, mess-free, and durable dividers that protect products during shipping and enhance convenience for on-the-go consumers.

Germany: Circular Economy Regulations Strengthen Demand for Sustainable Packaging Dividers

Germany is setting the pace in the European packaging divider market, thanks to stringent sustainability regulations and advanced innovation ecosystems. The EU’s Packaging and Packaging Waste Regulation (PPWR), combined with updates to the German Packaging Act (VerpackG) in 2025, requires higher recyclability standards and increased recycled content in all packaging materials. These rules are compelling companies to rethink divider design, shifting toward modular, recyclable, and resource-saving solutions.

The country’s strong innovation culture is also evident, as the German Packaging Institute (dvi) highlighted sustainable divider solutions at the German Packaging Award 2025, showcasing lightweight designs and new material applications. Supported by one of the world’s most robust recycling infrastructures, Germany is a leader in the circular economy, particularly in producing ultra-light dividers for food, pharmaceutical, and automotive packaging. These dividers play a vital role in protecting fragile goods from glass bottles to heavy automotive components ensuring both safety and sustainability in transit.

China: Express Delivery Boom Fuels Surging Demand for Automation-Ready Packaging Dividers

China’s packaging divider market is expanding at an unprecedented pace, fueled by government initiatives, e-commerce growth, and rising consumer expectations. The government’s dual-carbon goals—carbon peak by 2030 and neutrality by 2060 are reshaping packaging standards, while new express delivery regulations effective in June 2025 mandate degradable and reusable packaging materials. With 175 billion parcel deliveries in 2024 alone, demand for strong, automation-ready dividers has reached record levels.

Chinese manufacturers are heavily investing in automation and AI-driven quality control systems to scale production and meet sustainability mandates. Leading companies, including Amcor, are setting up intelligent facilities such as its new Huizhou plant, designed to produce advanced, eco-friendly packaging solutions tailored for food processing and e-commerce. The rapid rise of consumer electronics and online retail has further accelerated demand for high-quality protective dividers, solidifying China’s role as a global leader in next-generation protective packaging solutions.

India: Circular Economy Policies and E-Commerce Growth Boost Packaging Divider Adoption

India’s packaging divider market is rapidly gaining traction, driven by government initiatives and a surging e-commerce ecosystem. The “Make in India” program and the Production Linked Incentive (PLI) scheme are incentivizing domestic production of sustainable packaging, while new Extended Producer Responsibility (EPR) guidelines are forcing companies to adopt recyclable and circular materials. These efforts align with India’s broader goal of transitioning toward a circular economy, creating fertile ground for the adoption of eco-friendly packaging dividers.

The growing penetration of online retail and food delivery services has made durable dividers essential for corrugated boxes, RTD teas, sports drinks, and packaged juices, which require added protection during shipping. At the same time, corporate initiatives like the Huhtamaki Foundation’s “CloseTheLoop” recycling plants are addressing post-consumer plastic waste and expanding recycling infrastructure. With e-commerce, food processing, and beverage industries expanding rapidly, India has emerged as a dynamic growth hub for divider technologies that balance cost-effectiveness, durability, and sustainability.

Japan: High-Quality Divider Innovations Align with Sustainability and Design Excellence

Japan’s packaging divider industry is being transformed by stringent regulations and a strong cultural emphasis on design and quality. The June 2025 implementation of new packaging rules introduced a “positive list” for approved synthetic materials, encouraging manufacturers to shift toward paper-based dividers with safe, certified coatings. These regulations, coupled with national sustainability goals, are steering companies toward eco-friendly, durable, and visually appealing divider solutions.

Technological innovation underpins Japan’s progress, with firms like Nippon Paper Industries developing SHIELDPLUS®, a paper-based barrier material that enhances oxygen and flavor protection, complementing advanced divider designs. Sustainability remains central, with companies such as Suntory advancing their “2R+B” strategy (Reduce, Recycle + Bio) to achieve 100% sustainable PET packaging by 2030, influencing the broader packaging ecosystem. The market is particularly strong in ready-to-drink teas, coffees, and snacks, where lightweight, functional, and design-driven dividers enhance both product protection and consumer appeal.

Brazil: Regulatory Shifts and Bio-Based Materials Drive Next-Gen Packaging Divider Market

Brazil’s packaging divider market is evolving rapidly under new regulations and sustainability-driven initiatives. The National Solid Waste Policy (PNRS) and oversight by the National Health Surveillance Agency (Anvisa) are reinforcing sustainable practices, while 2025 regulations mandate shared responsibility between manufacturers and consumers for product lifecycle management. Upcoming decrees requiring companies to recycle up to 50% of their products will directly impact divider design, pushing innovation in recyclable and reusable materials.

Technological advancements are also shaping the market, with manufacturers increasingly turning to bio-based materials such as sugarcane bagasse and corn starch for dividers. A recent breakthrough came from Klabin, in collaboration with Optima and Soulpack, which launched a 100% recyclable paper bag for diaper packaging—demonstrating how sustainability-focused innovations are redefining protective packaging. The food and beverage sector dominates Brazil’s divider demand, particularly in canned goods, where reliable protective dividers and barrier coatings are crucial for preventing damage during transport and storage.

Packaging Divider Market Report Scope

Packaging Divider Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.6 Billion

|

|

Market Size (2034)

|

$2.6 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Material Type (Corrugated Cardboard, Plastic, Molded Pulp, Foam, Others), By Application (Food & Beverage, Consumer Electronics, Automotive & Industrial Goods, Healthcare & Pharmaceutical, Personal Care & Cosmetics, Glass & Ceramics), By End-User (Food & Beverage Companies, Electronics Manufacturers, Automotive Manufacturers, Retailers, E-commerce & Logistics), By Product Type (Partitions, Inserts, Separators, Die-Cut Dividers)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, WestRock Company, Smurfit Kappa Group Plc, DS Smith Plc, Graphic Packaging Holding Company, International Paper Company, Sonoco Products Company, Mondi Group, Huhtamaki Oyj, Berry Global Inc., Billerud AB, Rengo Co., Ltd., Sealed Air Corporation, Ball Corporation, Crown Holdings, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Divider Market Segmentation

By Material Type

- Corrugated Cardboard

- Plastic

- Molded Pulp

- Foam

- Others

By Application

- Food & Beverage

- Consumer Electronics

- Automotive & Industrial Goods

- Healthcare & Pharmaceutical

- Personal Care & Cosmetics

- Glass & Ceramics

By End-User

- Food & Beverage Companies

- Electronics Manufacturers

- Automotive Manufacturers

- Retailers

- E-commerce & Logistics

By Product Type

- Partitions

- Inserts

- Separators

- Die-Cut Dividers

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Divider Market

- Amcor plc

- WestRock Company

- Smurfit Kappa Group Plc

- DS Smith Plc

- Graphic Packaging Holding Company

- International Paper Company

- Sonoco Products Company

- Mondi Group

- Huhtamaki Oyj

- Berry Global Inc.

- Billerud AB

- Rengo Co., Ltd.

- Sealed Air Corporation

- Ball Corporation

- Crown Holdings, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a robust and multi-faceted research methodology to deliver in-depth insights into the global packaging divider market. The approach integrates primary research, secondary data analysis, and advanced modeling techniques. Primary research involves consultations with packaging engineers, supply chain managers, materials scientists, and sustainability experts across leading companies such as Amcor, Smurfit WestRock, and International Paper. Secondary research sources include regulatory frameworks like the EU Packaging and Packaging Waste Regulation (PPWR), U.S. state-level plastic bans, and national circular economy policies in China, India, and Brazil, alongside press releases detailing mergers, acquisitions, and technological innovations. Market sizing and forecasts are derived from historical growth trends, material adoption patterns, and technological advancements in corrugated, molded pulp, foam, and plastic dividers. USDAnalytics also evaluates emerging trends in automation, on-demand partition systems, and smart dividers with RFID or QR code integration, as well as sustainability shifts toward 100% recycled and plastic-free solutions. Competitive landscape analysis highlights global leaders’ strategic initiatives in R&D, operational efficiency, and sustainable product development, offering industry professionals actionable insights for market expansion, product innovation, and supply chain optimization.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.