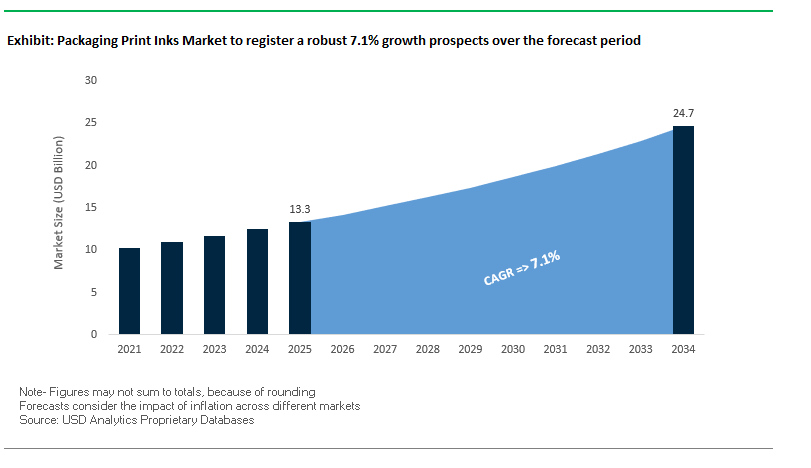

Packaging Print Inks Market Poised to Reach $24.7 Billion by 2034 Driven by Sustainability and Digital Printing

The Global Packaging Print Inks Market is projected to grow from $13.3 billion in 2025 to $24.7 billion by 2034, registering a CAGR of 7.1%. This growth is propelled by rising demand for low-migration, food-safe inks, regulatory compliance, and the shift toward eco-friendly and high-performance ink technologies. Packaging inks are no longer limited to coloring—they are crucial for brand differentiation, high-fidelity graphics, functional coatings, and product safety.

Key Insights for Industry Professionals:

- Regulatory Compliance Driving Demand: Increasing adoption of food-safe, low-migration inks ensures consumer safety and meets strict standards in food, beverage, and pharmaceutical packaging.

- Sustainability and Eco-Friendly Solutions: Growth in water-based, UV/EB-cured, and bio-renewable inks reduces VOC emissions and aligns with circular economy initiatives.

- High-Fidelity Printing for Premium Packaging: Superior color gamut, gloss, and tactile effects enhance brand visibility and create memorable unboxing experiences.

- Digital Printing Integration: Adoption of inkjet and digital technologies enables shorter print runs, mass customization, and faster time-to-market, transforming supply chain management.

- Functional Coatings and Advanced Properties: Specialty inks now provide durability, light fastness, and security features that extend product lifecycle and enhance packaging functionality.

The market outlook demonstrates a strong emphasis on innovation, regulatory compliance, and sustainable printing solutions, positioning packaging inks as a critical enabler of modern packaging design and brand strategy.

Strategic Developments and Technology Adoption Shaping the Packaging Print Inks Industry

The Packaging Print Inks Industry continues to evolve rapidly, with strategic acquisitions, product launches, and technological innovations driving market transformation. In September 2025, Siegwerk showcased its circular packaging innovations in Mumbai, highlighting expanded coating expertise following its acquisition of Allinova. This acquisition, completed in August 2025, strengthens Siegwerk’s position in functional coatings and sustainable packaging solutions.

In August 2025, Flint Group highlighted its advanced ink and coating portfolio at Labelexpo Europe, showcasing Flexocure® LEAP, a UV flexo ink system designed for superior performance. During July 2025, Sun Chemical launched SunCure Advance ECO UV inks for folding cartons, containing 25–30% bio-renewable content, certified by the American Soybean Association. That same month, Hubergroup introduced its HYDRO-X CONTACT water-based inks for direct food contact, further emphasizing safety and sustainability.

Additional moves include Hubergroup’s new mixing station in Sainte-Sigolène, France (June 2025) to improve regional responsiveness, and Dynamic Dies’ expansion in Indianapolis (March 2025) to enhance production for packaging dies and printing applications.

Trends and Opportunities Transforming the Packaging Print Inks Market

Accelerated Regulatory Phase-Out of Per- and Polyfluoroalkyl Substances (PFAS)

The packaging print inks market is undergoing a regulatory-driven transformation as PFAS, long relied upon for their oil- and water-resistant properties, face global restrictions. In the U.S., states including California, Colorado, and Vermont banned intentionally added PFAS in food packaging from January 2024, while additional bans in Minnesota and other states will take effect in 2025. These laws create an immediate compliance requirement for ink and coating suppliers.

At the European level, the EU Packaging and Packaging Waste Regulation (PPWR), adopted in December 2024, enforces a ban on food packaging containing PFAS above set thresholds, effective by late 2026. The regulation underscores Europe’s commitment to a toxic-free circular economy, pushing the entire value chain to reformulate inks and coatings.

The supply chain is already responding. Clariant’s June 2025 launch of PFAS-free polymer processing aids illustrates how chemical manufacturers are proactively replacing hazardous chemistries ahead of legislative deadlines. At the same time, the U.S. EPA’s revised chemical review process under TSCA, requiring deeper assessments of persistent, bioaccumulative, and toxic substances, is accelerating innovation toward safer ink chemistries. These converging factors are not only regulatory obligations but also competitive differentiators, forcing brands to adopt PFAS-free packaging inks to meet both compliance and consumer expectations.

Rapid Adoption of UV-LED Curable Inks for Operational Efficiency

The second dominant trend is the shift to UV-LED curable inks, driven by cost efficiency, sustainability, and high-performance printing capabilities. UV-LED curing consumes 60–65% less energy than conventional mercury vapor lamps, directly lowering electricity costs and carbon footprints. The technology also eliminates VOC emissions and ozone generation, making it attractive for printers operating under strict environmental standards.

Performance benefits are equally compelling. Low heat emission allows UV-LED inks to be applied on heat-sensitive substrates such as thin flexible films, a critical advantage for packaging converters in food, beverage, and personal care industries. The technology also delivers faster curing speeds and sharper print quality, enabling higher production throughput.

Technology providers are accelerating adoption with new product launches. At China Print 2025, HP Indigo introduced the 120K HD press, designed for high-volume digital packaging with AI-driven print management. The machine is compatible with a broad range of specialty inks, including invisible and fade-resistant types, underscoring how UV-LED curing systems have matured into a mainstream technology that combines sustainability with productivity.

Development of High-Performance Bio-Based Inks and Varnishes

A significant growth opportunity lies in the commercialization of bio-based inks that balance sustainability with high performance. Governments are tightening VOC restrictions, and consumer demand for renewable packaging solutions is growing, fueling R&D into inks derived from vegetable oils, algae biomass, and bacterial fermentation.

Performance parity with petroleum-based inks is now within reach. Academic studies show that bio-based pigments can achieve excellent light and wash fastness, making them suitable even for high-performance packaging and textile applications. Companies are investing heavily in bio-based alternatives, supported by partnerships to secure renewable raw materials at scale. For example, algae-derived black pigments and soy protein-based inks are being engineered to meet durability and color vibrancy requirements for packaging.

Beyond sustainability, the key advantage of these inks lies in their end-of-life compatibility. Bio-based inks and varnishes are compostable and recyclable, ensuring they do not contaminate fiber recycling or organic waste streams. This dual benefit—regulatory compliance and environmental alignment—makes bio-based inks an attractive solution for converters and brands aiming to meet EPR-driven recyclability mandates.

Integration of Functional and Smart Inks for Brand Protection and Engagement

The second major opportunity for the market is the integration of functional and smart inks that transform packaging from passive to interactive. Counterfeiting remains a major challenge, and invisible fluorescent or phosphorescent inks provide an effective anti-counterfeiting layer by revealing hidden identifiers under UV light. This technology is particularly valuable in pharmaceuticals, luxury goods, and premium food packaging.

Smart inks also enable real-time quality monitoring. For instance, thermochromic inks can visually indicate when a perishable product has been exposed to unsafe temperatures, enhancing food safety and reducing waste. In pharmaceuticals, these inks ensure cold-chain compliance for sensitive medicines.

Leading Packaging Print Ink Companies Driving Sustainability, Innovation, and Global Reach

The Packaging Print Inks Market is shaped by key players leveraging materials science, R&D, and sustainability programs to deliver high-performance solutions across packaging applications. These companies are expanding globally, adopting digital printing, and creating eco-conscious ink portfolios to meet evolving customer and regulatory demands.

Siegwerk: Advancing Circular Packaging Solutions with Functional Coatings

Siegwerk Druckfarben AG & Co. KGaA is a global leader in printing inks and coatings for packaging and labels, recognized for its expertise in product safety and sustainability through its HorizonNOW program. In August 2025, Siegwerk acquired Allinova to enhance functional coating capabilities. Its portfolio includes water-based, solvent-based, and UV-curing inks, with a focus on low-migration solutions for food packaging. Siegwerk aims to enable circular packaging innovations, mono-material solutions, and reduced environmental impact.

Sun Chemical: Innovating Eco-Friendly and High-Performance Ink Solutions

Sun Chemical Corporation, part of the DIC Group, provides a wide range of packaging and graphic solutions, pigments, and specialty coatings. In July 2025, Sun Chemical launched SunCure Advance ECO UV inks with bio-renewable content for folding cartons and showcased advanced color and effect pigments at ABRAFATI 2025. Its offerings include lithographic, flexographic, gravure, digital inks, adhesives, and coatings, with a strong focus on sustainability and performance.

Flint Group: Delivering Advanced Inks and Coatings to Meet Tomorrow’s Packaging Challenges

Flint Group is a global supplier of inks and coatings for printing and packaging, known for its diverse product portfolio and worldwide reach. In August 2025, it showcased Flexocure® LEAP UV flexo inks at Labelexpo Europe, demonstrating commitment to performance and sustainability. Flint provides solutions for flexo, gravure, offset, and packaging applications, along with coatings and pressroom consumables, helping customers enhance efficiency, reduce costs, and meet environmental targets.

Hubergroup: Pioneering Water-Based Inks for Direct Food Contact Applications

Hubergroup specializes in printing inks and specialty chemicals, emphasizing product safety and sustainable solutions. In July 2025, it launched the HYDRO-X CONTACT system, offering water-based inks and varnishes suitable for direct food contact, and opened a new mixing station in France (June 2025). Hubergroup’s portfolio spans sheetfed offset, web offset, flexographic, and gravure inks, focusing on innovation, efficiency, and global service expansion.

Sakata INX Corporation: Expanding Packaging Ink Solutions Through Innovation and Sustainability

Sakata INX Corporation provides a wide range of printing inks and functional materials, supporting traditional and digital printing technologies. In August 2025, the company expanded its packaging ink operations in Brazil and the Philippines, while publishing its SAKATA INX VISION 2030 strategic plan emphasizing innovation, sustainability, and global growth. Its offerings include gravure, flexo, offset, and energy-curable inks, along with functional coatings, supporting sustainable packaging and diverse market applications.

Packaging Print Inks Market Share Insights, 2025-2034

Flexographic Printing Holds Largest Market Share by Technology in the Packaging Print Inks Industry

Flexographic printing inks account for 45% of the packaging print inks market, confirming flexo as the workhorse technology for modern packaging. Its dominance comes from its ability to print on diverse substrates corrugated boards, flexible films, and paper—with high speed, cost efficiency, and adaptability for long and medium runs. Continuous improvements in water-based and UV-curable flexo inks have significantly elevated print quality, making flexo competitive with offset and gravure in many applications while also aligning with environmental compliance standards. Rotogravure maintains a strong role in high-definition, long-run flexible packaging like confectionery and snacks, while digital printing is reshaping short-run, personalized packaging with variable data printing. Lithographic printing remains relevant for cartons and labels but is gradually losing share. The trajectory clearly highlights flexography’s strategic advantage as brands demand sustainable inks, reduced lead times, and print processes compatible with recyclable and bio-based substrates, making it the central technology in packaging inks.

Food & Beverage Industry Commands Majority Market Share by End-Use in Packaging Print Inks

The food and beverage sector accounts for 55% of global demand for packaging print inks, making it the single most influential application. The dominance of this segment stems from the massive volume of flexible films, folding cartons, and labels required for processed foods, beverages, frozen products, and snacks. A defining factor in this market is the strict regulatory requirement for low-migration inks that prevent harmful substances from transferring into consumables, forcing innovation in water-based, radiation-curable, and bio-based ink systems. Consumer goods, pharmaceuticals, and cosmetics also drive specialized demand—pharmaceuticals for anti-counterfeiting inks and sterilization-resistant formulations, cosmetics for aesthetic metallic and pearlescent inks, and consumer goods for durable, high-opacity solutions on plastics and rigid packaging. Nevertheless, the scale, regulatory stringency, and constant innovation pressure in food and beverage packaging ensure that this sector remains the anchor of demand, shaping the direction of R&D and capital investment in the packaging print inks market.

United States Packaging Print Inks Market Shaped by Low-VOC Regulations and FDA Food-Safety Standards

The United States packaging print inks market is being shaped by a growing preference for environmentally friendly, biodegradable, and water-based inks. State-level environmental regulations, combined with consumer demand for low-VOC and recyclable formulations, are forcing ink producers to innovate rapidly. The Food and Drug Administration (FDA) continues to enforce strict food-contact ink standards, emphasizing low-migration formulations to prevent contamination in packaged food and beverages.

Technology adoption is another key driver, with UV-curable and UV LED inks gaining popularity due to faster curing times, durability, and reduced waste. The rapid expansion of digital printing in packaging is also transforming the sector, offering customization, shorter runs, and sustainable production with lower resource use. Key demand comes from e-commerce packaging, particularly corrugated boxes requiring high-quality branding, and the food and beverage sector, where safe, durable, and regulation-compliant inks are indispensable.

Germany Packaging Print Inks Market Strengthened by PPWR Regulations and Eco-Friendly Formulations

Germany’s packaging print inks market is tightly governed by the EU Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025. These rules demand high recyclability, reuse, and restrictions on single-use plastics, directly impacting the types of inks used in packaging papers and plastics. The German Printing Inks Industry Association (VdD) plays a central role, offering compliance guidance and supporting innovation aligned with EU standards.

The market is experiencing a surge in eco-friendly ink solutions, such as bio-based coatings from PLA, PHA, cellulose, and vegetable oils, alongside water-based and UV-curable inks that significantly cut VOC emissions. Germany’s strong recycling infrastructure and industry-wide focus on sustainability position it as a leader in green packaging print inks for food, beverage, and cosmetics packaging. The demand for inks compatible with bioplastics and recycled papers reflects the country’s push toward circular economy practices.

China Packaging Print Inks Market Driven by Dual-Carbon Targets and Stricter Food-Contact Standards

The packaging print inks market in China is undergoing a regulatory transformation. The government’s dual-carbon targets, aimed at carbon peaking by 2030 and neutrality by 2060, are encouraging the use of sustainable and low-emission ink formulations. In March 2025, the GB 4806.14-2023 standard for food-contact inks took effect, followed by the July 2025 draft amendment to GB 9685, which bans high-risk substances such as PFAS and certain phthalates. These stricter regulations are reshaping ink production, forcing manufacturers to reformulate for compliance and safety.

On the innovation front, automation and AI integration in printing lines are boosting efficiency, precision, and quality control. The government is also pushing for smart regulatory tools and traceability platforms, especially critical in the food sector. China’s consumer goods, e-commerce, and electronics industries—backed by record parcel deliveries—are the main growth drivers, fueling unprecedented demand for high-quality, safe, and efficient packaging print inks.

India Packaging Print Inks Market Expanded by PLI Incentives and Foreign Direct Investments

India’s packaging print inks market is being strengthened by the government’s Make in India initiative and the Production Linked Incentive (PLI) scheme, both aimed at boosting domestic manufacturing. These policies are creating a favorable environment for investments in the packaging sector. A major development was Siegwerk’s INR 350 crore ($42 million) investment announced in 2024, which will expand advanced ink production and scale its Global Innovation and Capability Center (GICC) in India.

The market is seeing rising adoption of automation, robotics, and AI-enabled packaging lines, which enhance efficiency and reduce error rates in printing processes. Digital printing is gaining traction for customized FMCG packaging, short-run jobs, and rapid product launches, particularly in the food and beverage sector. India’s growing e-commerce ecosystem and strong demand for safe, flexible, and recyclable packaging inks in food and beverage applications position it as one of the fastest-growing packaging print inks markets globally.

Japan Packaging Print Inks Market Advanced by Positive List Regulation and Eco-Friendly Innovations

Japan’s packaging print inks market is evolving under the positive list system for food-contact materials, effective June 2025, which restricts unapproved chemicals in inks for food packaging. This regulation is pushing manufacturers toward low-toxicity, compliant, and food-safe formulations. The adoption of e-labeling and QR codes in packaging is further enhancing transparency, requiring specialized inks compatible with new labeling technologies.

Japanese companies are global leaders in high-quality and sustainable ink development. For example, Nippon Paper Industries and Stora Enso are introducing paper-based barrier packaging formats that require advanced, recyclable ink formulations. Sustainability goals also play a major role: Japan’s plan to reduce GHG emissions by 46% by 2030 and achieve net zero by 2050 is driving innovation in bio-based, recyclable, and UV-curable inks. Strong demand comes from the ready-to-drink tea, coffee, and snack packaging sectors, where aesthetic, lightweight, and environmentally friendly packaging print inks are highly valued.

Brazil Packaging Print Inks Market Reinforced by Anvisa RDC No. 983/2025 and Circular Economy Push

Brazil’s packaging print inks market is defined by new regulatory oversight. The National Health Surveillance Agency (Anvisa) approved RDC No. 983/2025 in August 2025, phasing out specific substances in food and beverage packaging inks. This aligns with Brazil’s National Solid Waste Policy (PNRS) and Conasq’s updated register of regulated chemicals, pushing manufacturers toward safer, sustainable formulations.

The industry is advancing with sustainable printing technologies, including inks aligned with international food-safety standards and compatible with biodegradable and recyclable substrates. Corporate investment is rising to comply with these new requirements, with manufacturers adopting eco-friendly practices to maintain competitiveness. The food and beverage industry, particularly canned goods and processed foods, is the largest consumer of packaging inks in Brazil, creating high demand for safe, durable, and compliant print inks that balance performance with sustainability.

Packaging Print Inks Market Report Scope

Packaging Print Inks Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.3 Billion

|

|

Market Size (2034)

|

$24.7 Billion

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Ink Type (Water-based, Solvent-based, UV-curable, Oil-based, Others), By Printing Technology (Flexographic, Rotogravure, Lithographic, Digital, Others), By Application (Flexible Packaging, Rigid Packaging, Labels, Corrugated Boxes, Others), By End-Use Industry (Food & Beverage, Personal Care & Cosmetics, Pharmaceutical & Healthcare, Consumer Goods, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DIC Corporation (Sun Chemical), Siegwerk Druckfarben AG & Co. KGaA, Flint Group, Hubergroup, Sakata INX Corporation, Toyo Ink SC Holdings Co., Ltd., Fujifilm Holdings Corporation, T&K Toka Co., Ltd., Wikoff Color Corporation, Zeller+Gmelin GmbH & Co. KG, Siegwerk India Region, Marabu GmbH & Co. KG, SICPA Holding SA, Altana AG, AkzoNobel N.V.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Print Inks Market Segmentation

By Ink Type

- Water-based

- Solvent-based

- UV-curable

- Oil-based

- Others

By Printing Technology

- Flexographic

- Rotogravure

- Lithographic

- Digital

- Others

By Application

- Flexible Packaging

- Rigid Packaging

- Labels

- Corrugated Boxes

- Others

By End-Use Industry

- Food & Beverage

- Personal Care & Cosmetics

- Pharmaceutical & Healthcare

- Consumer Goods

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Print Inks Market

- DIC Corporation (Sun Chemical)

- Siegwerk Druckfarben AG & Co. KGaA

- Flint Group

- Hubergroup

- Sakata INX Corporation

- Toyo Ink SC Holdings Co., Ltd.

- Fujifilm Holdings Corporation

- T&K Toka Co., Ltd.

- Wikoff Color Corporation

- Zeller+Gmelin GmbH & Co. KG

- Siegwerk India Region

- Marabu GmbH & Co. KG

- SICPA Holding SA

- Altana AG

- AkzoNobel N.V.

* List Not Exhaustive

Methodology

The research methodology combines primary and secondary approaches to ensure data reliability and market accuracy for the Packaging Print Inks Market. Primary research involved interviews with industry executives, ink formulators, packaging engineers, sustainability specialists, and supply chain stakeholders across key regions including the U.S., Germany, China, India, Japan, and Brazil. Secondary research included analysis of corporate annual reports, regulatory databases, patents, sustainability disclosures, trade publications, and verified industry journals. Advanced data triangulation was applied to validate market sizing, revenue, and growth projections, integrating macroeconomic indicators, raw material cost trends, technological adoption patterns, and regulatory frameworks such as PFAS bans, PPWR, FDA food-contact standards, and Positive List regulations. Forecasts were developed using both top-down and bottom-up approaches, while regional insights were contextualized against policy shifts, consumer behavior, and e-commerce and F&B industry trends. This multi-layered methodology by USDAnalytics ensures accurate, fact-based insights and actionable intelligence for professionals seeking to understand market dynamics, technological evolution, and sustainability-driven transformations in the global Packaging Print Inks industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.