Packaging Sacks Market Poised to Reach $40.9 Billion by 2034 on Rising Demand for Sustainable and High-Performance Bulk Packaging

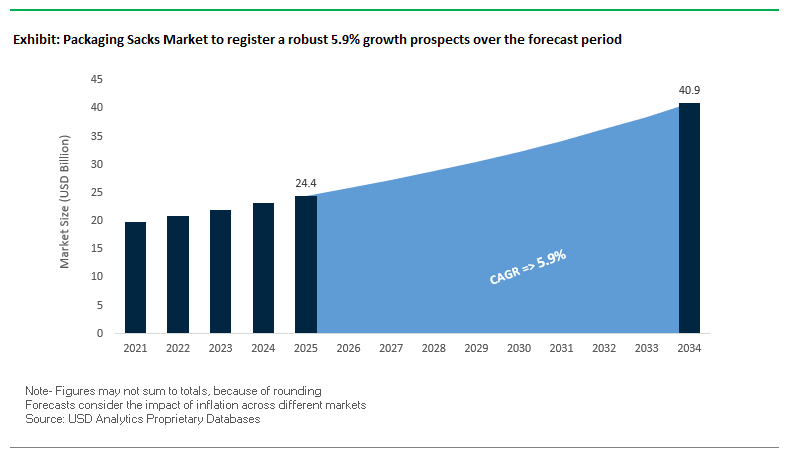

The Global Packaging Sacks Market is projected to grow from $24.4 billion in 2025 to $40.9 billion by 2034, reflecting a CAGR of 5.9%. The industry plays a crucial role in protecting, storing, and transporting bulk goods such as grains, seeds, cement, and chemicals. With evolving supply chain requirements, sustainability mandates, and material innovation, packaging sacks are moving beyond simple containers to functional, brandable, and eco-friendly solutions.

Key Insights for Industry Professionals:

- Moisture and Barrier Protection Remain Paramount: Advanced coatings and integrated films ensure product integrity for humidity-sensitive materials, extending shelf life and reducing spoilage.

- Sustainability Drives Innovation: There is a significant shift from multi-layer, non-recyclable sacks to monomaterial and PCR-based solutions, driven by corporate sustainability targets and regulatory compliance.

- Enhanced Functionality Boosts Supply Chain Efficiency: Features like easy-open designs, high-quality printability, and optimized palletizing shapes improve logistics efficiency and brand visibility.

- Automation Compatibility Is Shaping Design: Sacks are increasingly designed for high-speed automated filling and handling systems, enabling cost savings and productivity gains.

- Circular Economy Trends Influence Materials Choice: Companies are investing in recyclable, compostable, and low-carbon materials to align with sustainability expectations.

Recent Strategic Moves in the Packaging Sacks Industry Highlight Sustainability and Operational Efficiency

The Packaging Sacks Industry has seen dynamic developments in recent years, reflecting a focus on sustainable materials, market consolidation, and functional innovation. In August 2025, Greif, Inc. announced the sale of its timberlands and Containerboard Business, allowing the company to focus on core industrial packaging solutions. The same month, Smurfit WestRock plc closed several U.S. and German facilities, streamlining operations post-merger to optimize efficiency.

July 2025 saw Mondi collaborate with Saga Nutrition to launch a sustainable, paper-based pet food pouch, expanding paper-based solutions in niche segments. May 2025 highlighted ProAmpac’s commitment to sustainability and corporate social responsibility, recognizing employee contributions to safety and environmental initiatives.

Significant strategic acquisitions include International Paper completing its $9.9 billion purchase of DS Smith in April 2025, strengthening its European footprint in sustainable paper packaging. Earlier innovations include Billerud’s March 2025 launch of heat-sealable, recyclable paper and Mondi’s February 2025 re/cycle SpoutedPouch, showcasing the versatility of paper in replacing plastic.

Trends and Opportunities Reshaping the Packaging Sacks Market

Accelerated Adoption of High-Performance, Lightweight Multi-Layer Sacks

The packaging sacks market is undergoing a major shift toward lightweight, multi-layer structures that deliver both sustainability and efficiency benefits. A leading driver is the development of advanced resin formulations, such as the Exceed S performance polyethylene (PE) portfolio, which combines stiffness and toughness to create thinner yet stronger sacks. This innovation reduces raw material use while maintaining durability in demanding logistics conditions.

Lightweighting directly improves supply chain efficiency by reducing sack weight, allowing companies to ship more products per pallet or container. This optimization lowers freight costs, reduces fuel consumption, and cuts carbon emissions, making lightweight sacks a profitability and sustainability driver in logistics-heavy sectors such as chemicals, cement, fertilizers, and agriculture.

Importantly, performance has not been sacrificed. Next-generation sacks now incorporate ethylene vinyl alcohol (EVOH) barrier layers, protecting against oxygen and moisture to extend shelf life and preserve sensitive goods like food ingredients and specialty chemicals. To support these designs, manufacturers are investing in state-of-the-art extrusion technology. The rollout of 9-layer blown film lines reflects the industry’s strategic push to commercialize thinner, stronger, high-barrier sack structures at scale.

Regulatory and Consumer Pressure Driving Shift to Recyclable Mono-Material Sacks

Regulatory frameworks are also reshaping the market, with the European Union’s Packaging and Packaging Waste Regulation (PPWR) mandating design-for-recycling compliance from February 2025. Multi-material sacks—traditionally difficult to recycle—are being phased out in favor of mono-material polyethylene (PE) and polypropylene (PP) sacks that integrate seamlessly into recycling streams.

This shift is reinforced by corporate sustainability commitments. Major players such as Nestlé, Danone, and Kraft Heinz have pledged to ensure 100% of their packaging is recyclable or reusable by 2025, pushing sack manufacturers to accelerate mono-material adoption. Historically, performance challenges slowed this transition, as multi-layer laminates provided essential barrier protection. However, new engineered PE and PP resins now offer oxygen, moisture, and light resistance comparable to legacy multi-layer solutions, removing technical barriers to recyclability.

Together, regulatory compliance, consumer preference, and brand-level commitments to circularity are creating a strong, non-negotiable demand for recyclable mono-material sack solutions that support both environmental and operational goals.

Development of Bio-Based and Compostable Sacks for Agricultural Applications

Agriculture represents one of the largest and most challenging end-use segments for sacks, particularly due to the difficulty of recycling soiled sacks used for fertilizers, seeds, and soil. This creates a significant opportunity for bio-based and compostable sack solutions that align with farm-level waste management systems.

Certified compostable sacks made from cornstarch-based biopolymers have already been successfully deployed in large-scale applications, including school district composting programs. Extending this to agriculture provides a viable pathway to reduce landfill waste while aligning with global sustainability standards.

The next frontier lies in home-compostable solutions, which eliminate the need for industrial composting facilities. Research into novel biopolymer blends—particularly PLA-PHA composites—is focused on improving mechanical strength and enabling disintegration under wider environmental conditions. These innovations would provide farmers with a durable yet compostable alternative, offering both operational convenience and environmental benefits.

Integration of RFID and Smart Tracking into Bulk Sack Logistics

Digitalization is opening a new opportunity in sack packaging through the integration of RFID and smart tracking technologies. By embedding RFID tags into sacks, manufacturers and logistics providers gain real-time supply chain visibility, enabling the monitoring of bulk commodities such as grains, cement, and chemicals across global shipping networks.

This technology also supports automated inventory management, where hundreds of RFID-enabled sacks can be counted in seconds, eliminating manual scanning and improving warehouse efficiency. For high-value products like specialty chemicals or pharmaceuticals, RFID provides tamper-evidence and brand authentication, ensuring product origin traceability and protecting against counterfeiting.

Technology providers are advancing towards chipless RFID tags and compostable smart labels, ensuring digital solutions do not introduce new waste streams. The convergence of sustainability and digital traceability positions smart sacks as a critical enabler of the next-generation circular and transparent supply chain.

Competitive Landscape Shaped by Leaders Driving Sustainable, Functional, and High-Performance Packaging Sacks

The global packaging sacks market is dominated by a group of companies leveraging material science, innovation, and operational scale to provide durable, sustainable, and functional solutions. These players are driving circular economy adoption, advanced barrier solutions, and high-performance industrial packaging.

Smurfit WestRock: Leveraging Scale and Sustainability in Paper-Based Sacks

Smurfit WestRock is the product of the Smurfit Kappa and WestRock merger, combining expertise in vertically integrated paper sack production. In August 2025, it promoted FSC-certified recyclable open-mouth sacks, reinforcing its commitment to sustainability and post-merger efficiency. The company offers a wide range of paper sacks for industrial and food applications, featuring high-quality printing and customizable closure options, and focuses on circular business models and fiber-based replacements for plastic.

Mondi Group: Pioneering Functional and Eco-Friendly Industrial Paper Bags

Mondi is recognized for innovative paper bags and sustainable packaging solutions. In August 2025, it introduced the re/cycle PaperPlus Bag Advanced with a high-barrier film for humidity-sensitive products, while July 2024 saw the launch of water-soluble cement bags. Mondi’s portfolio includes pasted valve, pinch bottom, and open-mouth bags, as well as niche solutions like SolmixBag and EcoWicketBags. The company’s strategic focus is on developing reusable, recyclable, and compostable solutions for global packaging needs.

Billerud AB: Driving High-Performance Paper Sacks with Plastic-Free Innovations

Billerud AB specializes in virgin fiber-based, high-strength sack papers. In March 2025, it launched heat-sealable paper for low-carbon, recyclable alternatives to plastic, and in July 2022 introduced Performance White Barrier sack paper. Billerud’s offerings include DuoStrength and Conical Formable papers, designed for building materials, dry food, and animal feed. Its strategy emphasizes innovative, sustainable materials to reduce reliance on plastics in industrial packaging.

Greif, Inc.: Strengthening Core Industrial Packaging through Strategic Divestments

Greif is a leading provider of industrial packaging solutions, including paper sacks and containerboard. In August 2025, it divested timberlands and containerboard business to concentrate on core industrial packaging. Its portfolio includes fiber, steel, and plastic drums, with a focus on high-performance paper sacks. Greif’s strategic priority is operational excellence, customer service, and sustainable industrial packaging solutions.

ProAmpac: Expanding Paper-Based Solutions in Food and Industrial Applications

ProAmpac delivers flexible and paper-based packaging solutions with high customization and sustainability. In July 2025, it launched a recyclable-ready paper packaging solution for chunk cheese, highlighting the expansion of paper in food applications. Its offerings include multi-wall paper bags for pet food, lawn & garden, and agriculture, with printable, high-barrier, and functional features. ProAmpac focuses on innovation and circular economy initiatives to meet evolving brand and sustainability demands.

Packaging Sacks Market Share Insights, 2025-2034

Woven Sacks Dominate Market Share by Product Type in the Packaging Sacks Industry

Woven polypropylene (PP) sacks command 40% of the packaging sacks market, making them the most widely used format for bulk and heavy-duty applications. Their success is rooted in a superior strength-to-weight ratio, tear resistance, and moisture protection, which makes them indispensable for cement, fertilizers, grains, and animal feed. Unlike paper-based or sewn formats, woven sacks can withstand rough handling, stacking pressure, and outdoor storage, aligning with the operational needs of global construction and agriculture supply chains. Open-mouth and pasted-valve sacks maintain relevance for powder-based goods like flour and cement, but their use is often application-specific, depending on filling technology. Sewn and pinch-bottom sacks, while smaller in share, are important in niche applications where maximum product security or premium shelf presentation is required. The ongoing shift toward laminated woven PP sacks with enhanced printability and resealability highlights how the segment continues to evolve beyond functionality to branding and sustainability.

Cement & Building Materials Lead Market Share by End-Use Industry in the Packaging Sacks Sector

The cement and building materials sector accounts for 35% of global packaging sack consumption, underscoring its role as the backbone of demand. Each year, billions of tons of cement and construction aggregates are transported in heavy-duty sacks, making durability, moisture resistance, and stackability critical. Agriculture is the second pillar of demand, relying on both woven PP sacks and multi-wall paper sacks for crops, seeds, and animal feed. Together, construction and agriculture represent nearly two-thirds of the market, directly tied to urbanization, infrastructure spending, and global food security. Chemicals and fertilizers are high-value users requiring specialized sacks with barrier coatings, liners, and anti-static properties to ensure product stability and worker safety. Meanwhile, the food & beverage sector uses food-grade multi-wall paper sacks for staples such as sugar, flour, and rice, with a growing emphasis on high-quality graphics for branded retail distribution. Retail and consumer goods remain the smallest but fastest-evolving category, moving towards smaller, resealable sacks for premium pet food, charcoal, and gardening products, where convenience and brand presentation carry greater weight than bulk volume.

United States Packaging Sacks Market Driven by EPR Laws and Sustainable Material Innovations

The United States packaging sacks market is being reshaped by state-level Extended Producer Responsibility (EPR) laws, now enacted in seven states as of 2025. These laws hold producers accountable for end-of-life packaging, accelerating demand for recyclable sacks and PCR (post-consumer recycled) content integration. This regulatory momentum aligns with rising consumer and retailer expectations for eco-friendly packaging solutions.

Corporate investment is equally transformative. In August 2025, General Mills, Mars, and PepsiCo joined forces to launch the US Flexible Film Initiative (USFFI), targeting scalable recycling solutions for flexible plastics, including sacks. Additionally, manufacturers are focusing on mono-material paper-based sacks that replicate the barrier performance of plastics while being more easily recyclable. The boom in e-commerce and agriculture is further fueling demand, with shipping sacks for parcels, pet food, grains, and dry chemicals dominating usage. Automation-ready sack production is also gaining momentum as companies modernize supply chains to reduce costs and enhance efficiency.

Germany Packaging Sacks Market Strengthened by PPWR, EUDR, and Industrial Applications

Germany’s packaging sacks market is shaped by the EU Packaging and Packaging Waste Regulation (PPWR), which became effective in February 2025. This law mandates high recyclability, reuse, and minimum recycled content by 2030 and 2040, pushing sack manufacturers to adopt circular designs. The German Packaging Act (VerpackG), expanded in 2022, further enforces high recycling quotas, reinforcing the need for sacks made with bioplastics, recycled paper, and fiber blends.

A major development is the EU Deforestation Regulation (EUDR), requiring compliance by December 30, 2025. Paper sack producers must prove their raw material is deforestation-free, creating new due diligence systems for traceability. German innovation extends beyond compliance—advanced sorting, recycling technologies, and sack design improvements are enabling longer life cycles. Demand is particularly strong in food, beverages, and construction, where industrial sacks for cement, sand, and chemicals remain essential. This mix of regulation and innovation positions Germany as a European leader in sustainable sack production.

China Packaging Sacks Market Accelerated by Dual-Carbon Targets and E-Commerce Growth

China’s packaging sacks market is advancing under the dual-carbon policy, targeting carbon peaking by 2030 and neutrality by 2060. The government’s June 2025 express delivery regulations mandate eco-friendly and reusable packaging, directly boosting demand for sustainable sack formats.

The State Administration for Market Regulation (SAMR) has also issued nine new national standards for recycled plastics, effective February 2026. These require manufacturers to design sacks for recyclability, reduce adhesives, and avoid certain design features like metal fittings. Chinese companies are investing in automation, AI-enabled manufacturing, and smart traceability tools to meet both regulatory demands and consumer expectations. With 175 billion parcel deliveries recorded in 2024, e-commerce is a primary driver of demand for durable, lightweight, and cost-efficient sacks, while food and electronics also contribute to significant consumption growth.

India Packaging Sacks Market Boosted by Make in India and EPR Mandates

India’s packaging sacks market is expanding through strong policy support under the Make in India initiative and the PLI scheme, which incentivize domestic manufacturing. The government’s EPR rule requiring 30% recycled content in rigid plastics by April 2025 is pushing producers toward recyclable and resource-efficient sack solutions.

Investment is growing rapidly. Andhra Paper Limited signed a $14.4 million deal with Valmet AB in May 2024 for a new tissue production line, following a $31.1 million investment in Andhra Pradesh for new machinery, signaling ongoing capacity expansions. Technological upgrades, particularly automation and AI integration in packaging lines, are reducing labor costs and improving output consistency. The food and beverage industry, coupled with FMCG and e-commerce, remains the largest consumer of sacks. Growing demand for bulk agricultural packaging, branded FMCG sacks, and digitally printed short-run sacks highlights India’s dual focus on functionality and sustainability.

Japan Packaging Sacks Market Shaped by Positive List Regulations and Bio-Based Alternatives

Japan’s packaging sacks market is undergoing significant transformation under the positive list system for food-contact materials, effective June 2025. This policy restricts non-approved substances and is driving sack producers toward compliant, food-safe resin and paper alternatives. The rise of e-labeling and QR codes also impacts sack design, making traceability and consumer transparency standard features.

Sustainability targets add further momentum. Japan aims to reduce greenhouse gas emissions by 46% by 2030 and achieve net-zero by 2050, including the rollout of 2 million tonnes of bio-PP per year by 2030. Companies like Stora Enso are leading innovation with paper-based barrier sack materials that safeguard fragile and thermally sensitive products. Strongest demand is in ready-to-drink teas, coffees, snacks, and premium produce, where lightweight yet durable sack designs that combine performance with sustainability are increasingly favored.

Brazil Packaging Sacks Market Transitioning Under Anvisa RDC 983/2025 and PNRS Mandates

Brazil’s packaging sacks market is being reshaped by regulation and sustainability pressures. Anvisa’s RDC No. 983/2025, approved in August 2025, phases out certain substances in food and beverage packaging, directly impacting sack production. The National Solid Waste Policy (PNRS) further drives recyclability and circular economy adoption, requiring sack producers to innovate in material use and waste management.

Technological advances include eco-friendly sack materials made from forest-certified paper and bioplastics, aligning with international food safety standards. The food and beverage sector remains the dominant consumer, with sacks widely used in canned goods, grains, and agricultural supply chains. Brazil’s National Commission for Chemical Safety (Conasq) has also updated its registry of regulated chemicals, compelling companies to shift toward safer resin-based sacks. With sustainability at the forefront, Brazil is evolving into a leading Latin American hub for recyclable and compliant packaging sacks.

Packaging Sacks Market Report Scope

Packaging Sacks Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24.4 Billion

|

|

Market Size (2034)

|

$40.9 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Material Type (Paper, Plastic, Woven PP, Jute/Hessian), By Product Type (Open-Mouth, Pinch-Bottom, Pasted-Valve, Sewn, Woven), By End-Use Industry (Cement & Building Materials, Food & Beverage, Agriculture, Chemicals & Fertilizers, Retail & Consumer Goods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, Mondi Group, Smurfit Kappa Group Plc, DS Smith Plc, Intermas Nets S.A., Billerud AB, Sonoco Products Company, Oji Holdings Corporation, Rengo Co., Ltd., Huhtamaki Oyj, Graphic Packaging Holding Company, Amcor plc, Greif, Inc., Novolex, Bag Corp.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Sacks Market Segmentation

By Material Type

- Paper

- Plastic

- Woven PP

- Jute/Hessian

By Product Type

- Open-Mouth

- Pinch-Bottom

- Pasted-Valve

- Sewn

- Woven

By End-Use Industry

- Cement & Building Materials

- Food & Beverage

- Agriculture

- Chemicals & Fertilizers

- Retail & Consumer Goods

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Sacks Market

- International Paper Company

- Mondi Group

- Smurfit Kappa Group Plc

- DS Smith Plc

- Intermas Nets S.A.

- Billerud AB

- Sonoco Products Company

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Huhtamaki Oyj

- Graphic Packaging Holding Company

- Amcor plc

- Greif, Inc.

- Novolex

- Bag Corp.

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and data-driven research methodology to provide comprehensive insights into the global Packaging Sacks Market, combining both primary and secondary research approaches. Primary research involves interviews and consultations with key industry stakeholders, including sack manufacturers, raw material suppliers, distributors, brand owners, and logistics providers, to validate trends, innovations, and growth drivers. Secondary research encompasses a thorough analysis of regulatory frameworks, company reports, industry publications, trade associations, and government policies to understand historical performance and project future growth trajectories. USDAnalytics utilizes advanced forecasting models, scenario analysis, and quantitative techniques to assess market size, CAGR, and segment performance across materials, product types, and end-use industries. The methodology also incorporates sustainability initiatives, circular economy adoption, automation trends, and digital traceability advancements, ensuring that industry professionals receive actionable intelligence on technological developments, regulatory compliance, and regional dynamics, including detailed insights for the U.S., Germany, China, India, Japan, and Brazil.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.