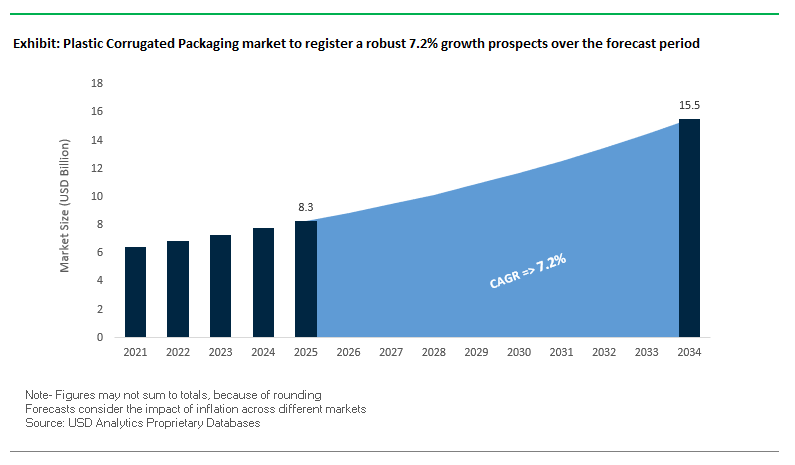

Market Overview: Plastic Corrugated Packaging Market to Reach $15.5 Billion by 2034 Driven by Durability, Reusability, and Logistics Efficiency

Market Value (MV) 2025: $8.3 billion │ 2034: $15.5 billion │ CAGR (2025–2034): 7.2%

The global plastic corrugated packaging market is witnessing accelerated growth as industries increasingly prioritize reusable, durable, and lightweight packaging solutions. Unlike single-use paper or plastic formats, plastic corrugated packaging offers exceptional durability, with the ability to withstand 50+ reuses in closed-loop supply chains, delivering both cost savings and sustainability benefits. For buyers and professionals, the critical considerations are: How does durability translate into long-term supply chain savings? Which sectors benefit most from moisture- and chemical-resistant packaging? And how does customization enhance product-specific protection across industries such as automotive, electronics, and healthcare?

Key Insights for Decision-Makers:

- Reusable Packaging Advantage: Plastic corrugated packaging outperforms single-use formats, lowering overall costs in returnable supply chains.

- Superior Performance: Resistance to moisture, temperature extremes, and chemicals positions it as a top choice for food, agriculture, pharmaceutical, and industrial sectors.

- Logistics Benefits: Lightweight structure reduces freight costs and transportation emissions, aligning with carbon reduction goals.

- Customization Capabilities: Options such as anti-static, UV-resistant, and conductive coatings support sensitive applications in electronics, automotive, and aerospace packaging.

Market Analysis: Recent Developments Driving Plastic Corrugated Packaging

The plastic corrugated packaging industry is shaped by strategic mergers, acquisitions, and investments that redefine global market dynamics. In April 2024, International Paper announced its $7.2 billion acquisition of DS Smith, creating a global packaging powerhouse with enhanced resources to expand fiber and specialty packaging, including hybrid corrugated solutions. Similarly, in October 2024, Mondi Group acquired Schumacher Packaging’s operations across Germany, Benelux, and the UK, strengthening its corrugated presence in Western Europe and reinforcing its sustainable packaging portfolio.

Consolidation trends continued with the Smurfit Kappa and WestRock merger (July 2024), forming Smurfit WestRock, a global leader with a strong circular economy framework. At the same time, manufacturers pursued targeted investments: Sonoco announced a $30 million expansion (July 2025) to increase adhesives and sealants capacity, ensuring resilience in industrial applications. Companies like Ball Corporation (February 2024) shifted focus exclusively to packaging after divesting its aerospace arm for $5.6 billion, reinforcing growth in high-performance packaging formats.

Other significant moves included Pactiv Evergreen’s divestment of two facilities (July 2024) for $110 million, Clearwater Paper’s $1 billion divestiture of its tissue business (July 2024) to refocus on paperboard, and Veritiv’s acquisition of Orora Packaging Solutions (September 2024) to expand specialty packaging capabilities.

Trends and Opportunities Reshaping the Plastic Corrugated Packaging Market

Strategic Capacity Expansion for Reusable Transport Packaging (RTP)

The plastic corrugated packaging market is experiencing a surge in capital investment aimed at scaling production for reusable transport packaging (RTP). Unlike single-use cardboard, plastic corrugated containers and trays are built for multi-trip logistics systems, offering durability, washability, and superior protection in industries such as automotive, agriculture, and retail.

A comparative study found that cardboard boxes can typically be reused only three times before degradation, while plastic corrugated containers last for 50+ reuse cycles, dramatically lowering the total cost of ownership despite a higher upfront investment. In the automotive sector, RTP solutions are integrated into closed-loop supply chains, where standardized container dimensions enhance automated handling systems, streamline workflows, and reduce reliance on manual labor. Beyond automotive, these containers are gaining traction in fresh produce and seafood logistics, where exposure to moisture quickly compromises cardboard. Plastic corrugated’s imperviousness to water and structural durability positions it as the packaging of choice for sectors where hygiene, consistency, and cost efficiency are paramount.

Advanced Material Science for Enhanced Recycled Content and Recyclability

A second defining trend in the plastic corrugated packaging market is the acceleration of material innovation, with manufacturers incorporating higher percentages of post-consumer recycled (PCR) content and creating mono-material blends to support circularity. This is driven by brand owner sustainability commitments and tightening regulatory frameworks, particularly in Europe.

The EU Packaging and Packaging Waste Regulation (PPWR) mandates at least 30% PCR content by 2030, escalating to 65% for beverage bottles by 2040, indirectly influencing the broader plastics supply chain, including corrugated formats. Suppliers are responding by innovating with both mechanically recycled (mPCR) and chemically recycled (cPCR) inputs, while advancing mono-material polypropylene (PP) and polyethylene (PE) structures to ensure recyclability in existing infrastructure. Companies like Mondi are leading this transition by integrating high-PCR solutions while maintaining performance standards. In parallel, corporate sustainability strategies from consumer goods leaders such as Henkel and Unilever are reinforcing demand, ensuring that corrugated plastics evolve in step with the circular economy transition.

Penetration into E-Commerce Fulfillment and Reverse Logistics

The e-commerce sector presents a high-growth opportunity for plastic corrugated packaging, especially given the logistical and environmental challenges of last-mile delivery and reverse logistics. As online shopping volumes increase, so too does the demand for packaging that can withstand multiple touchpoints, variable environmental exposure, and repeated return cycles.

Plastic corrugated offers superior durability, moisture resistance, and reusability compared to cardboard, making it particularly suitable for protecting high-value electronics, groceries, and fragile goods. Unlike cardboard packages that degrade after exposure to rain or snow, plastic corrugated containers ensure consistent product protection, directly reducing instances of product loss and customer dissatisfaction. Moreover, e-commerce returns one of the sector’s costliest pain points can be streamlined using corrugated plastic boxes that endure multiple trips without compromising structure. With customizability and lightweight formats, these containers offer not only cost efficiency through lower shipping weights but also improved brand presentation and sustainability credentials for retailers and fulfillment operators.

Development of High-Performance, Lightweight Solutions for Cold Chain Logistics

The rising importance of cold chain logistics in pharmaceuticals, healthcare, and food delivery creates a significant expansion avenue for insulated plastic corrugated packaging. Traditional cold chain solutions rely on EPS or heavy rigid containers, both of which are facing regulatory and environmental scrutiny. Plastic corrugated’s potential lies in combining its lightweight durability with integrated insulation and phase change materials (PCMs) for temperature-sensitive goods.

The World Health Organization (WHO) reports that over 50% of vaccines are wasted globally due to cold chain failures, underscoring the urgency for more reliable insulated solutions. Plastic corrugated shippers, embedded with insulation materials like aerogels or PCMs, can maintain critical ranges (e.g., 2°C to 8°C) for extended durations, protecting vaccines, insulin, and diagnostic samples. Beyond healthcare, insulated corrugated containers are also gaining traction in premium food and seafood logistics, ensuring freshness without reliance on external power. By targeting the last-mile delivery challenge, manufacturers can capture a growing share of the cold chain packaging market with solutions that combine robust protection, sustainability, and performance.

Competitive Landscape: Key Players in Plastic Corrugated Packaging

The competitive environment of the plastic corrugated packaging market features a mix of multinational corporations, specialized material science companies, and custom solution providers. Competition is defined by material innovation, reusability, customization, and sustainability integration.

Coroplast LLC Innovation in Durable and Chemical-Resistant Corrugated Sheets

Coroplast is a recognized leader in plastic corrugated sheets, with its flagship Coroplast® brand widely used for signage, displays, and reusable packaging. Its products excel in durability, water resistance, and chemical resistance, making them critical for closed-loop supply chains in automotive and industrial sectors. Specialized innovations include conductive polypropylene sheets for electronics packaging and laminated sheets with foam or fabric for added cushioning. Advanced extrusion facilities allow precise customization of thickness, colors, and coatings, enabling product-specific solutions.

Inteplast Group Custom-Engineered Corrugated Solutions Through IntePro Brand

Inteplast Group’s World-Pak division produces IntePro corrugated sheets, known for their strength-to-weight ratio and impact resistance. The company excels in customization, offering tailor-made boxes, containers, and dividers engineered by in-house technicians. Applications range from automotive laminated liners to construction storm panels, reflecting broad sectoral use. With over 50 North American facilities, Inteplast follows a vertically integrated strategy, ensuring efficiency, consistent supply, and continuous innovation across its operations.

Primex Plastics Corporation Sustainable Innovation and Specialty Product Development

Primex Plastics is a leading extruder of performance plastics, offering corrugated sheets across industries from foodservice to automotive. Recent innovations include Prime Sulapac, a premium wood composite for sustainable packaging, and Prime Weather-X InDURO, engineered for outdoor durability. Primex Plastics UK achieving ISO 14001 certification underscores its environmental commitment. Beyond manufacturing, the company emphasizes safety and product integrity, as highlighted by its Governor’s Safety Rising Star Award, reinforcing its reputation for quality-driven operations.

DS Smith Circular Packaging Model with Plastic Corrugated Solutions

DS Smith, primarily known for paper-based corrugated packaging, also provides plastic corrugated transit packaging. Its solutions are especially relevant for returnable supply chains in e-commerce and logistics. The company’s acquisition by International Paper (April 2024) enhances its global scale, creating synergies for integrated packaging solutions across materials. DS Smith’s circular business model, with integrated recycling and design teams, supports sustainability and e-commerce optimization, helping customers reduce carbon footprint and material waste while benefiting from durable packaging formats.

New-Tech Packaging Custom Plastic Corrugated Packaging for High-Value Industries

New-Tech Packaging specializes in custom-designed corrugated plastic boxes, totes, and partitions, particularly for high-value applications in aerospace, automotive, healthcare, and medical devices. Its key strength lies in bespoke engineering, incorporating features like custom foam inserts, Velcro closures, and printed branding for superior protection. With an in-house manufacturing model, New-Tech ensures fast turnaround times and strict quality control. Its reusable, heavy-duty products directly address the industry’s demand for durable and cost-effective alternatives to single-use packaging.

Plastic Corrugated Packaging Market Share Insights

Boxes and Containers Dominate Market Share by Product Type in Plastic Corrugated Packaging

Boxes and containers account for the largest share of the plastic corrugated packaging market in 2025 at 35%, reflecting their critical role as a durable, reusable replacement for cardboard in high-stakes logistics. Their dominance is anchored in industries where moisture, rough handling, and long supply chains make paper-based solutions inadequate, particularly in agriculture, food distribution, and closed-loop logistics systems. Crates and bins follow closely, serving as the industrial backbone for harvesting, automotive part transport, and in-plant handling, valued for their rigidity, stackability, and resilience under extreme conditions. Sheets, while smaller, secure their position as a dual-purpose substrate protective for packaging and promotional for advertising and signage leveraging their excellent printability. Dividers and separators command a high-value niche, protecting sensitive goods such as circuit boards and pharmaceutical vials, where precision and contamination prevention justify premium pricing. Totes and custom-engineered solutions, though smaller in volume, represent specialized, high-margin growth opportunities, catering to industries requiring tailored protection and handling. Collectively, the product segmentation highlights how boxes dominate through scale, crates and bins anchor industrial logistics, and custom solutions carve out value-driven niches.

Agriculture and Automotive Anchor Market Share by End-Use in Plastic Corrugated Packaging

Agriculture leads the plastic corrugated packaging market with a 20% share in 2025, driven by the widespread use of reusable crates and bins for harvesting and transporting fresh produce under wet and rugged conditions. Automotive follows with 18%, where reusable totes, bins, and custom dunnage underpin closed-loop logistics systems, protecting high-value parts from moisture and electrostatic discharge. E-commerce and logistics, along with food and beverage, are tied as moisture-resistance-driven segments. For e-commerce, weather-resistant plastic corrugated boxes improve last-mile delivery reliability, while in food and beverage, the material prevents spoilage during cold chain and wet handling. Pharmaceuticals and medical applications rely on sterile, chemical-resistant packaging for devices and biologics, meeting strict hygiene and compliance requirements. Electronics and electricals represent another critical niche, where anti-static properties protect delicate circuit boards and chips. Meanwhile, construction and advertising applications highlight versatility: temporary protection on job sites and durable substrates for signage. This breakdown shows how agriculture and automotive anchor demand, while e-commerce, food, pharma, and electronics accelerate diversified adoption across high-value supply chains.

United States: E-Commerce Expansion and Automation Drive the Plastic Corrugated Packaging Market

The United States plastic corrugated packaging market is accelerating in response to the surge in e-commerce and logistics, where lightweight, durable, and reusable packaging plays a vital role in reducing shipping costs and preventing product damage. Reusable corrugated plastic containers are gaining traction in closed-loop supply chains across automotive and pharmaceutical industries, driven by corporate sustainability commitments and the push to minimize waste. The industry also faces an evolving regulatory landscape, with state-level initiatives like California’s SB-54 Extended Producer Responsibility (EPR) law and PFAS-free mandates reshaping nationwide supply chains and spurring innovation in recyclable packaging materials.

Adding to this momentum, expansion in domestic manufacturing is strengthening supply capacity. A notable example is McKinley Packaging’s new 500,000-square-foot corrugated box plant in Lancaster, Texas, designed to serve the e-commerce boom. Technological advancements are also redefining the sector, with automation, robotics, and on-demand production enabling greater efficiency and scalability. These developments position the U.S. market as a leader in sustainable, tech-enabled packaging solutions.

Germany: Circular Economy Leadership and High Recycling Rates Fuel Market Growth

Germany’s plastic corrugated packaging industry is shaped by its rigorous regulatory framework, particularly the EU Packaging and Packaging Waste Regulation (PPWR), which mandates recyclable and eco-friendly packaging solutions. The country’s long-standing leadership in the circular economy has fostered deep collaboration between manufacturers and end-users, resulting in packaging products that incorporate high recycled content while meeting EU sustainability targets.

Germany also benefits from one of Europe’s highest recycling rates, exceeding 50% for plastic packaging in 2022, which provides a solid foundation for producing high-quality corrugated plastic from recycled feedstock. Additionally, the market is witnessing a surge in reusable solutions, particularly in automotive and industrial supply chains, where durable and long-lasting containers reduce transportation costs and material waste. This integration of strict policy, high recycling efficiency, and reusable innovation makes Germany one of the most advanced and sustainable hubs for plastic corrugated packaging.

China: Sustainability Policies and E-Commerce Boom Strengthen Plastic Corrugated Packaging Demand

China’s plastic corrugated packaging market is thriving under the dual forces of sustainability mandates and explosive e-commerce growth. The government’s “dual carbon” strategy, aimed at achieving carbon peak and neutrality, is driving eco-friendly practices in logistics, with new rules pushing express delivery companies to adopt recyclable, reusable, and reduced packaging solutions. Plastic corrugated containers are emerging as a durable and sustainable alternative to paper and single-use plastics in this context.

The rapid expansion of e-commerce and logistics networks further amplifies demand, as secure and efficient packaging is essential to protect products during fast-paced shipping. At the same time, government efforts to curb over-packaging are accelerating adoption of lightweight and efficient corrugated plastic containers. Chinese manufacturers are heavily investing in automation, AI, and robotics to enhance production efficiency and ensure compatibility with automated logistics systems, making China a global growth engine for this sector.

India: Government Policies and E-Commerce Fuel Expansion of Plastic Corrugated Packaging

India’s plastic corrugated packaging market is expanding rapidly, fueled by regulatory, industrial, and consumer demand factors. The Plastic Waste Management (Amendment) Rules are phasing out single-use plastics and accelerating the shift toward reusable and sustainable alternatives, directly benefiting corrugated plastic packaging. Government-led initiatives such as the “Integrated Cold Chain and Value Addition Infrastructure” program are further boosting demand for insulated plastic corrugated containers to support the transportation of pharmaceuticals and perishable goods.

E-commerce growth is another major catalyst, particularly through online grocery and food delivery platforms, which rely heavily on water-resistant and durable packaging solutions. At the same time, the industry is seeing a manufacturing expansion, with companies scaling up production to supply plastic corrugated containers for fruits, vegetables, pharmaceuticals, and fast-moving consumer goods. These combined drivers firmly position India as a high-potential market for sustainable plastic corrugated packaging.

Brazil: Cold Chain Logistics and Circular Economy Regulations Accelerate Market Transition

Brazil’s plastic corrugated packaging market is undergoing a strong transition, driven by legislation such as the National Solid Waste Policy, which restricts single-use plastics and advances the country’s circular economy agenda. This regulatory push is steering industries toward reusable and durable corrugated plastic containers that align with sustainability mandates.

A significant growth driver lies in Brazil’s expanding cold chain logistics market, where durable, temperature-resistant packaging is essential for pharmaceuticals and perishable food transportation. At the same time, industries such as agriculture and automotive are increasingly adopting reusable corrugated plastic containers to reduce waste and logistics costs. With innovation in reusability and government-backed sustainability efforts, Brazil is emerging as a competitive player in the global corrugated plastic packaging sector.

Japan: Recycling Leadership and Advanced Functional Packaging Innovation

Japan’s plastic corrugated packaging industry is built on one of the world’s most advanced recycling systems, which ensures high collection and utilization rates for plastic waste. This recycling infrastructure provides a reliable feedstock for producing sustainable corrugated plastic packaging. Reinforcing this, the Japanese government’s Plastic Resource Circulation Act is accelerating the adoption of circular packaging solutions across industries.

Japanese manufacturers are also leading in functional innovation. Advances in material science have enabled the development of corrugated plastic packaging that is stronger, water-resistant, and capable of meeting demanding industrial applications. Companies are designing packaging for sectors such as electronics, healthcare, and logistics, where durability and performance are critical. With a combination of strong recycling systems, policy support, and innovation-driven manufacturing, Japan stands out as a model for sustainable and high-performance plastic corrugated packaging solutions.

Plastic Corrugated Packaging Market Report Scope

Plastic Corrugated Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.3 Billion

|

|

Market Size (2034)

|

$15.5 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Product Type (Boxes and Containers, Crates and Bins, Totes, Sheets, Dividers and Separators, Custom Solutions), By Material Type (Polypropylene, Polyethylene, High-Density Polyethylene, Polyvinyl Chloride, Polystyrene), By Application (Agriculture, Automotive, Construction, Advertising & Signage, E-commerce & Logistics, Electronics & Electricals, Food & Beverage, Pharmaceuticals & Medical, Other Applications), By Use Type (Reusable, Single-Use)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Twinplast Ltd., Coroplast, American Paper & Plastic Inc., DS Smith Plc, Emballages Saint-Jacques Inc., Corex Plastics, The Corrugated Plastic Company, Huiyuan Plastic, Shandong Tianhong Plastic Co., Ltd., Shijiazhuang Guanghua Plastic Co., Ltd., Northern Sheets, Inc., New Plastic Concepts, Plasti-Fab Ltd., Karton S.p.A., Zezhi Packaging Technology Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plastic Corrugated Packaging Market Segmentation

By Product Type

- Boxes and Containers

- Crates and Bins

- Totes

- Sheets

- Dividers and Separators

- Custom Solutions

By Material Type

- Polypropylene

- Polyethylene

- High-Density Polyethylene

- Polyvinyl Chloride

- Polystyrene

By Application

- Agriculture

- Automotive

- Construction

- Advertising & Signage

- E-commerce & Logistics

- Electronics & Electricals

- Food & Beverage

- Pharmaceuticals & Medical

- Other Applications

By Use Type

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Plastic Corrugated Packaging Market

- Twinplast Ltd.

- Coroplast

- American Paper & Plastic Inc.

- DS Smith Plc

- Emballages Saint-Jacques Inc.

- Corex Plastics

- The Corrugated Plastic Company

- Huiyuan Plastic

- Shandong Tianhong Plastic Co., Ltd.

- Shijiazhuang Guanghua Plastic Co., Ltd.

- Northern Sheets, Inc.

- New Plastic Concepts

- Plasti-Fab Ltd.

- Karton S.p.A.

- Zezhi Packaging Technology Co., Ltd.

*List not Exhaustive

Research Coverage

This report investigates the dynamic landscape of the global Plastic Corrugated Packaging market, examining key breakthroughs in reusable and durable packaging solutions, advanced material innovations, and sector-specific applications. USDAnalytics’ analysis reviews market transformations driven by sustainability imperatives, e-commerce growth, cold chain logistics, and strategic corporate investments, highlighting how reusable corrugated plastic containers are replacing single-use formats in diverse industrial supply chains. This report is an essential resource for packaging professionals, supply chain managers, procurement specialists, and sustainability officers seeking actionable insights into market size, growth drivers, technological advancements, competitive strategies, and end-use adoption patterns. By integrating historic data from 2021 to 2024 and forecast trends to 2034, this study provides a forward-looking perspective on reusable transport packaging, high-performance material solutions, and the evolving regulatory landscape across global regions.

Scope Highlights:

- Segmentation: By Product Type (Boxes and Containers, Crates and Bins, Totes, Sheets, Dividers and Separators, Custom Solutions), By Material Type (Polypropylene, Polyethylene, High-Density Polyethylene, Polyvinyl Chloride, Polystyrene), By Application (Agriculture, Automotive, Construction, Advertising & Signage, E-commerce & Logistics, Electronics & Electricals, Food & Beverage, Pharmaceuticals & Medical, Other Applications), By Use Type (Reusable, Single-Use)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historical & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies Covered: Analysis/profiles of 15+ leading players including Twinplast Ltd., Coroplast, American Paper & Plastic Inc., DS Smith Plc, Emballages Saint-Jacques Inc., Corex Plastics, The Corrugated Plastic Company, Huiyuan Plastic, Shandong Tianhong Plastic Co., Ltd., Shijiazhuang Guanghua Plastic Co., Ltd., Northern Sheets, Inc., New Plastic Concepts, Plasti-Fab Ltd., Karton S.p.A., Zezhi Packaging Technology Co., Ltd.

Methodology

The study employs a robust research methodology combining primary and secondary data collection, extensive interviews with industry executives, and analysis of company financial reports, strategic announcements, and supply chain trends. Market sizing and forecasts leverage bottom-up and top-down approaches, cross-validated with regional production, consumption, and trade statistics. USDAnalytics employs scenario analysis to assess demand across reusable and single-use applications, material types, and product categories, incorporating macroeconomic, regulatory, and technological factors. Data accuracy is ensured through triangulation across multiple sources, while expert insights are used to interpret competitive dynamics, end-use adoption, and market growth drivers. Key performance indicators, adoption rates, and sector-specific growth trajectories are modeled to provide actionable intelligence for investment, product development, and strategic decision-making.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.