Retail Glass Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Retail Glass Packaging Market Set to Reach $85.6 Billion by 2034 Driven by Sustainability and Premiumization

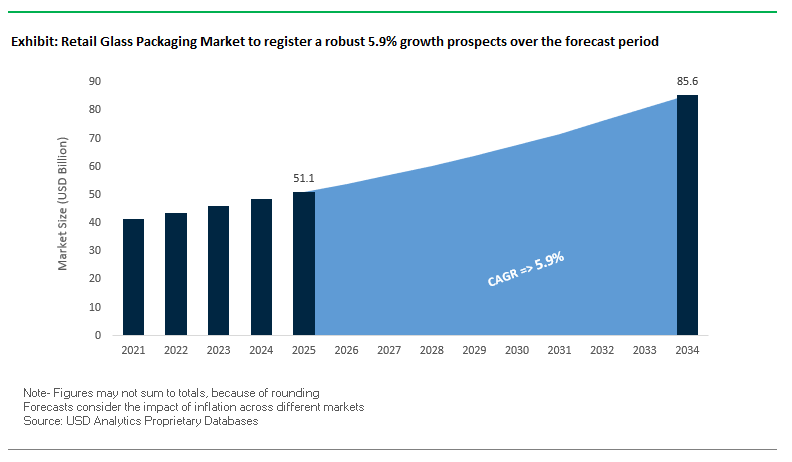

The global retail glass packaging market is projected to grow from $51.1 billion in 2025 to $85.6 billion by 2034, at a CAGR of 5.9%. Growth is fueled by the increasing demand for sustainable packaging, premium product presentation, and lightweight innovations. Glass packaging continues to be a preferred choice due to its high recyclability, aesthetic appeal, and ability to maintain product quality, particularly in the alcoholic beverage, cosmetics, and gourmet food sectors.

Key Insights for industry professionals and buyers:

- Recycled Content as a Key Metric: Manufacturers are boosting the use of recycled cullet, reducing energy consumption and raw material needs.

- Lightweighting Innovations: Notable examples, such as Johnnie Walker’s 180-gram glass bottle, highlight a focus on reducing carbon footprint during production and transportation.

- Premiumization Trends: Brands increasingly use glass packaging to enhance perceived product value, especially in spirits, cosmetics, and specialty foods.

- Infinite Recyclability: Glass can be recycled repeatedly without quality loss, supporting circular economy initiatives.

- Sustainability Leadership: Companies are investing in renewable energy, hybrid furnaces, and low-carbon production technologies to meet regulatory and environmental goals.

Market Analysis: Industry Innovation and Sustainability Investments Are Accelerating Global Glass Packaging Growth

The retail glass packaging market is witnessing rapid developments in sustainability, lightweighting, and premium packaging design. In August 2025, GCA accelerated its global growth by investing in lightweight glass technologies, reflecting an industry-wide push to reduce material usage and carbon footprint. Similarly, Beta Glass reported a 63% surge in revenue in H1 2025, signaling strong adoption of glass packaging in African markets.

European players are advancing both technology and environmental performance. In July 2025, Ardagh Glass Packaging-Europe launched a 300g lightweight wine bottle, while also committing to produce the world’s first emerald green glass bottle using a hybrid electric furnace and biofuel. Concurrently, O-I Glass validated early sustainability achievements, progressing toward Paris-aligned carbon targets, reflecting increasing pressure on glass manufacturers to integrate environmental performance with operational efficiency.

Investment in renewable energy is also shaping the market. In March 2025, Ardagh Glass Packaging-North America completed a 13-megawatt solar project in California, demonstrating a commitment to decarbonization.

Retail Glass Packaging Market: Trends and Opportunities Driving Innovation and Sustainability

Strategic Lightweighting to Reduce Environmental Footprint and Logistics Costs

A central trend shaping the retail glass packaging market is the lightweighting of glass bottles and containers to minimize raw material use, reduce logistics costs, and lower environmental impact. Advanced manufacturing technologies like Narrow Neck Press and Blow (NNPB) are enabling glassmakers to deliver thinner yet stronger bottles that preserve iconic brand aesthetics. For example, Ardagh Group partnered with Coca-Cola to reduce the weight of a 330ml glass bottle from 240 grams to 190 grams, a 21% reduction achieved without compromising performance or design. Beyond production efficiencies, lightweighting delivers measurable sustainability benefits. Verallia’s case study with a rum brand demonstrated that a 30% weight reduction in glass bottles cut transport-related carbon emissions by 12,000 miles annually. Such outcomes highlight how lightweighting strategies go beyond cost savings—they serve as a critical decarbonization tool for beverage and food companies aiming to achieve Scope 3 emissions reductions while maintaining premium product appeal.

Premiumization and Brand Differentiation Through Custom Molded Glass

Another transformative trend in retail glass packaging is the move toward custom-molded, premium designs that elevate brand identity and enhance consumer engagement. Glass packaging continues to be associated with craftsmanship, luxury, and heritage, making it the material of choice for spirits, cosmetics, and perfumery. PGP Glass has demonstrated this with bespoke bottle designs for specialty spirits and personal care products, such as guitar-shaped decanters and intricately molded perfume bottles. These unique formats not only differentiate products on crowded shelves but also strengthen brand storytelling. Importantly, the demand for premium aesthetics is being matched with sustainable innovation. Verescence’s sustainable luxury portfolio showcases intricate lightweight bottles for high-end cosmetics that combine artistry with environmental responsibility. This integration of premium feel, creative customization, and lightweight sustainability illustrates the evolution of glass packaging from a traditional container to a strategic branding and sustainability asset.

Advanced Coating Technologies to Enhance Durability and Functionality

One of the most promising opportunities lies in the application of advanced coating technologies to improve the performance of glass packaging. Hybrid organic-inorganic coatings are enhancing strength by 6% to 90%, significantly reducing breakage and extending the lifecycle of reusable glass bottles. This is particularly relevant in the context of deposit-return and reuse systems, where bottle durability is crucial to achieving economic and environmental viability. Beyond durability, coatings are also being engineered for functional benefits. Invisible UV-blocking coatings are increasingly applied to protect light-sensitive products such as craft beer, olive oil, cosmetics, and pharmaceuticals, ensuring product integrity and extending shelf life. By combining strength with product protection, coatings expand the versatility of glass packaging, allowing it to meet the rigorous demands of diverse retail sectors while reducing waste and enhancing consumer confidence in product quality.

Integration of Hybrid Packaging with Smart Features

Another major opportunity is the integration of digital and smart features into retail glass packaging, transforming bottles into interactive and traceable assets. A Univerre case study illustrated how NFC tags embedded in limited-edition liqueur bottles enabled consumers to unlock a digital photo album via their smartphones, merging physical packaging with digital storytelling. This enhances consumer engagement, brand loyalty, and product authentication, while also helping combat counterfeiting in high-value segments like premium spirits and luxury cosmetics. Similarly, QR codes are being widely adopted to enhance supply chain transparency. For example, Hershey’s demonstrated the use of QR codes on packaging to provide instant access to nutritional details, ingredient information, and corporate contact points, strengthening consumer trust and regulatory compliance. As digital product passports gain traction in Europe and beyond, hybrid packaging with smart identifiers will play a central role in ensuring regulatory alignment while enhancing consumer experiences.

Competitive Landscape: Leading Global Players Are Pioneering Lightweight, Sustainable, and Premium Glass Packaging Solutions

The retail glass packaging industry is highly competitive, with top companies combining innovation, sustainability, and premiumization strategies to meet global demand. The competitive focus is on lightweight materials, recycled content, and carbon-efficient production.

Owens-Illinois Inc. (O-I): Driving Sustainable Glass Packaging with a Focus on Recycled Content and Premium Operations

O-I is among the world’s largest glass container manufacturers, serving food and beverage brands globally. In July 2025, the company reconfigured its Bowling Green facility to enhance premium operations under the “Fit to Win” strategy. O-I aims for 50% average recycled content by 2030 and a 25% reduction in GHG emissions, highlighting its leadership in sustainable glass packaging. The company has also achieved a 13.67% CO2 reduction since 2017 and works to expand glass recycling accessibility across all locations.

Ardagh Group SA: Leading Lightweighting and Decarbonization Initiatives in Glass Packaging

Ardagh is a global supplier of infinitely recyclable glass containers. In July 2025, the company produced the world’s first emerald green glass bottle using biofuel and hybrid electric furnaces, alongside a 300g lightweight wine bottle. Ardagh’s sustainability strategy spans ecology, emissions, and social responsibility, complemented by its solar energy project in California. Recognized as Supplier of the Year by Diageo in 2022, the company blends innovation with environmental commitment.

Verallia S.A.: Expanding European Footprint and Advancing Recycled Glass Integration

Verallia ranks among the top three global glass producers for beverages and food. In July 2024, it acquired Vidrala’s glass business in Italy, enhancing its European operations. The company operates 12 cullet processing centers to support circular economy goals and maintains vertical integration across 34 glass plants and five decoration facilities, enabling comprehensive solutions for its global clientele.

Stoelzle Glass Group: Specializing in Premium Glass Solutions with Carbon-Neutral Ambitions

Stoelzle, based in Austria, produces high-end glass for pharmaceuticals, spirits, food, and cosmetics. Partnering with Siemens, it implements the Simatic Energy Manager PRO system to improve efficiency and reduce CO2 emissions. By 2030, Stoelzle targets a 50% carbon emissions reduction and 20% energy savings, combining premium craftsmanship with sustainability initiatives.

Saverglass S.A.: Delivering Customized and Premium Glass Packaging for Luxury Brands

Saverglass focuses on high-end spirits, fine wine, and champagne packaging. Its strategy emphasizes premiumization and customization, offering over 220 bottle designs and advanced decoration techniques. Sustainability is a core commitment, with an 11% CO2 footprint reduction over the last decade and a goal to cut process emissivity by 45% by 2035, reflecting its dedication to environmentally responsible luxury packaging.

Retail Glass Packaging Market Share Insights, 2025-2034

Food & Beverages anchor Market Share by Application in the Retail Glass Packaging market

Food & Beverages command 75% of retail glass packaging demand, reflecting glass’s premium positioning in spirits, wine, craft beer, specialty sauces, and premium juices where flavor protection, chemical inertness, and brand heritage justify higher unit economics versus PET or aluminum. Personal Care & Cosmetics ( 15%) leverages heavy-walled bottles and jars to signal luxury and ensure formula stability, reinforcing glass’s shelf-power in beauty aisles. Pharmaceuticals ( 5%) rely on Type I borosilicate vials, ampoules, and syrup bottles for barrier integrity and long-term stability, a niche insulated by regulation. Homecare ( 3%) remains a premium/natural-positioned sliver—concentrates and essential-oil cleaners exploit glass’s purity halo—while Industrial Goods ( 2%) is limited to specialized chemicals where inert containers mitigate compatibility risks. The mix underscores a strategic shift toward high-value, brand-differentiated categories, where infinitely recyclable glass secures price realization and ESG alignment despite supply-chain penalties from weight and breakage risk.

Retail remains the dominant sales channel in Retail Glass Packaging market share by end-use

Retail accounts for 80% of sales as glass’s clarity, gloss, and tactile weight convert at point-of-sale, enabling premium pricing and impulse purchasing across beverage and gourmet categories. Food Service ( 10%)—bars, restaurants, hotels—cements glass as part of the on-premise experience, from table-presented condiments to signature spirits, translating packaging into brand theater. E-commerce ( 5%) grows selectively in premium SKUs (e.g., prestige beauty, high-end spirits) where AOV supports protective secondary packaging and higher freight, but adoption is constrained by breakage and dimensional weight. Healthcare ( 4%) distributes glass based on regulatory fit rather than merchandising, while Industrial ( 1%) reflects highly specialized B2B uses. Net-net, retail channel dominance highlights glass’s role as a visual merchandising asset; omnichannel growth depends on packaging engineering (shock/tilt testing, partitioning, right-weighting) that de-risks last-mile fulfillment without eroding sustainability credentials.

European Union: Regulatory Mandates and Deposit Return Systems Boosting Glass Packaging

In the European Union, the Packaging and Packaging Waste Regulation (PPWR), effective February 2025, is reshaping the retail glass packaging market. The regulation requires a certain percentage of takeaway food and beverage products to be offered in reusable or refillable glass packaging, strengthening the role of glass as a sustainable material. The PPWR further introduces a grading system for recyclability, requiring all packaging sold in the EU to reach at least 70% recyclability by 2030 and up to 95% (Grade A) by 2038. This regulation, combined with the Ecodesign for Sustainable Products Regulation (ESPR) and the Digital Product Passport, ensures complete transparency on the origin, recyclability, and compliance of glass packaging.

The EU is also accelerating the rollout of Deposit Return Systems (DRS) across member states to increase collection and reuse rates of bottles and jars. With Europe’s paper recycling rate already at 79.3% in 2023, the retail glass packaging sector is building on this circular economy momentum. By 2026, restrictions on PFAS in food contact materials will also impact coatings used on glass containers, pushing manufacturers to adopt safer alternatives. Pilot projects such as Germany’s “Mehrweg Modell Stadt”, which tests reusable container networks across providers, highlight how the EU is fostering a transition toward circular and refillable retail packaging systems.

United States: EPR Legislation and Circular Economy Targets Reshaping Market Dynamics

The United States retail glass packaging market is being shaped by both federal and state-level initiatives. The EPA and the U.S. Plastics Pact are pushing for a circular economy, and seven states have now enacted Extended Producer Responsibility (EPR) laws, with Maryland mandating Producer Responsibility Organizations (PROs) to cover 90% of packaging waste management costs by 2030. These laws directly impact retailers and packaging suppliers, encouraging greater use of glass containers due to their recyclability and long life cycle.

Investment in advanced recycling infrastructure, funded by the Infrastructure Investment and Jobs Act, is strengthening local supply chains for packaging materials. A key trend is the replacement of rigid plastics in fresh produce, grocery, and beverage packaging with lightweight, recyclable glass bottles and jars. The U.S. is also witnessing strong collaboration between companies and the U.S. Plastics Pact to align with national circular economy targets. Furthermore, premium retail brands are focusing on eco-friendly glass packaging innovations, aligning product aesthetics with consumer expectations for sustainability and reducing dependency on virgin plastics.

China: Regulatory Push and E-Commerce Growth Driving Retail Glass Packaging

China is accelerating the adoption of retail glass packaging through new regulations effective June 2025, which require express delivery companies to prioritize eco-friendly, reusable, and reduced packaging formats. The NDRC and the Ministry of Ecology and Environment (MEE) are implementing policies under the 14th Five-Year Plan to curb plastic pollution, indirectly boosting the use of glass in both food and beverage retail and e-commerce deliveries.

Leading logistics companies such as JDL Express and SF Express are adopting reusable circulation boxes and return-based packaging models, where glass containers play a significant role in replacing single-use packaging. Community-led programs, such as Zhejiang University’s package reuse initiative, encourage consumers to return glass bottles and jars for circulation. With the dual drivers of environmental policy and e-commerce growth, China is positioning retail glass packaging as a sustainable alternative to plastics, supported by large-scale domestic manufacturing and automation in the packaging supply chain.

India: Extended Producer Responsibility and Traceability Fueling Glass Packaging Growth

In India, the Plastic Waste Management (Amendment) Rules, 2024 are central to the growth of the retail glass packaging market, as they shift responsibility for packaging waste to producers and importers under Extended Producer Responsibility (EPR). While MSMEs are exempt, larger players must comply with strict recycling and waste recovery standards. Starting July 2025, all packaging must be traceable through QR codes, barcodes, or unique identifiers, increasing accountability across supply chains and creating opportunities for glass packaging manufacturers, who benefit from the material’s high recyclability and ease of traceability.

Another trend in India is the development of bioplastics from agricultural and dairy waste, but glass remains a preferred material in retail food, dairy, and beverage packaging due to its inertness, reusability, and premium appeal. Innovations such as dust-resistant and UV-stable packaging solutions are also being tested in parallel to India’s climate-specific needs. The rising demand for packaged foods and beverages, combined with national commitments under the India Plastics Pact, is expected to accelerate the adoption of refillable and recyclable glass packaging solutions.

Japan: Refillable Packaging Innovations and Bio-Based Material Integration

Japan is positioning itself as an innovation leader in the retail glass packaging market, aligned with its Plastic Resource Circulation Strategy, which mandates that all packaging be reusable or recyclable by 2025. The government has also set targets to double renewable material usage by 2030, which is shaping how companies integrate bio-based and recyclable materials alongside glass.

Companies like Shiseido and Tokiwa Cosmetics are pioneering refillable packaging systems in the beauty and personal care sector, incorporating glass jars and bottles designed for multiple reuse cycles. Alongside, Nippon Paper Industries’ SHIELDPLUS demonstrates Japan’s push toward paper-based alternatives, but glass remains a core material in cosmetics, food, and beverage retail packaging due to its premium look and recyclability. Collaborations with global players such as LyondellBasell are driving hybrid material innovations, yet glass packaging continues to gain traction in Japan’s high-end retail and circular economy framework, particularly for luxury goods and refillable beauty products.

Brazil: Reverse Logistics and Waste Policy Enhancing Glass Packaging Adoption

In Brazil, the National Solid Waste Policy (PNRS) underpins the retail glass packaging market by enforcing guidelines for recycling, reuse, and waste reduction. A key element is the reverse logistics system, which makes producers accountable for post-consumer packaging recovery. This has led to increased adoption of glass bottles and jars, which are easier to reuse in beverage and food supply chains compared to plastics.

The Brazilian government is also encouraging sustainable retail packaging innovations, especially in fresh food and beverage segments. The growing use of MAP (Modified Atmosphere Packaging) and vacuum-sealed formats is complemented by glass containers that extend product freshness and align with consumer preferences for sustainable solutions. By promoting responsible waste management and supporting sustainable packaging initiatives, Brazil is positioning retail glass packaging as an essential component of its circular economy transition.

Retail Glass Packaging Market Report Scope

Retail Glass Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$51.1 Billion

|

|

Market Size (2034)

|

$85.6 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Material (Plastic, Glass, Metal, Paper & Paperboard), By Application (Food & Beverages, Personal Care & Cosmetics, Homecare, Pharmaceuticals, Industrial Goods), By End-Use Industry (E-commerce, Retail, Food Service, Industrial, Healthcare)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, DS Smith Plc, Smurfit Kappa Group Plc, Graphic Packaging Holding Company, Sonoco Products Company, Huhtamaki Oyj, International Paper Co., WestRock Company, ProAmpac, Berry Global, Inc., Greif, Inc., Silgan Holdings Inc., Pactiv Evergreen Inc., PAPACKS

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Retail Glass Packaging Market Segmentation

By Material

- Plastic

- Glass

- Metal

- Paper & Paperboard

By Application

- Food & Beverages

- Personal Care & Cosmetics

- Homecare

- Pharmaceuticals

- Industrial Goods

By End-Use Industry

- E-commerce

- Retail

- Food Service

- Industrial

- Healthcare

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Retail Glass Packaging Market

- Amcor plc

- Mondi Group

- DS Smith Plc

- Smurfit Kappa Group Plc

- Graphic Packaging Holding Company

- Sonoco Products Company

- Huhtamaki Oyj

- International Paper Co.

- WestRock Company

- ProAmpac

- Berry Global, Inc.

- Greif, Inc.

- Silgan Holdings Inc.

- Pactiv Evergreen Inc.

- PAPACKS

* List Not Exhaustive

Methodology

USDAnalytics applies a comprehensive and structured methodology to analyze the retail glass packaging market, combining both quantitative and qualitative research approaches to deliver actionable insights for industry professionals. Our process begins with exhaustive secondary research, sourcing data from company reports, regulatory filings, trade journals, press releases, patent databases, and verified news outlets to assess market dynamics, competitive strategies, and technological innovations. This is followed by primary research involving interviews with key stakeholders including manufacturers, distributors, retailers, and end-users across food & beverages, personal care, pharmaceuticals, and homecare sectors. Market sizing and forecasts are derived from historical data, current adoption rates, premiumization trends, and sustainability-driven initiatives, with special focus on lightweight glass innovations, recycled cullet usage, and hybrid furnace technologies. USDAnalytics integrates regional regulatory policies, circular economy initiatives, and environmental standards to evaluate their impact on demand and market evolution. Advanced analytical techniques, including predictive modeling and scenario analysis, are then applied to generate insights on material type adoption, application-specific growth, premium packaging trends, and emerging market opportunities, enabling decision-makers to leverage sustainability, energy efficiency, and brand differentiation strategies in the global retail glass packaging market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.