Reusable Corrugated Plastic Boxes Market Size, Overview, and Growth Outlook (2025–2034)

Reusable Corrugated Plastic Boxes Market Poised for $15.7 Billion by 2034 as Supply Chain Efficiency and Sustainability Drive Adoption

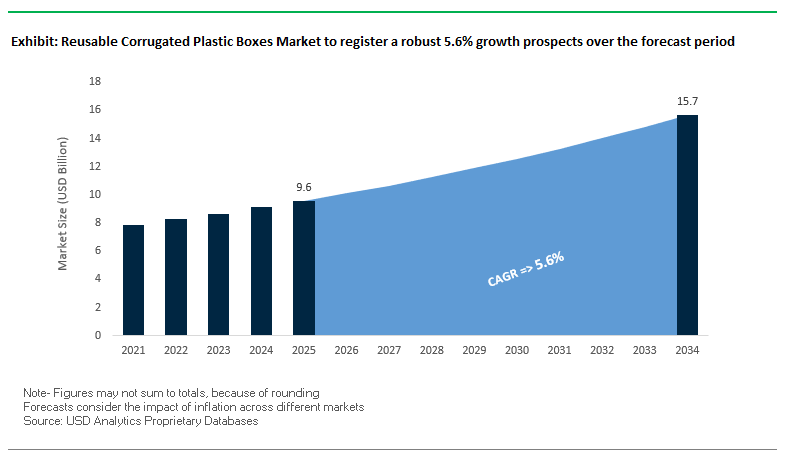

The global reusable corrugated plastic boxes (RCPB) market is projected to grow from $9.6 billion in 2025 to $15.7 billion by 2034, representing a CAGR of 5.6%. Growth is propelled by the need for durable, multi-use packaging solutions that improve product protection, cost-efficiency, and environmental performance. RCPBs are increasingly critical in automotive, food, pharmaceutical, and retail supply chains, where hygiene, reliability, and reduced product damage are key priorities.

Key Insights for industry professionals and buyers:

- Cost Savings Over Time: Multi-use RCPBs reduce total cost of ownership compared to single-use cardboard, achieving ROI within a few cycles.

- Minimized Product Damage: High durability helps prevent breakage and spoilage during transit, reducing waste and insurance costs.

- Integration with Automation: Designed for conveyor belts, robotic sorting, and automated warehouse operations, improving throughput and labor efficiency.

- Sustainability Benefits: Reusable plastic boxes contribute to lower carbon footprint, supporting corporate ESG and circular economy goals.

- Customization and Flexibility: Growing demand for custom-sized boxes with interchangeable parts or specialized inserts allows tailored solutions for complex product handling.

- Material Innovation: Advanced composite plastics offer enhanced wear and abrasion resistance, extending lifespan and enabling use in more challenging environments.

RCPBs are becoming a strategic asset for companies seeking to balance operational efficiency, environmental compliance, and product protection.

Market Analysis: Technological Innovation and Strategic Collaborations Are Driving Growth in Reusable Corrugated Plastic Boxes

The RCPB market is experiencing dynamic developments through strategic partnerships, mergers, acquisitions, and innovative product launches. In August 2025, a study revealed a composite antimicrobial film made from carrageenan and polyoxometalate, exhibiting strong bactericidal activity and biodegradability—an important advancement for food and pharmaceutical transport applications.

Strategic collaborations continue to shape the industry. In October 2024, Newwen partnered with Parrdekopper to launch reusable transport boxes equipped with RFID and QR codes, enhancing traceability and enabling reuse for up to 25 cycles. Similarly, Sprouts Farmers Market partnered with IFCO in October 2024 to replace single-use shipping packaging, reducing food waste and improving operational efficiency. In September 2024, Array Technologies transitioned from cardboard to durable reusable plastic casings, supporting bulk packaging and more efficient transportation.

Industry consolidation and portfolio expansion are also key drivers. Inteplast Group’s acquisition of CoolSeal USA in December 2024 expanded its sustainable packaging offerings, while Zeus Group acquired The Weedon Group in April 2024, strengthening capabilities in integrated corrugated manufacturing. In May 2024, Condor Expedite launched a fully reusable cold chain packaging division, enabling refrigeration for up to nine days without dry ice. The merger of Smurfit Kappa and WestRock in September 2024 further underscores the drive towards global scale, sustainable innovation, and end-to-end supply chain solutions.

Reusable Corrugated Plastic Boxes Market: Trends and Opportunities Driving Cost-Efficient and Sustainable Logistics

Corporate Adoption for Internal Material Handling Efficiency

A defining trend in the reusable corrugated plastic boxes (RCPBs) market is the corporate shift from single-use corrugated cardboard to durable, reusable solutions that reduce costs over time. While RCPBs require a higher upfront investment, their ability to withstand hundreds of reuse cycles makes them far more cost-effective on a per-use basis. A comparative study in North America demonstrated that reusable containers for fresh produce required 39% less total energy and generated 95% less solid waste over a two-year period compared to single-use corrugated trays. Beyond sustainability, corporations are adopting RCPBs to streamline internal operations. Closed-loop supply chains—such as in the automotive and electronics industries—leverage RCPBs for shuttling parts and components between suppliers and assembly plants. Their standardized dimensions, stacking strength, and compatibility with automated handling systems improve material flow, reduce labor costs, and minimize product damage. This operational efficiency, paired with environmental benefits, positions RCPBs as a preferred option for companies pursuing both economic and sustainability goals.

Regulatory Pressure and Government-Mandated EPR Frameworks

The rise of Extended Producer Responsibility (EPR) regulations is another significant driver for RCPB adoption, particularly as governments tie financial obligations to packaging sustainability. The U.K. Plastics Packaging Tax, introduced in April 2022, penalizes companies that use less than 30% recycled content, creating financial incentives for businesses to transition to reusable solutions manufactured with recycled inputs. Globally, similar frameworks are accelerating change. India’s Plastic Waste Management (Amendment) Rules, 2022 mandate reuse targets for rigid plastic packaging, directly pushing corporations to adopt durable and reusable packaging formats like RCPBs. These government initiatives not only penalize unsustainable practices but also reward circular packaging models, thereby positioning RCPBs as an essential tool for regulatory compliance. As EPR frameworks expand across Europe, North America, and Asia, RCPBs will see growing demand from businesses aiming to avoid penalties and improve their sustainability credentials.

Integration with IoT for Smart Logistics and Asset Tracking

One of the most impactful opportunities for RCPBs lies in IoT-enabled logistics and asset tracking. Their durability and higher unit value make them ideal candidates for RFID, GPS, and sensor integration. According to a 2024 study, companies equipping returnable transport items (RTIs) with RFID and GPS trackers reduced asset loss rates from 10–15% to as low as 1.5%, significantly lowering replacement costs and improving asset utilization. IoT sensors embedded in RCPBs can also track location, temperature, humidity, and shock exposure, providing real-time visibility for sensitive supply chains like pharmaceuticals, electronics, and fresh produce. By enabling data-driven optimization of return routes, reducing empty miles, and ensuring product safety, smart-enabled RCPBs not only cut operational inefficiencies but also strengthen resilience in global supply chains. This digitalization of reusable packaging will play a pivotal role in advancing Industry 4.0 logistics systems.

Standardization and Pooling Systems for Open-Loop Supply Chains

Another growth opportunity comes from expanding standardized pooling systems for RCPBs across open-loop supply chains. While reusable systems are already well-established in closed-loop operations, scaling them for industries like fresh produce and retail distribution requires collaborative models. Companies such as IFCO are pioneering pooling systems where standardized, reusable containers are shared across growers, distributors, and retailers. IFCO manages collection, washing, and redistribution, creating economies of scale and lowering costs for all participants. A 2024 report from the Sustainable Packaging Coalition emphasized that collaboration and standardization are key to scaling reuse beyond closed loops, making RCPBs widely available and cost-effective. By creating interoperable pools accessible to multiple stakeholders, businesses can dramatically reduce packaging waste while optimizing logistics networks. As industries move toward circular economy targets, open-loop pooling represents a powerful enabler for mainstreaming reusable corrugated plastic boxes in global supply chains.

Competitive Landscape: Leading Reusable Corrugated Plastic Boxes Companies Are Advancing Sustainability, Traceability, and Operational Efficiency

The global RCPB market is shaped by major players leveraging materials science, innovation, and sustainability-focused strategies to deliver high-performance solutions. Top companies are investing in circular economy models, advanced manufacturing, and integrated services to maintain leadership in the reusable packaging sector.

Smurfit Kappa Group: Expanding Global Capabilities Through Strategic Mergers and Sustainable Packaging Solutions

Smurfit Kappa is a global leader in paper-based and reusable corrugated packaging. The September 2024 merger with WestRock enhanced its product portfolio and global reach, supporting the RCPB sector. Its Better Planet 2050 strategy focuses on reducing environmental footprint and advancing circular economy solutions. Smurfit Kappa leverages a vertically integrated business model to serve multiple industries, providing innovative and compliant packaging solutions.

DS Smith Plc: Leveraging Sustainability and Vertical Integration for Reusable Packaging Excellence

DS Smith offers a range of sustainable packaging solutions, including reusable corrugated boxes. In April 2024, International Paper proposed acquiring DS Smith to create a leading presence in North America and EMEA. By December 2024, DS Smith maintained robust financial performance despite market challenges. Its vertical integration, material expertise, and sustainability initiatives position it as a key player in delivering durable, cost-effective RCPB solutions.

Sonoco Products Company: Driving Sustainable Packaging Innovation Across Food and Pharmaceutical Supply Chains

Sonoco provides rigid and flexible packaging solutions for food, personal care, and pharmaceutical sectors. In May 2025, it published its 2024 Corporate Sustainability Report and committed $30 million for adhesives and sealants capacity expansion, aligning with growing demand for eco-friendly packaging solutions. Sonoco’s vertically integrated operations and brand reputation strengthen its capability to provide innovative, high-quality RCPBs globally.

Amcor plc: Pioneering Circular Economy and Flexible Packaging Solutions for Global Supply Chains

Amcor delivers flexible and rigid plastic packaging, including AmLite metal-free laminates and AmPrima™ recycle-ready pouches. In August 2025, it upgraded its UK recycling facility to increase post-consumer recycled content utilization. Amcor is also developing the AmSky™ thermoform blister system, a PVC- and aluminum-free solution. Its strategy emphasizes circular economy, sustainability, and product protection across multiple industries.

Oji Holdings Corporation: Integrating Sustainability and Innovation in Paper-Based Reusable Packaging

Oji Holdings offers paper and pulp products designed for printing, publishing, and reusable packaging applications. Its Oji Way strategic plan focuses on environmental footprint reduction, new material development, and circular economy solutions. Oji Holdings’ vertically integrated model and expertise in sustainable materials allow it to deliver high-quality, compliant RCPB solutions worldwide.

Reusable Corrugated Plastic Boxes Market Share Insights, 2025-2034

Crates & Totes dominate Market Share by Product Type in the Reusable Corrugated Plastic Boxes Market

Crates and totes account for the largest share at 35%, establishing themselves as the workhorses of reusable corrugated plastic packaging. Their dominance is attributed to their unmatched versatility in factories, warehouses, and retail distribution systems, where stackability, nestability, and durability over hundreds of trips deliver superior ROI compared to single-use alternatives. Flap boxes follow with 30%, serving as durable replacements for cardboard, favored for secure closures and efficient palletization that suit closed-loop logistics. Bulk containers represent a key segment for agriculture and industrial supply chains, enabling efficient high-volume handling of produce and loose components where single-item handling is impractical. Sleeves and dividers contribute by protecting fragile, high-value goods like electronics and glass, ensuring product integrity through segregation and cushioning. Layer pads, although the smallest segment, are indispensable for pallet stability and load safety, supporting industries such as food & beverages and electronics where multi-layer palletization is common. Collectively, these product types highlight how versatility, protective performance, and efficiency in reverse logistics shape market share allocation.

Food & Beverages lead Market Share by End-Use Industry in the Reusable Corrugated Plastic Boxes Market

The food & beverages sector leads with 32%, driven by the critical role of reusable corrugated plastic in maintaining hygiene, supporting cold chain logistics, and reducing spoilage for perishables such as fresh produce, dairy, and meat. Automotive follows as a mature and precision-focused user, deploying standardized crates and totes to protect high-value components in just-in-time (JIT) assembly lines while reducing logistics costs. E-commerce and retail represent one of the fastest-growing users, with reusable boxes integrated into fulfillment centers, sortation hubs, and last-mile delivery loops, where durability and branding potential make them superior to disposable cartons. Agriculture remains a core segment, particularly for bulk containers and harvest crates, as the industry transitions from wood and cardboard to Reusable Plastic Containers (RPCs) to reduce waste and improve field-to-shelf efficiency. Electronics manufacturers adopt these boxes for anti-static protection and superior durability, ensuring safe transit of delicate, high-value devices and components. Pharmaceuticals and healthcare, while smaller in volume, demand specialized hygienic, trackable containers designed for sterile environments, supporting compliance in hospital networks and medical supply chains. This distribution highlights how hygiene, durability, and sector-specific precision drive end-use adoption.

European Union: PPWR and Automotive Applications Driving Market Growth

The European Union reusable corrugated plastic boxes market is being redefined by the Packaging and Packaging Waste Regulation (PPWR), which came into effect in February 2025. The regulation introduces sector-specific reuse targets and mandates a reduction in packaging waste per capita by 5% in 2030, 10% in 2035, and 15% in 2040 compared to 2018 levels. This has accelerated the adoption of returnable corrugated plastic boxes across industries, as businesses seek to reduce single-use reliance and comply with EU-wide standards. The EU is also promoting Deposit Return Systems (DRS) to improve collection efficiency and ensure packaging circulates back into the system.

A significant demand driver is the automotive industry, where companies like Karton S.p.A. are developing customized reusable corrugated plastic packaging solutions to optimize supply chain logistics. These solutions improve product flow, cut costs, and support sustainability goals in an intensely competitive market. Meanwhile, Germany’s “reusable packaging obligation”, effective since January 2023, has reshaped foodservice and catering operations by mandating cost-equivalent reusable alternatives to disposables. Further reinforcement comes from the Ecodesign for Sustainable Products Regulation (ESPR), which requires a Digital Product Passport for packaging, ensuring transparency on compliance and product origin. Collectively, these regulations and industry shifts are positioning Europe as a global leader in sustainable, reusable corrugated plastic packaging.

United States: EPR Laws and Local Investments Fueling Reusable Packaging Expansion

The United States reusable corrugated plastic boxes market is advancing under the combined influence of Extended Producer Responsibility (EPR) laws and major investment initiatives. With seven states adopting EPR regulations, including Maryland’s mandate that PROs cover 90% of packaging waste management costs by 2030, manufacturers and distributors are transitioning to durable and recyclable corrugated plastic formats. The U.S. Plastics Pact is also guiding industry alignment with national circular economy targets.

A notable industry move is Saica Group’s $110 million investment in a corrugated manufacturing facility in Anderson, Indiana, underscoring the market’s shift to localized and sustainable production. Trends such as mono-material packaging to simplify recycling streams, and the development of lightweight yet durable packaging for groceries and fresh produce, are gaining traction. Federal support through the Infrastructure Investment and Jobs Act is funding advanced recycling facilities, enhancing the supply chain for reusable packaging. Together, regulatory frameworks and infrastructure investments are ensuring strong growth for returnable corrugated plastic boxes in U.S. retail, logistics, and food distribution networks.

China: Regulatory Pressure and Logistics Giants Accelerating Reuse

In China, the reusable corrugated plastic boxes market is being propelled by stringent government regulations and a booming logistics sector. From June 1, 2025, express delivery companies must prioritize reusable and eco-friendly packaging, creating a direct push for corrugated plastic boxes in parcel logistics. Agencies such as the National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) are implementing strict measures under the 14th Five-Year Plan to reduce plastic pollution.

Logistics giants like JDL Express and SF Express are leading the transition, deploying reusable circulation boxes to replace single-use cardboard. Moreover, Shanghai’s new plastic restriction policy (September 2025) is cracking down on “greenwashing” practices, banning foam bowls, plastic straws, and hybrid containers. With government-backed tax incentives promoting remanufacturing and green technology, China is fostering large-scale adoption of reusable corrugated plastic packaging across e-commerce, retail, and industrial supply chains. This regulatory and industrial alignment is making China a global model for large-scale implementation of reusable transport packaging.

India: EPR Rules and Cold Chain Demand Boosting Adoption

The India reusable corrugated plastic boxes market is being shaped by the Plastic Waste Management (Amendment) Rules, 2024, which emphasize Extended Producer Responsibility (EPR) for producers, importers, and brand owners. While small businesses (MSMEs) are exempt, larger companies face strict compliance obligations. Effective July 1, 2025, all plastic packaging must be traceable via barcodes or QR codes, increasing accountability in packaging waste management. Additionally, from April 1, 2025, PIBOs must integrate a minimum 30% recycled plastic content in rigid plastics, directly influencing the material composition of reusable packaging.

A major driver in India is the growing cold chain sector, particularly for processed foods, dairy, and pharmaceuticals. Reusable corrugated plastic boxes are gaining adoption due to their moisture resistance, durability, and temperature stability, making them well-suited for storage and transport. Combined with strong regulatory pressure and rising consumer demand for packaged goods, India represents a rapidly expanding market for reusable corrugated packaging solutions, with increasing focus on sustainability and compliance-driven innovation.

Japan: Circular Economy Strategy and Bio-Based Packaging Integration

The Japan reusable corrugated plastic boxes market is evolving under the country’s Plastic Resource Circulation Strategy, which mandates that all plastic packaging and goods must be reusable or recyclable by 2025. This regulation, along with the Plastic Resource Circulation Promotion Law (2025), is forcing companies to redesign single-use formats into reusable or compostable alternatives. At the same time, the government aims to double renewable material use by 2030 and enforce waste sorting at collection for improved efficiency.

Leading Japanese companies like Shiseido and Tokiwa Cosmetics are pioneering refillable and reusable packaging systems, influencing broader adoption across industries. In parallel, innovations in bio-polypropylene (bio-PP) and advanced paper-based materials such as Nippon Paper Industries’ SHIELDPLUS are further supporting the transition. With its focus on high-quality, long-lasting packaging, Japan is setting global benchmarks for combining aesthetics, performance, and sustainability in reusable corrugated plastic packaging solutions.

Brazil: PNRS and Reverse Logistics Strengthening Reusable Packaging Systems

The Brazil reusable corrugated plastic boxes market is guided by the country’s National Solid Waste Policy (PNRS), which prioritizes reuse, recycling, and waste reduction across packaging supply chains. Reinforcing this, Law No. 15,088 (January 2025) bans the import of paper, plastic, glass, and metal waste, compelling industries to adopt domestic recycling and reuse practices. The government is also expanding a reverse logistics system, holding producers accountable for post-consumer collection and recycling of packaging.

The policy environment strongly supports the use of reusable corrugated plastic boxes, especially in agriculture, retail distribution, and food logistics, where durability and reusability are critical. Brazil’s push to curb solid waste generation is aligning with increasing adoption of sustainable packaging alternatives, making reusable corrugated plastic solutions a key enabler of supply chain efficiency and environmental compliance.

Reusable Corrugated Plastic Boxes Market Report Scope

Reusable Corrugated Plastic Boxes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.6 Billion

|

|

Market Size (2034)

|

$15.7 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Material Type (PP, PE, PET, Others), By Product Type (Flap Boxes, Bulk Containers, Crates & Totes, Sleeves & Dividers, Layer Pads), By End-Use Industry (Automotive, Food & Beverages, E-commerce & Retail, Electronics, Pharmaceuticals & Healthcare, Agriculture)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Schoeller Allibert, DS Smith Plc, Smurfit Kappa Group Plc, Orbis Corporation, Rehrig Pacific Company, Myers Industries, Inc., Nefab Group, SABIC, Georg Utz AG, Karton S.p.A., Menasha Corporation, Buckhorn Inc., MDI (Minnesota Diversified Industries), IPL Plastics Inc., Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Reusable Corrugated Plastic Boxes Market Segmentation

By Material Type

By Product Type

- Flap Boxes

- Bulk Containers

- Crates & Totes

- Sleeves & Dividers

- Layer Pads

By End-Use Industry

- Automotive

- Food & Beverages

- E-commerce & Retail

- Electronics

- Pharmaceuticals & Healthcare

- Agriculture

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Reusable Corrugated Plastic Boxes Market

- Schoeller Allibert

- DS Smith Plc

- Smurfit Kappa Group Plc

- Orbis Corporation

- Rehrig Pacific Company

- Myers Industries, Inc.

- Nefab Group

- SABIC

- Georg Utz AG

- Karton S.p.A.

- Menasha Corporation

- Buckhorn Inc.

- MDI (Minnesota Diversified Industries)

- IPL Plastics Inc.

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-layered research methodology to deliver actionable insights into the global reusable corrugated plastic boxes (RCPB) market. Our approach combines extensive secondary research, including corporate filings, sustainability reports, industry whitepapers, regulatory frameworks, and trade publications, with primary interviews of packaging manufacturers, logistics operators, distributors, and end-users across automotive, food & beverage, pharmaceutical, e-commerce, and agriculture sectors. We analyze operational metrics such as cost-per-use, product protection, lifecycle durability, and integration with automation and smart logistics systems. Quantitative forecasting models incorporate material innovations, technological advancements (IoT, RFID), regional regulations (EPR, PPWR, Plastic Resource Circulation Laws), and market adoption trends. USDAnalytics also evaluates mergers, acquisitions, and strategic collaborations to map competitive dynamics and growth potential. This methodology enables the assessment of RCPBs’ environmental and financial impact, including ROI, CO2 reduction, and waste minimization, delivering high-value insights for professionals seeking to optimize reusable packaging strategies, enhance supply chain efficiency, and achieve sustainability targets.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.