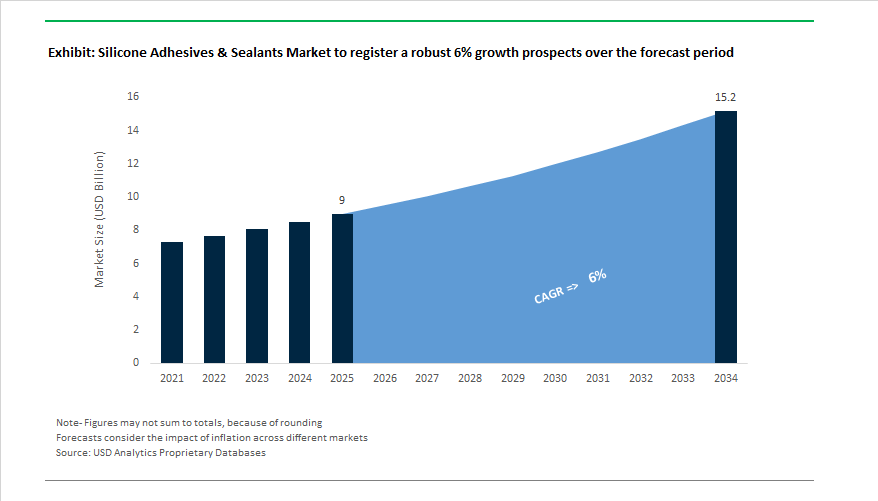

The Global Silicone Adhesives and Sealants Market is projected to grow from $9 billion in 2025 to $15.2 billion by 2034, registering a compound annual growth rate (CAGR) of 6%. The industry is witnessing sustained expansion due to its unique material properties — including thermal stability, flexibility, weather resistance, and dielectric strength — which make silicone-based systems indispensable across construction, automotive, medical, and electronic manufacturing sectors.

Silicone adhesives and sealants are transitioning from commodity “finish” products to specification-driven materials whose chemistry, cure mechanism, and supply footprint materially affect qualification, warranty and lifecycle risk. Leading manufacturers position silicones around a narrow set of non-substitutable performance attributes: long-term elastic recovery under cyclic strain, UV and ozone stability across decades, and a wide continuous service window (commonly quoted from roughly −50°C to +200°C and in some commercial grades up to +300°F/+150°C–200°C depending on system and cure). These material baselines define acceptance criteria for façade glazing, structural glazing, electrical insulation and high-temperature gasketing and are documented in product datasheets across the supplier base.

Contemporary product differentiation is concentrated in formulation and process compatibility rather than gross end-use claims. Suppliers are shipping: neutral-cure and condensation/addition silicones for long-term weathering; UV/visible-curable silicones that provide rapid skin-over plus secondary moisture cure for shadowed geometries; and liquid silicone rubbers (LSRs) that deliver primerless adhesion and USP/ISO biocompatibility for medical assemblies. These options change downstream manufacturing choices — primer steps, cure ovens, line speed, rework windows, and clean-room handling — and therefore belong in procurement specs and DfX reviews, not only in application appendices.

The global silicone adhesives and sealants industry has entered a phase of technological acceleration, sustainability alignment, and regional capacity optimization. Key events indicate a strategic shift by major manufacturers toward eco-innovation, electrification, and digital integration.

In May 2025, Henkel AG & Co. KGaA inaugurated a state-of-the-art Application Engineering Center in Shanghai, designed to accelerate the localization of advanced bonding and sealing solutions for the electronics, mobility, and building sectors. This facility exemplifies Henkel’s strategy of combining regional innovation with process scalability to serve the fast-growing Asia-Pacific manufacturing ecosystem. Similarly, in July 2025, Henkel expanded its automotive logistics base in Chakan, India, supporting localized supply chains for automotive bonding and powertrain sealing solutions amid the region’s strong EV adoption trend.

In the same month (May 2025), Shin-Etsu Chemical Co., Ltd. launched a new set of eco-friendly silicone sealant formulations, emphasizing low-VOC and solvent-free compositions to align with global green building certification systems. The company’s product focus reflects an accelerating market preference for environmentally sustainable silicones capable of maintaining performance integrity under harsh conditions while reducing carbon footprints.

From the materials innovation front, Dow Inc. introduced a bio-based silicone emulsion (August 2024) containing over 80% renewable content, demonstrating leadership in circular economy-focused silicone chemistry. In August 2024, Dow’s new silicone-modified polyester resin won a prestigious R&D innovation award, validating its performance in heat-resistant and durable coatings. This underlines Dow’s push toward long-lasting and energy-efficient silicone systems for architectural and industrial coatings.

3M Company advanced its medical technology focus by launching Hi-Tack Silicone Adhesive Tapes for wearable medical devices such as continuous glucose monitors (CGMs). These solutions are designed for strong, skin-safe adhesion with sterilization compatibility, reinforcing the growing medical-grade silicone adhesives segment.

In February 2025, the market experienced a notable R&D milestone when Momentive Performance Materials highlighted its SilCool thermal management silicones, integral for EV battery systems and ADAS sensors, marking the convergence of silicone chemistry with the electrification revolution. Meanwhile, industry dynamics were influenced by raw material constraints in early 2025, with global silicone spot prices rising due to chlor-alkali feedstock shortages and logistics bottlenecks, prompting several formulators to reassess sourcing strategies and cost structures.

Market Trend 1: Accelerated Shift to UV and Dual-Cure Silicone Systems for High-Throughput Electronics Manufacturing

The growing complexity and volume of electronic assemblies, power modules, and display technologies are driving the widespread shift toward UV-curable and dual-cure (UV + heat/moisture) silicone formulations. These systems enable rapid processing while maintaining high-performance bonding and insulation characteristics, crucial for automotive, semiconductor, and consumer electronics sectors.

Modern UV/dual-cure silicones allow exposed sections to achieve fixture strength in as little as five seconds upon UV irradiation, followed by secondary curing in shadowed regions via moisture or heat—eliminating production bottlenecks historically associated with RTV cure times of up to 24 hours. The innovation dramatically increases manufacturing throughput, particularly for complex assemblies like automotive display modules, flexible PCBs, and high-density power units.

Leading electronics manufacturers and material suppliers are integrating optically clear silicone resins (OCRs) with greater than 99% transmittance and <0.1% haze, ideal for high-precision display bonding in electric vehicles, wearables, and smartphones. Further, studies have confirmed that thermally conductive, fast-curing silicone encapsulants can reduce component heat stabilization time from nearly two hours to under 20 minutes, highlighting their superior role in thermal regulation and production efficiency. The convergence of UV speed, optical precision, and dual-cure reliability is positioning these silicones as a foundation for next-generation electronics encapsulation and protection.

Market Trend 2: Reformulation Toward Catalyst-Free and Ultra-Pure Silicone Systems for Sensitive Medical and Optical Applications

Stringent purity requirements across semiconductor, optical, and biomedical sectors are propelling the transition from platinum-catalyzed systems to non-platinum and clean-cure chemistries, such as tin-catalyzed condensation and oxime-based neutral cure silicones. These next-generation materials minimize contamination risk, improve biocompatibility, and eliminate the potential for substrate interaction or cure inhibition—an essential attribute in implantable devices and cleanroom environments.

For medical and pharmaceutical applications, non-platinum-cure silicones produce no volatile organic byproducts, ensuring compatibility with direct-contact devices, drug delivery systems, and neuroprosthetic interfaces. Products utilizing such formulations are already marketed for neuroscience applications, where hydrogen is the only byproduct, demonstrating near-zero toxicity.

In optical bonding, tin-catalyzed systems are gaining favor for their stability and low viscosity, enabling defect-free encapsulation in camera modules, medical sensors, and photonic devices. Simultaneously, USP Class VI and ISO 10993-certified medical-grade silicones with addition-type curing mechanisms are being introduced, ensuring cytotoxicity-free performance for implantables and ophthalmic devices. For industrial applications, oxime-cure silicones have emerged as the preferred neutral systems for corrosion-free sealing of sensitive electronic assemblies, balancing fast cure speed with excellent moisture resistance.

Market Opportunity 1: Engineering Thermally Conductive yet Electrically Insulating Silicones for Electric Vehicle Power Module Potting

The exponential growth in electric vehicle (EV) production is catalyzing a major materials innovation wave focused on thermally conductive but electrically insulating silicone encapsulants. These materials serve as essential components for EV power modules, inverters, battery packs, and charging infrastructure, enabling efficient heat dissipation while maintaining superior dielectric protection.

Empirical data reports that potting a power inductor with a 4.0 W/m∙K thermally conductive silicone can reduce internal heat rise by nearly 50°C compared to standard 0.1 W/m∙K insulating materials, substantially enhancing component reliability and energy efficiency. Advanced formulations, such as those introduced by major manufacturers, achieve dielectric strengths ≥20 kV/mm, ensuring high-voltage isolation essential for onboard chargers and inverter modules.

The latest two-component gap filler silicones demonstrate thermal conductivities up to 6.0 W/m∙K, combining rapid dispensing capability with reworkability for automated manufacturing environments. Their operational temperature range—from −60°C to +250°C—enables stable performance under extreme thermal cycling, aligning perfectly with under-the-hood EV applications. As automotive electrification accelerates globally, the development of next-generation high-durability, heat-conductive silicones represents a critical opportunity for manufacturers to support both thermal management and lightweight component integration.

Market Opportunity 2: Development of High-Refractive-Index (HRI) Optically Clear Silicone Adhesives for Augmented Reality (AR) and Advanced Optics

The emerging Augmented Reality (AR) and Mixed Reality (MR) markets are opening a high-value frontier for the silicone adhesives sector through the design of high-refractive-index (HRI) optically clear silicones used in waveguide bonding and optical interconnects. These advanced materials are engineered to enhance light transmission, reduce scattering, and improve color uniformity—all critical parameters for the performance of AR headsets and next-generation displays.

Recent patents detail the development of elastomeric polymer blends with low molecular weight additives, achieving refractive indices above that of standard 1.41 silicone baselines. Concurrently, phenyl-functionalized silicone gels—marketed as HRI encapsulants—are offering higher optical density while maintaining transparency and flexibility, optimizing light coupling efficiency in compact waveguide systems. Commercial silicone adhesive films already demonstrate 100% light transmission and low haze (0.34%), setting an industry benchmark for optical clarity that future HRI products aim to exceed.

Academic advancements in Silicon Carbide (SiC) waveguide structures—which weigh as little as 3.795 g per optical layer—highlight the urgent need for compatible, ultra-clear HRI bonding materials. These adhesives must seamlessly integrate with nanoimprinted AR substrates, ensuring mechanical stability and optical continuity without adding weight or distortion. As AR adoption scales across consumer and enterprise applications, high-index optical silicone adhesives are poised to become one of the most disruptive material technologies within the global display and photonics ecosystem.

Silicone Adhesives & Sealants Market Share Insights, 2025-2034

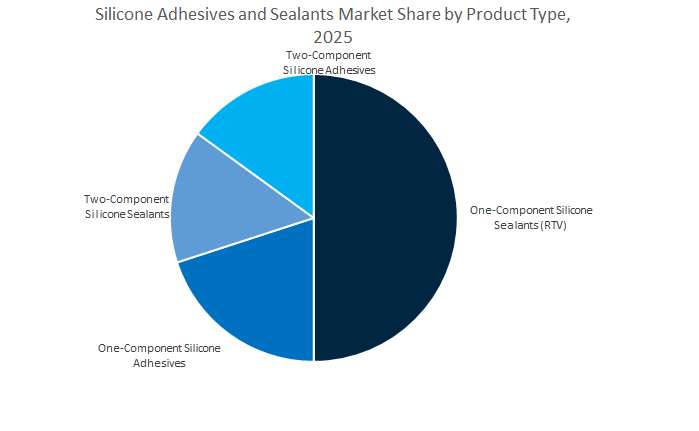

Market Share by Product Type

One-Component Silicone Sealants (RTV) dominate the global silicone adhesives and sealants industry, holding an estimated 49.4% market share by 2025. This dominance is attributed to their versatility, ease of application, and excellent weathering resistance, making them indispensable in construction, automotive, and general industrial sealing applications. The “ready-to-use” nature of room temperature vulcanizing (RTV) systems eliminates the need for mixing, enabling faster application and reducing labor costs across large-scale infrastructure and renovation projects. Their superior performance in moisture-curing environments, along with excellent adhesion to a wide range of substrates — including glass, aluminum, plastics, and ceramics — has cemented their use in structural glazing, window sealing, and façade systems. Moreover, the construction industry's continued shift toward low-VOC and energy-efficient building materials further reinforces the adoption of RTV silicone sealants as they offer long service life, flexibility, and compliance with green building standards such as LEED and BREEAM.

One-Component Silicone Adhesives maintain a strong secondary position, serving diverse end-use sectors where fast assembly, vibration resistance, and thermal endurance are essential. These adhesives are extensively used in automotive components, consumer electronics, and general industrial assembly, offering manufacturers reliable solutions for bonding dissimilar materials under dynamic stress conditions. Two-Component Silicone Sealants and Adhesives, while representing smaller market shares, are crucial for high-performance and technical applications. Their deep section curing capabilities, chemical stability, and controlled processing characteristics make them indispensable in electronics potting, aerospace, and industrial sealing operations. As industries move toward automation and precision bonding, two-component systems are gaining traction in electric vehicles (EVs) and semiconductor packaging, driven by the need for enhanced thermal management and material compatibility.

Market Share by End-Use Industry

The Building & Construction sector dominates the global silicone adhesives and sealants market, accounting for 42.5% of total market share in 2025, underscoring its foundational role in global infrastructure and real estate development. Silicone sealants are indispensable for structural glazing, weatherproofing, expansion joints, and curtain wall systems, providing long-term resistance to UV radiation, temperature extremes, and moisture ingress. The increasing global emphasis on sustainable and energy-efficient buildings has boosted demand for high-durability, low-emission silicone formulations that contribute to extended service life and reduced maintenance costs. Rapid urbanization in emerging economies, coupled with the rise of smart city initiatives and prefabricated construction systems, continues to fuel the sector’s reliance on high-performance silicone sealants. In residential and commercial applications, their flexibility and adhesion to multiple substrates make silicones the preferred material for bathroom, kitchen, and façade sealing applications, further consolidating their leadership position.

The Electrical & Electronics industry represents the second-largest segment, benefiting from silicones’ dielectric strength, heat resistance, and chemical stability. They are critical in potting, encapsulation, and conformal coating processes for protecting delicate components from moisture and mechanical shock. The rise of electric vehicles, 5G devices, and renewable energy systems has accelerated demand for silicone adhesives in battery modules, sensors, and circuit assemblies. The Transportation sector, encompassing automotive, aerospace, and marine industries, is another key market driver, leveraging silicone materials for bonding windshields, sealing gaskets, and reducing NVH (Noise, Vibration, Harshness) while meeting rigorous temperature and durability standards. Meanwhile, Industrial Assembly and Healthcare applications demand specialized silicone systems designed for medical-grade biocompatibility, sterilization resistance, and flexible bonding in medical devices, implants, and wearables. ental conditions.

The Global Silicone Adhesives and Sealants Market is highly consolidated, with leading multinational players including Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Henkel AG & Co. KGaA, and Momentive Performance Materials Inc. dominating global supply. These companies focus on vertical integration, application-specific innovation, and regional manufacturing optimization to maintain market leadership.

Dow Inc. continues to lead the market through its DOWSIL™ product line, offering premium silicone sealants and adhesives for mobility, electronics, and construction. In 2024, Dow secured four R&D 100 Awards for its pioneering work in mechanical and materials innovations, including a bio-based silicone emulsion containing 81% renewable content. Its silicone portfolio enhances power cable jackets, flexible waterproof coatings, and dielectric encapsulants for demanding industrial environments. Dow’s long-term strategy centers on material circularity, reduced carbon emissions, and product longevity, reinforcing its leadership in sustainable silicone technology.

Wacker Chemie AG, the world’s second-largest silicone producer, operates one of the most vertically integrated silicone value chains — from silicon metal and siloxane production to finished compounds. Its ELASTOSIL® and SILPURAN® lines address specialized markets such as medical implants, healthcare devices, and structural construction. Certified for USP Class VI biocompatibility, Wacker’s medical silicones offer superior sterilization stability and tear resistance, vital for surgical and diagnostic applications. The company’s solid silicone rubber (HCR) solutions serve injection and compression molding, ensuring flexibility for diverse manufacturing processes across industrial sectors.

Shin-Etsu Chemical continues to expand its footprint in functional silicone materials, reporting a 17.7% increase in operating income in FY2024 driven by high-value electronics and specialized silicones. The company’s focus on thermal interface materials (TIMs) for electric vehicles and semiconductors reinforces its position as a key enabler of AI-driven and electrified manufacturing. Its R&D investments in material-device integration and sustainable elastomers ensure its competitiveness in both high-performance and environmentally responsible silicone products.

Henkel’s Adhesive Technologies division, generating over €10 billion in 2024 sales, remains the global leader in industrial adhesives and sealants. Its silicone portfolio serves diverse applications — from construction weatherproofing to electronics encapsulation and automotive bonding. The launch of Henkel’s Shanghai Application Engineering Center (May 2025) marks a pivotal move toward localized R&D and faster technology deployment. Henkel’s strategic pillars—electrification, sustainable building, and circular design—reflect its transformation into a technology-driven adhesive powerhouse focused on mobility and green infrastructure.

Momentive maintains a deep specialization in automotive electronics and thermal management silicones, particularly through its SilCool™ product series. These materials provide low-stress protection, high adhesion, and superior heat dissipation for ADAS sensors, EV batteries, and high-voltage assemblies. With fully vertically integrated manufacturing, Momentive controls its process from base silicone to finished formulation, ensuring reliability and consistency. Its innovation efforts in low-modulus encapsulants and high-temperature sealants place it at the forefront of automotive electrification and next-generation connectivity systems.

United States: Energy-Efficient Construction and Medical Innovation Driving Silicone Adhesive Evolution

The US Silicone Adhesives and Sealants Market size is estimated at $1570 Million in 2025. The US market is anchored by strong demand from sustainable construction, high-tech industries, and medical device innovation. A notable breakthrough occurred in 2024 when 3M Company launched a long-duration silicone medical adhesive that adheres to skin for up to 28 days, surpassing the previous 14-day benchmark and enabling greater patient comfort for wearable health technologies and monitoring devices. The innovation underscores the growing integration of biocompatible silicone chemistries in healthcare-grade adhesive applications.

In the construction segment, over USD 139 billion in energy retrofit projects is catalyzing the use of low-VOC neutral-cure silicone sealants that comply with LEED and BREEAM certification requirements. The sealants enhance energy efficiency in retrofitted buildings, providing long-term air and moisture barriers. The DIY renovation boom, with nearly 67% of U.S. homeowners preferring renovation over relocation, continues to drive consumption of mold- and mildew-resistant silicone grades used in kitchens and bathrooms. Additionally, the acquisition of a U.S.-based flooring adhesives firm by Sika AG reinforces the nation’s strong demand for interior bonding and sealant systems in flooring and architectural finishes.

Europe Silicone Adhesives and Sealants Market Size Outlook

Europe Silicone Adhesives and Sealants Market continue to offer significant business potential with $2094 Million sales revenue in 2025. In Europe, the silicone adhesives and sealants market is shaped by strict sustainability regulations, growing adoption in green building projects, and increasing demand from the medical and aerospace sectors. Countries such as Germany, France, and the UK are leading in innovation, with a focus on solvent-free, low-VOC, and recyclable silicone formulations to meet EU environmental directives. The automotive industry’s shift toward lightweight materials and electric mobility is also accelerating demand for advanced silicone-based bonding solutions. However, challenges such as high production costs, regulatory compliance under REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals), and supply chain disruptions due to geopolitical tensions impact market growth.

Germany: Sustainability and E-Mobility Strengthening Europe’s Silicone Sealant Competitiveness

Germany’s silicone adhesives and sealants industry stands as a cornerstone of Europe’s high-performance materials ecosystem, underpinned by the country’s deep chemical expertise, engineering precision, and sustainability mandates. Wacker Chemie AG, a global leader headquartered in Germany, continues to dominate through its Wacker Silicones division, which now encompasses more than 2,800 products tailored for automotive, construction, and industrial sectors. Wacker’s commitment to low-carbon manufacturing and closed-loop recycling reinforces Germany’s position at the forefront of sustainable adhesive chemistry.

The ongoing electric mobility revolution across Europe is significantly driving demand for silicone adhesives in battery module sealing, structural bonding, and dielectric insulation. German automakers and Tier-1 suppliers are investing heavily in high-temperature and flame-retardant silicone solutions to enhance EV performance and passenger safety. Additionally, Germany’s stringent building codes and energy efficiency regulations (EnEV) have led to strong demand for long-life, elastic silicone sealants in façade sealing and glazing applications. The integration of advanced hybrid polymer systems and low-VOC elastomeric formulations further aligns with EU sustainability directives, ensuring Germany remains a technological leader in silicone-based engineering materials.

France: Arkema and Bostik Leading in E-Mobility and Sustainable Silicone Solutions

France remains a strategic innovation center for high-value silicone adhesives, led by Arkema S.A. and its Bostik division, both of which are advancing specialty applications in electronics, e-mobility, and sustainable construction. In March 2023, Arkema’s acquisition of Polytec PT GmbH, a leader in battery and electronics adhesives, marked a major step in strengthening its silicone bonding portfolio for thermal management, encapsulation, and EV battery protection systems.

Additionally, Bostik launched Supergrip SG6518 and SG6520, two Hot-Melt Polyurethane Reactive (HMPUR) adhesives, expanding its offering in high-performance woodworking and edge-banding applications. The innovations align with France’s and the EU’s push for low-VOC, solvent-free adhesive technologies under tightening environmental standards. French manufacturers are at the forefront of oxime-free silicone sealant development, targeting sustainable façade and structural glazing systems for green-certified buildings. France’s integration of specialty chemicals expertise with circular economy principles is solidifying its position as a leader in advanced, eco-friendly silicone adhesive technologies across Europe and global export markets.

Asia Pacific Regional Developments Defining the Global Silicone Adhesives and Sealants Industry

China: Infrastructure Acceleration and EV Growth Cement China’s Leadership in Silicone Sealants

China remains the largest market for silicone sealants and adhesives in the Asia-Pacific region, driven by its massive infrastructure buildout, expanding industrial base, and rapid advancement in electric mobility and smart manufacturing. The National Development and Reform Commission (NDRC) has allocated approximately CNY 4 trillion (USD 0.56 trillion) for infrastructure upgrades through 2030. The investments encompass urban pipeline systems, industrial facilities, and energy-efficient buildings, all of which heavily rely on neutral-cure silicone sealants for UV resistance, waterproofing, and structural integrity. Unlike acrylics, silicone-based products are preferred for their long lifespan and superior weather resistance, especially in large-scale curtainwall and glazing projects.

China’s chemical manufacturing investment growth of 8.9% (2024) further strengthens the supply of raw materials required for high-performance silicone elastomers, ensuring self-sufficiency and cost control. The construction boom continues to drive the adoption of silicone sealants with 20-year weathering warranties, particularly for skyscrapers and public infrastructure. In parallel, the government’s E-mobility push, through EV and battery manufacturing incentives, is fueling demand for fast-curing silicone adhesives with tack-free times below 10 minutes, enabling efficient automated assembly in battery production lines. The alignment between policy-driven infrastructure expansion and industrial innovation firmly positions China as a strategic global hub for advanced silicone-based adhesive systems.

Japan: Advanced Silicone Chemistry for Electronics and High-Tech Manufacturing

Japan continues to lead the high-purity silicone adhesives and sealants market, emphasizing precision engineering, electronics miniaturization, and advanced materials science. Shin-Etsu Chemical Co., Ltd., Japan’s largest silicone manufacturer, remains a global benchmark for functional silicone materials used in electronics, automotive, and healthcare sectors. With over 5,000 silicone product variants, Shin-Etsu’s Functional Materials division delivers innovations ranging from optical encapsulants and heat-resistant coatings to semiconductor-grade silicone gels with ultra-low impurity levels.

In early 2025, Wacker Chemie AG expanded its specialty silicone production capacity in Japan and South Korea, reinforcing its commitment to serve Asia’s booming automotive and electronic component markets. The region’s semiconductor and display manufacturing sectors continue to rely on high-performance silicone adhesives with precise dielectric and thermal stability properties. Japan’s commitment to R&D excellence and strict quality standards ensures its continued leadership in high-specification silicone technologies that support next-generation consumer electronics, EVs, and advanced robotics.

India: Expanding Domestic Manufacturing and Construction-Driven Demand

India represents one of the fastest-growing markets for silicone adhesives and sealants, driven by rapid industrialization, infrastructure modernization, and expanding manufacturing capacity. With the nation’s manufacturing value reaching USD 461.38 billion in 2024, the demand for ISO-10993-compliant silicones for machinery assembly, electronics, and medical applications continues to rise. Alstone Industries, India’s first domestic producer of silicone sealants, utilizes German technology at its Rajasthan facility to supply both general-purpose and weatherproofing sealants, reducing the nation’s reliance on imports.

Further growth is supported by joint ventures such as McCoy Soudal, a 50:50 partnership with Belgium’s Soudal Group, which focuses on introducing global-standard adhesive and sealant technologies to the Indian market. Large-scale housing and infrastructure initiatives, including the Pradhan Mantri Awas Yojana (PMAY), continue to boost the need for durable construction-grade silicone sealants in waterproofing, glazing, and expansion joint applications. India’s emerging role as a regional manufacturing hub and its focus on sustainability and localization are expected to accelerate adoption of low-VOC, high-strength silicone formulations across construction and industrial markets.

Silicone Adhesives & Sealants Market Report Scope

Silicone Adhesives & Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9 Billion

|

|

Market Size (2034)

|

$15.2 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Product Type (Silicone Adhesives, Silicone Sealants), By Technology (Room Temperature Vulcanizing, Pressure Sensitive Adhesives, Heat/Thermal Curing, Radiation Curing, Ambient Temperature Vulcanizing), By End-Use Industry (Building & Construction, Transportation, Electrical & Electronics, Healthcare, Packaging, Consumer Goods & DIY, Industrial Assembly), By Chemistry- Sealants (Neutral, Oxime, Alkoxy, Acetone, Acid

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, The DOW Chemical Company, Wacker Chemie AG, Sika AG, Shin-Etsu Chemical Co., Ltd., 3M Company, H.B. Fuller Company, Arkema Group (Bostik SA), Elkem ASA, Momentive Performance Materials Inc., Huntsman Corporation, Mapei S.p.A., RPM International Inc., Illinois Tool Works Inc. (ITW), Avery Dennison Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

- Silicone Adhesives

- Silicone Sealants

By Technology

- Room Temperature Vulcanizing

- Pressure Sensitive Adhesives

- Heat/Thermal Curing

- Radiation Curing

- Ambient Temperature Vulcanizing

By End-Use Industry

- Building & Construction

- Transportation

- Electrical & Electronics

- Healthcare

- Packaging

- Consumer Goods & DIY

- Industrial Assembly

By Chemistry/Cure Type - for Sealants

- Neutral

- Oxime

- Alkoxy

- Acetone

- Acid

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Silicone Adhesives and Sealants Market

- Henkel AG & Co. KGaA

- The DOW Chemical Company

- Wacker Chemie AG

- Sika AG

- Shin-Etsu Chemical Co., Ltd.

- 3M Company

- H.B. Fuller Company

- Arkema Group (Bostik SA)

- Elkem ASA

- Momentive Performance Materials Inc.

- Huntsman Corporation

- Mapei S.p.A.

- RPM International Inc.

- Illinois Tool Works Inc. (ITW)

- Avery Dennison Corporation

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Silicone Adhesives and Sealants Market, connecting demand inflection points in EV platforms, high-performance building envelopes, and clean-manufacturing healthcare to chemistry breakthroughs in UV/dual-cure systems, biocompatible grades, and thermally conductive yet dielectric formulations; our analysis reviews competitive moves, raw-material volatility, and compliance dynamics (low-VOC, ISO 10993/USP VI), and highlights how next-gen silicones are displacing legacy chemistries in heat, weathering, and high-voltage environments—this report is an essential resource for product strategists, sourcing leaders, and engineering teams who need defensible sizing, specification-level benchmarks, and a 2025–2034 opportunity map aligned to electrification and green-building mandates.

Scope Highlights

Segmentation:

- By Product Type: Silicone Adhesives; Silicone Sealants.

- By Technology: Room Temperature Vulcanizing; Pressure Sensitive Adhesives; Heat/Thermal Curing; Radiation Curing; Ambient Temperature Vulcanizing.

- By End-Use Industry: Building & Construction; Transportation; Electrical & Electronics; Healthcare; Packaging; Consumer Goods & DIY; Industrial Assembly.

- By Chemistry/Cure Type – for Sealants: Neutral; Oxime; Alkoxy; Acetone; Acid.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis / profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.