Specialty Pulp and Paper Chemicals Market Valuation 2025–2034: $25.4 Billion to $34.6 Billion at 3.5% CAGR Anchored in Strength Resins, Retention Aids, and Low-Carbon Process Chemistry

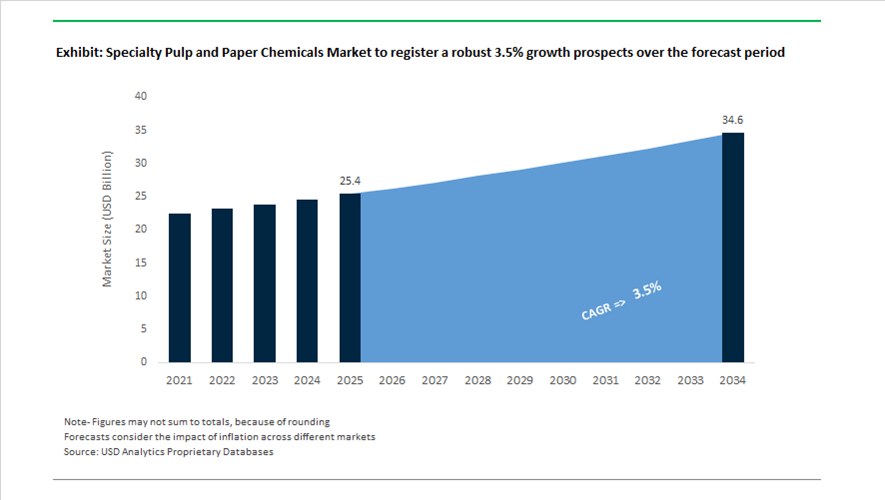

The global specialty pulp and paper chemicals market is valued at $25.4 billion in 2025 and is projected to reach $34.6 billion by 2034, expanding at a CAGR of 3.5%. Growth is supported by sustained demand for wet-strength resins, dry-strength agents, retention and drainage aids, sizing chemicals, bleaching agents, coating binders, and process water treatment solutions across packaging grades, tissue, specialty papers, and BCTMP pulp production. The market is transitioning toward biomass-balanced chemistries, ISCC-certified inputs, digital process optimization, and low-carbon papermaking platforms as mills focus on fiber yield improvement, water reuse efficiency, and Scope 1–3 emission reductions.

Portfolio rationalization began in early 2024 when Kemira finalized the $280 million divestment of its Oil & Gas business, sharpening its strategic focus on pulp & paper and water treatment chemistries. In January 2024, Ecolab inaugurated a 3,000-square-meter manufacturing plant in Vietnam, strengthening supply of specialty papermaking and microelectronics water treatment chemicals across Southeast Asia. In early 2024, Kemira launched the industry’s first biomass-balanced, ISCC-certified wet-strength resins, enabling packaging producers to reduce fossil-carbon content while maintaining tensile performance. During Q3 2024, Nouryon reorganized into three business segments, establishing the Resource Solutions division to prioritize investment in renewable fiber and sustainable pulp chemical innovations.

Innovation and regional capacity expansion accelerated in 2025. In early 2025, Solenis introduced PerForm™ SP 4715 KR, a high-efficiency retention and drainage aid implemented in collaboration with Saudi Paper Manufacturing, reducing chemical consumption and cutting Scope 3 CO2 emissions by over 330,000 kg annually. In March 2025, Kemira announced a multi-million Euro investment to expand strength chemical production lines at its Wellgrow, Thailand site, with implementation targeted for early 2026 and capacity reaching 100,000 tons by August 2026. In July 2025, Pritzker Private Capital completed its acquisition of Buckman Laboratories, positioning the company to scale digital “smart technology” platforms that integrate real-time papermaking analytics with specialty process chemistry. In August 2025, Buckman Laboratories and Atul Ltd formed a joint venture to supply advanced process chemicals and water treatment solutions to Indian and Sri Lankan paper mills through localized manufacturing.

Technology integration and circular chemistry initiatives intensified into 2026. In early 2025, BASF started operations at its commercial loopamid® facility in Shanghai, introducing depolymerization technology adaptable for high-purity paper coating applications. JK Paper is commissioning a 125,000 ADMT BCTMP mill in Gujarat during 2025–2026, increasing reliance on advanced bleaching, refining, and strength chemicals to optimize fiber yield and brightness. In December 2025, Nalco Water and ANDRITZ announced a strategic collaboration at the Tissue Innovation and Application Center in Austria to accelerate dry-end specialty chemical development for tissue manufacturing efficiency. These developments in ISCC-certified resins, retention aid efficiency, strength chemical capacity expansion, digital papermaking platforms, and circular coating technologies are shaping the specialty pulp and paper chemicals market through 2034.

Key Trends and High-Impact Opportunities in the Specialty Pulp and Paper Chemicals Market

Accelerated Transition to PFAS-Free Barrier and Wet-Strength Chemistries

The Specialty Pulp and Paper Chemicals Market is undergoing a structural inflection as PFAS elimination shifts from voluntary commitments to enforceable regulatory deadlines. Effective June 2025, the U.S. Food and Drug Administration finalized the phase-out of 35 perfluoroalkyl grease-proofing substances used in food-contact materials. This decision has triggered an industry-wide reformulation cycle, compelling paper mills and chemical suppliers to replace fluorochemical barriers with polysaccharide-based systems, silicone-modified polymers, and next-generation wet-strength resins that meet food safety and recyclability criteria.

Strategic product innovation is accelerating to close the historical performance gap between PFAS and non-fluorinated alternatives. At the K 2025 trade fair in June 2025, Clariant introduced its AddWorks PPA manufacturing line, positioning PFAS-free polymer processing aids as scalable, mill-ready solutions. In parallel, Cargill and BASF are expanding starch-derived chemistries and Alkyl Ketene Dimer derivatives that deliver grease resistance and fiber bonding suitable for high-throughput QSR packaging lines.

Volume dynamics underscore the non-discretionary nature of this shift. Industry estimates for 2025 project PFAS-free specialty chemical demand in North America and Europe to reach approximately 244.32 kilotons, driven by state-level bans in California and Washington and reinforced by the EU Packaging and Packaging Waste Regulation, which mandates PFAS thresholds of 25 ppb by August 2026. As compliance windows narrow, PFAS-free chemistries are becoming baseline specifications rather than premium options.

Enzymatic Fiber Engineering to Enable High PCR Content Paper Grades

Rising commitments to post-consumer recycled content are transforming enzyme adoption from a cost-optimization tool into a core production requirement. Specialty depolymerization enzymes, particularly xylanases and cellulases, are being deployed to re-engineer fiber architecture in low-quality recycled pulp, restoring tensile strength, improving drainage, and stabilizing formation at higher machine speeds. This enzymatic approach enables mills to meet aggressive PCR targets without sacrificing runnability or end-product performance.

Operational data from late 2025 highlights the commercialization of AI-engineered enzyme systems capable of selectively degrading contaminants such as stickies and residual ink particles. These targeted biocatalysts reduce chemical deinking intensity, lower bleaching chemical consumption, and help mills maintain premium brightness even at 100% recycled fiber input. The result is a measurable reduction in variable operating costs alongside improved yield and consistency.

Capital allocation trends further validate this shift. The global market for enzymes in pulp and paper applications is projected to reach $2.4 billion by 2032, with Asia-Pacific leading capacity integration. New and expanded mills in China and India are embedding enzymatic bleaching and deinking suites as standard infrastructure, reflecting a long-term strategy to minimize chlorine dependency while maximizing fiber recovery in increasingly constrained raw material markets.

Bio-Based Acrylic Binders and Functional Coatings for Plastic Replacement

The accelerating move toward plastic-free cups, cartons, and foodservice packaging is opening a high-growth opportunity for bio-based acrylic binders and mineral-enhanced barrier coatings. These chemistries are designed to replicate the heat-sealability, moisture resistance, and grease performance of polyethylene coatings while remaining fully repulpable within existing recycling systems.

In January 2025, Arkema launched a dedicated line of bio-based acrylic binders aimed at reducing Product Carbon Footprint in technical paper applications. Derived from renewable plant oils and starch feedstocks, these binders form continuous barrier films that do not contaminate fiber recovery streams. Performance benchmarks from recent studies indicate that advanced bio-coatings, including chitosan-based systems and starch-graft-polydimethylsiloxane copolymers, can achieve Kit ratings of 12 out of 12 for oil resistance. This level of barrier performance positions fiber-based substrates as credible replacements for synthetic films in premium food, beverage, and beauty packaging.

Specialty Chemical Programs for Zero Liquid Discharge Mill Operations

Water scarcity and tightening discharge regulations are accelerating adoption of Zero Liquid Discharge systems across pulp and paper manufacturing hubs. By 2025, advanced ZLD configurations are enabling mills to reduce freshwater intake by up to 95%, fundamentally altering the chemistry of closed-loop water circuits. As dissolved solids and organic salts concentrate, demand is rising sharply for high-performance deposit control chemicals, non-oxidizing biocides, and membrane-compatible antiscalants.

Hybrid ZLD architectures deployed by technology providers such as SUEZ Asia and Aquatech integrate membrane brine concentrators that lower energy consumption by approximately 30%. However, these systems require chemical programs capable of operating at extreme pH levels and salinities without fouling reverse osmosis membranes or crystallizers.

Regulatory incentives are amplifying this opportunity. In May 2025, China’s Ministry of Ecology and Environment introduced targeted incentives for industries implementing ZLD technologies, catalyzing demand for high-purity dispersants and antiscalants tailored to closed-loop mill environments. For specialty chemical suppliers, ZLD-driven water treatment represents a durable, regulation-backed growth avenue with high technical barriers and recurring revenue potential.

Specialty Pulp and Paper Chemicals Market Share and Segmentation Insights

Functional Chemicals Lead the Specialty Pulp and Paper Chemicals Market Through Performance Enhancement

Functional chemicals accounted for 48.60% of the specialty pulp and paper chemicals market in 2025, reflecting their critical role in determining the final performance characteristics of paper products. These chemicals include sizing agents, dry and wet strength additives, dyes, pigments, and optical brighteners, which enhance properties such as strength, water resistance, brightness, and color stability. Their use allows paper manufacturers to tailor products for specific applications including packaging, tissue, and printing grades. A major 2025 industry driver is the expansion of paper-based packaging materials, where functional chemicals are essential for improving barrier properties, mechanical strength, and printability required for containerboard, cartonboard, and specialty packaging papers.

Packaging and Industrial Applications Drive Demand for Pulp and Paper Chemicals

Packaging and industrial applications represent the largest segment in the specialty pulp and paper chemicals market, accounting for 42.80% of global demand in 2025 due to the rapid growth of paper-based packaging materials. Paper grades such as containerboard, folding cartonboard, and industrial specialty papers require functional chemicals to achieve structural strength, moisture resistance, and printing compatibility. The expansion of e-commerce logistics and sustainable packaging initiatives continues to increase demand for high-performance packaging papers. A key 2025 industry trend is the rising use of recycled fiber in packaging production, where higher recycled content requires increased levels of strength additives, sizing agents, and processing chemicals to maintain paper quality and meet performance standards.

Specialty Pulp and Paper Chemicals Market Competitive Landscape

The specialty pulp and paper chemicals market in 2026 is shaped by functional sustainability, closed-loop water systems, and high-performance barrier coatings. Leading players are prioritizing strength additives for recycled fiber, PFAS-free packaging solutions, and AI-driven process optimization to enhance mill efficiency, regulatory compliance, and circular economy adoption.

Solenis Expands Digital-Chemical Ecosystem Through NCH Acquisition and Barrier Coating Innovation

Solenis is strengthening its leadership in specialty pulp and paper chemicals through aggressive M&A and integrated solution delivery. The 2025 acquisition of NCH Corporation expands its global reach across 24 manufacturing plants and enhances its on-site technical service model. Following the integration of Diversey, Solenis combines hygiene technologies with paper process chemicals for food-grade packaging and tissue applications. Its 2025 innovation pipeline includes PFAS-free barrier coatings designed to replace poly-laminate structures with recyclable fiber-based alternatives. Under Platinum Equity, the company is advancing digital-chemical convergence through real-time monitoring and digital twin technologies for water circuit optimization. This integrated approach positions Solenis as a one-stop provider for water treatment chemicals, functional coatings, and process efficiency solutions.

Kemira Accelerates Green Transformation with PHA Barrier Coatings and Advanced Water Treatment Solutions

Kemira is reinforcing its competitive position through renewable chemistry and water treatment innovation in pulp and paper chemicals. The company’s 2026 investment in a Swedish activated carbon reactivation plant strengthens its PFAS removal capabilities in industrial effluents. Its partnership with Bluepha focuses on scaling PHA-based barrier coatings for sustainable packaging applications. Kemira reported a strong 19.1% EBITDA margin in 2025, driven by its Packaging & Hygiene Solutions segment. The company achieved a 55% transition toward renewable raw materials, aligning with its €500 million renewable revenue target by 2030. Its portfolio emphasizes bio-based additives, digital services, and high-performance functional chemicals for recycled fiber systems.

BASF Strengthens Specialty Binder Leadership with Verbund Integration and APAC Capacity Expansion

BASF is advancing its specialty pulp and paper chemicals portfolio through integrated production and strategic portfolio optimization. The 2026 expansion of dispersions capacity in Mangalore enhances supply for high-growth APAC paper and packaging markets. BASF’s divestment of its Softex business enables a shift toward high-margin barrier resins and strength additives for e-commerce packaging. The company generated €1.3 billion in free cash flow in 2025, supporting investments in sustainable and high-performance coating technologies. Its vertical integration in acrylic monomers ensures cost leadership in key raw materials such as butyl acrylate and 2-EHA. BASF’s focus remains on recyclable coatings, functional binders, and low-VOC solutions for specialty paper applications.

Nalco Water Drives AI-Based Process Optimization and Wastewater Management for Recycled Fiber Mills

Nalco Water is leading digital transformation in specialty paper chemicals through AI-enabled process control and advanced water treatment solutions. Its collaboration with ANDRITZ at the Tissue Innovation Center focuses on optimizing chemical dosing using sensor-driven analytics. The updated 3D TRASAR™ technology enhances wastewater treatment efficiency, particularly for mills utilizing high recycled fiber content. Ecolab’s 2026 pricing strategy reflects a shift toward value-based chemical solutions amid rising energy costs. Nalco Water leverages its global footprint across 170 countries to deliver on-site expertise and integrated service models. Its solutions reduce fiber loss, energy consumption, and operational costs while improving mill productivity.

Buckman Enhances Smart Chemistry Capabilities with R&D Investment and Asia-Focused Joint Ventures

Buckman is expanding its specialty pulp and paper chemicals footprint through smart technology integration and strategic partnerships. The 2025 acquisition by Pritzker Private Capital is accelerating investment in digital solutions and customized chemical programs. Its $10 million pilot plant in Memphis enables real-world simulation of biocide and scale-control applications for faster commercialization. The joint venture with Atul Ltd strengthens its presence in India and Sri Lanka, targeting high-growth regional markets. Buckman implemented price increases in 2026 to offset regulatory and feedstock cost pressures. Its focus remains on tailored chemistry, process optimization, and intelligent monitoring systems for modern paper mills.

Nouryon Expands Bio-Based Polymer Portfolio and Bleaching Capacity to Support Sustainable Paper Production

Nouryon is reinforcing its leadership in specialty pulp and paper chemicals through bio-based innovation and capacity expansion. The 20% increase in sodium chlorate production supports rising demand for bleached pulp in premium tissue applications. Its 2026 launch of biodegradable carboxymethylcellulose introduces high-performance rheology modifiers for coatings and paper processing. Strategic collaborations with BASF and Maersk strengthen its low-carbon supply chain and logistics resilience. Nouryon is integrating production and innovation centers in China to develop next-generation catalysts and specialty polymers. Its portfolio emphasizes sustainable bleaching chemicals, cellulose derivatives, and functional additives aligned with circular economy goals.

Brazil Specialty Pulp and Paper Chemicals Market Anchored in Integrated Megaprojects

Brazil has consolidated its position as the most capital-intensive growth hub for specialty pulp and paper chemicals, driven by large-scale, fully integrated pulp mill investments. In August 2025, Nouryon finalized a long-term agreement with Arauco to construct an on-site sodium chlorate and chlorine dioxide facility in Mato Grosso do Sul. The project directly supports Arauco’s $4.6 billion pulp mill and increases Nouryon’s regional capacity by 20%, reinforcing the trend toward captive chemical supply to minimize logistics risk and ensure bleaching consistency at scale.

This integration model is being replicated across the country. In May 2025, CMPC announced its Projeto Natureza eucalyptus pulp mill in Rio Grande do Sul, a $4.6 billion investment that is expected to generate sustained demand for specialty bleaching sequences, pitch-control agents, and recovery-cycle chemicals. Similarly, Suzano S.A. operationalized the Cerrado Project in late 2024, the world’s largest single-line pulp mill, incorporating a closed-loop chemical recovery system integrating sulfuric acid and caustic soda. With Brazil’s planted forest area reaching 10.2 million hectares in 2025, R&D focus has shifted decisively toward surfactants, drainage aids, and strength additives optimized for short-fiber eucalyptus pulp rather than generic softwood chemistries.

China Specialty Pulp and Paper Chemicals Market Reshaped by Green Packaging and Compliance

China’s specialty pulp and paper chemicals market is being reshaped by regulatory mandates that prioritize recyclability, chemical transparency, and emission control. Following the 2025 National Green Packaging Standards, major mills in Zhejiang and Guangdong have replaced polyethylene coatings with aqueous specialty barrier polymers that allow full repulpability while maintaining moisture and grease resistance. This transition has materially increased demand for water-based binders, dispersion aids, and surface treatment chemistries tailored for high-speed coating lines.

Regulatory oversight is extending deeper into chemical supply chains. In August 2025, the Ministry of Industry and Information Technology released draft GHS-aligned labeling standards mandating QR-coded safety and traceability information for all specialty chemicals used in paper production. At the same time, BASF commissioned a CFRP-based dispersant production line in Nanjing in November 2025 to stabilize high-performance pigments in specialty coated papers. Environmental pressure is intensifying further. The Ministry of Ecology and Environment expanded VOC tax pilots in late 2025 to include specialty paper-finishing solvents, accelerating the shift toward solvent-free formulations. Tighter GACC controls on recycled pulp imports have also raised demand for advanced de-inking and stickies-control chemistries capable of handling lower-quality domestic recovered fiber.

United States Specialty Pulp and Paper Chemicals Market Driven by PFAS Exit and Bio-Based Substitution

The United States market is undergoing a structural reset driven by regulatory deadlines and mill reconfiguration. The EPA’s 2025 Unified Regulatory Agenda reaffirmed PFAS compliance as a priority, triggering a complete industry exit from fluorinated grease-proofing agents. Mills have rapidly transitioned toward specialty starches, cellulose derivatives, and bio-based surface treatments that meet food-contact performance requirements without persistent fluorine chemistry.

Operational changes are reinforcing this shift. Sappi North America completed its Somerset Mill conversion in 2025, pivoting toward solid bleached sulfate packaging. This conversion increased demand for high-opacity wet-end additives, retention systems, and advanced surface sizing agents optimized for premium board grades. Parallel to this, adoption of enzyme-based processing has accelerated. By late 2025, over one-third of North American producers had integrated cellulases and hemicellulases to reduce refining energy while improving fiber strength. Federal procurement under the USDA BioPreferred Program has further amplified demand for sustainable specialty additives, with reported adoption rising 32% year on year.

Germany Specialty Pulp and Paper Chemicals Market Focused on Circularity and Digital Control

Germany’s specialty pulp and paper chemicals market is increasingly defined by circular-economy mandates and process digitalization. Updates to the Circular Economy Act in late 2025 require higher integration of secondary raw materials, driving demand for re-pulping aids capable of separating complex multilayer barrier structures without degrading fiber quality. This has elevated the role of enzyme-assisted separation agents and selective surfactant systems.

Strategic portfolio shifts are also evident. In September 2025, BASF announced its exit from the hydrosulfites business and closure of the Ludwigshafen facility, signaling a broader industry move away from traditional reductive bleaching toward more stable, environmentally aligned alternatives. Compliance with EU PFHxA restrictions has already resulted in a full transition to fluorine-free food-contact paper chemistries for the 2025–2026 cycle. On the operational side, approximately 42% of German mills have deployed AI-driven chemical dosing systems, reducing chemical waste by an average of 12% per ton and reinforcing Germany’s position as a benchmark for precision chemical management.

India Specialty Pulp and Paper Chemicals Market Accelerated by Packaging and Localization Policies

India’s specialty pulp and paper chemicals market is expanding on the back of aseptic packaging growth, localization incentives, and mill modernization. In late 2025, SIG completed its ₹880 crore aseptic carton facility in Ahmedabad, creating sustained local demand for extrusion primers, adhesion promoters, and functional barrier chemistries used in liquid packaging. This investment has reduced reliance on imported specialty coatings while improving supply reliability for food and beverage converters.

Policy support is reinforcing domestic chemical capacity. Under the Production Linked Incentive scheme, realized investments in specialty chemicals reached ₹1.76 lakh crore by March 2025, including new AKD and ASA sizing agent lines that were previously imported. At the mill level, Andhra Paper Ltd. invested ₹125 crore in advanced wet-end chemistry automation during 2024–2025, targeting high-strength tissue and technical paper grades. These developments position India as an increasingly self-sufficient market for functional pulp and paper chemicals aligned with packaging and hygiene demand.

Comparative Snapshot: Specialty Pulp and Paper Chemicals by Country

Specialty Pulp and Paper Chemicals Market County Level Snapshot

|

Country

|

Core Demand Driver

|

Chemical Focus Area

|

Structural Trend

|

|

Brazil

|

Megapulp investments

|

Bleaching and recovery chemicals

|

On-site integration

|

|

China

|

Green packaging mandates

|

Aqueous barriers, dispersants

|

Regulatory-led reformulation

|

|

United States

|

PFAS phase-out

|

Bio-based sizing and coatings

|

Substitution and mill conversion

|

|

Germany

|

Circular economy laws

|

Repulping aids, digital dosing

|

Precision and compliance

|

|

India

|

Aseptic packaging growth

|

Sizing agents, barrier primers

|

Localization and modernization

|

Specialty Pulp and Paper Chemicals Market Report Scope

Specialty Pulp and Paper Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.4 Billion

|

|

Market Size (2034)

|

$34.6 Billion

|

|

Market Growth Rate

|

3.5%

|

|

Segments

|

By Functional Category (Functional Chemicals, Process Chemicals, Bleaching and Pulping Chemicals), By Form Factor (Liquid Formulations, Powder and Granular, Solid), By Application (Packaging and Industrial, Printing and Writing, Tissue and Hygiene, Graphic and Decorative)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kemira Oyj, Solvay S.A., BASF SE, Nouryon, Ecolab Inc., Buckman Laboratories International, Inc., Kurita Water Industries Ltd., Dow Inc., Evonik Industries AG, Archroma, Ingredion Incorporated, Solenis LLC, Ashland Inc., Fineotex Chemical Limited, Clariant AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Pulp and Paper Chemicals Market Segmentation

By Functional Category

- Functional Chemicals

- Process Chemicals

- Bleaching and Pulping Chemicals

By Form Factor

- Liquid Formulations

- Powder and Granular

- Solid

By Application

- Packaging and Industrial

- Printing and Writing

- Tissue and Hygiene

- Graphic and Decorative

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Pulp and Paper Chemicals Industry

- Kemira Oyj

- Solvay S.A.

- BASF SE

- Nouryon

- Ecolab Inc.

- Buckman Laboratories International, Inc.

- Kurita Water Industries Ltd.

- Dow Inc.

- Evonik Industries AG

- Archroma

- Ingredion Incorporated

- Solenis LLC

- Ashland Inc.

- Fineotex Chemical Limited

- Clariant AG

*- List not Exhaustive