Spoon-in-Lid Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Spoon-in-Lid Packaging Market to Reach $670.9 Million by 2034 Driven by Rising Consumer Demand for Convenience and Hygiene

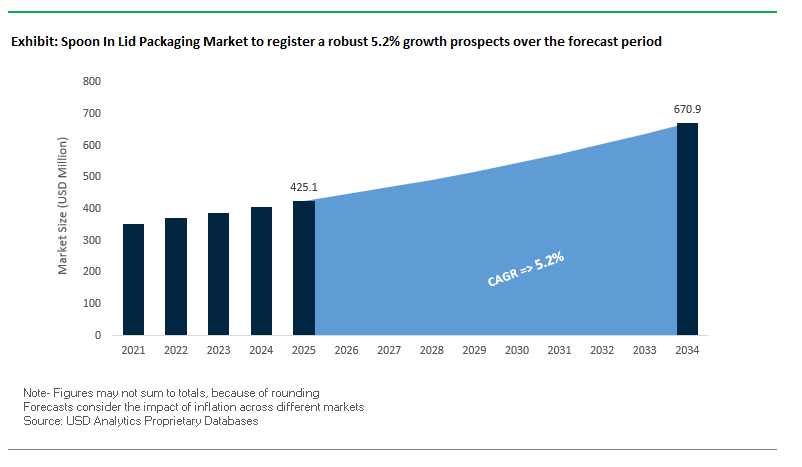

The global spoon-in-lid packaging market is projected to grow from $425.1 million in 2025 to $670.9 million by 2034, registering a CAGR of 5.2%. This specialized market provides integrated container and utensil solutions, primarily for dairy products, desserts, and ready-to-eat meals, enabling on-the-go consumption while maintaining hygiene.

Key Insights for Industry Professionals:

- Urbanization and busy lifestyles are accelerating demand for single-serve, portable food products.

- Sustainability is central: Mono-material solutions (all-PP or all-PET) and cardboard spoons are increasingly adopted to comply with EU single-use plastic regulations.

- Hygiene-focused design: Integrated spoons protect against contamination, a critical factor for post-pandemic consumer preferences.

- Brand differentiation and shelf appeal: Innovative designs and premium materials enhance visibility and consumer engagement.

- Innovation trend: Packaging solutions are evolving to balance convenience, safety, and sustainability in a highly competitive market.

Market Analysis: Recent Developments Highlight a Shift Toward Sustainability, Innovation, and Market Expansion in Spoon-in-Lid Packaging

The spoon-in-lid packaging market has experienced significant innovation and strategic expansion over the past few years. In November 2024, Tekplas and Chadwick introduced a spoon-in-lid solution for infant formulas, signaling the format’s expansion beyond traditional dairy and dessert applications. In October 2024, Amcor strengthened its Indian market presence by acquiring Phoenix Flexibles, aligning with the growing demand for on-the-go packaging in emerging markets.

Sustainability trends are influencing material choices and design strategies. In July 2024, Greiner Packaging partnered to develop a 100% recyclable cardboard spoon, responding to the EU single-use plastic ban. April 2024 saw Dr. Pfleger collaborate with ETIMEX on recyclable pastille blisters, reflecting a broader industry pivot toward eco-friendly materials. Even older innovations, like RPC Superfos’ 2017 PET-based spoon-in-lid solution, highlight the market’s ongoing emphasis on convenience and user-friendly design.

The market also demonstrates a strong focus on hygiene, user experience, and convenience. June 2024, ITC Packaging’s mass production of “Spoon-caps” for infant nutrition underscores the high demand for hygienic, integrated packaging solutions.

Trends and Opportunities Reshaping the Spoon-in-Lid Packaging Market

Strategic Integration of Post-Consumer Recycled (PCR) Materials

One of the most significant trends driving the spoon-in-lid packaging market is the growing use of post-consumer recycled (PCR) plastics to meet sustainability goals. Leading FMCG brands are under pressure from both regulators and consumers to increase their PCR content usage across all packaging formats. A 2025 case study highlights a skin packaging film with a minimum of 30% PCR PET content, underscoring how extrusion and filtration technologies are enabling the integration of recycled content without compromising clarity, barrier properties, or sealing performance. For spoon-in-lid formats, where both transparency and durability are critical, these advancements are particularly impactful. This move is not only about compliance but also about building consumer trust in eco-conscious brands. For instance, Coca-Cola’s PETValue Philippines recycling facility, designed to process two billion PET bottles annually, demonstrates how companies are actively building a sustainable feedstock pipeline for PCR plastics. ProAmpac’s launch of spoon-in-lid solutions with conventional, recycle-ready, and PCR options further emphasizes how brands are diversifying their portfolios to offer environmentally responsible alternatives while maintaining product convenience.

Material Science Innovation for Functional Barrier Properties

Another key trend lies in material science, where the challenge is balancing sustainability with high performance. Spoon-in-lid packaging often requires strong barrier protection to extend shelf life for dairy, desserts, and prepared meals. Recent innovations include recyclable EVOH-based co-polymers that can be co-extruded with PE to create high-barrier, mono-material films compatible with recycling systems. Simultaneously, nanocomposite-based polymer films are being engineered to deliver superior moisture and oxygen resistance, particularly for oily or sensitive foods like yogurt parfaits, fruit cups, or protein-based snacks. These developments are critical as the spoon-in-lid format expands into fresh meal solutions and premium food categories. By enabling packaging to meet the functional demands of diverse food products while remaining recyclable, these innovations strengthen the market position of spoon-in-lid formats in both convenience and sustainability-focused retail channels.

Expansion into New Fresh Food and Prepared Meal Categories

The spoon-in-lid format offers an untapped growth avenue in fresh food and ready-to-eat meals. Traditionally used in dairy and desserts, this format is now being adapted for high-demand segments such as grab-and-go meal trays, yogurt parfaits with granola, and fruit cups. With the convenience of an integrated utensil, consumers can enjoy a complete, on-the-go meal solution without relying on disposable cutlery, which aligns with global bans on single-use plastics. Retailers and meal-prep brands are also increasingly adopting resealable lidding films that improve user experience and reduce food waste. For food service providers, particularly in urban centers and institutional catering, spoon-in-lid packaging addresses both operational efficiency and environmental concerns by consolidating utensils into the packaging itself. This innovation is poised to reduce secondary packaging waste, capture a broader consumer base, and significantly enhance brand differentiation in the competitive ready-meal market.

Design for Advanced Recycling Streams

A second major opportunity lies in designing spoon-in-lid systems to align with advanced recycling technologies. Many current designs use multi-material structures combining PP, PS, or PET with barrier layers, making them difficult to recycle through conventional mechanical streams. However, advancements in chemical recycling technologies such as pyrolysis and depolymerization are unlocking new potential. These processes can break down mixed plastics into their molecular building blocks, yielding virgin-quality resins suitable for food-contact applications. ExxonMobil’s research demonstrates the scalability of advanced recycling for complex structures, particularly barrier films used in lids. By designing spoon-in-lid packaging specifically for compatibility with advanced recycling, manufacturers can position their solutions as circular-ready. This not only ensures regulatory compliance with future mandates but also appeals to brands seeking to achieve ambitious sustainability targets while safeguarding food safety.

Competitive Landscape: Leading Packaging Companies Are Innovating Spoon-in-Lid Solutions to Enhance Convenience, Sustainability, and Brand Differentiation

The global spoon-in-lid packaging industry is dominated by companies leveraging expertise in materials science, design, and manufacturing to provide durable, hygienic, and increasingly sustainable solutions.

Greiner Packaging International GmbH: Pioneering Recyclable and Digitally Integrated Spoon-in-Lid Solutions

Greiner Packaging offers thermoformed and injection-molded cups and tubs with plastic and cardboard spoon options. In 2024, the company won a Hungaropack Award for a digital drinking cup with integrated RFID technology and partnered to develop 100% recyclable cardboard spoons. Its strength lies in material innovation and circular economy leadership, with a strategy centered on sustainability and comprehensive packaging solutions for evolving consumer and regulatory demands.

ITC Packaging: Leading High-Volume Spoon-Cap Production with a Focus on Infant Nutrition

ITC Packaging specializes in hinged “Spoon-caps” for baby formula and other products, producing millions for brands like Arla, Hero, and Danone. The company offers a Bio version using sustainable materials and emphasizes high-volume, high-quality manufacturing. Its strategy focuses on customized, hygienic, and convenient packaging solutions tailored to food and infant nutrition markets.

Berry Global Inc.: Expanding Reusable and Recyclable Spoon-in-Lid Solutions for Food and Beverage

Berry Global provides spoon-in-lid solutions for dairy, desserts, and frozen foods. In November 2023, it launched Berry Agile Solutions, enabling access to reusable and recyclable packaging. The company’s global manufacturing footprint, expertise in plastics, and vertically integrated operations strengthen its position, while its strategy emphasizes sustainable, efficient, and reliable packaging solutions.

Sealed Air Corporation: Enhancing Food Shelf-Life with High-Barrier Lid Films

Sealed Air develops CRYOVAC® lid films for lidded containers, including those with integrated utensils. Its innovations include anti-fog and high-barrier films to maintain freshness. The company focuses on materials science innovation, recyclability, and performance enhancement, providing packaging solutions that preserve product quality and extend shelf life.

Huhtamaki Oyj: Driving Sustainable Food Packaging Through Fiber-Based and Circular Materials

Huhtamaki offers paper, fiber, and molded fiber containers, integrating spoon-in-lid solutions and sustainable alternatives. Collaborations with SABIC and Mars Petcare focus on circular polypropylene, while its Blueloop platform enhances recyclability. Huhtamaki’s global footprint and material expertise enable it to deliver comprehensive, sustainable packaging solutions, aligned with its 2030 recyclability and compostability goals.

Spoon In Lid Packaging Market Share Insights, 2025-2034

Food & Beverages Dominate Market Share by End-Use Industry in Spoon-in-Lid Packaging

Food & Beverages account for nearly 80% of the spoon-in-lid (SIL) packaging market, cementing their position as the undisputed leader in this convenience-driven format. The dominance of this segment is directly tied to the rise of on-the-go consumption and the consumer preference for hygienic, single-serve solutions. Dairy products such as yogurt, puddings, and cottage cheese are the primary drivers, as SIL packaging eliminates the need for additional utensils while maintaining sterility and portability. In addition, powdered drink mixes and instant meal applications reinforce demand, particularly among urban consumers seeking functional, ready-to-use solutions. While healthcare and cosmetics are growing niches, the sheer scale of daily food consumption ensures that Food & Beverages remain the cornerstone of SIL packaging growth worldwide.

Cups & Tubs Command Market Share by Product Type in Spoon-in-Lid Packaging

Cups and tubs represent 70% of the global spoon-in-lid packaging market, making them the format standard for this packaging innovation. Their rigid structure provides the necessary stability to integrate spoons within the lid, ensuring reliability for semi-solid and liquid products across food, dairy, and healthcare applications. This stability is critical for consumer confidence, especially for products where the lid-spoon mechanism must function seamlessly in a single-serve context. The format also enables high-quality branding and printing, making it attractive to companies seeking strong shelf appeal. With their proven performance and widespread acceptance across global markets, cups and tubs will continue to anchor SIL packaging adoption, even as pouches and trays explore niche opportunities.

United States: Recycling Infrastructure and Growth in On-the-Go Food Packaging

The United States spoon-in-lid packaging market is growing rapidly, supported by the U.S. Environmental Protection Agency’s (EPA) goal of achieving a 50% national recycling rate by 2030. This initiative is a key driver for packaging companies to invest in recycling infrastructure, sustainable materials, and post-consumer recycled (PCR) plastics. A notable industry example is Berry Global, which produces plastic cups and lids for major food brands while increasingly integrating PCR content to meet both regulatory and consumer sustainability expectations.

The U.S. market is also shaped by the rising demand for ready-to-eat and on-the-go food products, such as yogurts, instant oatmeal, and ice creams, where spoon-in-lid packaging provides hygiene and convenience. Consumers prefer integrated spoons for single-use, clean, and portable applications, making it an attractive choice for foodservice brands and quick-service restaurants. At the same time, guidance from the Association of Plastic Recyclers (APR) is accelerating the adoption of washable inks, floatable films, and recyclable lid materials, reinforcing the U.S. market’s focus on both safety and sustainability.

European Union: PPWR, SUPD, and Innovation in Compostable Lid and Spoon Materials

The European Union spoon-in-lid packaging market is experiencing major regulatory-driven transformation under the Packaging and Packaging Waste Regulation (PPWR), effective from February 2025. This regulation mandates that all plastic parts, including lids and integrated spoons, must contain specified recycled content by 2030, while the Single-Use Plastics Directive (SUPD) has already banned plastic cutlery and set recycling targets for PET bottles. Together, these frameworks are forcing manufacturers to accelerate the shift toward recyclable, compostable, and refill-friendly designs.

A notable innovation area is the development of alternative barrier coatings and compostable lid solutions to address restrictions on per- and polyfluoroalkyl substances (PFAS) effective August 2026. Companies like Huhtamaki are at the forefront of developing recyclable and bio-based spoon-in-lid formats, leveraging R&D in paperboard composites, bioplastics, and reusable designs. The introduction of Digital Product Passports under the Ecodesign for Sustainable Products Regulation (ESPR) is further driving packaging transparency, ensuring that material origins, recyclability, and compliance data are accessible across the EU supply chain.

China: The “Lazy Economy” and Rising Demand for High-End Convenience Packaging

In China, the spoon-in-lid packaging market is expanding rapidly, driven by two forces: government regulations under the 14th Five-Year Plan and consumer preferences shaped by the “Lazy Economy.” From June 2025, new regulations require companies in logistics and e-commerce to adopt eco-friendly, reusable, and reduced packaging, which directly impacts single-use spoon-in-lid formats.

On the consumer side, the “Lazy Economy” trend, where buyers are willing to pay more for convenience, is fueling growth in spoon-in-lid packaging for instant noodles, desserts, and dairy products. Manufacturers are also responding to rising demand for high-end and visually appealing packaging by adopting advanced printing technologies, tamper-evident designs, and enhanced barrier films. Additionally, the Chinese government’s tax incentives for green technology are encouraging companies to adopt remanufacturing and recyclable solutions, ensuring that convenience packaging aligns with the country’s sustainability objectives.

India: EPR Compliance and Growth in Dairy and Dessert Packaging

The India spoon-in-lid packaging market is witnessing strong regulatory and demand-driven growth. The Plastic Waste Management (Amendment) Rules, 2024, effective from April 2025, emphasize Extended Producer Responsibility (EPR), making manufacturers accountable for recycling and disposal. From July 1, 2025, all plastic packaging, including spoon-in-lid formats, must carry traceable barcodes or QR codes, ensuring environmental accountability. However, MSMEs are exempt, with the responsibility shifted to raw material suppliers and larger manufacturers.

Market demand is being driven by the growing dairy, dessert, and retail sectors, as spoon-in-lid packaging offers a hygienic and convenient solution for yogurts, puddings, and ice creams. The rapid rise of e-commerce and modern retail chains is further accelerating adoption. Manufacturers are introducing cost-efficient, recyclable spoon-in-lid solutions to cater to India’s price-sensitive but convenience-driven consumer base, positioning the format as a practical and sustainable solution for both urban and rural markets.

Japan: Plastic Circulation Laws and the Shift Toward Compostable Alternatives

The Japan spoon-in-lid packaging market is being shaped by the Plastic Resource Circulation Strategy, which mandates that all packaging must be reusable or recyclable by 2025. The accompanying Plastic Resource Circulation Promotion Law, effective in 2025, also enforces the redesign and reduction of 12 types of single-use plastic products, encouraging companies to adopt reusable, compostable, or paper-based spoon-in-lid alternatives.

In line with Japan’s goal of doubling renewable material usage by 2030, manufacturers are increasingly experimenting with paper-based lids, bio-based polymers, and recyclable bioplastics for food and beverage packaging. The country’s emphasis on waste sorting and consumer participation in recycling programs ensures that sustainable spoon-in-lid packaging solutions gain rapid adoption. This regulatory framework, combined with Japan’s innovation-driven food packaging industry, is expected to accelerate the development of eco-friendly designs for convenience products.

Brazil: Reverse Logistics and Sustainable Waste Management in Food Packaging

The Brazil spoon-in-lid packaging market is governed by the National Solid Waste Policy (PNRS), which emphasizes responsible waste disposal, reuse, and recycling. With Law No. 15,088 taking effect in January 2025, banning imports of plastic waste, domestic manufacturers are being pushed to adopt sustainable packaging practices.

Brazil is also actively promoting reverse logistics systems, making producers responsible for collecting and recycling post-consumer packaging. This directly impacts spoon-in-lid packaging in dairy and dessert applications, where sustainability is becoming a strong market differentiator. Local and international companies are introducing eco-friendly spoon-in-lid designs, including recyclable polymers and compostable materials, to comply with national regulations and meet the rising consumer demand for convenient, hygienic, and environmentally sustainable packaging solutions.

Spoon In Lid Packaging Market Report Scope

Spoon In Lid Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$425.1 Million

|

|

Market Size (2034)

|

$670.9 Million

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Material (Plastic, Paper & Paperboard, Bio-based & Compostable Materials, Aluminum), By End-Use Industry (Food & Beverages, Medical & Healthcare, Cosmetics & Personal Care), By Product Type (Cups & Tubs, Pouch & Sachets, Trays)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Berry Global, Inc., Amcor plc, Huhtamaki Oyj, Greiner Packaging International GmbH, Sonoco Products Company, Tekpak Solutions, ITC Packaging, RPC Group (part of Berry Global), Rosti Group, Silgan Holdings Inc., B&R Plastics, Inc., Faerch Plast A/S, Visy Industries, Poloplast S.r.l., EcoTensil

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Spoon In Lid Packaging Market Segmentation

By Material

- Plastic

- Paper & Paperboard

- Bio-based & Compostable Materials

- Aluminum

By End-Use Industry

- Food & Beverages

- Medical & Healthcare

- Cosmetics & Personal Care

By Product Type

- Cups & Tubs

- Pouch & Sachets

- Trays

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Spoon In Lid Packaging Market

- Berry Global, Inc.

- Amcor plc

- Huhtamaki Oyj

- Greiner Packaging International GmbH

- Sonoco Products Company

- Tekpak Solutions

- ITC Packaging

- RPC Group (part of Berry Global)

- Rosti Group

- Silgan Holdings Inc.

- B&R Plastics, Inc.

- Faerch Plast A/S

- Visy Industries

- Poloplast S.r.l.

- EcoTensil

* List Not Exhaustive

Methodology

The Spoon-in-Lid Packaging Market analysis presented by USDAnalytics is based on a comprehensive, multi-step research methodology combining primary and secondary approaches to deliver accurate, actionable insights for industry professionals. Primary research involved detailed interviews with packaging engineers, R&D specialists, supply chain managers, and brand managers from leading global companies such as Berry Global, Greiner Packaging, ITC Packaging, Huhtamaki, and Amcor, focusing on market dynamics, material innovations, and end-user preferences. Secondary research incorporated a thorough review of company reports, sustainability and regulatory publications, academic journals, industry news, and trade association data to identify trends in convenience packaging, PCR integration, barrier material development, and compostable solutions. Market sizing, growth forecasts, and segmentation were determined using both top-down and bottom-up approaches, factoring in regional regulations including EU SUPD, PPWR, India’s EPR, and Japan’s Plastic Resource Circulation Strategy. Data triangulation and cross-validation ensured reliability across materials, end-use industries, and product formats, providing a robust framework for stakeholders seeking insights into market opportunities, sustainability initiatives, and competitive strategies in the evolving spoon-in-lid packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.