Thermal Ceramics Market Overview: Ultra-High-Temperature & LBP Insulation Driving Steady Growth

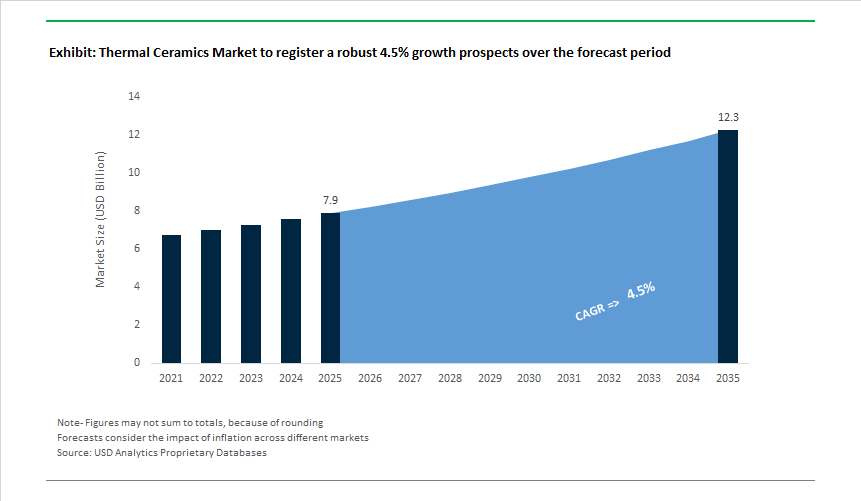

The Thermal Ceramics Market is valued at USD 7.9 billion in 2025 and is projected to reach USD 12.3 billion by 2035, growing at a 4.5% CAGR as high-temperature insulation shifts from a maintenance consumable to a strategic lever for energy efficiency, safety compliance, and lifecycle cost control. Demand is anchored in industries where thermal losses, safety risk, or regulatory non-compliance translate directly into operating cost penalties and production constraints.

At the core of market expansion is the tight coupling between temperature capability and regulation. Heavy industries-steel, non-ferrous metals, glass, cement, chemicals, and advanced ceramics continue to push operating temperatures higher to improve throughput and product purity. This sustains demand for high-alumina fibers, zirconia systems, and Ultra-High Temperature Ceramics (UHTCs) capable of retaining structural and insulating integrity above 2,000°C. At the same time, health and safety frameworks in developed markets are accelerating the transition toward Low-Bio-Persistent (LBP) fiber chemistries, forcing manufacturers and end users to replace legacy refractory ceramic fibers regardless of residual asset life. As a result, thermal ceramics demand is increasingly policy-reinforced rather than cyclical.

Energy economics provide a second, durable pull. Rising fuel costs, carbon pricing, and Scope 1 emissions scrutiny are driving furnace operators to re-evaluate insulation performance rather than furnace design. Upgrading refractory and insulation linings routinely delivers 15-30% reductions in energy consumption and CO₂ emissions, creating a short payback period even in conservative retrofit scenarios. This shifts purchasing decisions from lowest upfront cost to total cost of ownership (TCO), favoring suppliers that can demonstrate heat-loss modeling, installation efficiency, and longer service intervals.

Electrification is opening a newer, higher-value demand channel. EV battery systems and power electronics require thermal barriers that not only insulate but delay heat propagation during thermal runaway events. Ceramic fiber products engineered to provide 5-15 minutes of propagation delay are increasingly embedded into battery pack architectures as safety requirements tighten. Unlike industrial insulation, these applications demand lightweight, compact, and highly engineered formats-pushing thermal ceramics into closer alignment with automotive qualification cycles and premium pricing structures.

Aerospace and advanced mobility reinforce the market’s performance ceiling. Ceramic fiber blankets and rigidized insulation systems are specified because they deliver equivalent high-temperature insulation at up to 90% lower mass than dense firebrick, enabling payload gains and fuel efficiency improvements. UHTC materials further support extreme thermal environments in propulsion, hypersonics, and advanced metallurgy, where substitution options are effectively nonexistent.

From a competitive standpoint, the market is consolidating around materials compliance, system integration, and global execution. Suppliers that combine LBP-compliant chemistries, high-alumina and zirconia portfolios, and scalable manufacturing footprints are best positioned to serve multinational industrial customers. Increasingly, value is captured through system solutions-integrating insulation design, modular installation, and even digital monitoring to optimize kiln and furnace lifecycles.

Thermal Ceramics Market Analysis: Capacity Builds, LBP Compliance and Modular Systems Reshape Demand

The Thermal Ceramics industry showed a pattern of product innovation, regional capacity expansion and a renewed focus on health-compliant fiber chemistries. In December 2024, Zircar Zirconia ramped capacity for ultra-high temperature zirconia fiber boards (continuous use up to 2,200°C), highlighting the strategic push into hypersonic and re-entry thermal protection systems. Through March-June 2025, multiple vendors targeted modularity and EV safety: April 2025 saw CCEWOOL introduce modular ceramic fiber units with wrinkled-fiber blanket compression for faster installation and improved sealing in large industrial furnaces, while June 2025 CeramTec launched the Sinalit platform addressing thermal/electrical insulation needs for high-power SiC modules in EV inverters.

In September-November 2025 the market emphasis shifted to both raw material security and compliant product lines. September 2025 RHI Magnesita’s vertical integration (acquisition of a raw material mine) secured ~67% internal sourcing for magnesite/dolomite - strengthening refractory supply resilience. November 2025 Morgan Advanced Materials initiated a dedicated LBP production line in Eastern Europe to align capacity with EU safety standards, reflecting regulatory-driven demand. Finally, December 2025 pilot launches of nanoparticle-infused ceramic fiber blankets promised a ~10% thermal conductivity reduction, indicating an industry trajectory toward higher-performance, lower-mass insulation solutions that directly support energy efficiency and emissions goals.

Thermal Ceramics Market Trends and Opportunities

Trend 1: Ultra-High-Temperature Insulation for Hydrogen and Syngas Production

Hydrogen pathways such as turquoise hydrogen (methane pyrolysis) and advanced thermochemical water-splitting are redefining the operating envelope for refractory and insulating ceramics. These processes require continuous stability under 1,200°C–1,600°C, exposure to hydrogen-rich atmospheres, and resistance to carbon fouling—conditions that exceed the capabilities of legacy insulating firebricks.

In December 2025, NewHydrogen reported progress in its ThermoLoop™ platform, which replaces electricity-intensive electrolysis with heat-driven redox cycles. The system relies on high-purity thermal ceramics to withstand repeated oxidation–reduction cycling without microcracking or thermal drift—placing insulation reliability directly in the hydrogen cost equation.

Parallel momentum is visible in methane pyrolysis, where academic and pilot-scale data in early 2025 confirmed that porous ceramic filters and zirconia-stabilized alumina linings are now preferred for hot gas cleanup. These materials prevent carbon deposition while preserving thermal efficiency, enabling sustained reactor uptime. In steel and syngas applications, Midrex Flex reformers are increasingly specified with lightweight ceramic blanket modules rather than dense bricks, improving thermal shock resistance as hydrogen content in the reducing gas fluctuates between 30% and 100%.

Trend 2: Structural Shift from RCF to Low-Bio-Persistent (LBP) Ceramic Fibers

Health, safety, and regulatory pressure is accelerating a structural transition away from traditional Refractory Ceramic Fibers (RCFs) toward Low-Bio-Persistent (LBP) alkaline earth silicate (AES) fibers. Unlike RCFs, LBP fibers dissolve in lung fluid within weeks, materially reducing long-term occupational health risks while maintaining high thermal performance.

By late 2025, industry data indicated a clear pivot toward amorphous AES fibers with classification temperatures up to 1,300°C, sufficient for most industrial furnaces and reformers. This shift is not cosmetic; it is being embedded into procurement standards across aerospace, energy, and advanced manufacturing. Updated NASA material handling and safety frameworks in 2024–2025 further reinforced the preference for low-persistence ceramic textiles in high-temperature aerospace ground operations.

On the supply side, capacity investments reflect this rebalancing. The 2025 commissioning of Morgan Advanced Materials’ expanded Yixing facility underscores industry commitment to bio-soluble, high-purity fiber platforms produced via advanced sol-gel and spinning routes. These next-generation LBP fibers deliver higher tensile strength and chemical resistance, closing the historical performance gap with RCFs.

Opportunity 1: Ceramic Fiber Modules as Enablers of Electrified Industrial Heating

Industrial electrification—rather than fuel switching alone—is emerging as the dominant decarbonization pathway for high-heat processes. This creates a sizeable retrofit opportunity for ceramic fiber modules in Electric Arc Furnaces (EAFs), electric boilers, and resistance-heated kilns, where minimizing thermal losses directly reduces electricity demand.

In early 2025, the UK’s Materials Processing Institute announced a £2.9 million upgrade of its seven-tonne EAF as part of a green steel pilot. Ceramic fiber modules were central to the redesign, improving heat retention and enabling faster ramp-up cycles compared with legacy dense linings. According to the Energy Transitions Commission’s 2025 industrial decarbonization analysis, electrification is the only scalable route for eliminating fossil fuels in high-temperature manufacturing—and thermal ceramics are explicitly identified as the gating technology.

Policy alignment is amplifying this opportunity in Asia. India’s clean energy subsidies rose 31% year-on-year in 2025, reaching INR 32,000 crore, incentivizing steel, glass, and textile producers to retrofit gas-fired systems with electrically heated furnaces. High-efficiency ceramic insulation is now treated as a prerequisite for economic electrification, not an optional upgrade.

Opportunity 2: Thin Ceramic Tapes and Papers for EV Battery Thermal Runaway Control

Battery architecture evolution—particularly Cell-to-Pack (CTP) and Cell-to-Chassis designs—has elevated thermal ceramics from peripheral insulation to core safety components. These architectures reduce structural mass but eliminate traditional spacing between cells, making thin, flexible ceramic barriers essential for arresting thermal runaway propagation.

In January 2025, ProLogium launched its fourth-generation lithium-ceramic battery platform, highlighting the broader industry shift toward inorganic, nonflammable materials. Even in conventional lithium-ion systems, ceramic-based tapes and papers are increasingly used as intercell firewalls capable of withstanding 1,000°C+ during failure events.

Commercial scaling is already underway. Asahi Kasei expanded deployment of its LASTAN ceramic-based nonwoven fabric across EV platforms in 2024–2025, targeting flame resistance and dimensional stability during runaway. In parallel, Oerlikon introduced ceramic safety components—including gas guidance and fire-delay systems—designed to meet current five-minute escape-time regulations and anticipated future extensions.

Market Share Analysis: Thermal Ceramics Market

Market Share by Product Form: Ceramic Fiber Blankets & Mats Capture Volume Through Energy, Safety, and Downtime Economics

Ceramic fiber blankets and mats hold roughly 35% of the thermal ceramics market because they deliver the fastest and most economically defensible path to high-temperature insulation upgrades in energy-intensive industries. Their dominance in 2025 is not driven by temperature capability alone, but by measurable operating cost reductions and regulatory alignment. AES and low-bio-persistence fiber blankets now enable up to 15% furnace energy savings versus insulating firebricks, a figure that directly offsets rising carbon pricing and fuel volatility in steel, aluminum, and glass plants. The widespread adoption of the 128 kg/m³ density standard reflects hard-earned field optimization: this density minimizes heat loss at operating temperatures near 1,000°C while retaining enough mechanical strength to withstand vibration, thermal cycling, and negative pressure environments. Equally decisive is the regulatory-driven pivot toward bio-soluble fibers, which meet 2025 occupational exposure limits in the EU and North America without forcing operators to compromise on 1,200–1,430°C service ratings. From a maintenance economics standpoint, modular blanket systems have redefined shutdown planning—cutting installation time by around 30% compared to brick linings and materially reducing lost production during relines. These combined advantages—energy efficiency, worker safety compliance, and outage minimization—explain why blankets and mats remain the highest-volume product form rather than a transitional insulation solution.

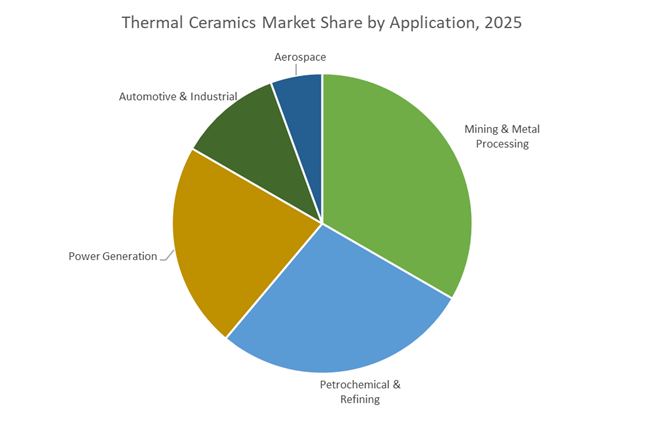

Market Share by Application: Mining & Metal Processing Anchors Demand Through High-Heat, High-Utilization Assets

Mining and metal processing accounts for approximately 30% of global thermal ceramics demand, reflecting the sector’s unmatched concentration of continuously operated, ultra-high-temperature assets. Smelting, refining, and foundry operations consume thermal ceramics not as discretionary upgrades but as process-critical infrastructure, particularly as global output of steel, aluminum, and copper scales to support EVs, renewable energy, and grid expansion. Within this segment, metallurgy and foundry operations alone represent about 42% of industrial ceramics value, underscoring the intensity of refractory and insulation consumption per unit of output. Advanced lining systems introduced in 2025 now deliver double-digit energy savings while improving melt quality, such as reducing hydrogen absorption in aluminum—directly linking thermal ceramics selection to downstream yield and scrap rates. At the upper end, next-generation refractory and insulation solutions capable of 1,800°C service temperatures are enabling production of superalloys and specialty steels for aerospace and defense, where thermal stability directly determines product certification. Demand in this application is also tightly correlated to macro production cycles: manufacturers report a ~65% correlation between global steel output and thermal ceramics consumption, with hydrogen-based “green steel” projects further accelerating adoption of low-thermal-mass, fast-cycling linings.

Competitive Landscape: System Suppliers & Raw-Material Integrated Players Lead the Thermal Ceramics Value Chain

The Thermal Ceramics competitive field is dominated by vertically integrated refractory groups, advanced-ceramics specialists and fiber innovators that combine R&D, raw material control and system delivery. Winners deliver compliance (LBP), ultra-high temperature performance (UHTC/Zirconia) and modular, installable thermal systems tailored to EV battery safety, industrial furnace retrofits and aerospace heat-shielding.

Morgan Advanced Materials - Leader in High-Temperature Insulation Solutions With R&D and EV Focus

Morgan’s Thermal Products division reported strong scale (revenue base ~£418.2m in 2024) and is executing efficiency gains through a Simplification Programme targeting a 12.5% adjusted operating profit margin in 2025. The company invests heavily in R&D (≈£31.1m in 2024) across four centers of excellence, focusing on EV battery protection systems and advanced refractory products. Morgan’s strategy emphasizes complex, integrated thermal management systems that combine material innovation with lifecycle services-well suited to capture retrofit and new-build industrial furnace and EV Tier-1 opportunities.

RHI Magnesita - Vertical Integration and Digital Refractory Lifecycle Management

RHI Magnesita strengthened raw-material security by acquiring a specialized mine to internally source ~67% of magnesite and dolomite needs, bolstering supply stability for high-grade refractories. Its 4PRO initiative couples refractory products with digital sensors and robotics for real-time monitoring of refractory depletion - a compelling value proposition for large kilns and continuous process plants seeking lower downtime and energy use. The company’s global footprint (35 production sites; 10,000+ customers) gives it scale advantages in heavy industrial markets.

Saint-Gobain - Diversified High-Performance Materials With Sustainability Commitments

Saint-Gobain’s High Performance Materials division supplies silica and basalt fiber based insulation systems rated up to 1,200°C, and targets thermal management for EV battery packs and industrial heat shields. The group’s integrated offering (coatings, tapes, cloths) and digital customer tools align with construction and industrial specifiers. Saint-Gobain’s sustainability agenda and product portfolio enable it to serve energy-efficiency retrofit projects and large architectural glazing/insulation programs.

Unifrax / Lydall Ecosystem - LBP and Flexible High-Performance Fiber Leader

Unifrax (now in Lydall/Aspen Aerogels context) leads in Low-Bio-Persistent fiber technology (e.g., Isofrax 1400) and supplies critical materials for EV battery protection and fire-barrier systems. Its broad LBP and high-alumina product range addresses occupational safety and regulatory compliance while enabling thin, flexible insulation formats suited to transportation and appliance markets.

Zircar Zirconia - Niche Specialist For Ultra-High Temperature Aerospace and R&D Applications

Zircar Zirconia focuses on ultra-high temperature zirconia-based fiber boards (continuous use up to 2,200°C) and high-purity alumina fiber products for hot-face applications up to 1,800°C. The company is a preferred partner for hypersonic, re-entry and specialized industrial processes where extreme thermal resistance and custom problem-solving are required.

The United States thermal ceramics market in 2025 is increasingly anchored to wide-bandgap semiconductor expansion and domestic refractory reshoring, marking a decisive shift from commodity insulation toward high-temperature, high-purity ceramic systems. The ramp-up of 200 mm silicon carbide (SiC) wafer fabrication has materially altered demand patterns for advanced thermal ceramics. The strategic collaboration between Morgan Advanced Materials and Wolfspeed—expanded through academic engagement with Pennsylvania State University—has placed ceramic insulators, setters, and crucibles at the center of the Mohawk Valley SiC fab’s thermal architecture. These components must withstand extreme thermal cycling while maintaining dimensional stability at elevated process temperatures, elevating performance thresholds across the U.S. thermal ceramics supply base.

Consolidation has further reinforced domestic capacity. In March 2025, RHI Magnesita completed the acquisition of Resco Group for approximately $430 million, significantly expanding U.S.-based production of alumina monolithics and engineered refractories. This move aligns with tightening industrial energy-efficiency mandates highlighted in the October 2025 ACEEE Energy Efficiency Scorecard, which increasingly requires advanced-level furnace and boiler performance. As a result, U.S. demand is shifting toward low-porosity ceramic linings and high-performance fiber modules that actively reduce heat loss and carbon intensity across steel, petrochemical, and semiconductor operations.

China: Mandatory Energy Intensity Reduction and Large-Scale Refractory Replacement

China’s thermal ceramics market is being reshaped by state-mandated energy conservation, transforming refractory replacement into a policy-driven volume engine. Under the 2024–2025 Energy Conservation and Carbon Reduction Action Plan issued by the State Council, national energy intensity reduction targets of 2.5% economy-wide and 3.5% for large industrial enterprises have triggered compulsory upgrades across energy-intensive sectors. For thermal ceramics suppliers, this has translated into a rapid, large-scale replacement cycle of legacy linings across more than 530 million tons of steelmaking capacity, favoring high-efficiency ceramic fiber systems and ultra-low thermal conductivity insulation.

Regulatory reinforcement by Ministry of Industry and Information Technology has further accelerated adoption. Expanded energy-efficiency specifications effective April 2024 now explicitly cover industrial boilers and photovoltaic manufacturing equipment, pulling demand toward micro-fine glass fibers, high-purity insulation wool, and bio-soluble ceramic fibers. At the corporate level, Alkegen’s majority investment in Luyang Energy Savings Material Co. in 2025 consolidated the world’s largest ceramic fiber production base within China. This consolidation strengthens China’s role as both the largest consumer and supplier of thermal ceramics, while embedding ultra-low-emission refractory solutions as a structural requirement rather than a discretionary upgrade.

Japan: GX 2040 Vision Positions Thermal Ceramics as Decarbonization Enablers

Japan’s thermal ceramics strategy is explicitly aligned with its Green Transformation (GX) 2040 Vision, reframing heat management materials as instruments of national decarbonization and energy security. The Cabinet-approved GX framework, backed by ¥20 trillion in GX Economy Transition Bonds, is channeling capital toward alkaline earth silicate (AES) fibers, low-biopersistent insulation, and high-purity ceramic composites capable of operating in hydrogen-rich and electrified process environments. These materials are increasingly critical as Japan’s chemical, cement, and glass industries transition away from fossil-fuel-intensive thermal systems.

Technological leadership underpins this policy push. In mid-2025, Morgan Advanced Materials conducted the world’s first real-time ceramic sintering research, enabling precise control over microstructure evolution during firing. This capability allows Japanese manufacturers to optimize ceramic-ceramic composites for aerospace, solid-state batteries, and energy storage systems. Coupled with Japan’s 7th Strategic Energy Plan, which mandates decarbonized power adoption in heavy industry, thermal ceramics with hydrogen resistance, thermal shock stability, and extended service life are becoming indispensable to Japan’s industrial transition.

Germany: Euro 7 Compliance and Circular Refractory Economics

Germany continues to lead Europe in integrating thermal ceramics into ESG-driven industrial frameworks, with Euro 7 standards acting as a powerful accelerator. The 2025 Euro 7 update has intensified focus on non-exhaust emissions, prompting German automotive and mobility suppliers to scale production of ceramic-coated brake discs and high-temperature exhaust insulation systems. These applications require ceramics that can simultaneously manage extreme thermal loads and minimize particulate emissions, elevating demand for advanced oxide ceramics and engineered coatings.

Circularity is equally central to Germany’s thermal ceramics strategy. RHI Magnesita expanded its MIRECO refractory recycling program across Germany and Italy between 2024 and 2025, enabling the recovery and reuse of spent linings from steel and cement kilns. This model materially reduces embodied carbon while stabilizing raw material supply amid volatile magnesia and alumina markets. Complementing these efforts, Saint-Gobain commissioned a new low-carbon stone wool insulation plant in 2025, supplying German furnace operators with high-performance insulation engineered to meet stringent energy-intensity benchmarks.

India: PLI-Led Refractory Localization and Steel-Driven Demand

India’s thermal ceramics market is entering a scale-up phase driven by Production Linked Incentive (PLI) deployment and aggressive steel capacity expansion. By September 2025, ₹23,946 crore had been disbursed across PLI schemes, with the Specialty Steel and White Goods sectors creating strong downstream demand for magnesia-carbon bricks, alumina monolithics, and advanced insulation systems. New domestic manufacturing facilities for air conditioners, LEDs, and industrial equipment are structurally increasing consumption of high-performance thermal ceramics.

Steel remains the dominant long-term driver. With a national target of 300 MTPA steel capacity by 2030, India’s Ministry of Steel is actively incentivizing domestic refractory production to reduce import dependence, particularly on Chinese magnesia-based products. This policy environment is fostering local capacity in high-durability linings and low-iron insulation ceramics, while regional developments—such as Southeast Asian semiconductor and electronics investments—are opening secondary export channels for Indian-produced thermal and dielectric ceramics.

United Kingdom: Low-Carbon Stone Wool and Aerospace Heat Resistance

The United Kingdom is carving out a focused position in low-carbon thermal insulation and aerospace-grade ceramics, aligning industrial heat management with climate commitments. In May 2025, Saint-Gobain inaugurated its first low-carbon stone wool plant in the UK, utilizing electric melting technology to achieve substantially lower embodied carbon. With an annual capacity of 50,000 tons, the facility supports both industrial furnaces and energy-efficient building envelopes, reinforcing the UK’s role in sustainable thermal insulation.

Aerospace applications provide a parallel growth axis. In 2025, the UK Midlands aerospace cluster recorded a 15% increase in R&D investment into ceramic matrix composites (CMCs) for next-generation jet engines. These materials enable higher operating temperatures, directly improving fuel efficiency and reducing lifecycle emissions. As global aerospace platforms push thermal limits, the UK’s specialization in CMCs positions its thermal ceramics sector at the intersection of sustainability and high-value propulsion technology.

2025 Strategic Matrix: Thermal Ceramics National Developments

Thermal Ceramics Strategic Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Key Material Focus

|

|

United States

|

Semiconductor reshoring

|

RHI Magnesita–Resco acquisition

|

Alumina monolithics & kiln linings

|

|

China

|

Energy conservation mandates

|

2.5% national energy intensity target

|

Ceramic fiber & micro-fine glass

|

|

Japan

|

GX 2040 decarbonization

|

¥20T GX transition bond deployment

|

AES fibers & high-purity ceramics

|

|

Germany

|

ESG & Euro 7 compliance

|

MIRECO refractory recycling expansion

|

Brake & exhaust ceramic coatings

|

|

India

|

PLI & steel expansion

|

₹23,946 Cr PLI disbursement

|

Magnesia-carbon & specialty refractories

|

|

United Kingdom

|

Low-carbon manufacturing

|

Stone wool electric-melt plant launch

|

Stone wool & aerospace CMCs

|

Thermal Ceramics Market Report Scope

Thermal Ceramics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.9 Billion

|

|

Market Size (2035)

|

$12.3 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Material Type (Ceramic Fibers, Insulating Firebricks, Microporous Insulation, Ceramic Matrix Composites, Thermal Barrier Coatings), By Temperature Range (1000–1200 °C, 1200–1500 °C, Above 1500 °C), By Product Form (Blankets & Mats, Boards & Blocks, Papers & Felts, Castables & Monolithics, Ropes & Braids), By Application (Mining & Metal Processing, Power Generation, Petrochemical, Automotive, Aerospace)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Morgan Advanced Materials plc, Alkegen, RHI Magnesita N.V., Luyang Energy-Saving Materials Co. Ltd., Ibiden Co. Ltd., Isolite Insulating Products Co. Ltd., Pyrotek Inc., Saint-Gobain S.A., Vesuvius plc, Nutec Group, Rath Group, Mitsubishi Chemical Corporation, 3M Company, Zircar Ceramics Inc., Promat

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Thermal Ceramics Market Segmentation

By Material Type

- Ceramic Fibers

- Insulating Firebricks

- Microporous Insulation

- Ceramic Matrix Composites (CMCs)

- Thermal Barrier Coatings (TBC)

By Temperature Range

- 1000°C to 1200°C

- 1200°C to 1500°C

- Above 1500°C

By Product Form

- Blankets & Mats

- Boards & Blocks

- Papers & Felts

- Castables & Monolithics

- Ropes & Braids

By Application

- Mining & Metal Processing

- Power Generation

- Petrochemical

- Automotive

- Aerospace

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Thermal Ceramics Market

- Morgan Advanced Materials plc

- Alkegen

- RHI Magnesita N.V.

- Luyang Energy-Saving Materials Co., Ltd.

- Ibiden Co., Ltd.

- Isolite Insulating Products Co., Ltd.

- Pyrotek Inc.

- Saint-Gobain S.A.

- Vesuvius plc

- Nutec Group

- Rath Group

- Mitsubishi Chemical Corporation

- 3M Company

- Zircar Ceramics, Inc.

- Promat

*- List not Exhaustive