UV Water Treatment Systems Market Overview – Size, Growth, and Strategic Imperatives

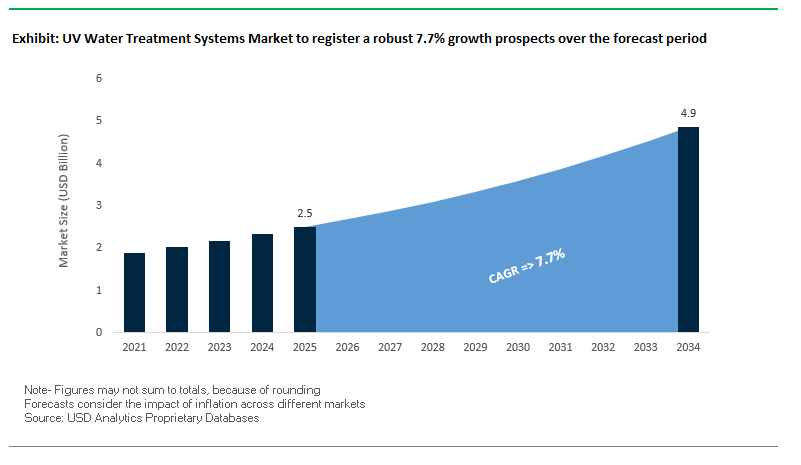

The global UV Water Treatment Systems market is projected to reach USD 2.5 billion in 2025 and expand to USD 4.9 billion by 2034, registering a CAGR of 7.7% during the forecast period. The growth is fueled by stricter international water quality regulations, rising concerns over chlorine-resistant pathogens, and a shift toward sustainable, chemical-free disinfection methods.

Regulatory frameworks such as the U.S. EPA Surface Water Treatment Rule and the IMO Ballast Water Management Convention are accelerating UV adoption by municipal utilities and industrial operators. UV technology’s proven ability to neutralize pathogens like Cryptosporidium and Giardia without producing harmful disinfection byproducts positions it as a preferred solution for safe water treatment.

Industry advancements are further propelling the market, with energy-efficient UV systems like Xylem’s Wedeco Spektron series are delivering operational cost savings of up to 50% and meeting sustainability objectives. Meanwhile, Advanced Oxidation Processes (AOPs) are gaining traction to address micropollutants, including pharmaceuticals and pesticides, as water treatment regulations grow more stringent.

The market is also seeing increased demand for modular, decentralized UV systems for rural communities, small municipalities, and onsite industrial applications, offering scalable and cost-effective alternatives to centralized facilities.

Strategic Imperatives for Shareholders:

- Capitalize on Regulatory Tailwinds: Align product portfolios with evolving EPA, IMO, and EU water quality mandates.

- Invest in Energy-Efficient Innovations: Prioritize low-energy UV systems to meet both cost and sustainability requirements.

- Leverage AOP Integration: Target the growing segment focused on micropollutant removal for premium market positioning.

- Expand Modular Offerings: Address underserved markets with flexible, plug-and-play UV treatment systems.

Market Analysis – Recent Developments and Competitive Positioning

The UV water treatment sector is experiencing a wave of technological launches, strategic mergers, and infrastructure investments, reshaping the competitive landscape.

In March 2025, Xylem introduced new additions to its Wedeco Spektron UV series, certified to the latest global standards and delivering up to a 50% reduction in energy use an efficiency benchmark for water treatment plants. Just a month later, in April 2025, Kurita America merged with Avista Technologies, enhancing its integrated water treatment portfolio with a stronger emphasis on UV pre-treatment in membrane systems.

By June 2025, Xylem’s TrojanUV brand launched an AOP Demonstration System at ACE 2025, enabling municipalities and industries to test solutions for persistent contaminants before full-scale deployment. That same month, Veolia unveiled its Drop® PFAS destruction technology, capable of achieving 99.9999% elimination of targeted compounds, often paired with UV as part of a multi-barrier strategy.

Infrastructure expansion is also underway. In August 2025, the City of Florence, Oregon, neared completion of its UV Disinfection System Improvement Project, aimed at boosting capacity and redundancy for municipal wastewater treatment. In July 2025, H2O America acquired Quadvest for USD 540 million, announcing plans to invest over USD 500 million in modernization projects that will incorporate advanced UV and AOP solutions.

Globally, hybrid disinfection approaches are gaining traction. SUEZ, now part of Veolia, secured a contract in October 2024 to upgrade a Danish wastewater plant for pharmaceutical residue removal, employing inline ozonation and GAC filtration alongside UV processes. The growing preference for multi-barrier systems underscores UV’s integral role in comprehensive water treatment frameworks.

Trends and Opportunities in UV Water Treatment Systems Market

Trend 1: UV-LED Technology Disrupts Traditional Mercury Lamp Systems

The UV water treatment systems market is witnessing a major shift with UV-LED technology replacing conventional mercury-based lamps. UV-LEDs offer instant on/off functionality, reducing energy consumption by up to 25% in point-of-use systems, while eliminating warm-up delays typical of mercury lamps. Their extended lifespan and ability to handle tens of thousands of on/off cycles improve operational efficiency and reduce replacement frequency. Mercury-free construction aligns with global environmental standards, mitigating disposal risks associated with toxic mercury. Compact and durable, UV-LED systems can be integrated into diverse applications, from residential under-sink units to industrial and municipal-scale systems, offering flexibility, reliability, and sustainability for modern water treatment.

Trend 2: Municipalities Adopt UV as Primary Disinfection Method Over Chlorine

Municipal water treatment plants are increasingly choosing UV disinfection to meet strict microbial safety standards while avoiding harmful disinfection byproducts (DBPs) like trihalomethanes (THMs) and haloacetic acids (HAAs) associated with chlorine. UV systems effectively inactivate chlorine-resistant pathogens such as Cryptosporidium and Giardia, achieving up to 99.99% microbial removal in seconds. The chemical-free process ensures safe drinking water, reduces residual chemicals, and minimizes environmental impact. Multi-barrier approaches combining UV with low doses of chlorine or chloramine enhance reliability, providing redundancy to maintain water safety even during unexpected operational variations, making UV a critical technology for municipal utilities worldwide.

Opportunity 1: Portable UV Water Purifiers for Emergency & Outdoor Recreation Markets

The growing demand for safe drinking water in emergency and outdoor scenarios presents a substantial opportunity for portable UV water purifiers. Battery-powered pens and straw-style devices offer rapid disinfection, treating a liter of water in under 90 seconds, much faster than chemical alternatives like iodine tablets. Their lightweight and compact design makes them ideal for hikers, travelers, and disaster response teams. Portable UV systems are versatile, able to treat clear water from streams, ponds, and rivers without altering taste, color, or odor. Their portability, speed, and chemical-free operation make them highly suitable for humanitarian aid, outdoor recreation, and emergency preparedness markets.

Opportunity 2: UV-AOP (Advanced Oxidation Process) for Pharmaceutical & Chemical Removal

Advanced oxidation processes (AOPs) combining UV light with oxidants like hydrogen peroxide provide an innovative solution for degrading persistent organic pollutants (POPs), pharmaceuticals, and pesticides in water. UV-AOP systems efficiently break down chemically stable and small-molecule contaminants resistant to conventional treatment, achieving high removal rates (for example, up to 87.6% COD reduction in pharmaceutical wastewater studies). Compact design allows easy retrofitting into existing water treatment infrastructure, reducing capital costs and spatial requirements. As regulatory frameworks increasingly target trace pharmaceuticals and endocrine-disrupting chemicals (EDCs), UV-AOP systems enable utilities to proactively meet future compliance standards while delivering high-quality, contaminant-free water.

UV Water Treatment Systems Market Share Insights

Residential and Commercial UV Systems Lead Market Penetration

Residential UV systems dominate the market in 2025, accounting for approximately 30.4% of global unit shipments. Growth is driven by homeowner awareness of waterborne pathogens and the preference for chemical-free, point-of-use (under-sink) and point-of-entry (whole-house) solutions for well water or municipal backup. Commercial UV systems represent a high-value growth segment, deployed across hotels, hospitals, schools, offices, and restaurants. Demand is largely fueled by Legionella prevention mandates, safe drinking water requirements, and process water disinfection in food service and institutional facilities, reflecting a strong combination of volume and revenue growth potential.

.png)

Low Pressure UV Remains the Efficiency Standard Across Applications

Low Pressure (LP) UV lamps hold a 55.4% market share, reflecting their dominance in residential, commercial, and municipal drinking water applications. Valued for high electrical efficiency and optimal 254nm germicidal wavelength, LP UV is ideal for clear water applications where consistent pathogen inactivation is required. Medium Pressure (MP) UV (34.5%) serves as the industrial and wastewater powerhouse, offering higher intensity and broader spectrum penetration to handle turbid waters and high organic loads, making it essential for industrial, municipal wastewater, and challenging process water applications. Emerging UV technologies like LED and pulsed UV are gaining attention for smart, compact, and specialized industrial applications, though adoption is currently limited by cost and power output.

Drinking Water and Wastewater Applications Drive Volume and Compliance

Drinking water disinfection is the largest application (40.6%), spanning residential wells, commercial buildings, and municipal water treatment plants, driven by chemical-free pathogen control mandates. Wastewater treatment (24.9%) is critical for environmental compliance, particularly in municipal and industrial effluent disinfection before river discharge or irrigation reuse, with medium-pressure UV systems frequently deployed in the segment. Process water treatment ensures microbial-free water in pharmaceuticals, food & beverage, and microelectronics, where contamination could disrupt manufacturing or compromise product quality. Niche applications include aquaculture and swimming pools, focusing on animal health and recreational water quality, while emergency water supply relies on portable UV units for disaster relief, military, and remote deployments.

Smart Features Enhance Monitoring and Maintenance Efficiency

Dose monitoring (35.2%) is the fundamental smart feature, using UV intensity sensors and flow meters to ensure that the required germicidal dose is consistently delivered, meeting compliance standards. Remote monitoring provides IoT-based connectivity, enabling centralized oversight, multi-unit management, and reduced site visits. Auto-cleaning mechanisms protect system performance by preventing fouling of quartz sleeves and maintaining UV transmittance, while predictive maintenance leverages AI algorithms to anticipate lamp failure or sleeve fouling, reducing downtime and enhancing operational reliability across residential, commercial, and municipal installations.

Country Analysis of the UV Water Treatment Systems Market

United States: Driving UV Water Disinfection Through Regulatory Support and Smart Systems

The United States market for UV water treatment systems is propelled by the EPA’s tightening regulations on contaminants, including PFAS, driving the adoption of advanced oxidation processes (AOPs) that integrate UV disinfection with chemicals like hydrogen peroxide. The Bipartisan Infrastructure Law allocates over $50 billion for water and wastewater infrastructure upgrades, creating a strong demand for modernized UV disinfection technologies. Municipalities are increasingly investing in IoT-enabled smart monitoring systems, which provide real-time data on water quality, optimize disinfection, reduce energy consumption, and ensure regulatory compliance. Industry players like Xylem have achieved California State Water Resources Control Board approval for Wedeco LBX 850e and LBX 1500e UV systems, endorsing their effectiveness for unrestricted water reuse applications. Additionally, the Department of the Interior’s $300 million funding for water recycling and desalination projects further supports the adoption of advanced UV treatment technologies in the U.S.

China: Expanding UV Disinfection Driven by National Water Infrastructure Initiatives

China’s Water Ten Plan and Beautiful China initiative are central to national water safety, fueling substantial investments in UV water treatment systems. The government has set ambitious targets of 95% wastewater treatment for all county-level cities, which drives adoption of high-performance disinfection technologies. SUEZ’s recent project in Jining Industrial Park, aimed at achieving 100% wastewater recycling, demonstrates the integration of UV disinfection and advanced filtration for industrial applications. The Ministry of Ecology and Environment mandates real-time emission disclosure for key enterprises, emphasizing the need for constantly monitored UV disinfection systems. Between 2017 and 2022, RMB 673 billion was allocated to water pollution control, reinforcing market growth and the adoption of sustainable and high-efficiency UV water treatment technologies.

India: Promoting Smart, IoT-Enabled UV Disinfection in Rural and Urban Areas

India’s Jal Jeevan Mission is creating a strong market for UV water treatment systems by deploying sensor-based IoT devices in over six lakh villages to monitor rural drinking water supply networks. The CPCB’s stringent discharge standards for all STPs are driving adoption of advanced UV disinfection technologies capable of meeting regulatory requirements. The government also promotes water ATMs, mobile or containerized purification units that rely on on-site UV disinfection to ensure safe drinking water. Additionally, the Namami Gange Mission supports decentralized wastewater treatment systems in smaller cities and rural regions, where conventional centralized plants are impractical, highlighting the importance of final-stage UV disinfection for safe and sustainable water reuse.

Germany (Europe): Integrating UV Disinfection with Tertiary Treatment and Energy-Efficient Systems

Germany’s UV water treatment market is influenced by the EU’s Urban Wastewater Treatment Directive, which requires treatment for communities above 1,000 population-equivalents and drives demand for advanced UV disinfection solutions. Extended Producer Responsibility mandates pharmaceutical and cosmetics companies to contribute to the costs of micropollutant removal, promoting the use of tertiary treatment and AOPs integrated with UV disinfection. Germany emphasizes energy efficiency and resource recovery, leading to the adoption of intelligent monitoring systems and UV technologies that optimize operational performance while lowering energy usage. The Fraunhofer-Allianz SysWasser initiative consolidates expertise to develop system-oriented water extraction and disinfection solutions, ensuring sustainable and modular water treatment infrastructure.

South Korea: Advancing UV Disinfection Through Filtration Integration and IoT Innovation

South Korea has positioned its water technology sector as a strategic growth area, offering R&D support for advanced disinfection systems. The Korean Register of Shipping provides U.S. Coast Guard-type approvals, giving local companies a competitive advantage in maritime applications, where UV disinfection systems play a key role. The market emphasizes integrating advanced filtration technologies to support disinfection stages in both municipal and residential applications. Companies like LG Electronics are introducing smart, IoT-enabled purifiers in South Korea and Japan that incorporate UV technology, enhancing water quality monitoring, predictive maintenance, and energy-efficient disinfection performance.

Japan: Leading Innovations in Microplastics Removal and Advanced UV Disinfection

Japan is a global leader in advanced UV water treatment systems, particularly for applications targeting microplastics and high-efficiency water reuse. Mitsui O.S.K. Lines and Miura Co., Ltd. developed devices to collect microplastics at sea, serving as a pre-treatment stage that enhances UV disinfection efficiency. The KUBOTA Submerged Membrane Unit reclaims effluent efficiently, supporting sustainable water reuse. Fukuoka’s desalination plant employs innovative ultrafiltration membranes in place of sand filtration, providing a stable supply of clean seawater and improving the effectiveness of final-stage UV disinfection. Japan’s regulatory framework and sustainability emphasis continue to drive the development of IoT-enabled and machine learning-supported UV disinfection technologies, ensuring reliable, energy-efficient, and environmentally responsible water treatment solutions.

Competitive Landscape – Key Players and Strategic Outlook

The UV water treatment market is dominated by a handful of global leaders leveraging diversified portfolios, technological innovation, and strategic acquisitions to maintain market share.

Xylem Inc. – Expanding Leadership in Integrated UV Solutions

Xylem focuses on delivering smart, interconnected water technology solutions that enhance efficiency and sustainability. With brands like TrojanUV, Wedeco, and Evoqua, Xylem offers UV systems for municipal drinking water, wastewater, reuse, and industrial applications. Recent innovations include the energy-efficient Wedeco Spektron series and the pilot-scale TrojanUV AOP Demonstration System. Its portfolio strength lies in combining UV disinfection with advanced monitoring platforms like Rivo™ I and Hubgrade, optimizing compliance and operational performance.

Kurita Water Industries Ltd. – Integrating Chemical and Physical Treatment Expertise

Kurita specializes in creating unique value through comprehensive water and environmental solutions. Its offerings span UV disinfection, membrane filtration, and advanced chemical dosing, with a focus on industry-specific applications such as food and beverage or power generation. The April 2025 merger of Kurita America and Avista Technologies strengthens its integrated approach, blending membrane treatment and UV systems for optimized water quality management.

Veolia Environnement S.A. – Driving Ecological Transformation Through Innovation

Veolia delivers a full range of disinfection solutions including UV, ozonation, and chemical dosing are integrated into large-scale water reuse and resource security projects. The company’s patented Drop® PFAS destruction technology, launched in June 2025, enhances its advanced oxidation capabilities. Its Hubgrade digital platform supports AI-powered optimization, reinforcing its position as a leader in smart, sustainable water solutions.

SUEZ (Part of Veolia) – Specialist in Multi-Barrier Treatment Solutions

Before its integration into Veolia, SUEZ maintained a strong UV market presence, with advanced disinfection systems deployed globally. Its October 2024 project in Denmark showcased a hybrid treatment model using UV alongside ozonation and GAC filtration for pharmaceutical residue removal. The brand’s expertise in meeting stringent micropollutant regulations continues under the Veolia umbrella.

Pentair – Bridging Residential and Industrial UV Applications

Pentair offers advanced disinfection technologies for residential, commercial, and industrial markets, with strong brand recognition in foodservice (via Everpure) and residential point-of-entry systems. The acquisition of Porous Media expanded its industrial filtration capabilities, complementing UV in comprehensive treatment solutions. Pentair also provides certified technologies for PFAS removal, addressing one of the most urgent water quality challenges globally.

UV Water Treatment Systems Market Report Scope

UV Water Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.5 Billion

|

|

Market Size (2034)

|

$4.9 Billion

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By System Type (Residential UV Systems, Commercial UV Systems, Municipal UV Systems, Industrial UV Systems), By Lamp Technology (Low Pressure (LP) UV, Medium Pressure (MP) UV, Light Emitting Diode (LED) UV, Pulsed UV), By Application (Drinking Water Disinfection, Wastewater Treatment, Process Water Treatment, Aquaculture & Pools, Emergency Water Supply), By Component Type (UV Chambers/Reactors, UV Lamps, Quartz Sleeves, Control Systems, Sensors & Monitors), By Smart Features (Dose Monitoring, Auto-cleaning Mechanisms, Remote Monitoring, Predictive Maintenance)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Xylem Inc., Trojan Technologies, Veolia Water Technologies, SUEZ, Halma Group, De Nora S.p.A., Atlantium Technologies Ltd., Pentair, Evoqua Water Technologies (now part of Xylem), Calgon Carbon Corporation, Aquionics, Atlantic Ultraviolet Corporation, BWT Holding GmbH, ProMinent GmbH, Watts Water Technologies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

UV Water Treatment Systems Market Segmentation

By System Type

- Residential UV Systems

- Commercial UV Systems

- Municipal UV Systems

- Industrial UV Systems

By Lamp Technology

- Low Pressure (LP) UV

- Medium Pressure (MP) UV

- Light Emitting Diode (LED) UV

- Pulsed UV

By Application

- Drinking Water Disinfection

- Wastewater Treatment

- Process Water Treatment

- Aquaculture & Pools

- Emergency Water Supply

By Component Type

- UV Chambers/Reactors

- UV Lamps

- Quartz Sleeves

- Control Systems

- Sensors & Monitors

By Smart Features

- Dose Monitoring

- Auto-cleaning Mechanisms

- Remote Monitoring

- Predictive Maintenance

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in UV Water Treatment Systems Market

- Xylem Inc.

- Trojan Technologies

- Veolia Water Technologies

- SUEZ

- Halma Group

- De Nora S.p.A.

- Atlantium Technologies Ltd.

- Pentair

- Evoqua Water Technologies (now part of Xylem)

- Calgon Carbon Corporation

- Aquionics

- Atlantic Ultraviolet Corporation

- BWT Holding GmbH

- ProMinent GmbH

- Watts Water Technologies

* List Not Exhaustive

Research Coverage

This report investigates the Global UV Water Treatment Systems Market, presenting in-depth analysis reviews of regulatory drivers, technological breakthroughs, and strategic shifts shaping the industry from 2025 to 2034. Published by USDAnalytics, the study highlights how global mandates such as the U.S. EPA Surface Water Treatment Rule and the IMO Ballast Water Management Convention are accelerating adoption of UV disinfection technologies. The report reviews milestones including UV-LED disruption, advanced oxidation processes (AOPs) for micropollutant removal, modular UV systems for decentralized applications, and energy-efficient innovations such as Xylem’s Wedeco Spektron series. With coverage of infrastructure investments, mergers, and smart IoT-enabled monitoring platforms, this report is an essential resource for utilities, regulators, technology providers, and investors seeking strategic insights into the rapidly expanding UV water treatment market.

Scope Includes:

- Segmentation: By Technology (Low Pressure UV, Medium Pressure UV, UV-LED, Pulsed UV, Hybrid UV-AOP), By Application (Drinking Water, Wastewater, Process Water, Aquaculture & Pools, Emergency/Portable Systems), By End-User (Residential, Commercial, Municipal, Industrial).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic Data: 2021 to 2024, and Forecast Data: 2025 to 2034.

- Companies: Profiles and competitive analysis of 15+ leading players including Xylem, Trojan Technologies, Veolia, SUEZ, Kurita, and Pentair.

Methodology

The research methodology employed by USDAnalytics combines primary and secondary research to deliver accurate and actionable market intelligence. Primary inputs were collected through interviews with utilities, technology providers, regulators, and industrial operators to validate demand trends, regulatory impacts, and technology adoption. Secondary research included analysis of company filings, government regulations, international project databases, and peer-reviewed publications. Market sizing was derived through top-down and bottom-up triangulation, aligning installation data, contract values, and technology penetration rates. Forecast models incorporated multiple scenarios including accelerated PFAS mandates, UV-LED cost reductions, and decentralized adoption in rural and industrial settings, ensuring projections reflect both regulatory imperatives and technological innovation.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: UV Water Treatment Systems Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Shareholders

1.3. Global Market Snapshot

2. UV Water Treatment Systems Market Outlook (2025–2034)

2.1. Market Valuation and Growth Projections

2.1.1. Current Market Size (2025): USD 2.5 Billion

2.1.2. Forecasted Market Size (2034): USD 4.9 Billion at 7.7% CAGR

2.2. Key Drivers and Market Dynamics

2.2.1. Stricter Water Quality Regulations

2.2.2. Rising Concerns over Chlorine-Resistant Pathogens

2.2.3. Shift to Sustainable, Chemical-Free Disinfection

3. Market Analysis: Recent Developments and Competitive Positioning

3.1. Overview of Technology Launches, Mergers, and Investments

3.2. Recent Strategic Developments of Key Players

3.2.1. Xylem's New Wedeco Spektron UV Series (March 2025)

3.2.2. Kurita America and Avista Technologies Merger (April 2025)

3.2.3. TrojanUV AOP Demonstration System Launch (June 2025)

3.2.4. Veolia's Drop® PFAS Destruction Technology (June 2025)

3.3. Infrastructure Expansion and Multi-Barrier Systems

4. Trends and Opportunities in the UV Water Treatment Systems Market

4.1. Trend 1: UV-LED Technology Disrupts Traditional Mercury Lamps

4.1.1. Energy Efficiency and Extended Lifespan

4.1.2. Mercury-Free and Compact Design

4.2. Trend 2: Municipalities Adopt UV as Primary Disinfection Method

4.2.1. Avoiding Harmful Disinfection Byproducts (DBPs)

4.2.2. Inactivation of Chlorine-Resistant Pathogens

4.3. Opportunity 1: Portable UV Water Purifiers

4.3.1. Rapid Disinfection for Emergency and Outdoor Use

4.3.2. Lightweight, Versatile, and Chemical-Free

4.4. Opportunity 2: UV-AOP for Pharmaceutical & Chemical Removal

4.4.1. Degrading Persistent Organic Pollutants

4.4.2. Compact Retrofitting for Existing Infrastructure

5. UV Water Treatment Systems Market Share Insights

5.1. By System Type

5.1.1. Residential and Commercial UV Systems Lead Market Penetration

5.1.2. Municipal and Industrial UV Systems

5.2. By Lamp Technology

5.2.1. Low Pressure (LP) UV Remains the Efficiency Standard

5.2.2. Medium Pressure (MP) and UV-LED

5.3. By Application

5.3.1. Drinking Water and Wastewater Applications Drive Growth

5.3.2. Process Water, Aquaculture & Pools, and Emergency Supply

5.4. By Smart Features

5.4.1. Dose Monitoring and Remote Monitoring

5.4.2. Auto-cleaning Mechanisms and Predictive Maintenance

6. Country Analysis of the UV Water Treatment Systems Market

6.1. United States: Driving UV Through Regulatory Support and Smart Systems

6.2. China: Expanding UV Disinfection Driven by National Initiatives

6.3. India: Promoting Smart, IoT-Enabled UV Disinfection

6.4. Germany (Europe): Integrating UV with Tertiary Treatment

6.5. South Korea: Advancing UV Through Filtration Integration

6.6. Japan: Leading Innovations in Microplastics Removal

7. Competitive Landscape: Key Players and Strategic Outlook

7.1. Xylem Inc.: Expanding Leadership in Integrated UV Solutions

7.2. Kurita Water Industries Ltd.: Integrating Chemical and Physical Treatment

7.3. Veolia Environnement S.A.: Driving Ecological Transformation

7.4. SUEZ (Part of Veolia): Specialist in Multi-Barrier Treatment

7.5. Pentair: Bridging Residential and Industrial UV Applications

8. Market Size Outlook by Region (2025–2034)

8.1. North America Market Size Outlook to 2034

8.1.1. By System Type

8.1.2. By Application

8.2. Europe Market Size Outlook to 2034

8.2.1. By System Type

8.2.2. By Application

8.3. Asia Pacific Market Size Outlook to 2034

8.3.1. By System Type

8.3.2. By Application

8.4. South America Market Size Outlook to 2034

8.4.1. By System Type

8.4.2. By Application

8.5. Middle East and Africa Market Size Outlook to 2034

8.5.1. By System Type

8.5.2. By Application

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations