Waterborne UV Curable Resins Market Size, Overview, and Growth Outlook (2025–2034)

Waterborne UV Curable Resins Market Expected to More Than Double by 2034 Driven by Sustainability and Performance Demands

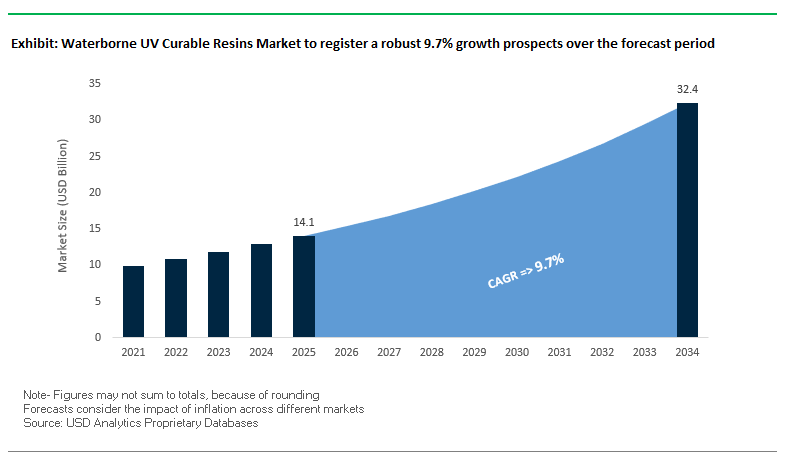

The global waterborne UV curable resins market is projected to grow from $14.1 billion in 2025 to $32.4 billion by 2034, representing a CAGR of 9.7%. This market is shaped by the convergence of waterborne technology, which reduces VOC emissions, and UV curing, which enables instant polymerization, creating a high-performance, environmentally friendly solution. These resins are widely used across wood coatings, graphics, electronics, and industrial applications, offering energy efficiency, faster production cycles, and superior durability.

Key Insights for industry professionals and buyers:

- VOC reduction compliance: Waterborne UV curable resins help manufacturers meet stringent environmental regulations on solvent emissions.

- Faster production cycles: UV curing accelerates production while reducing energy consumption compared to conventional thermal drying.

- Enhanced performance: Resins provide scratch, chemical, and heat resistance, making them ideal for furniture, flooring, and automotive interiors.

- Sustainable raw materials: Increased integration of bio-based content helps reduce reliance on fossil fuels and enhances environmental profiles.

- Market growth drivers: Rising demand for eco-friendly coatings, energy-efficient manufacturing, and high-performance protective coatings is fueling market expansion.

Market Analysis: Strategic Developments and Technology Advancements Are Accelerating Market Growth

The waterborne UV curable resins market is experiencing rapid growth driven by technological innovations and strategic industry collaborations. In August 2025, Allnex showcased its UV curable resins at CAMX 2025, highlighting solutions that enable reduced VOC emissions and faster processing for composites. In the same month, Cortec Corporation launched Eco Works 100, a USDA-certified compostable bioplastics product, reinforcing the industry's sustainability focus.

In July 2025, Mondi Group introduced SolmixBag, a water-soluble bag for the construction industry, enhancing operational convenience. A June 2025 study highlighted a composite antimicrobial film made from carrageenan and polyoxometalate, demonstrating excellent bactericidal properties and biodegradability, emphasizing the growing demand for safer, sustainable materials.

Strategic collaborations have also shaped the market’s landscape. Henkel and Celanese partnered in November 2024 to produce water-based adhesives from captured CO2 emissions, enhancing renewable content. Bostik, Dow, and Nordson launched Kizen™ LIME in September 2024, a minimum 80% renewable adhesive for recyclable paper and cardboard. Earlier, in March 2024, Arkema obtained ISCC+ certification for its French UV resin production site, enabling the launch of bio-attributed UV-LED-EB curable resins, reflecting the industry's push toward circular economy solutions.

Trends and Opportunities in the Waterborne UV Curable Resins Market

Development of High-Performance Hybrid Systems for Industrial Coatings

A defining trend in the waterborne UV curable resins market is the strategic development of hybrid resin systems aimed at replacing solvent-based coatings in industrial applications. Technical challenges such as yellowing and reduced curing speed have historically limited adoption, but new light stabilizers are significantly improving performance. For example, a novel light stabilizer (NLS) developed in 2025 was shown to reduce yellowing by up to 79% without compromising curing speed, addressing a long-standing limitation in UV-curable technologies.

Hybrid systems are also redefining industrial coatings by combining the benefits of multiple chemistries. Silicone epoxide hybrid resins, as highlighted by Biesterfeld SE, bring together the toughness of epoxy resins with the weatherability of silicone topcoats. This creates a single-layer protective system capable of withstanding demanding industrial environments such as metal protection, heavy machinery, and high-wear surfaces.

Additionally, the industry’s pivot toward high-solid waterborne UV systems is directly aligned with global Volatile Organic Compound (VOC) reduction mandates. BASF’s acrylic and polyurethane dispersions for both 1K and 2K systems enable durable coatings on wood, plastics, and metals with low VOC emissions, making them ideal for eco-conscious manufacturers operating under strict sustainability targets.

Optimization for Sustainable Packaging Inks and Overprint Varnishes

Another transformative trend is the use of waterborne UV resins in sustainable packaging inks and coatings, driven by corporate sustainability pledges and regulatory mandates. Companies such as Sun Chemical have introduced bio-renewable ink systems like SunVisto AquaGreen, which incorporate naturally derived resin content for flexographic and gravure printing, delivering both high scuff resistance and recyclability.

The European Union’s packaging regulations are accelerating adoption of safe, sustainable solutions, particularly for direct food-contact applications. Hubergroup’s HYDRO-X CONTACT series exemplifies this trend, offering inks and varnishes certified for food-safe printing, fully aligned with EU legislation.

From a technical standpoint, resolubility during recycling is emerging as a critical property. BASF’s Joncryl® line demonstrates how resins can maintain print performance while being easily removed in recycling processes, ensuring that inks do not contaminate the recovered material stream. This dual functionality—durability in use and compatibility in recycling positions waterborne UV resins as central to the circular economy in packaging.

Enabling the Digital Printing of Electronics and Functional Materials

One of the most promising opportunities in the waterborne UV curable resins market is their use in printed electronics and flexible functional materials. The combination of precision inkjet application and low-temperature UV curing makes these resins highly suitable for substrates sensitive to heat, such as flexible plastics used in wearables, sensors, and OLED displays.

Beyond acting as a binder, waterborne UV resins are being designed to integrate functional materials. SioResin’s waterborne polyurethane acrylic UV resin demonstrates this potential, offering scratch resistance for optical films and consumer electronics coatings. Furthermore, the ability to incorporate conductive or dielectric additives opens up opportunities for printed circuit components and protective films, directly supporting the growth of IoT devices and smart consumer products.

Formulating for Consumer-Safe and Direct-Food-Contact Applications

Another high-value opportunity is the formulation of consumer-safe UV-curable resins tailored for direct food-contact and child-safe applications. With low odor, low migration, and complete curing, these resins are now being approved for use inside packaging where consumer exposure is a concern. Hubergroup’s HYDRO-X CONTACT inks illustrate how waterborne UV systems can comply with stringent food safety regulations while offering new design flexibility for food packaging.

Applications extend beyond food packaging into children’s toys, furniture, and premium consumer goods. BASF’s Joncryl® DFC series, with enhanced rub and block resistance, demonstrates the readiness of UV resins for high-performance, consumer-facing markets. These formulations deliver durability, safety, and regulatory compliance, making them essential for brands targeting sustainability and consumer trust.

Competitive Landscape: Leading Companies Are Shaping the Future of Waterborne UV Curable Resins Through Innovation and Sustainability

The waterborne UV curable resins market is highly competitive, with major players leveraging materials science expertise, manufacturing excellence, and sustainability innovations to deliver high-performance solutions across industries.

Allnex: Driving Sustainable and Fast-Curing Coating Solutions with Advanced UV Resins

Allnex offers waterborne UV curable resins under UCECOAT® and EBECRYL® brands for industrial wood coatings and composites. In August 2025, Allnex participated in CAMX 2025 to showcase advanced formulations and promote ECOWISE™ sustainable solutions. Its core strengths include deep materials expertise, a broad sustainable product range, and vertically integrated operations, positioning it as a leader in the global coating resins market.

BASF SE: Expanding High-Performance, Eco-Friendly UV Resin Solutions Across Industrial Applications

BASF provides waterborne UV curable resins under the LAROMER® brand, used in automotive coatings, furniture, and flooring. Recent innovations include LAROMER UA 9005 Aqua ECO, a urethane-modified acrylic resin for radiation-curable coatings. BASF’s core strengths lie in brand recognition, chemical expertise, and integrated global operations, supporting its strategic focus on sustainable, high-quality, and compliant solutions.

Covestro AG: Innovating Waterborne UV Resins for Industrial Coatings and Sustainable Applications

Covestro offers Bayhydrol® and NeoRad™ product lines, used in wood coatings, printing inks, and packaging. In February 2024, Covestro launched high-performing waterborne UV resins for industrial applications and explored self-initiating resin technologies. Covestro’s strategy focuses on circularity and climate neutrality by 2035, supported by its strong brand recognition and vertically integrated operations.

Dymax Corporation: Pioneering Light-Curable Adhesives with a Focus on Circular Economy Compliance

Dymax manufactures light-curable adhesives, coatings, and encapsulants with a strong sustainability focus. Its recent TPO-free adhesive range addresses regulatory and market demands for environmentally friendly solutions. Dymax leverages materials expertise, sustainable innovation, and integrated operations, maintaining a leadership position in light-curable resin markets.

Arkema Group: Leading Specialty Chemical Innovations with Bio-Attributed UV Resin Technologies

Arkema delivers Sartomer® and Sarbio® product lines for coatings, 3D printing, and graphic arts. In March 2024, Arkema obtained ISCC+ certification for bio-attributed UV-LED-EB resins and continues to develop renewable raw material technologies. Its strategy emphasizes high-quality, compliant solutions across global specialty chemicals markets, backed by strong brand recognition and integrated operations.

Waterborne UV Curable Resins Market Share Insights, 2025-2034

Polyurethane Acrylates Dominate Market Share by Chemistry Type in the Waterborne UV Curable Resins Industry

Waterborne UV polyurethane acrylates lead the chemistry segmentation with nearly 45% share, reflecting their superior balance of mechanical durability, chemical resistance, and rapid-curing performance. This dominance is rooted in their ability to deliver abrasion resistance, flexibility, and strong adhesion across substrates like wood, plastics, and automotive interiors. Their widespread use in wood flooring, furniture, and high-performance coatings highlights the synergy between environmental compliance—low VOC emissions—and industrial efficiency, as they allow high-speed curing on automated lines. In contrast, waterborne UV acrylics remain a lower-cost alternative for packaging and printing, while epoxy and polyester acrylates carve out smaller shares for applications demanding niche properties such as extreme hardness or intermediate flexibility. The commanding position of polyurethane acrylates underscores how performance versatility and sustainability compliance are now the decisive factors in resin adoption.

Wood & Furniture Hold the Largest Market Share by End-Use in the Waterborne UV Curable Resins Industry

The wood and furniture sector commands around 35% of the market, making it the leading end-use industry for waterborne UV curable resins. This leadership is driven by the furniture industry’s need for coatings that combine high durability with environmentally responsible formulations. UV-cured waterborne resins enable manufacturers to achieve superior scratch resistance, high-gloss finishes, and immediate handling strength, which significantly reduces production cycle times. Additionally, the sector’s focus on reducing VOC emissions and meeting stringent indoor air quality standards makes these resins a natural fit. Their use in flooring, cabinetry, and paneling has set a benchmark for sustainable yet high-performance coatings, positioning the wood and furniture segment as both the largest and most strategically significant market for resin suppliers.

European Union: Green Deal, Horizon Europe, and Allnex Leading Sustainable Innovations

The European Union waterborne UV curable resins market is strongly driven by sustainability policies and regulatory frameworks under the European Green Deal, which targets climate neutrality by 2050. The Packaging and Packaging Waste Regulation (PPWR) and the REACH regulation enforced by the European Chemicals Agency (ECHA) are restricting the use of hazardous chemicals and VOCs, accelerating the shift toward safer, eco-friendly resin formulations. Funding programs such as Horizon Europe are actively supporting bio-based UV-curing monomers and oligomers, with collaborations across German and Belgian universities pushing innovation in high-performance sustainable coatings.

Leading companies like allnex are setting benchmarks with products such as UCECOAT® 7999, a bio-based, tin-free, and APEO-free polyurethane dispersion designed for industrial wood coatings. The automotive sector is emerging as a significant end-user, with manufacturers adopting UV-curable resins for interior and exterior applications to reduce emissions while enhancing coating performance. This synergy between strict regulation, corporate innovation, and strong demand from automotive and industrial sectors ensures steady market expansion across the EU.

United States: EPA VOC Regulations and Demand from Automotive, Electronics, and 3D Printing

The United States waterborne UV curable resins market is driven by strict VOC emission regulations from the Environmental Protection Agency (EPA) and local air quality districts such as California’s South Coast AQMD. These regulations have accelerated the transition from solvent-based to waterborne UV technologies, especially in industries requiring high-performance, eco-friendly coatings. A key example is BASF’s UV-cured automotive primer, which reduces VOCs by more than 50% compared to traditional primers.

The U.S. market is witnessing high demand in electronics, automotive, and furniture industries, where coatings must provide durability, scratch resistance, and aesthetic appeal. Moreover, the 3D printing industry is adopting UV-curable resins for producing durable, high-precision components. This trend highlights the adaptability of waterborne UV resins across diverse industrial sectors. With companies increasingly investing in premium finishes and sustainable manufacturing processes, the U.S. is expected to remain a global leader in this market.

China: 14th Five-Year Plan, Eco-Friendly Regulations, and Rising Wood Coatings Demand

The China waterborne UV curable resins market is rapidly expanding, supported by government policies under the 14th Five-Year Plan, which prioritize green technology adoption and pollution control. Regulations limiting high-VOC coatings and incentives for remanufacturing industries are driving industries to adopt waterborne UV solutions across coatings, adhesives, and inks.

Chinese manufacturers are increasingly investing in automated application systems, integrating smart technologies to improve efficiency and reduce labor costs. The construction boom and growth in furniture and flooring applications are significantly boosting demand for eco-friendly wood coatings based on UV-curable resins. These trends, coupled with the government’s push for cost-effective, low-emission technologies, position China as one of the largest growth markets for waterborne UV resins.

India: Make in India, BIS Standards, and Rising Demand from Construction and Electronics

The India waterborne UV curable resins market is shaped by government-led initiatives like Make in India and Smart Cities, which are stimulating demand in construction, automotive, and woodworking sectors. The Bureau of Indian Standards (BIS) continues to introduce new standards for product safety and performance, encouraging manufacturers to develop eco-friendly and compliant resin formulations.

Consumer awareness of health and environmental risks from VOCs is also driving demand for low-emission coatings. Furthermore, India’s growing electronics industry is adopting waterborne UV resins for high-performance and durable electronic components, underscoring their versatility across sectors. Challenges such as raw material price volatility remain, but companies are investing in local R&D centers to develop new resin formulations tailored to the Indian market.

Japan: DIC Corporation, METI Support, and High-Performance Adhesive Solutions

The Japan waterborne UV curable resins market is led by long-standing innovation from companies like DIC Corporation, which pioneered UV-curable resin technologies in the 1970s and continues to advance organic-inorganic hybridization solutions. These resins are widely used in wood coatings, printing inks, and optical films, underlining their cross-sector applications.

The Ministry of Economy, Trade and Industry (METI) is actively supporting the revitalization of Japan’s manufacturing sector with investments in advanced materials and production technologies. The automotive industry is a key driver, particularly for multi-material designs requiring lightweight yet strong adhesives. With Japan’s commitment to resource efficiency and advanced R&D, the market is evolving toward specialized, high-performance UV solutions that meet both industrial and environmental needs.

Brazil: PNRS Policy, Furniture Sector Demand, and Low-Cost Adhesives Adoption

The Brazil waterborne UV curable resins market is benefiting from sustainability regulations under the National Solid Waste Policy (PNRS), which emphasizes waste reduction, recycling, and reuse. This regulatory push is encouraging local industries to replace solvent-based adhesives and coatings with waterborne UV alternatives.

The furniture and woodworking sector is a primary growth driver, with rising consumer demand for eco-friendly coatings. Waterborne adhesives are already dominant in Brazil due to their lower costs and user-friendly application, and their integration into UV-curable systems is expanding their market potential. With Brazil’s growing domestic market and government-backed sustainability initiatives, the country is expected to see rapid adoption of waterborne UV resins across multiple industrial sectors.

Waterborne UV Curable Resins Market Report Scope

Waterborne UV Curable Resins Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.1 Billion

|

|

Market Size (2034)

|

$32.4 Billion

|

|

Market Growth Rate

|

9.7%

|

|

Segments

|

By Chemistry Type (Waterborne UV Polyurethane Acrylates, Waterborne UV Epoxy Acrylates, Waterborne UV Polyester Acrylates, Waterborne UV Acrylics), By Formulation (Oligomers, Monomers, Photoinitiators, Additives), By Application (Coatings, Adhesives, Inks, 3D Printing, Other Applications), By End-Use Industry (Wood & Furniture, Paper & Packaging, Automotive & Transportation, Consumer Electronics, Construction, Industrial)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Allnex, BASF SE, Covestro AG, Arkema Group (Sartomer), DIC Corporation, DSM (part of Covestro), IGM Resins B.V., Mitsubishi Chemical Corporation, Wanhua Chemical Group Co., Ltd., Resonac Holdings Corporation, Eternal Materials Co., Ltd., Toagosei Co., Ltd., Miwon Specialty Chemical Co., Ltd., Rahn AG, Dymax Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Waterborne UV Curable Resins Market Segmentation

By Chemistry Type

- Waterborne UV Polyurethane Acrylates

- Waterborne UV Epoxy Acrylates

- Waterborne UV Polyester Acrylates

- Waterborne UV Acrylics

By Formulation

- Oligomers

- Monomers

- Photoinitiators

- Additives

By Application

- Coatings

- Adhesives

- Inks

- 3D Printing

- Other Applications

By End-Use Industry

- Wood & Furniture

- Paper & Packaging

- Automotive & Transportation

- Consumer Electronics

- Construction

- Industrial

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Waterborne UV Curable Resins Market

- Allnex

- BASF SE

- Covestro AG

- Arkema Group (Sartomer)

- DIC Corporation

- DSM (part of Covestro)

- IGM Resins B.V.

- Mitsubishi Chemical Corporation

- Wanhua Chemical Group Co., Ltd.

- Resonac Holdings Corporation

- Eternal Materials Co., Ltd.

- Toagosei Co., Ltd.

- Miwon Specialty Chemical Co., Ltd.

- Rahn AG

- Dymax Corporation

* List Not Exhaustive

Methodology

USDAnalytics applies a rigorous, data-driven research methodology to provide comprehensive insights into the global waterborne UV curable resins market. Our approach combines primary research, including interviews and surveys with key stakeholders such as resin manufacturers, coatings producers, electronics and furniture industry specialists, and regulatory bodies, with extensive secondary research from company reports, patent filings, scientific publications, and government regulations. The study evaluates market trends, including VOC reduction compliance, hybrid resin technologies, sustainable and bio-based raw materials, digital printing for electronics, and consumer-safe formulations. Market segmentation by chemistry type, formulation, application, and end-use industry is analyzed across regions such as North America, Europe, China, India, Japan, and Brazil. USDAnalytics also examines competitive landscapes, strategic collaborations, and technological innovations, providing actionable insights on growth drivers, operational efficiency, sustainability trends, and regulatory influences shaping the market. The methodology ensures a precise understanding of adoption patterns, performance requirements, and sustainability opportunities in the waterborne UV curable resins sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.