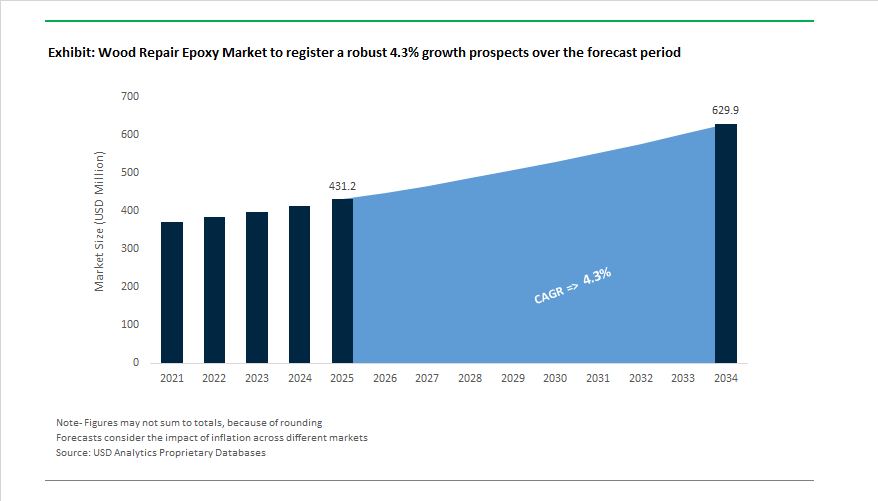

The Global Wood Repair Epoxy Market is projected to expand from USD 431.2 million in 2025 to USD 629.9 million by 2034, advancing at a CAGR of 4.3%, as epoxy repair systems move from niche maintenance products to strategic asset-life extension materials across residential renovation, heritage conservation, and commercial property maintenance. Market growth is not volume-driven; it is anchored in a structural shift toward repair-over-replacement economics, where owners and contractors increasingly prioritize lifecycle cost control, sustainability, and speed of intervention.

Epoxy-based wood repair systems are gaining preference because they consistently deliver 40%–70% cost savings compared with full wood replacement, while restoring structural integrity, load transfer, and surface finish. This value proposition is particularly compelling in historic buildings, bridges, windows, façades, and premium furniture, where material matching, regulatory constraints, and downtime costs limit replacement options. As a result, specifiers are treating wood repair epoxies less as fillers and more as structural reinforcement systems, selected based on compressive strength, adhesion to degraded substrates, and long-term dimensional stability.

A second structural driver is the reformulation of epoxy systems toward low-VOC and solvent-free chemistries, aligned with tightening indoor air quality standards and contractor safety requirements. Leading manufacturers have optimized two-component epoxies with high solids content, controlled exotherm, and extended working times, enabling deep penetration into rotten or delaminated wood without shrinkage or embrittlement. These systems are increasingly specified for interior restoration projects where odor, emissions, and curing predictability directly affect site productivity and occupant safety.

Performance differentiation is also accelerating at the premium end of the market. Demand is rising for UV-resistant, moisture-tolerant, and nanotechnology-enhanced epoxy formulations, particularly for exterior applications exposed to cyclic wetting, freeze–thaw, and solar radiation. Nanofillers and advanced resin architectures are being used to improve impact resistance, crack bridging, and long-term color stability, extending service life in window frames, decking, marine woodwork, and architectural elements. These innovations are allowing epoxy repairs to compete with replacement materials not only on cost, but on durability parity.

Professionals in the sector are recalibrating procurement and specification standards around formulation safety, field workability, and bond performance—especially as accelerated weathering tests confirm that modern wood epoxies retain over 95% of original strength after five years of exposure. Simultaneously, the push for fast-curing systems (gel times <60 minutes) is improving contractor productivity and DIY consumer satisfaction, cutting project turnaround times by up to 25%.

Key Industry Insights

- Repair vs. Replacement Efficiency: Structural epoxy repair delivers 40%–70% cost savings on restoration projects, optimizing lifecycle maintenance budgets.

- Superior Bond Strength: Modern two-part systems achieve >3,000 psi bond strength (ASTM D-905), surpassing natural wood integrity.

- Sustainable Formulation Shift: 50%+ of new launches feature low-VOC, solvent-free systems meeting stringent indoor air quality standards.

- Exterior Durability Proven: Less than 5% strength degradation in five-year simulated weathering tests validates long-term performance.

- Fast-Cure Productivity Gains: Quick-set epoxy formulations have reduced field installation time by 25%, particularly in high-volume restoration projects.

The wood repair epoxy segment is undergoing a measurable shift from generic filler products toward engineered restoration systems, shaped by sustainability requirements, infrastructure spending, and productivity demands from professional users. In October 2025, a major U.S. adhesives manufacturer expanded Midwest capacity for bio-based epoxy hardeners, directly addressing two structural pressures: supply-chain resilience and rising specification of eco-friendly polymer systems in professional wood restoration. This investment signals that bio-based content is becoming integral to mainstream wood repair epoxy portfolios where contractors and public agencies increasingly weigh environmental credentials alongside mechanical performance.

Performance differentiation is also expanding the application envelope of wood repair epoxies, particularly in exterior and infrastructure contexts. In August 2025, a European chemical group launched a UV-resistant epoxy putty engineered for exterior window frames and fascia, resolving a persistent failure mode—UV-induced degradation—in exposed repairs. Public-sector demand reinforces this performance-led trajectory. In June 2025, a specialty adhesives firm secured a multi-year European government contract for its structural wood epoxy system used in restoring historic wooden bridge components, underscoring epoxy’s growing role in heritage conservation and structural rehabilitation, where replacement is either impractical or prohibited. These developments highlight epoxy’s evolution from cosmetic repair material to load-bearing restoration solution in regulated environments.

Operational scalability and ease of use are becoming decisive adoption levers, particularly for professional contractors. In April 2025, Henkel Adhesive Technologies introduced a dual-cartridge dispensing system for its two-part wood epoxies, delivering consistent mix ratios and materially improving on-site productivity while reducing waste and rework. This focus on application control mirrors broader industry efforts to lower skill barriers and standardize outcomes in repair work. At the same time, global M&A activity is extending product reach into adjacent end uses: in February 2025, a South American chemical company acquired a regional specialist in high-viscosity epoxy fillers for marine repair, strengthening its position in boatbuilding and marine restoration—segments that demand moisture tolerance, gap-filling capability, and long-term durability.

Innovation momentum across Asia and North America reinforces the market’s technical direction. In December 2024, a Japanese materials science company published research integrating nanotechnology into wood epoxies, achieving approximately 15% improvement in impact resistance, a meaningful gain for high-stress repairs. Earlier, in September 2024, a North American resins producer invested USD 15 million to manufacture lightweight, non-sag epoxy resins optimized for vertical and overhead filling—addressing a critical pain point in structural and exterior repairs. Parallel to these professional and industrial advances, retail channels are also maturing: October 2024 saw a major DIY retailer partner with an epoxy supplier to host hands-on consumer workshops, signaling deeper engagement, education-driven demand, and continued expansion of the wood repair epoxy market beyond trade professionals.

Market Trend 1: Rising Adoption of Low-Viscosity, Deep-Penetration Epoxy Formulations for Historic Timber Restoration

The global restoration industry is experiencing a pronounced shift toward low-viscosity, deep-penetrating epoxy systems, primarily for use in historic timber frame stabilization, architectural wood preservation, and cultural heritage restoration. These specialized formulations are designed to permeate porous or decayed wooden structures, providing internal reinforcement while preserving original material authenticity—an essential requirement for heritage architects and conservation engineers.

Extensive research into wood consolidation mechanics demonstrates that epoxy penetration depth is inversely proportional to viscosity (as defined by Washburn’s equation). For effective consolidation of decayed oak or pine elements, epoxies must achieve sub-10 centipoise (cP) viscosity levels to wick into microscopic capillaries, ensuring durable internal bonding without excessive surface buildup. In practical applications, restorers have successfully injected low-viscosity epoxies into hollow or insect-damaged cores of heritage beams, sealing voids while maintaining visual integrity through protective clay or wax barriers.

From a validation standpoint, digital radiography and X-ray imaging are being increasingly used to verify epoxy penetration depth in restored timber. The non-destructive evaluation (NDE) technique provides measurable assurance of consolidant performance—critical for structural approval and long-term conservation documentation.

As the restoration market expands, deep-penetration epoxy systems are becoming indispensable for projects involving large-format structural elements like columns, trusses, and beams in 18th- and 19th-century buildings, where minimal intervention and material compatibility are paramount.

Market Trend 2: Growing Demand for UV-Stable, Color-Stable Epoxy Putties in Exterior and Marine Applications

The market is witnessing strong growth in UV-stable and color-retentive wood repair putties, especially for decking, façade restoration, and marine wood structures exposed to extreme outdoor environments. Traditional epoxy putties, although durable, suffer from UV-induced yellowing, microcracking, and surface degradation—issues that compromise both aesthetic appeal and performance over time.

Recent nanocomposite stabilization research has proven that the incorporation of halloysite nanotubes (HNTs) encapsulated with organic UV stabilizers or lignin-based nano-fillers significantly improves resistance to photooxidation. Experimental epoxy coatings enhanced with these additives demonstrated superior UV stability, with performance improvements extending service life by over 40% compared to unmodified resins.

In a landmark color stability study, newly developed low-yellowing epoxy putties recorded a ΔE*ab color change 20 times lower than conventional formulations after prolonged UV exposure—establishing a quantitative benchmark for aesthetic durability. These results position UV-stabilized epoxy systems as the preferred choice for high-end exterior applications, marine restorations, and artistic wood installations where visual uniformity and long-term performance are essential.

Additionally, the growing popularity of nano-reinforced epoxy systems aligns with consumer and commercial demand for low-maintenance exterior repair materials capable of withstanding humidity, saltwater corrosion, and continuous solar radiation without surface deterioration.

Market Opportunity 1: Development of Bio-Based Epoxy Hardeners from Lignin and Cashew Nut Shell Liquid (CNSL)

As sustainability becomes a central business priority, bio-based epoxy formulations derived from renewable feedstocks like lignin, vanillin, and cashew nut shell liquid (CNSL) represent one of the most lucrative innovation pathways in the wood repair epoxy industry. The transition away from petroleum-based systems not only reduces carbon footprint but also aligns with global green building certifications such as LEED and WELL.

A recent technological breakthrough by Sika AG confirmed that lignin-derived amine curing agents can match or even outperform traditional fossil-based epoxy hardeners in terms of mechanical strength, bond durability, and chemical resistance. The company’s patented bio-based amine formulation demonstrated equivalent structural performance, achieving high flexural strength and thermal stability while reducing lifecycle emissions.

Similarly, Cardolite Corporation’s CNSL-based curing agents (phenalkamines) have gained commercial traction due to their moisture tolerance, rapid curing, and low Global Warming Potential (GWP). These bio-based epoxies offer a particularly strong value proposition for marine wood repairs and outdoor restoration, where humidity resistance is essential.

Further, advanced R&D using vanillin and amino acid–derived epoxy curing agents has produced fully bio-based resins with glass transition temperatures above 141°C and Young’s modulus exceeding 1000 MPa, surpassing petroleum analogues in structural rigidity and longevity. The confirms the technical maturity of renewable epoxies for mainstream adoption in both architectural restoration and high-end woodworking markets.

Market Opportunity 2: Engineering of Reversible and Re-Treatable Epoxy Systems for Conservation-Grade Restoration

A major emerging opportunity lies in developing reversible or re-treatable epoxy systems designed for museum-grade and conservation-grade wood restoration. The modern conservation philosophy emphasizes reversibility and minimal intervention, creating demand for epoxy formulations that can be softened, dissolved, or safely removed without damaging original substrates.

Academic studies have reported a growing market need for epoxy-like polymers that retain high mechanical strength yet exhibit controlled solubility under specific solvents or chemical triggers. For example, experimental urethane-based resin systems demonstrated complete dissolution in acetone or ethanol within 12 hours, compared to the irreversible nature of standard epoxies—a critical feature for conservation laboratories managing priceless wooden artifacts.

Chemical engineering breakthroughs are also emerging through Schiff base modifications in bio-based epoxy hardeners, which introduce cleavable linkages allowing the material to be reprocessed or softened while retaining structural stability across cycles. The advancement not only supports future re-treatability but also enhances waste reduction and recyclability, aligning with circular economy principles in the adhesives sector.

As museums, cultural heritage institutes, and restoration firms adopt stricter conservation ethics, reversible epoxy systems are set to define a high-value specialty niche—bridging the gap between structural strength and ethical preservation.

Wood Repair Epoxy Market Share Insights, 2025-2034

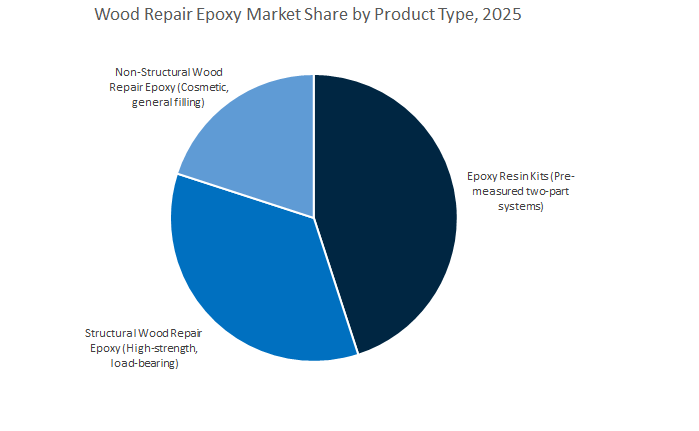

Market Share by Product Type

The epoxy resin kits segment holds the dominant position in the global wood repair epoxy industry, accounting for an estimated 44.2% of the projected 2025 market share. This dominance is attributed to the segment’s unmatched convenience, accessibility, and versatility, making it the top choice for both professionals and DIY users. These pre-measured two-part epoxy kits simplify the repair process by eliminating the guesswork involved in resin-to-hardener ratios, ensuring consistent results while minimizing waste. Their popularity is particularly strong in residential renovation, furniture restoration, and small-scale woodworking projects, where consumers prioritize ease of use and reliability. With the rising global trend in home improvement and DIY woodworking, epoxy kits have become a staple in retail and e-commerce channels. Additionally, manufacturers have been innovating through packaging (dual-syringe dispensers, pre-filled cartridges) and improved curing technologies, further expanding their reach into consumer and small trade markets.

The structural wood repair epoxy segment represents a high-value and performance-critical category, integral to load-bearing repairs and long-term restoration in construction, marine, and heavy timber applications. These epoxies offer exceptional compressive strength, adhesion, and durability, making them indispensable for repairing beams, columns, and joists subject to stress and environmental degradation. In structural preservation, especially in heritage buildings, bridges, and docks, epoxy formulations replace or reinforce deteriorated wood while maintaining mechanical integrity. Their role is particularly significant in North American and European markets, where restoration of historical wooden structures is regulated by strict engineering and preservation standards. Ongoing innovation in low-VOC, moisture-tolerant, and flexible epoxies continues to enhance adoption for modern and legacy applications alike, with demand being driven by construction rehabilitation and marine infrastructure maintenance.

Meanwhile, the non-structural wood repair epoxy segment serves a specialized but essential role in cosmetic and decorative restoration. These formulations—often modified with fillers like wood flour, silica, or microballoons—are optimized for sanding, carving, and finishing rather than bearing mechanical loads. They are widely used in furniture restoration, cabinetry repair, and aesthetic woodworking, where achieving a visually seamless and stainable finish is critical. The segment’s share is buoyed by the growing demand for custom furniture refinishing and antique restoration, particularly in the craftsman and hobbyist communities. Additionally, innovations such as tintable and clear epoxies have extended their utility into creative applications like river tables, inlays, and artistic woodcraft, further diversifying their use case.

Market Share by End-Use Industry

The residential repair and renovation segment leads the global wood repair epoxy market, commanding approximately 47.4% of the projected 2025 market share. This segment’s dominance stems from the explosion of DIY culture, aging housing stock, and the steady rise of home renovation projects across developed and emerging economies. Homeowners and contractors alike rely on wood repair epoxies for fixing rot, cracks, and moisture damage in decking, window frames, door sills, staircases, and outdoor furniture. The versatility of epoxies—able to bond, fill, and structurally restore deteriorated wood—has made them indispensable in both preventive maintenance and major repair work. Additionally, retail hardware chains and e-commerce platforms have made two-part epoxy kits widely accessible, expanding their usage beyond professionals to the general public. The increased focus on sustainable home restoration and material reuse has also amplified epoxy use in refurbishing existing wooden structures rather than full replacement, reinforcing this segment’s long-term growth.

The commercial and industrial construction segment represents the second-largest market, emphasizing structural-grade epoxy formulations for restoration and reinforcement in large-scale applications. Commercial buildings, warehouses, and industrial facilities often use high-strength, low-viscosity epoxies to stabilize wooden beams, trusses, and flooring subjected to heavy loads and harsh environments. These epoxies are also employed in timber bridge rehabilitation, dock and marina repair, and prefabricated wood module restoration, particularly in sectors prioritizing durability, safety, and reduced downtime. The segment’s demand is growing in regions investing in infrastructure rehabilitation and sustainable construction materials, particularly in Europe, where wood is being increasingly used as a renewable structural component.

The furniture and cabinetry repair segment holds a strong and steady market share, supported by the rising popularity of furniture restoration and upcycling trends. Both professional and DIY restorers rely on epoxy systems for tasks like filling voids, bonding split panels, and refinishing worn or damaged wood surfaces. These applications require epoxies with fine sandability, stain compatibility, and clarity, allowing craftsmen to achieve seamless aesthetic finishes that mimic natural wood grain. The continued expansion of the custom woodworking and interior design sectors, coupled with the proliferation of online restoration tutorials and social media-driven crafts, is sustaining growth in this segment.

The global wood repair epoxy market is characterized by a blend of specialized manufacturers, heritage-focused innovators, and industrial materials leaders. While West System and Abatron dominate in marine and heritage applications, H.B. Fuller and Sika (via Axson Technologies) leverage industrial chemistry scale for structural and commercial building applications. Meanwhile, PC Products and The Titebond Company remain go-to brands in professional contracting and DIY markets due to their ease-of-use, multi-substrate adhesion, and retail presence.

With over five decades of legacy, West System has become synonymous with marine-grade epoxy excellence. Its flagship 105 Resin/200-Series hardener system, adaptable with multiple fillers, provides unmatched flexibility for structural wood repair and moisture protection. The product’s customizable hardener speeds (e.g., 205 Fast, 206 Slow) empower professionals to adjust to varying environmental conditions. Field-proven manuals, certified test data, and high technical reliability make West System a preferred choice for boatbuilders, restoration experts, and outdoor furniture refinishers seeking long-term stability.

Abatron stands at the forefront of architectural conservation, with its LiquidWood and WoodEpox systems dominating the restoration sector for over 40 years. Known for shrink-free curing and seamless integration, WoodEpox is favored in historic building rehabilitation, offering machinability similar to natural wood—sawable, sandable, and paintable. The brand’s GREENGUARD Certified, low-VOC portfolio meets strict indoor air quality standards, making Abatron a trusted partner for heritage architects and contractors in both commercial and residential sectors.

Titebond, a name trusted in woodworking for over 80 years, continues to lead in PU and urethane-based wood adhesives. Its epoxy and hybrid systems cater to floor repair, cabinet assembly, and decorative woodworking, combining high initial tack with superior final bond strength. The brand’s presence in 60+ countries ensures compliance with international safety and performance regulations, reinforcing its reputation for professional-grade reliability. Its synergy of fast-set adhesives and repair kits supports both industrial manufacturers and on-site carpenters seeking consistent results.

Under Sika AG, Axson Technologies leverages a robust chemical engineering infrastructure to develop two-component structural epoxy systems for industrial repair and wood restoration. These formulations deliver high compressive strength, chemical resistance, and dimensional stability, suited for flooring, beams, and structural members in commercial construction. Axson’s integration with Sika’s R&D network ensures the use of advanced polymer technologies, while its focus on non-residential wood and hybrid repairs positions it as a global leader in industrial-grade epoxy innovation.

PC Products specializes in user-friendly epoxy putties and sealants optimized for both professional and residential applications. Its multi-substrate formulations bond effectively to wood, metal, and masonry, offering high durability in extreme weather conditions. Notably, PC’s non-sag, moldable putties are ideal for vertical and overhead repairs, eliminating the need for support structures. Simple 1:1 mix ratios streamline application, reducing on-site errors. This combination of performance and convenience has made PC Products a trusted brand in infrastructure maintenance, furniture repair, and general contracting.

Country Analysis – Global Structural Wood Repair Epoxy Industry Developments

China: Expanding Epoxy Resin Capacity and Infrastructure Demand Drive Structural Wood Repair Market Growth

China remains the largest producer and consumer of epoxy resins globally, positioning itself as a central hub for structural wood repair epoxy manufacturing and innovation. Rapid industrialization and infrastructure growth continue to amplify domestic consumption across sectors such as construction, shipbuilding, and furniture restoration, creating strong downstream demand for epoxy-based wood repair systems. In 2023, Dongying Yiruizheng New Material Technology Co., Ltd. announced an investment exceeding USD 100 million to expand its epoxy resin production capacity—critical for the supply of high-performance, moisture-resistant wood bonding and repair products.

China’s urbanization-led construction boom is fueling large-scale demand for epoxy adhesives used in structural wood rehabilitation, coatings, and restoration of load-bearing components. The State Council’s infrastructure programs emphasize material durability, accelerating the transition to polymer-modified epoxy systems for timber protection in bridges, public housing, and cultural heritage restoration. Additionally, the shipbuilding sector, a major consumer of marine-grade epoxy, continues to expand as the country strengthens its export shipyards, boosting demand for waterproof, UV-stable, and abrasion-resistant epoxies.

China’s leadership in epoxy resin feedstock manufacturing, coupled with domestic innovation in graphene- and nano-silica-enhanced repair epoxies, ensures a competitive cost structure for both domestic and international markets. Local R&D institutes are increasingly focused on low-VOC, sustainable epoxy technologies, aligning with national goals for green building materials.

India: Infrastructure Boom and Domestic Epoxy Resin Expansion Transforming the Wood Repair Industry

India’s structural wood repair epoxy market is witnessing rapid growth, driven by domestic capacity expansions, infrastructure development, and housing initiatives. The sector benefits from large-scale government-backed programs like Pradhan Mantri Awas Yojana (PMAY-U) and Smart Cities Mission, both promoting resource-efficient and durable construction technologies. The initiatives are boosting the demand for high-strength epoxy formulations used in repairing and reinforcing wooden beams, bridges, and roofing structures.

In 2024, Grasim Industries Limited (Aditya Birla Group) expanded its epoxy resin production facility in Gujarat, bringing total capacity to 246,000 tonnes per annum. The investment enhances India’s ability to locally supply epoxy-based wood repair systems, significantly reducing reliance on imports. Similarly, DCM Shriram’s USD 10 billion greenfield project aims to develop advanced material solutions, including liquid epoxy resins for structural adhesives and coatings.

The construction and renovation industries, spurred by rapid urbanization and rising disposable incomes, are major consumers of wood repair and protection systems. Epoxy resins are now widely adopted in flooring, heritage structure restoration, and furniture manufacturing, owing to their strength, fast-curing capability, and long-term resistance to heat and humidity. India’s ongoing infrastructure modernization and the growth of domestic specialty chemical production position it as a critical regional supplier of cost-effective, high-quality structural wood repair epoxies.

United States: Innovation and Marine Applications Strengthen Market Leadership

The U.S. structural wood repair epoxy industry continues to lead globally in innovation, sustainability, and performance-driven applications, particularly across the recreational boating, construction, and restoration sectors. The recreational boating industry, valued at over USD 41 billion, remains a primary consumer of marine-grade epoxy systems used for boat hull repair, wooden deck lamination, and corrosion protection. The niche drives continuous product development focused on UV resistance, flexibility, and clear-coat longevity.

In 2024, Westlake Corporation introduced a new epoxy resin series engineered to minimize yellowing and improve optical clarity, directly addressing consumer and contractor concerns in aesthetic wood restoration projects. Major market participants such as 3M, H.B. Fuller, and Sherwin-Williams continue to dominate through product diversification, expanding their portfolios in wood filler compounds, epoxy pastes, and moisture-curing structural adhesives.

The U.S. market is also experiencing a surge in eco-friendly, low-VOC epoxy solutions, supported by EPA and LEED-certified green building initiatives. The systems are now preferred for heritage timber restoration and structural wood reinforcement in both residential and commercial projects. The growing intersection between advanced polymer research and sustainability regulation cements the United States as a pioneer in next-generation epoxy resin formulations for the wood repair segment.

United Kingdom: Timber Roadmap and Circular Construction Goals Accelerate Epoxy Adoption

The United Kingdom’s structural wood repair epoxy market is evolving under the government’s Timber in Construction Roadmap 2025, which aims to expand the use of sustainable wood and promote circular economy principles. The policy measures are generating strong demand for high-performance structural epoxy systems that extend the life of existing wooden structures instead of replacing them, reducing embodied carbon in the built environment.

The Net Zero 2050 goal further emphasizes retrofit and repair over demolition, pushing the use of durable, low-waste epoxy bonding and injection systems in heritage buildings and timber bridges. Government-funded collaborations between industry and academia are exploring advanced epoxy repair technologies, including low-viscosity injection resins for deep wood penetration and bio-based resin systems with reduced environmental impact.

As the U.K. construction sector prioritizes retrofit efficiency and material preservation, epoxy adhesives are increasingly recognized as sustainable enablers of structural integrity in restoration projects. The initiatives are positioning the country as a leading European market for circular construction-grade epoxy adhesives and repair solutions.

Germany: Advanced Epoxy Formulation and Sustainability Regulations Propel Market Development

Germany’s structural wood repair epoxy market is closely tied to its advanced chemical manufacturing ecosystem and stringent environmental regulations. The country’s role as a European leader in automotive, wind energy, and composite material technology has facilitated breakthroughs in epoxy resin chemistry—advancements that are now being adapted to structural timber repair and conservation.

German chemical innovators are developing high-strength, thermally stable epoxy systems that enhance the durability and mechanical performance of structural wood components in mass timber and restoration projects. The country’s alignment with EU Green Deal policies and low-VOC directives is driving manufacturers to adopt solvent-free and bio-enhanced epoxy formulations. Global players such as Henkel and BASF continue to invest in R&D laboratories for resin optimization, with focus areas including recyclability, micro-crack resistance, and hybrid polyurethane-epoxy systems.

Germany’s integration of digital material design and precision dispensing technologies into the wood repair industry reflects its commitment to both quality assurance and sustainability. The innovation-driven approach ensures that Germany remains a benchmark for environmentally compliant, high-performance wood repair epoxy manufacturing in Europe.

Japan: Engineered Wood and Seismic-Resistant Epoxy Adhesive Innovation

Japan’s structural wood repair epoxy market is deeply connected to its precision engineering culture and focus on seismic-resilient construction materials. Leading chemical manufacturers such as AICA Kogyo Co., Ltd. and Kuraray Co., Ltd. continue to drive advancements in high-performance epoxy and polyurethane adhesives used in engineered wood applications like glulam beams and CLT panels.

Japanese R&D centers are heavily investing in epoxy formulations optimized for long-term adhesion and stress resistance in both structural repairs and earthquake-prone environments. The products are designed to withstand temperature variations, high humidity, and dynamic loading conditions, ensuring reliability in timber reinforcement and retrofitting applications. Additionally, innovations in low-odor and solvent-free epoxy systems align with Japan’s environmental and indoor air quality standards, reinforcing its leadership in precision-formulated structural repair adhesives.

Wood Repair Epoxy Market Report Scope

Wood Repair Epoxy Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$431.2 Million

|

|

Market Size (2034)

|

$629.9 Million

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Product Type (Structural, Non-Structural, Epoxy Kits), By Application Method (Injection, Trowelable, Pourable), By End-User (Residential, Commercial/Industrial, Marine, Infrastructure, Historic Preservation, Furniture), By Raw Material (BPA Based, Novolac Based, Specialty, Bio-Based

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, 3M Company, Arkema SA, Sika AG, The Sherwin-Williams Company, Huntsman Corporation, Dow Inc., AkzoNobel N.V., BASF SE, Westlake Corporation, Hexion, Franklin International, Jowat SE, Pidilite Industries Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

- Structural

- Non-Structural

- Epoxy Kits

By Application Method

- Injection

- Trowelable

- Pourable

By End-Use Industry

- Residential

- Commercial/Industrial

- Marine

- Infrastructure

- Historic Preservation

- Furniture

By Raw Material

- BPA Based

- Novolac Based

- Specialty

- Bio-Based

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Wood Repair Epoxy Market-

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- 3M Company

- Arkema SA

- Sika AG

- The Sherwin-Williams Company

- Huntsman Corporation

- Dow Inc.

- AkzoNobel N.V.

- BASF SE

- Westlake Corporation

- Hexion

- Franklin International

- Jowat SE

- Pidilite Industries Limited

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Wood Repair Epoxy Market across value creation levers from specification and compliance to application efficiency and lifecycle economics; our analysis reviews demand catalysts in restoration and renovation, compares chemistry and cure profiles for structural vs. cosmetic uses, and benchmarks durability under moisture/UV/thermal cycling. It highlights breakthroughs in low-VOC/solvent-free systems, deep-penetration consolidants, fast-cure field productivity, and UV-stable nano-modified putties, mapping how product innovation, channel reach, and pricing discipline shape margins through 2034—making this report an essential resource for procurement leaders, contractors, conservation engineers, and investors. With side-by-side technology scoring, risk dashboards, and adoption curves, the study distills what matters most for bid wins and warranty performance, etc……

Scope Highlights

Segmentation:

- By Product Type: Structural; Non-Structural; Epoxy Kits

- By Application Method: Injection; Trowelable; Pourable

- By End-Use Industry: Residential; Commercial/Industrial; Marine; Infrastructure; Historic Preservation; Furniture

- By Raw Material: BPA Based; Novolac Based; Specialty; Bio-Based

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast 2025–2034.

Companies (analysis/profiles of 15+): Henkel AG & Co. KGaA; H.B. Fuller Company; 3M Company; Arkema SA; Sika AG; The Sherwin-Williams Company; Huntsman Corporation; Dow Inc.; AkzoNobel N.V.; BASF SE; Westlake Corporation; Hexion; Franklin International; Jowat SE; Pidilite Industries Limited.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.