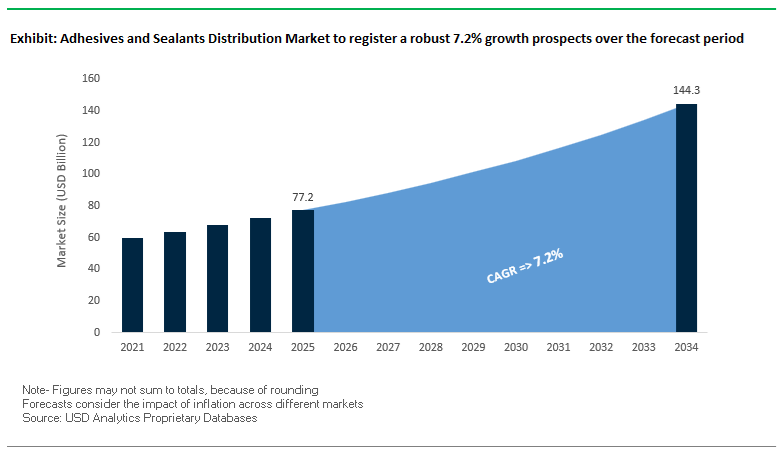

The global adhesives and sealants distribution market, projected to grow from USD 77.2 billion in 2025 to USD 144.3 billion by 2034 at a CAGR of 7.2%, is undergoing a structural shift from volume-based trading to technology-enabled, compliance-driven distribution. Growth is no longer defined solely by end-use demand in construction, packaging, and automotive, but by the ability of distributors to safely handle, technically support, and locally supply increasingly complex adhesive and sealant chemistries.

Manufacturers are accelerating the transition toward low-VOC, water-based, moisture-curing, and reactive adhesive systems, fundamentally reshaping distributor requirements around storage conditions, shelf-life management, technical training, and regulatory documentation. As a result, distributors are investing in climate-controlled warehousing, formulation-specific logistics, digital inventory monitoring, and application-level technical support, positioning themselves as operational extensions of manufacturers rather than passive resellers.

From a customer perspective, construction contractors, packaging converters, and automotive OEMs are demanding faster response times, just-in-time (JIT) delivery, and on-site technical assistance—particularly for structural adhesives, polyurethane and silicone sealants, and two-component systems that directly affect production uptime and product liability. This is pushing distributors to specialize by application segment, deepen supplier partnerships, and deploy field engineers alongside traditional sales teams.

Similarly, regionalization of supply chains—driven by geopolitical risk, transportation cost volatility, and sustainability mandates—is strengthening the role of local and regional distributors. Manufacturers are actively expanding regional production and distribution footprints to shorten lead times and ensure compliance with evolving environmental regulations, reinforcing distribution as a strategic control point in the adhesives and sealants value chain.

The adhesives and sealants distribution industry is undergoing a period of rapid transformation characterized by strategic acquisitions, regional manufacturing expansions, and sustainability-driven product launches. In mid-2025, Huntsman expanded its thermoplastic polyurethane (TPU) distribution with WOBATEK, strengthening supply chain access for performance elastomers used in coatings and automotive adhesives. This expansion underscores a trend of material-specific partnerships improving regional responsiveness and distributor specialization.

Also in mid-2025, Safic-Alcan acquired a regional distributor to deepen its Latin American presence, signaling consolidation among specialty chemical distributors to capture emerging market demand. Around the same time, Henkel announced the expansion of its flagship South Dakota facility, boosting North American distribution capacity for high-demand adhesive systems serving packaging and general assembly markets.

In October 2024, Sika AG acquired a mortar company in Denmark, strategically enhancing its Nordic sealant distribution footprint. Similarly, ATP Adhesives entered the North American market in mid-2025 by opening a manufacturing and distribution hub in South Carolina, increasing localized supply for pressure-sensitive adhesives (PSAs) and intensifying competition in specialty tape distribution.

The integration wave continued with Arkema’s Bostik division, which finalized the acquisition of Dow’s flexible packaging laminating adhesives business in December 2024. This merger significantly broadens Bostik’s laminating portfolio and requires optimization of its global adhesives distribution network. Earlier in January 2024, Sika launched new production plants in Singapore, Xi’an, and Suzhou, shortening supply chains for construction sealants and mortars in Asia-Pacific.

A major product development milestone came from H.B. Fuller, which plans to roll out its ECO2™-driven Millennium PG-1 EF adhesive in 2025 for the commercial roofing market. This innovation addresses low-GWP and low-VOC compliance, compelling distributors to manage environmentally sensitive inventory that aligns with the global decarbonization movement in the adhesives industry.

The adhesives and sealants distribution landscape is experiencing an aggressive wave of mergers, acquisitions, and vertical integration, as companies pivot toward technical service specialization and application expertise. The shift is redefining competitive positioning—distributors are expanding their role from material suppliers to technical collaborators capable of offering formulation consulting, training, and process optimization.

The M&A activity among manufacturers is setting a new benchmark for distributors. For instance, Arkema’s 2023 acquisition of Polytec PT—a high-performance adhesive supplier for battery and electronics markets—signals a clear strategic intent to control high-growth niches in e-mobility and advanced manufacturing. Distributors are under pressure to match the expertise through similar acquisitions or by expanding in-house technical service capabilities.

Sika AG’s 2023 acquisition of Chema in Peru exemplifies the move toward regional specialization and last-mile technical support. The acquisition not only strengthened Sika’s building finishing portfolio (including tile adhesives and grouts) but also enhanced its on-site service capabilities, such as technical training and product demonstrations. The trend is mirrored globally, as value-added distribution becomes a crucial differentiator in competitive and service-oriented markets.

At the industrial level, Brenntag’s acquisition of Aik Moh Group in Southeast Asia further demonstrates how distributors are diversifying portfolios to include custom blending, repackaging, and formulation support for industrial-grade adhesives and solvents. Such expansions signal a shift toward industrial consolidation, where expertise in application engineering and localized service networks are the key growth levers.

The strategic consolidation trend reflects a broader market realignment where distributors must provide holistic solutions—ranging from customized product delivery to technical field support—to remain integral to the adhesives and sealants value chain.

The shift toward digital-first distribution models is revolutionizing how adhesives and sealants are procured, managed, and delivered. Distributors are leveraging IoT-enabled logistics platforms, predictive analytics, and B2B e-commerce ecosystems to create a transparent, responsive, and resilient supply network.

Before 2020, digital maturity across the adhesives distribution sector was limited. However, the pandemic and subsequent supply chain disruptions accelerated the adoption of Big Data and automation technologies. Today, leading distributors use real-time inventory monitoring systems to support Vendor-Managed Inventory (VMI) programs, optimizing customer supply and reducing downtime.

Post-pandemic, manufacturers’ digital transformation efforts—such as real-time product performance dashboards and remote technical monitoring platforms—have redefined expectations. Distributors are developing online self-service portals, integrating digital order management, documentation repositories, and predictive restocking tools to meet customer demands for instant, transparent service.

These digital investments are particularly relevant for industrial clients requiring continuous production, such as automotive and electronics manufacturers. Predictive analytics helps distributors anticipate adhesive demand fluctuations and streamline just-in-time delivery—ensuring end-to-end supply chain resilience.

The emergence of e-commerce-driven B2B adhesive supply models is also reshaping customer engagement, offering direct technical downloads, live support, and performance data—all key to digital supply chain modernization and competitive differentiation.

Massive global infrastructure investment—particularly under initiatives such as the U.S. Infrastructure Investment and Jobs Act (IIJA)—is driving sustained demand for construction adhesives and high-performance sealants. The expansion is not just increasing product volumes; it is also reshaping the expectations of service delivery.

In 2024, infrastructure-related construction accounted for approximately 52% of global adhesives and sealants demand in the building sector, highlighting the pivotal role of distributors in managing supply and service. As megaprojects scale up, the need for on-site inventory management, technical training, and equipment rental services is becoming a core market differentiator.

Distributors who offer Vendor-Managed Inventory (VMI) programs and mobile storage solutions for adhesives and sealants are emerging as indispensable partners for large-scale construction contractors. In addition, growing emphasis on energy-efficient building systems—requiring advanced silicone and polyurethane sealants for airtightness and insulation—creates additional value-added opportunities.

Through on-site product demonstrations, technical workshops, and application troubleshooting, distributors are reinforcing their role as essential solution providers rather than passive suppliers. The convergence of infrastructure expansion, green construction mandates, and smart project management presents a long-term growth avenue for distributors that invest in field-level technical support and training infrastructure.

As sustainability and ESG compliance become non-negotiable priorities, distributors are uniquely positioned to develop circular economy services that manage the return, recycling, and safe disposal of adhesive containers and related waste. The shift represents a critical value-added service opportunity aligned with regulatory and corporate sustainability frameworks.

Globally, eco-friendly products represent nearly 38% of all new innovations within the adhesives and sealants sector, encompassing low-VOC, water-based, and bio-based formulations. Yet, sustainability no longer ends with the product—it extends to the entire lifecycle, including packaging and waste recovery. Distributors can leverage the shift by developing reverse logistics systems that facilitate container take-back programs, collection of unused adhesives, and compliant waste processing—helping customers meet environmental goals while minimizing operational waste.

Manufacturers like Henkel are already setting industry standards by embedding circular design principles into their products and packaging, ensuring compatibility with recycling systems and introducing debonding-on-demand solutions. To support these efforts, distributors are increasingly expected to execute local-level recycling and container recovery programs, thereby operationalizing the manufacturer’s sustainability commitments.

Adhesives and Sealants Distribution Market Share Insights, 2025-2034

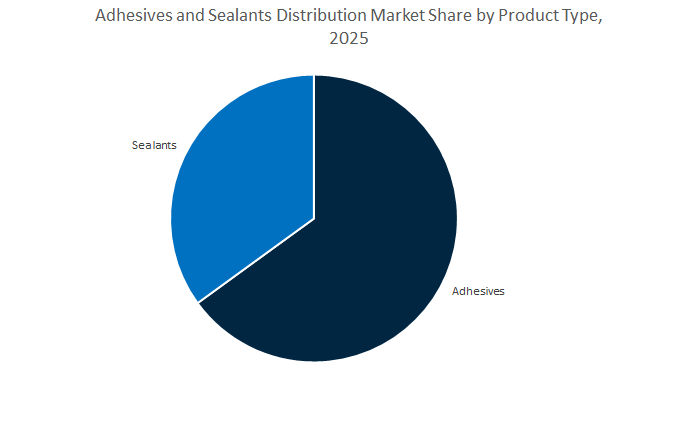

The adhesives segment dominates the global adhesives and sealants distribution industry, commanding an estimated 65% market share in 2025. This dominance is rooted in the breadth of adhesive formulations, wider industrial applicability, and higher average transaction value compared to standard sealants. Adhesives are distributed across diverse industrial verticals—including automotive assembly, aerospace, electronics, packaging, woodworking, and construction—each requiring specialized bonding solutions. Distributors thrive in this segment by offering technical expertise, inventory optimization, and custom blending services, which are critical for high-performance products such as epoxy resins, structural acrylics, polyurethane adhesives, and pressure-sensitive formulations. Furthermore, the shift toward lightweight materials, automation, and advanced composites has expanded the use of adhesives in place of mechanical fasteners, driving consistent demand from OEMs and MRO suppliers alike. As manufacturers increasingly prioritize sustainability and regulatory compliance, distributors are gaining new revenue streams through eco-friendly, low-VOC, and bio-based adhesives that align with green manufacturing initiatives. This ability to supply value-added, specialized, and compliant adhesive systems solidifies the segment’s leadership position in the global distribution ecosystem.

The sealants segment, holding the remaining 35% share, represents a stable and indispensable pillar of the distribution market. Sealants play a vital role in construction, transportation, electronics, and maintenance operations, providing environmental resistance, flexibility, and long-term durability in joint applications. The segment’s consistent performance is supported by steady replacement cycles and repair activities within construction and industrial maintenance sectors, where distributors ensure timely supply and substrate-specific product recommendations. Silicone, polyurethane, polysulfide, and hybrid MS polymer sealants dominate the mix, each catering to unique environmental and performance requirements. The increasing adoption of structural glazing, weatherproof façades, and fire-stop applications is fueling demand for high-performance specialty sealants, creating new profit margins for distributors who provide technical consultation and application training. While adhesives dominate by value and diversity, the sealants market provides volume stability and resilience, especially during cyclical fluctuations in industrial demand. For distributors, the sealants segment represents a steady income stream rooted in essential, recurring applications, balancing the volatility often associated with industrial adhesive demand.

The industrial segment forms the backbone of the global adhesives and sealants distribution market, accounting for approximately 70% of total share in 2025. This segment encompasses a vast and complex network of end-users spanning automotive, aerospace, packaging, electronics, energy, furniture, and general manufacturing industries. Industrial buyers typically demand bulk supply consistency, tailored formulations, and technical support, driving distributors to specialize in just-in-time (JIT) logistics, custom product kitting, and on-site service delivery. The rise of advanced materials and process automation has elevated the distributor’s role from that of a mere supplier to a strategic partner in process efficiency and materials innovation. For instance, in automotive and aerospace sectors, distributors support manufacturers with lightweight structural adhesives, high-temperature bonding systems, and hybrid sealing technologies designed to meet evolving regulatory and performance standards. In electronics, the shift toward miniaturized and thermally conductive bonding is further expanding opportunities for high-value distribution. As global manufacturing rebounds and infrastructure investments surge, industrial distribution networks are evolving to emphasize digital inventory control, predictive logistics, and compliance-driven sourcing, reinforcing this segment’s dominance and strategic value.

The consumer segment, representing about 30% of the total market, serves as the volume-driven and brand-dependent counterpart to the industrial market. Distributed primarily through retail chains, home improvement centers, and online marketplaces, this segment caters to DIY users, home renovators, and small workshops seeking accessible, pre-packaged adhesive and sealant products. Key growth drivers include housing market expansion, home renovation trends, and seasonal maintenance cycles, all of which directly influence consumption patterns. Distributors in this space rely heavily on brand partnerships, retail shelf management, and e-commerce logistics, ensuring consistent availability of popular consumer-grade adhesives—such as super glues, contact cements, and silicone sealants. However, the landscape is evolving with the rapid expansion of e-commerce and direct-to-consumer distribution models, which are bridging the gap between industrial-grade and consumer-grade supply chains. Professional tradespeople and small manufacturers purchase higher-performance adhesives through online platforms traditionally geared toward retail, creating a hybrid channel convergence. This transformation underscores how distributors must adapt by offering digital catalog integration, flexible packaging formats, and omnichannel fulfillment to remain competitive in the evolving adhesives and sealants distribution ecosystem.

The competitive environment in the adhesives and sealants distribution industry is defined by regional capacity expansion, sustainable chemistry portfolios, and digitized supply networks. Leading manufacturers such as Sika AG, H.B. Fuller, Bostik (Arkema Group), Wacker Chemie AG, Mapei S.p.A., and Ashland Inc. are investing heavily in localized production, in-country value creation, and low-carbon logistics to strengthen distribution efficiency and customer proximity.

Sika AG has achieved a remarkable distribution footprint, with over 100 production facilities across 101 countries as of 2024. Its localized “In-Country Value” model ensures supply reliability for adhesives and sealants in construction and industrial sectors. In June 2025, Sika invested in Giatec to advance digital concrete technology and supply chain efficiency, marking a step toward data-driven logistics. With the MBCC Group acquisition synergies expected to be fully realized in 2025, Sika’s integrated network is set to deliver optimized distribution routes and improved profitability. New plants in Kazakhstan and Morocco (2024) further strengthen its regional supply resilience and reduce delivery lead times.

H.B. Fuller Company maintains one of the most comprehensive adhesive distribution networks, operating over 60 manufacturing and technology centers worldwide. For fiscal 2025, it targets $300–$325 million in operating cash flow, dedicated to optimizing logistics and infrastructure. With $160 million in capital investments, Fuller is upgrading its manufacturing and supply chain footprint for long-term cost efficiency. Its launch of bio-based hot-melt adhesives (Swift®melt 1850) in 2025 supports distributors serving the sustainable packaging segment, while its global presence ensures rapid product availability across multiple high-growth end markets.

Bostik, a division of Arkema Group, is reinforcing its distribution strategy through sustainability and acquisitions. The company signed a 20-year renewable electricity agreement with EDF Renewables to cover 70% of its French operations from 2026—a critical sustainability credential for distributors. The September 2024 launch of Fast Glue Ultra+, containing 60% bio-based content, aligns Bostik’s network with eco-conscious construction customers. Acquisitions of Cromar (UK) and Arc Building Products (Ireland) in December 2024 consolidate its European reach, while partnerships with Dow and Nordson enable new recyclable packaging adhesive solutions tailored to FMCG industry needs.

Wacker Chemie AG increased its SILICONES division sales by 2% in 2024, driven by high-value specialty products demanding complex distribution management. With a global network of plants and distributors, Wacker ensures consistent supply for construction, automotive, and industrial customers requiring shelf-life-sensitive silicone materials. The company’s €665 million investment in 2024 boosts capacity across divisions, strengthening supply volume for distribution partners. Wacker’s ongoing efficiency programs enhance EBITDA performance, reflecting lean logistics and lower operational distribution costs across global markets.

Mapei S.p.A. closed 2024 with 106 production plants in 42 countries, ensuring short delivery lead times and localized support for professional users in the construction adhesives and sealants market. The company operates through 98 subsidiaries in 59 nations, underlining its decentralized distribution strength. With €213 million invested in fixed assets in 2024, Mapei expanded in Portugal, the UK, and Denmark, reinforcing its European network. Early 2025 expansions in Egypt and Sicily further strengthen supply coverage in Middle Eastern and Southern European infrastructure markets, reducing freight costs and improving responsiveness.

Ashland Inc. focuses on a high-value, low-volume distribution model that emphasizes specialty adhesives and performance polymers. Through 2025, the company optimized distribution overhead via restructuring and reduced SARD expenses, enhancing operational agility. It expanded its Natrosol™ cellulose derivative platform, improving sustainability and performance for adhesives used in coatings and construction. The Mullingar, Ireland facility expansion underscores Ashland’s ability to serve Life Sciences and medical adhesive markets, which require high regulatory compliance and temperature-controlled logistics—a strategic advantage in specialty chemical distribution.

China remains the largest and most dynamic market for adhesives and sealants distribution, underpinned by its extensive automotive, construction, and electronics manufacturing base. The launch of DuPont’s new automotive adhesive facility in Zhangjiagang (2023) marks a major milestone in strengthening the local supply chain for lightweight vehicle construction, directly serving domestic OEMs focused on EV platforms. The expansion reflects China’s strategic objective to reduce import reliance and enhance localized specialty materials production.

In May 2024, BASF SE’s supply agreement with Youyi Group, one of China’s leading adhesive tape manufacturers, further demonstrated the deepening of distribution partnerships between international chemical giants and domestic converters. Additionally, Sika AG’s acquisition of Crevo-Hengxin has expanded its footprint in silicone sealants and waterproofing systems, consolidating its reach across both construction and infrastructure markets.

The Chinese adhesives market is further driven by massive infrastructure and real estate investment programs, which are fueling large-scale consumption of construction adhesives and high-performance sealants. At the same time, the industry’s transition toward low-VOC and solvent-free adhesives is reshaping distribution portfolios as eco-compliance becomes a core purchasing criterion. China’s continued move toward domestically driven specialty material distribution networks, coupled with its industrial diversification, reinforces its status as the Asia-Pacific leader in adhesive and sealant distribution and manufacturing integration.

The United States adhesives and sealants distribution network is being redefined by strategic acquisitions, R&D investments, and evolving import regulations. In May 2024, H.B. Fuller’s acquisition of ND Industries Inc. significantly expanded its portfolio in specialty adhesives and fastener sealing solutions, enhancing distribution capabilities across aerospace, electronics, and industrial assembly sectors. The consolidation underscores a broader trend among U.S. distributors to broaden high-value specialty adhesive portfolios for advanced manufacturing.

However, U.S. housing and construction slowdowns reported by the Census Bureau in mid-2024 have slightly reduced DIY and general-purpose sealant volumes, shifting focus toward higher-margin commercial and industrial applications. The potential implementation of import tariffs has also prompted distributors to diversify sourcing channels away from traditional European and Asian suppliers.

Sustainability continues to shape the industry’s R&D and distribution outlook. U.S.-based suppliers are ramping up development of bio-based, solvent-free adhesives to meet corporate and environmental mandates. In parallel, 3M’s 2023 introduction of an extended-wear medical adhesive—capable of maintaining adhesion for up to 28 days—has boosted distribution in long-term medical device and wearable applications, a high-value growth segment.

Germany continues to serve as the nerve center of adhesives and sealants distribution across Europe, blending sustainability leadership with engineering precision and resilient logistics. Despite rising energy costs impacting the German chemical manufacturing sector, distributors are prioritizing cost efficiency, low-VOC product distribution, and sustainable formulation integration. Companies like Bodo Müller Chemie are expanding globally—opening new sales branches in Southeast Asia (Thailand and Vietnam) in 2024—to enhance access to emerging high-growth markets while optimizing distribution from Germany’s central European base.

The automotive and industrial sectors remain key distribution anchors, with strong demand for structural adhesives and lightweighting solutions from EV and aerospace manufacturers. In early 2024, Henkel’s acquisition of Seal for Life Group further reinforced its global MRO (Maintenance, Repair, and Overhaul) distribution portfolio, expanding access to industrial sealing and corrosion protection systems across Europe.

Meanwhile, the EU’s regulatory pressure under the Packaging and Packaging Waste Regulation (PPWR) continues to drive a market shift toward water-based, recyclable, and paper-based tapes and adhesives, influencing distribution strategies across the value chain. With Germany’s expertise in precision converting, digitalized logistics, and sustainable product transitions, it remains Europe’s benchmark market for advanced adhesive and sealant distribution systems.

India’s adhesives and sealants distribution ecosystem is witnessing rapid modernization, driven by infrastructure development, construction growth, and international strategic alliances. In May 2024, Dow’s partnership with Glass Wall Systems to supply DOWSIL façade sealants exemplified the country’s growing demand for high-performance construction sealants across premium real estate and architectural projects.

With government-backed programs like Smart Cities Mission and National Infrastructure Pipeline (NIP), adhesives distributors are expanding coverage in industrial, civil, and construction segments, supplying structural, waterproofing, and tile-bonding adhesives. Additionally, Pidilite Industries, India’s dominant domestic player, is broadening its industrial division portfolio—targeting adhesives for automotive, packaging, and construction applications—supported by one of the country’s strongest distribution networks.

The establishment of Petroleum, Chemical, and Petrochemical Investment Regions (PCPIRs) under the national policy is improving supply chain integration and logistics efficiency for global manufacturers setting up localized adhesive operations. With increasing foreign direct investment (FDI) from companies like Henkel and Dow, India’s adhesives distribution infrastructure is rapidly transforming into a hub for South Asia, catering to construction, packaging, and industrial growth sectors with localized, high-volume supply capabilities.

Brazil anchors the Latin American adhesives and sealants distribution market, benefiting from strong domestic demand across packaging, construction, and automotive manufacturing. With the regional market expanding steadily, Sika AG continues to reinforce its distribution portfolio through strategic investments in construction chemicals and building finishing materials, ensuring optimized coverage across key cities and industrial zones.

Growing infrastructure and automotive assembly projects are driving the distribution of hot-melt adhesives and polyurethane sealants, particularly for assembly lines, vehicle interiors, and structural bonding. Simultaneously, Brazil’s push toward sustainable construction practices is fueling interest in eco-friendly and low-solvent adhesive formulations, creating new market opportunities for global brands entering the distribution network.

The country’s robust food processing and agricultural packaging sectors are increasing the use of food-contact compliant adhesive systems, prompting distributors to strengthen specialized regulatory logistics for packaging adhesives. With its strategic location and expanding industrial base, Brazil remains the focal point for adhesive and sealant distribution in Latin America, supported by continuous investment in supply chain modernization and green product adoption.

Japan maintains a technologically advanced adhesives and sealants distribution model, catering to electronics, aerospace, and medical applications that demand high-purity, small-batch supply chains. The country’s focus on precision manufacturing and high-value materials drives continuous innovation in specialty adhesives such as epoxy, cyanoacrylate, and conductive films, distributed under tightly controlled conditions to maintain material integrity.

Companies like Nitto Denko Corporation are at the forefront of innovative tape technologies, including heat-peelable and security tapes, which require specialized distribution for technical and defense-grade applications. The aging population has also triggered a rising demand for medical-grade adhesive systems for wearable sensors, wound dressings, and disposable medical devices, prompting distributors to adopt pharmaceutical-grade logistics standards.

Japan’s adhesive distribution landscape is characterized by precision logistics, low-volume customization, and technical consultation-based sales models, ensuring compatibility with electronics, aerospace, and optical bonding solutions. The attributes position Japan as a global leader in precision adhesives distribution, setting benchmarks in material purity, application reliability, and high-end value chain integration.

Adhesives and Sealants Distribution Market Report Scope

Adhesives and Sealants Distribution Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$77.2 Billion

|

|

Market Size (2034)

|

$144.3 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Adhesives Product Type (Acrylic, Polyvinyl Acetate (PVA), Polyurethanes (PU), Styrenic Block Copolymers (SBC), Epoxy, Ethylene-Vinyl Acetate (EVA), Cyanoacrylate (CA), Pressure-Sensitive Adhesives (PSA), Hot-Melt Adhesives), By Adhesives Type (Silicone, Polyurethane (PU), Acrylic, Polysulfide, Butyl, Hybrid/SMP), By Adhesives Technology (Water-based, Solvent-based, Hot-Melt, Reactive, Natural/Bio-based), By Sealants Technology (Solvent-based, Water-based, Emulsion-based), By Application(Automotive & Transportation, Aerospace & Defense, Packaging, Construction, Woodworking & Joinery, Electrical & Electronics, MRO), By End-User Industry (Consumer), DIY, Footwear & Leather, Consumer Goods

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, H.B. Fuller Company, Arkema Group (Bostik), Dow Inc., Avery Dennison Corporation, Huntsman Corporation, Wacker Chemie AG, PPG Industries, Inc., RPM International Inc., Pidilite Industries, Master Builders Solutions (MBCC Group), DuPont de Nemours, Inc., Nitto Denko Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type (Adhesives)

- Acrylic

- Polyvinyl Acetate (PVA)

- Polyurethanes (PU)

- Styrenic Block Copolymers (SBC)

- Epoxy

- Ethylene-Vinyl Acetate (EVA)

- Cyanoacrylate (CA)

- Pressure-Sensitive Adhesives (PSA)

- Hot-Melt Adhesives

By Product Type (Sealants)

- Silicone

- Polyurethane (PU)

- Acrylic

- Polysulfide

- Butyl

- Hybrid/SMP

By Technology (Adhesives)

- Water-based

- Solvent-based

- Hot-Melt

- Reactive

- Natural/Bio-based

By Technology (Sealants)

- Solvent-based

- Water-based

- Emulsion-based

By End-User Industry (Industrial)

- Automotive & Transportation

- Aerospace & Defense

- Packaging

- Construction

- Woodworking & Joinery

- Electrical & Electronics

- MRO

By End-User Industry (Consumer)

- DIY

- Footwear & Leather

- Consumer Goods

By Distribution Channel

- Direct Sales

- Indirect Sales

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Major Manufacturers

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- H.B. Fuller Company

- Arkema Group (Bostik)

- Dow Inc.

- Avery Dennison Corporation

- Huntsman Corporation

- Wacker Chemie AG

- PPG Industries, Inc.

- RPM International Inc.

- Pidilite Industries

- Master Builders Solutions (MBCC Group)

- DuPont de Nemours, Inc.

- Nitto Denko Corporation

Major Distributors & Channel Partners

- Krayden Inc.

- Ellsworth Adhesives

- Biesterfeld AG

- Univar Solutions

- Azelis

- IMCD N.V.

- Brenntag

- Palmer Holland

- Nexeo Solutions

- Bodo Muller Chemie

- Stockmeier Group

- ChemPoint

*- List not Exhaustive

Research Coverage

This report investigates how the Adhesives and Sealants Distribution Market is being reshaped by sustainability mandates, e-commerce velocity, EV lightweighting, and digitized logistics; it consolidates breakthroughs in low-VOC portfolios, JIT models for EV lines, climate-controlled warehousing for water-based/2K systems, and value-added service integration into clear, decision-ready insights. Produced by USDAnalytics, the study’s analysis reviews demand pools, margin levers, and route-to-market shifts across industrial and consumer channels, and highlights the operational playbooks—VMI, reverse logistics, technical training, and application support—that de-risk supply while lifting service levels. By linking product compliance, network design, and working-capital turns to end-market growth, this report is an essential resource for executives, supply-chain leaders, commercial heads, and technical sales teams planning capacity, portfolio, and footprint moves through 2034.

Scope Highlights

- By Product Type (Adhesives): Acrylic; PVA; PU; SBC; Epoxy; EVA; Cyanoacrylate (CA); PSA; Hot-Melt

- By Product Type (Sealants): Silicone; PU; Acrylic; Polysulfide; Butyl; Hybrid/SMP.

- By Technology (Adhesives): Water-based; Solvent-based; Hot-Melt; Reactive; Natural/Bio-based.

- By Technology (Sealants): Solvent-based; Water-based; Emulsion-based.

- By End-User (Industrial): Automotive & Transportation; Aerospace & Defense; Packaging; Construction; Woodworking & Joinery; Electrical & Electronics; MRO.

- By End-User (Consumer): DIY; Footwear & Leather; Consumer Goods.

- By Distribution Channel: Direct Sales; Indirect Sales.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic & Forecast Window: 2021–2024 history and 2025–2034 forecasts.

- Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.