Beverage Cartoners Market Overview: Growth Anchored in Sustainability and Automation

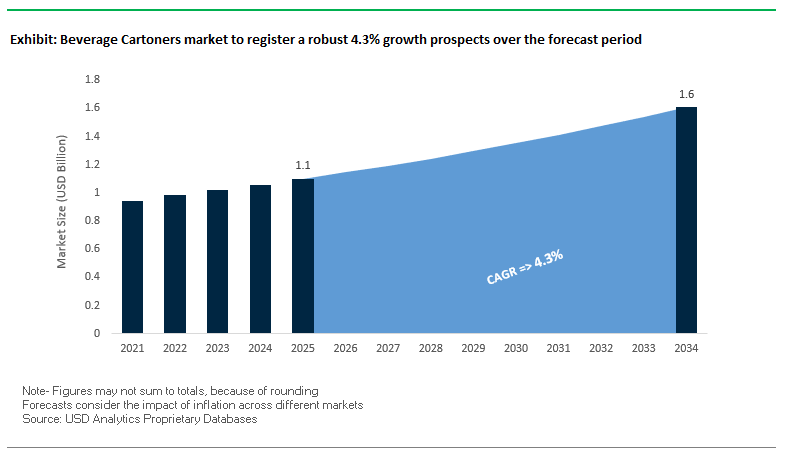

The global beverage cartoners market is projected to expand from USD 1.1 billion in 2025 to USD 1.6 billion by 2034, registering a steady CAGR of 4.3%. As consumer demand shifts towards renewable, safe, and convenient packaging, beverage cartoners have become a critical enabler for manufacturers seeking both efficiency and environmental compliance. For industry professionals, the central question is: how can beverage companies integrate automation and sustainable materials into their production lines while meeting the growing needs of e-commerce and consumer convenience?

Key Insights for Industry Stakeholders

- Dairy and Juice Remain Core Segments: Cartoners are widely adopted for dairy and juice packaging, ensuring longer shelf life and tamper-evident protection.

- E-commerce Fuels Transit-Ready Solutions: Direct-to-consumer beverage sales demand robust protective packaging, positioning carton-based solutions as critical for reducing breakage and enhancing consumer experience.

- Automation Drives Efficiency: A leading equipment manufacturer reported that fully automated cartoners represent a significant share of sales, underscoring the shift toward cost savings and high-speed production.

- Smaller Formats Gain Popularity: Rising demand for on-the-go and single-serve packs is pushing the need for flexible cartoning systems capable of handling multiple sizes and formats.

Market Analysis: Strategic Investments and Regulatory Tailwinds Reshape the Industry

The beverage cartoners industry has witnessed a wave of strategic expansions, sustainability-driven partnerships, and automation-focused innovations over the past year. In August 2025, Sidel opened a new Aseptic Training Center in Atlanta, USA, reflecting the rising demand for aseptic expertise in North and South America. In the same month, A-B-C Packaging Machine Corporation showcased its latest automated case and tray packers, strengthening its reputation as a leader in automation solutions.

Profitability improvements signal a robust industry outlook. In July 2025, Krones AG reported strong financial results driven by disciplined pricing and heightened demand for its equipment. In May 2025, Smurfit Kappa introduced a new “Bag-in-Box” packaging solution for wine, highlighting growing adoption of sustainable, large-format packaging compatible with modern cartoners. Similarly, the Amcor–Berry Global merger announced in April 2025, with combined revenues exceeding USD 24 billion, is expected to reshape the global packaging supply chain, with significant implications for beverage carton adoption.

Material innovation is also accelerating the industry’s transformation. In March 2025, a global paper manufacturer introduced paperboard with enhanced barrier properties, pushing the industry further towards recyclable and sustainable aseptic cartons. This momentum is supported by EU renewable packaging initiatives launched in February 2025, creating a regulatory environment favoring beverage cartoners. In January 2025, an industry report emphasized the rise of Industry 4.0 integration, such as predictive maintenance and real-time performance monitoring, underscoring the digitalization of cartoning operations. These developments collectively highlight how automation, sustainability regulations, and new materials are converging to elevate beverage cartoners’ role in the packaging ecosystem.

Emerging Trends and Opportunities Transforming the Beverage Cartoners Market

Accelerated Adoption of Robotic Automation and Integrated Line Solutions

The beverage cartoners market is undergoing a rapid technological shift as manufacturers increasingly adopt robotic automation and fully integrated line solutions. Robotic pick-and-place systems are now commonplace in high-speed production environments, offering precise, efficient loading while reducing human error. Collaborative robots (cobots) are also being deployed to handle repetitive and physically demanding tasks, freeing human operators for higher-value roles such as quality assurance and machine maintenance. This automation trend directly addresses one of the industry’s critical challenges labor shortages while simultaneously improving safety and lowering operational costs. Leading machinery providers such as Krones and WestRock are spearheading the movement toward smart integrated lines, linking upstream filling and downstream packaging into a single, data-rich ecosystem. These integrated lines allow for seamless product changeovers, improved traceability, and real-time performance monitoring, making them indispensable for manufacturers operating in a highly competitive, fast-paced beverage market.

Strategic Pivoting Towards Modular Systems for Plant-Based and Functional Beverages

The surge in plant-based milks, functional drinks, and cold-pressed juices is reshaping the design requirements of cartoning systems. These products demand flexibility, gentle handling, and batch efficiency, creating strong momentum for modular cartoning systems. Equipment is now being designed to handle multiple carton sizes and formats, ranging from small, single-serve protein shakes to large family-sized oat milk cartons. With premium beverages like kombucha or probiotic juices requiring careful handling, manufacturers are engineering gentle loading mechanisms and grippers to prevent damage and preserve product integrity. Moreover, as beverage companies launch more SKUs in shorter production cycles, average batch sizes are shrinking. Modular cartoning platforms with automated, rapid changeovers are proving vital in enabling cost-efficient small runs, helping brands balance variety and profitability. This strategic pivot ensures manufacturers can keep pace with consumer demand for innovation and health-oriented beverages, while maintaining operational efficiency.

Retrofitting and Upgrading Legacy Machinery with IoT and Data Capture Kits

A large proportion of the global cartoner installed base is aging yet still operational, creating a high-value retrofit market. By integrating IoT-enabled sensors and data-capture kits, these legacy machines can be transformed into smart, connected assets. Retrofitted equipment provides real-time visibility into key metrics such as uptime, output levels, and efficiency, empowering manufacturers to make data-driven improvements. Predictive maintenance is another major benefit: vibration and temperature sensors help anticipate mechanical issues before breakdowns occur, reducing downtime and boosting Overall Equipment Effectiveness (OEE). For equipment suppliers, retrofitting creates a lucrative aftermarket revenue stream, offering a more sustainable business model than solely relying on new machine sales. This trend is expected to redefine customer relationships, as OEMs provide continuous value through digital upgrades and service partnerships, bridging the gap between traditional cartoning and Industry 4.0 manufacturing.

Development of Cartoners Compatible with Fiber-Based Barrier Packaging

The global packaging industry’s shift away from plastic is opening significant opportunities for fiber-based carton solutions with advanced barrier properties. Regulations such as the EU’s Packaging and Packaging Waste Regulation (PPWR) are accelerating innovation in recyclable and compostable carton structures. These new materials, however, present challenges for conventional cartoning equipment, which was designed to handle laminated cartons with different stiffness and sealing requirements. As a result, machinery manufacturers are engineering specialized folding, cutting, and sealing mechanisms that ensure consistent integrity when processing fiber-based cartons. Industry collaboration is key to this opportunity: material innovators like Mondi and Graphic Packaging International are working directly with equipment manufacturers to optimize processing of these sustainable substrates at commercial scale. The development of fiber-compatible cartoners not only supports regulatory compliance but also enables beverage brands to strengthen their sustainability credentials while tapping into growing consumer demand for eco-friendly packaging.

Competitive Landscape: Global Leaders Driving Automation and Sustainable Packaging

The beverage cartoners market is competitive, with multinational corporations and specialized machinery providers advancing automation, Industry 4.0 capabilities, and sustainable solutions. The market is shaped by technological innovation, global service networks, and customer-centric strategies.

Sidel enhances aseptic expertise and full-line integration

Sidel, part of the Tetra Laval Group, offers advanced Cermex cartoning and case-packing solutions and is a leader in aseptic packaging lines for PET, cans, and glass. In August 2025, it opened its Aseptic Training Center in Atlanta, reinforcing its presence in the Americas. Its Cermex EvoPack platform is a benchmark in flexibility, capable of handling shaped containers with fast, repeatable changeovers. Sidel’s strength lies in full-line integration, providing turnkey solutions from blowing and filling to cartoning and palletizing, supported by a global service footprint.

Krones AG leverages profitability and lifecycle service leadership

Krones AG is a leading global supplier of filling and packaging lines, with a strong cartoning and case-packing portfolio. In July 2025, the company reported a sharp rise in profitability, reflecting strong market demand and disciplined price strategies. Its Lifecycle Service and Digital Services portfolio allow beverage manufacturers to reduce costs and optimize efficiency. By focusing on resource-efficient, high-performance machinery, Krones maintains its position as a sustainable value provider in the global beverage cartoners market.

A-B-C Packaging Machine Corporation pioneers automation in end-of-line packaging

A-B-C Packaging Machine Corporation specializes in end-of-line solutions, including case and tray packers for cartons and other formats. In August 2025, the company presented its latest automation-focused machines, including robotic packers and decasers, designed to maximize efficiency and reduce manual intervention. Known for rugged and user-friendly machinery, A-B-C has built a reputation for equipment longevity and low ownership costs. Its strategic focus on modularity and operational simplicity resonates with customers seeking flexibility and efficiency in cartoning operations.

Cermex drives innovation with patented end-of-line solutions

Cermex, part of the Sidel Group, provides case packers, shrink-wrappers, and palletizers, making it a trusted specialist in secondary packaging. It invests around 10% of turnover in R&D annually, generating 15–20 patents per year. Known for its ability to handle unstable or shaped containers, Cermex ensures flexibility in packaging solutions. Its integration with Sidel enables seamless full-line delivery, reinforcing its reputation for innovation and efficiency in beverage cartoning systems.

Serac Group strengthens its position in Latin America with innovative ESL packaging

Serac Group, a key provider of filling, capping, and blow molding machinery, is expanding its beverage packaging portfolio. In May 2025, it appointed a new General Manager for Serac MidAm to lead expansion across Mexico and Latin America. Its BluStream cap decontamination module is a recognized innovation in aseptic and Extended Shelf Life (ESL) packaging. With a strong focus on circular economy-driven solutions, Serac is investing in PET cups and yogurt packaging lines, aligning its growth strategy with sustainability and market diversification.

Beverage Cartoners Market Share Insights

Market Share by Packaging Type in the Beverage Cartoners Industry

Horizontal end-load cartoners lead the beverage cartoners market with a 45% share in 2025, reflecting their reputation as the workhorse of stability and versatility. This format is especially critical for packaging fragile containers such as glass bottles, as it offers superior structural integrity and secure tray-style bases for heavy multi-packs. Its dominance is tied to the ability to deliver high-speed operations while ensuring product safety during transit, making it the preferred choice for both dairy and premium beverage applications. Wraparound cartoners hold 30% of the market, emerging as the efficiency and economy champions of the industry. By forming a carton blank around clustered products instead of relying on pre-formed cartons, wraparound systems minimize paperboard use while maximizing throughput, making them the most cost-effective solution for high-volume canned beverage production. Top-load cartoners, though a smaller niche, play a vital role in handling delicate or irregularly shaped beverage containers, such as wine bottles or specialty packs. Their share is driven by applications that demand careful placement, where horizontal loading is impractical, albeit at the expense of speed. Other carton formats represent specialized and custom-designed solutions, such as four-packs, carry-handle cartons, and hybrid tray-overwrap systems, addressing unique branding and ergonomic needs in markets where differentiation and consumer convenience are key purchase drivers.

Market Share by End-Use Industry in the Beverage Cartoners Industry

Dairy beverages account for 35% of the beverage cartoners market in 2025, making them the single largest end-use segment. Multi-packaging of gallon and half-gallon milk containers heavily relies on end-load cartoners, highlighting their importance in ensuring both efficiency and stability for bulk dairy distribution. Fruit juices and nectars follow closely with 30% of the market, together forming the traditional backbone of the beverage cartoning industry. These products typically use gable-top or brick-style primary cartons that are easily grouped into stable secondary packs, ensuring cost-effective logistics. Soft drinks, while still a significant segment, face a shifting landscape. With carbonated soft drinks (CSDs) and still beverages increasingly packaged in cans, shrink film has overtaken cartoners as the dominant secondary packaging method due to its lower cost and lighter material weight. However, cartoners remain critical for premium glass bottle formats and in regulatory environments that restrict single-use plastics. Other beverages represent the fastest-growing category, encompassing plant-based milks, RTD coffee and tea, and functional wellness drinks. These products often prioritize sustainable and natural branding, making carton-based secondary packaging the logical choice to reinforce eco-friendly narratives. The momentum in this segment is drawing new investments in cartoning machinery tailored for flexible production and high product diversity, positioning it as the growth engine of the industry.

United States: Sustainability, Automation, and E-Commerce Fuel Beverage Cartoners Market Growth

The United States is emerging as one of the most influential markets for beverage cartoners, driven by the rising demand for sustainable and aseptic packaging. With consumers increasingly opting for plant-based milks, juices, and functional health beverages, the adoption of aseptic and extended shelf life (ESL) packaging is accelerating. Beverage manufacturers are turning to paper-based cartons to meet this demand while addressing growing concerns over preservatives and food safety. At the same time, legislative measures across states to reduce plastic waste are nudging beverage brands toward eco-friendly carton-based packaging solutions.

Beyond sustainability, U.S. companies are embracing automation and IoT integration in beverage cartoning machinery. Packaging lines are increasingly equipped with smart sensors, predictive maintenance systems, and AI-driven quality control to minimize downtime and improve throughput. The expansion of e-commerce and direct-to-consumer (DTC) channels is also reshaping requirements, with cartoners now being designed to create tamper-evident, durable, and easy-to-open packaging for online distribution. Furthermore, the U.S. market is witnessing demand for machinery that supports diverse formats from single-serve packs to family-sized cartons enabling beverage brands and co-packers to remain competitive in a fragmented consumer market.

Germany: EU Packaging Regulations and Machinery Innovation Drive Market Leadership

Germany plays a pivotal role in the global beverage cartoners market, powered by its strict alignment with EU packaging regulations and its strong machinery manufacturing base. The Packaging and Packaging Waste Regulation (PPWR) is significantly influencing the country’s beverage packaging landscape by enforcing recyclability standards, minimum recycled content, and waste reduction targets. As a result, beverage producers in Germany are rapidly adopting paper-based cartons to comply with these requirements while aligning with consumer demand for environmentally responsible packaging.

Germany also stands out as a hub for advanced packaging machinery innovation. Local manufacturers are heavily investing in R&D to produce high-speed, precision-driven cartoners capable of handling paper-based substrates while maintaining efficiency and sustainability. The country’s established circular economy practices and robust recycling infrastructure further strengthen the adoption of mono-material and easily separable beverage cartons. With strong consumption of dairy and plant-based drinks, Germany’s beverage cartoners market continues to grow steadily, supported by both regulatory alignment and consumer demand for greener packaging alternatives.

China: Urbanization and Technological Adoption Transform Beverage Cartoners Market

China’s beverage cartoners market is undergoing rapid expansion, driven by urbanization, rising disposable incomes, and changing lifestyles that favor packaged beverages. The demand for juices, milk, and ready-to-drink teas has surged, creating opportunities for investment in large-scale, high-speed beverage cartoning lines. This rapid consumption growth is placing immense pressure on manufacturers to scale production capacity and efficiency.

Technology adoption is another defining factor in China’s market development. Packaging lines are increasingly automated with robotics, smart systems, and AI-based controls to manage high-volume output while reducing operational costs. The demand for aseptic packaging is particularly strong, as consumers prioritize safety and hygiene. Aseptic beverage cartoners are now indispensable for extending shelf life without refrigeration, especially in the rapidly growing health beverage segment. Additionally, government-backed initiatives to modernize the manufacturing sector are pushing beverage companies to upgrade their operations with advanced machinery and quality assurance technologies, positioning China as a fast-growing hub for modern beverage packaging.

India: Rising Beverage Consumption and Sustainability Fuel Cartoners Adoption

India is witnessing significant momentum in the beverage cartoners market, largely fueled by its young, health-conscious population and growing demand for packaged juices, flavored milks, and nutritional drinks. With rising disposable incomes and increasing urbanization, packaged beverages are becoming a mainstream choice, opening vast opportunities for both domestic and international beverage companies. This demand surge has encouraged large investments in new production facilities and expansion of packaging capacity, driving the uptake of cost-efficient and high-volume beverage cartoners.

Sustainability is also a central theme in India’s beverage packaging transformation. With government-led initiatives to curb plastic waste and strengthen recycling practices, beverage producers are under pressure to adopt renewable and recyclable alternatives. Beverage cartons offer a compelling solution by combining product safety with eco-friendly attributes, aligning with both regulatory priorities and consumer values. These factors are cementing India’s position as one of the most promising markets for beverage cartoner machinery in the Asia-Pacific region.

Brazil: Hot Climate and Aseptic Packaging Needs Accelerate Beverage Cartoners Demand

Brazil is rapidly embracing beverage cartoners as the packaging of choice, particularly for dairy products and fruit juices that require extended shelf life in a hot and humid climate. The demand for aseptic packaging is rising sharply as it ensures food safety, maintains product freshness, and minimizes the need for preservatives. This shift is reshaping beverage production strategies and boosting investments in modern cartoning solutions tailored for aseptic processing.

In addition to safety, the Brazilian beverage industry is heavily focused on efficiency and cost-effectiveness. Manufacturers are increasingly adopting high-speed beverage cartoners capable of handling mass production with minimal downtime. This focus is essential in a price-sensitive market where operational reliability and scalability directly impact profitability. The growing consumer preference for packaged beverages, coupled with the need for affordable and efficient machinery, is positioning Brazil as a key emerging market for beverage cartoner adoption in Latin America.

Beverage Cartoners Market Report Scope

Beverage Cartoners market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.1 Billion

|

|

Market Size (2034)

|

$1.6 Billion

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Packaging Type (Horizontal End Side-Load Carton, Top-Load Carton, Wraparound Carton, Other Carton Formats), By Mode of Operation (Automatic, Semi-Automatic), By End-Use Industry (Dairy Beverages, Fruit Juices, Soft Drinks, Other Beverages)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Syntegon Technology GmbH, Tetra Pak, Krones AG, IMA Group, SIG Combibloc, Sidel S.A., Coesia S.p.A., Mpac Group, ADCO Manufacturing, The Schubert Group, Körber AG (via its subsidiary Körber Process Solutions), AR Packaging, Elopak, Mondi plc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Beverage Cartoners Market Segmentation

By Packaging Type

- Horizontal End Side-Load Carton

- Top-Load Carton

- Wraparound Carton

- Other Carton Formats

By Mode of Operation

By End-Use Industry

- Dairy Beverages

- Fruit Juices

- Soft Drinks

- Other Beverages

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Beverage Cartoners Market

- Syntegon Technology GmbH

- Tetra Pak

- Krones AG

- IMA Group

- SIG Combibloc

- Sidel S.A.

- Coesia S.p.A.

- Mpac Group

- ADCO Manufacturing

- The Schubert Group

- Körber AG (via its subsidiary Körber Process Solutions)

- AR Packaging

- Elopak

- Mondi plc

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global beverage cartoners market, highlighting critical breakthroughs, technological innovations, and emerging trends that are shaping industry growth. The analysis reviews the impact of automation, Industry 4.0 integration, and sustainability-driven packaging solutions on market dynamics, with particular focus on modular systems, aseptic packaging, and fiber-based carton compatibility. The report also highlights strategic partnerships, mergers, and capital investments across leading companies, offering a comprehensive overview of market competitiveness and operational excellence. In addition, the study examines how evolving consumer preferences, regulatory initiatives, and e-commerce growth are driving demand for flexible, transit-ready cartoning solutions. This report is an essential resource for industry professionals seeking insights into production efficiency, material innovation, and emerging opportunities in both developed and emerging markets. With detailed evaluations spanning historical data (2021–2024) and forecast projections (2025–2034), it provides a forward-looking perspective essential for decision-making, investment planning, and strategic positioning in the beverage packaging ecosystem.

Scope Highlights:

- Segmentation: By Packaging Type (Horizontal End Side-Load Carton, Top-Load Carton, Wraparound Carton, Other Carton Formats), By Mode of Operation (Automatic, Semi-Automatic), By End-Use Industry (Dairy Beverages, Fruit Juices, Soft Drinks, Other Beverages)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historic and Forecast Data: Historic data from 2021 to 2024; forecast from 2025 to 2034

- Companies Covered: Analysis/profiles of 15+ leading companies, including Syntegon Technology GmbH, Tetra Pak, Krones AG, IMA Group, SIG Combibloc, Sidel S.A., Coesia S.p.A., Mpac Group, ADCO Manufacturing, The Schubert Group, Körber AG, AR Packaging, Elopak, and Mondi plc

Methodology

The beverage cartoners market analysis employs a robust methodology combining primary and secondary research, quantitative modeling, and trend triangulation to deliver accurate, industry-focused insights. Primary research includes interviews with key stakeholders, machinery manufacturers, beverage producers, and packaging experts to capture operational nuances, investment patterns, and technology adoption. Secondary research draws from company filings, press releases, patent data, industry journals, and regional regulatory documents to validate market assumptions and ensure reliability. Historical market trends (2021–2024) were statistically analyzed and extrapolated to generate forward-looking forecasts (2025–2034), incorporating factors such as material innovation, automation adoption, and regional growth variations. Market sizing, share analysis, and segmentation were developed using a combination of bottom-up and top-down approaches, with cross-verification to ensure accuracy. USDAnalytics integrates sustainability metrics, Industry 4.0 readiness, and emerging consumer behavior trends into the methodology to provide actionable intelligence for both strategic and operational decision-making.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.