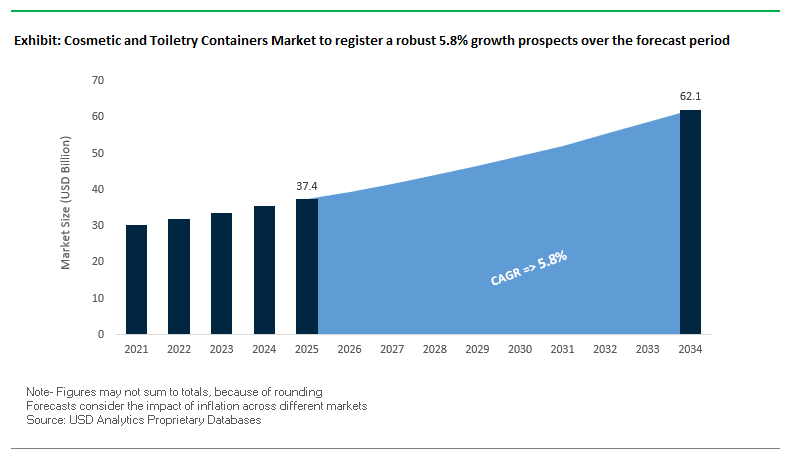

Market Overview: Global Cosmetic and Toiletry Containers Market Valued at $37.4 Billion in 2025

The Global Cosmetic and Toiletry Containers Market is valued at USD 37.4 billion in 2025 and projected to reach USD 62.1 billion by 2034, growing at a CAGR of 5.8%. This acceleration reflects not only rising consumption of personal care products but also a structural shift in packaging strategies influenced by sustainability mandates, consumer expectations, and digital brand engagement.

For professionals navigating this space, containers have become a strategic pillar of brand positioning. Packaging choices are now directly tied to regulatory compliance, consumer loyalty, and profitability. Millennials and Gen Z consumers are willing to pay up to 20% more for products with sustainable containers, shifting packaging innovation from cost optimization to value creation. Plastic remains dominant, particularly PET and HDPE, due to flexibility and lightweight design, while glass continues to command the premium segment for its recyclability, product protection, and luxury appeal.

The market is also embracing refillable models Kiehl’s refill stations, for instance, are estimated to reduce plastic use by around 80%, underscoring the circular economy’s commercial viability. Simultaneously, brands are leveraging digital decoration, unique finishes, and immersive unboxing experiences to differentiate in a saturated market.

Key Insights for Industry Professionals:

- MV (2025): USD 37.4 Billion | MV (2034): USD 62.1 Billion | CAGR: 5.8%

- Consumers willing to pay premiums for eco-friendly packaging (up to +20%).

- PET and HDPE remain preferred for versatility; glass dominates luxury positioning.

- Refillery and reuse systems rapidly scaling in skincare and haircare.

- Decorative packaging and unboxing experience driving brand equity.

- Regulatory and ESG commitments influencing material sourcing and investments.

Market Analysis: Recent Strategic Developments Shaping Cosmetic and Toiletry Containers

The cosmetic and toiletry containers industry in 2025 has been defined by a series of strategic moves, acquisitions, and recognitions that highlight its rapid evolution toward sustainability and market expansion.

In August 2025, Albéa made a decisive acquisition of Amfora Packaging in Colombia and Peru, securing access to one of the fastest-growing regional markets. That same month, Silgan’s Q2 2025 results reaffirmed its growth trajectory, led by robust demand for dispensing systems and specialty closures. Also in August, Huhtamaki earned its fifth consecutive EcoVadis Gold Medal, reinforcing its global sustainability leadership.

By June 2025, Aptar Beauty expanded ISTA-6 capabilities in Europe, enhancing support for clients facing e-commerce durability and integrity requirements. One month earlier, in May 2025, Aptar was recognized as one of the World’s Most Sustainable Companies by TIME, an accolade underscoring its role in reshaping eco-friendly product portfolios.

Strategic alliances were also critical: in March 2025, Constantia Flexibles and Aluflexpack AG joined forces to advance premium flexible packaging, a move expected to accelerate innovation pipelines. Earlier in February 2025, Albéa introduced EcoTop lightweight caps, reducing material usage by up to 75%, demonstrating the commercial viability of lightweighting strategies. In January 2025, Constantia Flexibles secured two WorldStar Global Packaging Awards, further consolidating its reputation for sustainability-focused product design.

Transformative Trends and Lucrative Opportunities in Cosmetic and Toiletry Containers Packaging

Accelerated Regulatory Mandates for Post-Consumer Recycled (PCR) Content

Governments in key markets are transitioning PCR adoption from voluntary sustainability efforts to binding regulatory requirements, fundamentally reshaping material sourcing strategies for cosmetic and toiletry containers. Washington State mandates a phased increase in PCR content from 15% by 2028 to 50% by 2036 providing a long-term compliance roadmap. Similarly, California’s Plastic Pollution Prevention and Packaging Producer Responsibility Act (SB 54) requires all single-use plastic packaging to be recyclable or compostable by 2032, creating significant pull for recycled materials. Brands like PepsiCo are aligning corporate ESG targets with these legislative frameworks, targeting 40% or higher recycled content in packaging by 2035. Enforcement is already in action, with fines totaling over $277,000 levied against 23 producers in Washington, emphasizing the financial consequences of non-compliance and driving guaranteed demand for high-quality PCR resin.

Strategic Pivot Towards Refillable and Reuse-Based Business Models

Leading cosmetic brands are transforming single-use containers into durable, multi-use packaging systems, converting packaging from a disposable commodity into a core brand asset. L’Oréal has expanded its refillable product offerings 17-fold between 2019 and 2024, reducing plastic use by up to 60% in refillable pouches for haircare products. Luxury brands such as Kjaer Weis reinforce premium brand identity through durable zamac compacts designed for repeated refills. Retail programs like Lush Cosmetics’ “Bring It Back” initiative enable consumers to return empty packaging, creating a closed-loop recycling system incentivized by rewards. Fenty Beauty’s refillable foundations illustrate how reusable containers foster deeper consumer engagement and long-term loyalty while contributing to sustainability objectives.

Development of High-Barrier, Monomaterial Structures for Recyclability

There is a critical opportunity to innovate containers that provide high-performance protection for sensitive cosmetic formulations while remaining fully recyclable. SML’s MDO-PE barrier films, incorporating thin EVOH layers, deliver oxygen and moisture protection within a monomaterial structure. Mondi Group’s PE-based mono-material StandUpPouch offers scalable, high-barrier solutions directly applicable to cosmetic and toiletry containers. Collaborations between ExxonMobil, Henkel, and Siegwerk have resulted in recyclable PE pouches with delamination capabilities to yield high-quality recyclate. Taghleef Industries’ EXTENDO® PP film enables fully recyclable, high-barrier containers compatible with existing PP recycling streams. This transition from multi-material to monomaterial packaging represents a major growth avenue for suppliers focused on sustainable and high-performance container solutions.

Integration of Digital Technologies for Authentication and Circularity

Digital technologies are emerging as a key value-add for cosmetic and toiletry packaging, enabling anti-counterfeiting, supply chain transparency, and consumer engagement. NFC chips embedded in luxury containers allow consumers to instantly verify authenticity, protecting brands from counterfeit losses. RFID-enabled containers provide real-time inventory tracking and digital audit trails, helping brands detect diversion and optimize logistics. Compliance with the EU Eco-design for Sustainable Products Regulation (ESPR) encourages the adoption of Digital Product Passports (DPPs) via QR codes, offering consumers detailed insights into product composition, recyclability, and durability. Beyond compliance, brands leverage QR codes for direct-to-consumer engagement, providing tutorials, product information, and interactive experiences that transform containers into digital platforms for building loyalty and driving brand value.

Competitive Landscape: Key Players Redefining Cosmetic and Toiletry Containers

The Global Cosmetic and Toiletry Containers Market is consolidated around a handful of companies investing in sustainability, technological innovation, and regional expansion. Each is adapting its strategy to meet consumer preferences and regulatory pressures while defending its market share.

Albéa Group: Scaling with Latin American Acquisition

Albéa remains a dominant player in tubes, jars, and dispensing systems, producing 8 billion tubes annually. Its August 2025 acquisition of Amfora Packaging bolstered its Latin American presence. Innovation is visible in products like the EcoFusion Top tube, which integrates head and cap to cut plastic use. With 23 industrial sites in 14 countries, Albéa combines global scale with regional integration, a competitive advantage for multinational beauty brands.

AptarGroup, Inc.: Driving Mono-Material Dispensing Innovation

Aptar leverages expertise in pumps, sprayers, and dispensing closures, with a strategic focus on reducing, reusing, and recycling. Its Future Made Better program drives the transition to all-plastic and mono-material designs. In 2025, Aptar advanced its ISTA-6 testing capacity in Europe, aligning with e-commerce durability standards. Its broad applications span fragrance, skincare, haircare, and home care, positioning it as a critical supplier across verticals.

Silgan Holdings Inc.: Strength in Dispensing and Closure Systems

Silgan is a global supplier of dispensing and closure solutions, with its Dispensing Solutions segment serving as a key growth driver. The company is investing in R&D to develop high-performance products that meet sustainability targets. Its strength lies in delivering high-quality, reliable systems that enhance consumer experience. Silgan’s commitment to recyclability and PCR integration resonates with clients under ESG scrutiny.

Gerresheimer AG: Realigning with Core Strengths

Gerresheimer, a specialist in glass and plastic primary packaging, announced in August 2025 its intention to divest its molded glass division to sharpen focus on pharma and medical devices. Despite this realignment, it continues to serve cosmetic and toiletry markets with premium glass containers. Its long-term sustainability target 50% CO2 reduction by 2030 and 100% renewable electricity sourcing strengthens its reputation as a high-standard supplier.

Amcor plc: Expanding Global Scale Through Berry Combination

Amcor, a leader in flexible and rigid packaging, finalized its combination with Berry Global in April 2025, creating one of the largest packaging entities worldwide. The expanded portfolio enables stronger positions in beauty, healthcare, and personal care containers. Innovations such as AmFiber™ Performance Paper and AmSky Blister Systems underline its commitment to recyclability and PVC-free solutions. Its global scale and material science expertise make it a formidable competitor in both developed and emerging markets.

Cosmetic and Toiletry Containers Market Share Insights

Bottles Dominate Market Share by Product Type in Cosmetic and Toiletry Containers Industry

Bottles lead the cosmetic and toiletry containers market with an estimated 35% share, cementing their role as the most versatile packaging format across personal care categories. Their dominance is rooted in their ability to accommodate a wide range of viscosities from shampoos and conditioners to serums and toners while supporting both mass-market PET/HDPE substrates and luxury glass designs. This versatility enables manufacturers to balance functionality, cost, and branding in one format, making bottles the default option for both premium and everyday use. In addition, advances in lightweighting and the integration of post-consumer recycled (PCR) resins are reshaping this segment, as beauty brands align packaging with corporate sustainability goals. Bottles also serve as a key platform for dispensing closures, pumps, and sprayers, allowing customization by product type, further entrenching their market leadership.

Skin Care Drives Market Share by Application in Cosmetic and Toiletry Containers Industry

Skin care represents the largest application segment, holding 30% of the market, reflecting the category’s central role in shaping container demand. Skincare encompasses diverse formats including bottles for cleansers, airless pumps for serums, jars for moisturizers, and tubes for sunscreens which makes it the most packaging-intensive sector of beauty. Growth in anti-aging, functional cosmetics, and dermo-cosmetics has elevated the importance of containers that preserve active ingredients, driving adoption of high-barrier laminates, UV-protective glass, and airless dispensing technologies. Skincare also drives premiumization trends, with packaging expected to convey efficacy, safety, and luxury in equal measure. As consumers demand transparency and eco-responsibility, brands are incorporating refillable bottles and mono-material packaging in skincare ranges, ensuring this application continues to dominate both unit volumes and innovation pipelines in the cosmetic and toiletry containers industry.

United States: Regulatory Reforms and Corporate Innovation Driving Sustainable Cosmetic and Toiletry Containers

The cosmetic and toiletry containers market in the United States is being reshaped by evolving regulations and sustainability commitments. California’s Plastic Pollution Prevention and Packaging Producer Responsibility Act (SB 54) has accelerated the shift toward recyclable and reusable packaging, creating momentum across industries from cosmetics to pharmaceuticals. Corporate initiatives are reinforcing this trend, with Amcor plc introducing its AmSky Blister System a PVC- and aluminum-free recyclable blister solution signaling the industry’s movement toward circular economy packaging. At the same time, the U.S. Drug Supply Chain Security Act (DSCSA) is strengthening demand for packaging with advanced security features such as RFID tags and barcodes to prevent counterfeiting and enhance traceability.

Sustainability is a top priority, supported by the U.S. Department of Energy’s $52 million investment into cellulose-based films as next-generation substrates, pushing manufacturers to phase out traditional plastics. Regulatory oversight is also tightening, with the Environmental Protection Agency (EPA) advancing new actions on PFAS, forcing companies to reformulate packaging materials. This shift is especially pronounced in pharmaceuticals and personal care, where demand for tamper-evident, portable, and PFAS-free packaging is rising. Together, these forces position the U.S. as a leader in sustainable, tech-enabled cosmetic and toiletry packaging innovation.

Germany: Circular Economy Leadership and EU PPWR Shaping the Packaging Industry

Germany stands at the forefront of the cosmetic and toiletry containers market, powered by stringent regulations and a well-established circular economy framework. The implementation of the EU Packaging and Packaging Waste Regulation (PPWR) in February 2025 is transforming the industry, mandating that all packaging be fully recyclable by 2030. Germany’s Verpackungsgesetz (Packaging Act) enforces producer responsibility across the entire packaging lifecycle, driving innovation in recyclability and reuse. This strong regulatory foundation ensures that cosmetic and toiletry brands must align with both national and EU-level sustainability goals.

German manufacturers are pioneering technological innovation with oxygen-barrier labels that integrate unique device identification (UDI) data, ensuring drug stability and compliance with the EU Medical Device Regulation (MDR). Companies like Gerresheimer AG are advancing eco-friendly packaging through bio-based closures and recyclable glass jars, launched in 2024. By blending cutting-edge technology with sustainability commitments, Germany is shaping the future of cosmetic and toiletry packaging across Europe.

China: Dual Carbon Policy and E-Commerce Expansion Fueling Eco-Friendly Packaging Demand

China’s cosmetic and toiletry containers market is undergoing a rapid transformation under the government’s “dual carbon” policy, which aims to achieve peak carbon emissions and carbon neutrality. Regulations restricting non-degradable plastics are creating significant demand for paper-based and recyclable laminates, while tax incentives are promoting investment in green packaging technologies. The expansion of e-commerce giants like Alibaba and JD.com is another major growth driver, as cosmetics and personal care brands require tamper-proof and secure packaging for online deliveries.

Technological advancements are also accelerating the market. The integration of AI, automation, and “5G plus industrial internet” solutions is enabling flexible and highly efficient production of cosmetic and toiletry containers. Furthermore, regulatory oversight has tightened with the National Medical Products Administration (NMPA) introducing new Good Manufacturing Practice (GMP) standards in June 2025, requiring manufacturers to implement advanced quality management systems. These combined regulatory, technological, and market dynamics are positioning China as a hub for next-generation cosmetic packaging solutions.

India: Regulatory Shifts and Consumer Demand Driving Next-Generation Packaging Solutions

India’s cosmetic and toiletry containers market is being driven by strong government support and rapidly changing consumer behavior. Initiatives such as “Make in India” and “Zero Effect Zero Defect” promote domestic manufacturing quality, while the Production Linked Incentive (PLI) scheme, worth INR 10,900 crore, supports high-quality packaging infrastructure. The Plastic Waste Management (Amendment) Rules, which target single-use plastics, are pushing cosmetic brands toward eco-friendly, recyclable, and water-soluble packaging alternatives.

Consumer dynamics are equally transformative. Rising disposable incomes, urbanization, and demand for convenient, single-serve packaging are fueling adoption in cosmetics and toiletries. Additionally, the pharmaceutical and healthcare sectors are expanding, requiring tamper-evident and child-resistant packaging to support home-based treatments. Corporate investments highlight this trend Kryolan’s INR 145 crore investment in India, announced in July 2025, is set to boost cosmetic packaging manufacturing capacity by 40% by 2026. Together, regulatory action, consumer demand, and private investment are making India a fast-emerging market for advanced cosmetic and toiletry packaging solutions.

Brazil: Sustainability Legislation and Technological Innovation Reshaping Packaging Practices

Brazil’s cosmetic and toiletry containers market is experiencing a strong regulatory push toward sustainability. The National Solid Waste Policy promotes circular economy practices, while the 2025 ban on solid waste imports, including plastics, has accelerated the need for domestic recycling and sustainable material development. These regulations are compelling cosmetic and toiletry manufacturers to prioritize reusable, recyclable, and eco-friendly packaging alternatives.

Technological innovation is another driving force, with robotics and AI being increasingly deployed for automated sorting, defect detection, and quality control in packaging production. The National Agency of Sanitary Surveillance (ANVISA) has also enforced stricter pharmaceutical packaging traceability rules, mandating serialization and unique identification to strengthen supply chain security. As a result, Brazil is becoming a dynamic market where sustainability mandates and high-tech packaging solutions converge.

Japan: Bio-Based Materials and Recycling Systems Leading Packaging Transformation

Japan’s cosmetic and toiletry containers market is defined by its advanced recycling infrastructure and strong government regulations. The Containers and Packaging Recycling Law assigns businesses responsibility for collection and recycling, creating one of the world’s most efficient systems for reusing rigid plastics and glass. In May 2025, the Ministry of Health, Labour and Welfare (MHLW) further strengthened the regulatory framework by revising packaging standards under the Food Sanitation Act, including migration limits for synthetic resins.

Sustainability trends are shaping packaging innovation, with Japanese companies investing in bio-based materials. LyondellBasell’s bio-based polypropylene adoption by Shiseido in September 2025 exemplifies this shift. Cosmetic brands are also prioritizing functional enhancements such as dimensional stability and resistance to deformation. Industry leaders like Kao Corporation are launching new product lines, such as its “melt” haircare brand in 2024, which is driving demand for specialized, high-performance containers. Japan’s blend of advanced recycling, regulatory rigor, and functional packaging innovation positions it as a global model for sustainable cosmetic and toiletry packaging.

Cosmetic and Toiletry Containers Market Report Scope

Cosmetic and Toiletry Containers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$37.4 Billion

|

|

Market Size (2034)

|

$62.1 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Material Type (Glass, Plastic, Metal, Paper & Paperboard, Bioplastics), By Product Type (Bottles, Jars, Tubes, Containers, Pumps & Dispensers), By Application (Skin Care, Hair Care, Fragrances, Oral Care, Makeup, Toiletries & Deodorants), By End-Use Industry (Commercial, Households)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Inc., AptarGroup, Inc., Gerresheimer AG, Silgan Holdings Inc., Albéa S.A., HCP Packaging, Cosmopak Corp., Quadpack, The Libo Cosmetics Company, Ltd., Verescence France, Vitro S.A.B., Lumson, DS Smith plc, Huhtamaki Oyj

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cosmetic and Toiletry Containers Market Segmentation

By Material Type

- Glass

- Plastic

- Metal

- Paper & Paperboard

- Bioplastics

By Product Type

- Bottles

- Jars

- Tubes

- Containers

- Pumps & Dispensers

By Application

- Skin Care

- Hair Care

- Fragrances

- Oral Care

- Makeup

- Toiletries & Deodorants

By End-Use Industry

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Cosmetic and Toiletry Containers Market

- Amcor plc

- Berry Global Inc.

- AptarGroup, Inc.

- Gerresheimer AG

- Silgan Holdings Inc.

- Albéa S.A.

- HCP Packaging

- Cosmopak Corp.

- Quadpack

- The Libo Cosmetics Company, Ltd.

- Verescence France

- Vitro S.A.B.

- Lumson

- DS Smith plc

- Huhtamaki Oyj

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive research methodology to provide a data-driven, actionable analysis of the global Cosmetic and Toiletry Containers Market. The study combined primary research, including interviews with packaging manufacturers, cosmetic and toiletry brands, distributors, and sustainability consultants, with secondary research encompassing regulatory frameworks, corporate ESG disclosures, trade publications, and market news. The methodology focused on evaluating key growth drivers such as post-consumer recycled (PCR) content mandates, refillable and reusable container trends, lightweight and high-barrier packaging innovations, and digital engagement technologies including QR codes, RFID, and NFC-enabled containers. Market sizing, segmentation, and forecasts were derived using historical data and adoption trends across leading regions including the U.S., Germany, China, India, Brazil, and Japan, along with insights into product type (bottles, jars, tubes, pumps) and application (skincare, haircare, fragrances, toiletries). Competitive intelligence was gathered on major players like Albéa, AptarGroup, Silgan, Gerresheimer, and Amcor, analyzing their sustainability strategies, technological innovations, regional expansions, and ESG commitments. By integrating regulatory, technological, and consumer-driven trends, USDAnalytics delivers insights tailored for industry professionals seeking strategic investment guidance, operational optimization, and market positioning intelligence.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.