Digital Printing for Packaging Market Overview: Growth to $70.9 Billion by 2034 Driven by Personalization, On-Demand Runs, and Smart Features (CAGR 9.2%)

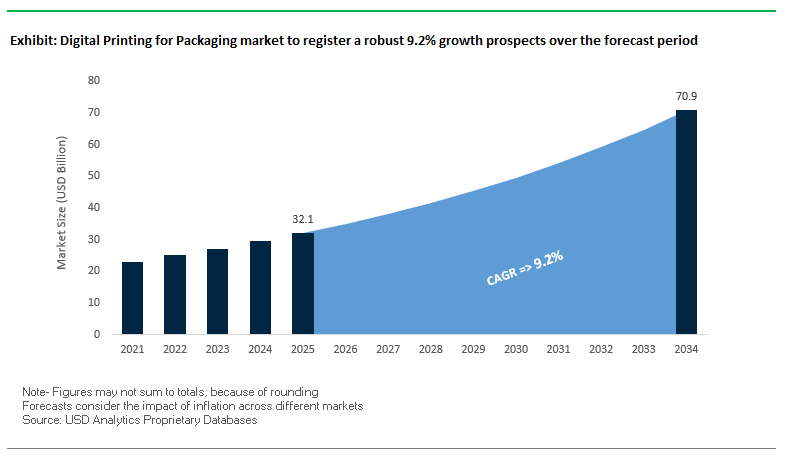

The global digital printing for packaging market is projected to rise from $32.1 billion in 2025 to $70.9 billion by 2034, expanding at a strong CAGR of 9.2%. As brand owners demand shorter lead times, personalization, and sustainable printing, digital technology is reshaping packaging across labels, cartons, corrugated, and flexible packaging. For industry professionals, the key questions are: how to maximize ROI on digital printing assets, how to merge sustainability with speed-to-market, and how to leverage smart packaging integration for consumer engagement and supply chain efficiency.

Key Insights for packaging buyers and strategists:

- On-Demand Efficiency: Digital printing reduces packaging inventory costs by 30%+, enabling frequent, small-batch runs and lowering waste.

- Personalized Packaging: Over 70% of new food & beverage launches now include customized graphics, using digital print as a consumer engagement tool.

- Eco-Friendly Inks: Shift toward water-based, VOC-free inks supports food safety, sustainability, and regulatory compliance.

- Smart Packaging Integration: Digital enables QR codes, NFC tags, and variable data, enhancing product traceability, loyalty programs, and anti-counterfeiting efforts.

Market Analysis: Strategic Consolidation and Eco-Innovation Define 2025

The year 2025 is proving pivotal as digital printing aligns with the packaging industry’s shift to low-carbon materials, smart functionalities, and supply chain optimization. In September 2025, Constantia Flexibles highlighted its Ecolutions portfolio at FACHPACK 2025, showcasing recyclable lidding with low-carbon aluminum, a sustainability trajectory that digital print supports through short-run agility and waste reduction. The same month, BERHALTER presented its Swiss Die-Cutter™, designed to minimize material waste and downtime perfectly complementing digital’s just-in-time, short-run capabilities.

In August 2025, industry focus intensified as HP and FIMI emerged as final bidders for Landa Digital Printing, underlining the strategic importance of nanographic technology in high-speed digital packaging markets. Also in August, Orora Group’s acquisition of Saverglass for €1.29 billion reinforced premiumization trends in luxury spirits and cosmetics, segments where digital embellishment and short-run customization are critical differentiators.

Earlier, in July 2025, Huhtamaki introduced fiber-based compostable ice cream cups, an innovation requiring high-quality digital print for branding on eco-friendly substrates. The same month, the merger of Smurfit Kappa and WestRock formed Smurfit WestRock, consolidating global paper-based packaging a key growth market for digital corrugated printing. In May 2025, DS Smith launched its DryPack corrugated solution in North America, targeting EPS replacement, with digital printing providing flexible branding. Meanwhile, in February 2025, The Good Cup introduced a plastic-free paper cup, relying on digital graphics to drive consumer appeal in sustainable foodservice formats.

Trends and Opportunities Shaping the Digital Printing for Packaging Market

Strategic Shift to Production-Level Speed and Scalability

The digital printing for packaging market is undergoing a pivotal transformation as technology advancements enable presses to move beyond short-run, niche applications into production-level speed and scalability. Historically, flexography and offset printing dominated medium-to-high volume packaging runs, but today’s single-pass inkjet and advanced digital presses are closing the productivity gap.

For instance, the EFI Nozomi single-pass inkjet press delivers speeds of up to 246 linear feet per minute, enabling converters to replace litho-laminated and pre-print corrugated operations with a flexible, on-demand alternative. In the folding carton and flexible packaging sectors, the HP Indigo 200K and 100K Digital Presses and the Landa S11 press now achieve throughputs of 6,000 to over 11,200 sheets per hour, rivaling traditional offset capabilities with the added benefit of shorter setup times and reduced waste. Meanwhile, the Kodak PROSPER 7000 Turbo Press, operating at an unmatched 1,345 feet per minute, demonstrates how continuous inkjet systems can deliver high-volume, hybrid solutions that compete directly with analog presses. These milestones illustrate how digital printing is becoming a mainstream solution for corrugated, flexible, and folding carton applications, reshaping investment decisions across global converters.

Expansion of Water-Based Inkjet for Food Contact and Sustainability

A second defining trend is the shift toward water-based inkjet inks that comply with global food safety regulations and align with brand sustainability mandates. As food packaging must meet EU 10/2011 and U.S. FDA 21 CFR compliance, water-based inks provide a safer alternative by eliminating heavy metals, solvents, and high VOC emissions common in UV-curable inks. This positions them as the preferred choice for direct food-contact applications, particularly in snack packaging, fresh produce labels, and folding cartons.

In parallel, sustainable ink formulations using bio-based ingredients are gaining adoption, reducing toxicity while improving recyclability. Leading innovations now allow water-based inks to perform across a broader substrate range, including flexible films and coated papers, enabling brands to standardize their digital printing systems across multiple product categories. This versatility not only meets environmental goals but also satisfies consumer expectations for safe, recyclable, and low-impact packaging. As regulations tighten and brand owners seek greener alternatives, water-based inkjet technology is emerging as a cornerstone of the digital packaging ecosystem.

Integration of AI and Machine Learning for Automated Workflow and Color Management

One of the most promising opportunities lies in integrating AI and machine learning to enhance automation, improve efficiency, and reduce waste in digital printing workflows. Traditional pre-press and color management tasks are labor-intensive, but AI-driven algorithms can automatically detect and correct deviations in real-time, ensuring consistent color across entire runs without human intervention. This reduces errors, shortens setup times, and enables printers to meet brand expectations for color accuracy and consistency.

Generative AI is also being leveraged for design innovation, producing hundreds of packaging variations that optimize for sustainability, structural strength, and visual appeal. This accelerates the design-to-market timeline, allowing brands to rapidly test new campaigns. Additionally, predictive maintenance powered by AI enables manufacturers to anticipate machine breakdowns before they occur, minimizing downtime and optimizing utilization rates. For converters, these advancements translate into higher productivity, lower operating costs, and greater flexibility in meeting dynamic packaging demands.

Development of Integrated Digital Finishing and Decoration

The evolution of digital printing is expanding beyond ink application into fully integrated finishing and embellishment processes, creating new opportunities for premium, high-value packaging. Digital embellishment units are now capable of applying spot gloss, foiling, and embossing inline, eliminating costly and time-intensive analog processes. This allows brands to achieve premium aesthetics and tactile experiences without compromising speed-to-market.

Moreover, digital finishing enables variable data embellishment, where each package can feature unique foiling or textured patterns. This capability is particularly valuable for limited-edition launches, serialized products, and personalized packaging, aligning with the growing trend of hyper-customization in consumer goods. By integrating finishing into the digital workflow, converters reduce material handling and production time while increasing efficiency and profitability. As a result, the market is seeing a rise in end-to-end digital production cells, offering a single streamlined solution for printing, decorating, and finishing packaging at scale.

Competitive Landscape: Leading Technology Providers Driving Customization and Sustainability

The digital printing for packaging market is dominated by a few technology leaders competing on print speed, ink chemistry, substrate versatility, and workflow integration. The following profiles highlight their core capabilities and strategies.

HP Inc. Indigo and PageWide Platforms Dominate Global Digital Packaging

HP leads with its HP Indigo and HP PageWide portfolios, serving labels, cartons, and flexible packaging. Indigo presses, such as the 200K for flexibles and 35K for cartons, deliver offset-comparable quality using liquid electrophotography (LEP). HP’s Indigo V12 and LEPx technology target high-volume label production, a traditionally analog space. Its ecosystem includes HP PrintOS software, enabling real-time workflow optimization. With the largest installed base globally, HP remains the market leader in digital packaging presses.

Konica Minolta, Inc. Inkjet Versatility and Premium Embellishment Capabilities

Konica Minolta drives innovation with its AccurioJet KM-1e UV inkjet for folding cartons and AccurioLabel series for labels. Its strength lies in versatility across substrates and automation for short-run jobs. Notably, its MGI JETvarnish solutions enable digital embellishments like spot varnish and 3D textures, a growing demand in premium packaging. By integrating presses, finishing equipment, and software, Konica Minolta offers end-to-end solutions tailored for converters expanding into high-value packaging.

Domino Printing Sciences plc Hybrid Printing and Industrial Inkjet Reliability

Domino excels in industrial inkjet printing, with its N-Series (labels) and X-Series (corrugated) platforms. The N730i UV inkjet press delivers high-quality variable data printing, while the K600i module integrates barcodes and QR codes directly into existing lines. Its Hybrid model, blending flexo with digital, helps converters balance speed and flexibility. Domino’s strength is in track-and-trace and coding integration, vital for regulated industries like pharma and beverages.

Landa Digital Printing Nanographic Technology as a Disruptive Force

Landa’s Nanographic Printing® (Nanography®) uses water-based inks to combine the speed of offset with the flexibility of digital. Its S11 and S11P B1-format presses serve folding cartons and flexible packaging at industrial volumes. Currently under creditor protection, with HP and FIMI vying for acquisition (Aug 2025), Landa remains a high-stakes player. Its core strength is scaling short-to-medium runs at cost structures competitive with analog, making it an attractive acquisition target for consolidators.

Durst Group Sustainable Inks and Corrugated Excellence

Durst is renowned for corrugated and carton printing systems, with its Rho and P5 platforms supporting large-format substrates. Innovations include water-based, food-safe inks and a white ink solution for printing vibrant graphics on unbleached brown board, aligning with eco-friendly trends. Durst’s strategy is holistic providing presses, inks, and workflow software as an integrated package. Its systems are widely used in point-of-sale displays and high-quality corrugated packaging requiring color consistency and sustainability compliance.

Digital Printing for Packaging market Share Insights

Labels Dominate Market Share by Packaging Format

Labels account for 35% of the global digital printing for packaging market in 2025, cementing their position as the entry point and volume leader. Labels were the first application to fully embrace digital technology due to their relatively small size, need for versioning, and the advantages of variable data printing such as QR codes, serialization, and product personalization. The massive production scale of food, beverage, and pharmaceutical labels ensures continued demand, while the flexibility of digital technology supports short-run customization and frequent design changes. Corrugated packaging, holding 25%, is the fastest-growing format, fueled by the e-commerce boom and direct-to-consumer (DTC) sales models. Retail-ready boxes increasingly require high-quality graphics, regional customization, and quick turnaround, making digital printing indispensable for brand owners looking to reduce inventory costs while enhancing consumer engagement. Flexible packaging is emerging as a critical growth driver, although technical challenges such as ink adhesion and durability on high-barrier substrates limit its penetration compared to labels and corrugated. Still, its role in prototyping, limited-edition launches, and personalized snack packaging ensures steady adoption. Folding cartons and rigid plastics serve the premium branding niche, where vibrant graphics, personalization, and short-run production are vital for cosmetics, luxury goods, and electronics. Meanwhile, metal packaging remains a highly specialized, small-volume segment, reserved for promotional or premium cans requiring durable curing inks where traditional offset or lithographic printing continues to dominate.

Food & Beverages Lead Market Share by End-Use Industry

The food and beverages sector captures 40% of the digital printing for packaging market in 2025, making it the largest and most influential end-use segment. This leadership is driven by the FMCG industry’s constant need for rapid packaging updates to support seasonal launches, regional product variants, and limited-time promotional campaigns. Digital printing offers unparalleled agility, enabling brand owners to test market trends without committing to costly long print runs. Personal care and cosmetics, with a 22% share, represent the second-largest and most value-driven segment, where aesthetics and exclusivity are critical to consumer perception. Digital solutions enable personalized product packaging such as printing consumer names or unique graphics on lipstick tubes and skincare cartons helping brands stand out in a crowded premium market. Consumer goods manufacturers are leveraging digital printing as an agile marketing tool, particularly for e-commerce platforms like Amazon, where smaller batch sizes and regionalized SKUs are common. Pharmaceuticals and healthcare represent a compliance-driven segment, where digital printing is indispensable for track-and-trace serialization, regulatory labeling, and tamper-evident coding under frameworks such as the U.S. DSCSA and Europe’s FMD. Electronics, while smaller in share, rely on digital printing for premium packaging and precision variable data, enhancing both consumer experience and supply chain traceability. Together, these end-use industries illustrate how digital printing is not only disrupting traditional workflows but also enabling packaging to become a dynamic marketing and compliance tool across sectors.

United States: E-Commerce and Personalized Packaging Driving Digital Printing Growth

The U.S. digital printing for packaging market is witnessing rapid growth, largely fueled by the explosive expansion of e-commerce and the rising demand for personalized, customized packaging solutions. Brands are leveraging digital printing to create unique consumer experiences, enhance brand loyalty, and implement marketing strategies that differentiate their products. Advanced investments in high-speed inkjet technology, including single-pass presses for corrugated cardboard, cartons, and flexible packaging, are enabling faster turnaround and greater efficiency. Companies like WestRock are deploying HP PageWide presses to expand their digital printing capabilities and meet increasing market demand.

Sustainability is another key trend shaping the U.S. market. Digital printing reduces waste from prepress stages, allows on-demand production, and supports eco-friendly, water-based inks, helping companies align with environmental regulations and consumer expectations. Additionally, healthcare and pharmaceutical applications are driving growth, as digital printing allows the printing of variable data such as unique serial numbers, barcodes, and QR codes, ensuring track-and-trace, anti-counterfeiting, and serialization compliance.

Germany: Automation, Hybrid Solutions, and Sustainable Business Models Lead the Market

Germany’s digital printing for packaging sector is characterized by its strong emphasis on automation and Industry 4.0 integration. Intelligent systems streamline workflows from prepress to postpress, improving precision and reducing labor requirements. Companies are also leveraging sustainable business models, adopting eco-friendly inks, and minimizing CO2 emissions throughout the production process.

Strategic investments are a major trend, with companies like Mondi implementing digital printing to enhance logistics efficiency, such as printing consecutive barcodes and QR codes directly onto packaging, eliminating the need for separate labels. Furthermore, the market is increasingly adopting hybrid printing presses, combining digital inkjet technology with traditional flexo or offset methods. This integration offers both speed and embellishment capabilities alongside the customization and flexibility of digital printing, positioning Germany as a pioneer in sustainable and high-precision packaging solutions.

China: High-Volume Production and Customization Fuel Digital Printing Demand

China’s digital printing for packaging market benefits from its role as a global manufacturing hub and the nation’s vast e-commerce ecosystem. The industry is driven by the need for both large-scale production and short-run, customized packaging jobs, enabling a balance between mass-market efficiency and niche product differentiation. Manufacturers are heavily investing in high-speed, efficient digital printing equipment, expanding the installed capacity of digital label presses to meet growing demand.

Digital printing is also being used to combat counterfeiting and improve traceability, with brands adopting variable data printing, including unique codes, serial numbers, and security features, to ensure product authenticity. However, the market must navigate fluctuating raw material prices, particularly for corrugated paper and other substrates, which influence production costs and pricing strategies.

India: Government Initiatives and Smart Packaging Accelerate Digital Printing Adoption

The Indian digital printing for packaging market is experiencing rapid growth, fueled by initiatives such as Make in India, which encourage modernization and digital adoption across manufacturing sectors. The food and beverage, pharmaceutical, and consumer goods industries are key catalysts, driving demand for customized, aesthetically appealing, and brand-differentiated packaging that resonates with a young, brand-conscious consumer base.

A notable trend is the rise of smart packaging, with QR codes and other interactive digital features integrated into packaging, allowing brands to engage directly with consumers and provide product information. The growth of local digital printing service providers is also supporting the market, with investments in advanced equipment enabling high-quality short-run jobs and custom packaging solutions for small and medium-sized enterprises.

Japan: Precision, Sustainability, and Workflow Optimization Define the Market

Japan’s digital printing for packaging market is distinguished by its emphasis on high-quality, precise, and visually striking packaging. Companies are investing in sustainable materials and eco-friendly inks, such as water-based solutions, reflecting the country’s environmental responsibility initiatives.

The industry is also focused on streamlining production workflows, reducing lead times, and enabling just-in-time manufacturing to minimize inventory costs. By integrating digital printing technologies, Japanese manufacturers are able to produce functional yet visually appealing packaging that meets the rigorous expectations of both domestic and international consumers.

Digital Printing for Packaging Market Report Scope

Digital Printing for Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$32.1 Billion

|

|

Market Size (2034)

|

$70.9 Billion

|

|

Market Growth Rate

|

9.2%

|

|

Segments

|

By Printing Technology (Inkjet Printing, Electrophotography Printing, Thermal Transfer Printing, Others), By Packaging Format (Labels, Flexible Packaging, Corrugated Packaging, Folding Cartons, Rigid Plastics, Metal Packaging, Other Formats), By Ink Type (UV-Curable Inks, Aqueous Inks, Solvent-Based Inks, Other Inks), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Personal Care & Cosmetics, Consumer Goods, Electronics, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

HP Inc., Canon Inc., Xerox Corporation, EFI (Electronics For Imaging), Konica Minolta, Inc., Domino Printing Sciences plc, Durst Group AG, Sistrade - Software Consulting, S.A., Sun Chemical, Siegwerk Druckfarben AG & Co. KGaA, Mark Andy Inc., Xeikon N.V., Bobst Group SA, Landa Corporation, Agfa-Gevaert Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Digital Printing for Packaging Market Segmentation

By Printing Technology

- Inkjet Printing

- Electrophotography Printing

- Thermal Transfer Printing

- Others

By Packaging Format

- Labels

- Flexible Packaging

- Corrugated Packaging

- Folding Cartons

- Rigid Plastics

- Metal Packaging

- Other Formats

By Ink Type

- UV-Curable Inks

- Aqueous Inks

- Solvent-Based Inks

- Other Inks

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Personal Care & Cosmetics

- Consumer Goods

- Electronics

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Digital Printing for Packaging market

- HP Inc.

- Canon Inc.

- Xerox Corporation

- EFI (Electronics For Imaging)

- Konica Minolta, Inc.

- Domino Printing Sciences plc

- Durst Group AG

- Sistrade - Software Consulting, S.A.

- Sun Chemical

- Siegwerk Druckfarben AG & Co. KGaA

- Mark Andy Inc.

- Xeikon N.V.

- Bobst Group SA

- Landa Corporation

- Agfa-Gevaert Group

* List Not Exhaustive

Research Coverage

This report investigates the Digital Printing for Packaging Market, presenting a comprehensive examination of technological breakthroughs, operational efficiencies, and sustainability-driven innovations that are redefining modern packaging. USDAnalytics’ analysis reviews key developments, including the transition from traditional analog printing to high-speed digital solutions, the adoption of water-based, food-safe inks, and integration of AI-enabled workflow automation for precision color management. The report highlights how personalization, short-run efficiency, and smart packaging functionalities such as QR codes, NFC tags, and variable data printing are driving brand engagement, supply chain optimization, and anti-counterfeiting measures. Strategic mergers, acquisitions, and innovative solutions by industry leaders like HP, Konica Minolta, Domino, Landa, and Durst are also analyzed to illustrate market dynamics. This report is an essential resource for packaging engineers, brand strategists, procurement professionals, and sustainability managers seeking actionable insights, historical trends from 2021 to 2024, and forward-looking forecasts from 2025 to 2034, enabling data-driven decision-making in a rapidly evolving market landscape.

Scope Highlights:

- Segmentation: By Printing Technology (Inkjet Printing, Electrophotography Printing, Thermal Transfer Printing, Others), By Packaging Format (Labels, Flexible Packaging, Corrugated Packaging, Folding Cartons, Rigid Plastics, Metal Packaging, Other Formats), By Ink Type (UV-Curable Inks, Aqueous Inks, Solvent-Based Inks, Other Inks), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Personal Care & Cosmetics, Consumer Goods, Electronics, Other Industries)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historical and Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis and profiles of 15+ companies including HP Inc., Canon Inc., Xerox Corporation, EFI, Konica Minolta, Domino Printing Sciences, Durst Group, Sistrade, Sun Chemical, Siegwerk, Mark Andy, Xeikon, Bobst Group, Landa Corporation, and Agfa-Gevaert

Methodology

The Digital Printing for Packaging Market report employs a rigorous methodology combining primary and secondary research to deliver accurate, actionable insights. Primary research involved consultations with packaging engineers, R&D managers, procurement heads, and brand strategists to assess emerging trends in ink chemistry, substrate versatility, short-run production efficiency, and smart packaging integration. Secondary research incorporated company reports, trade publications, regulatory standards, patent filings, and market databases to validate technology adoption, industry benchmarks, and regional growth patterns. Data triangulation and market modeling techniques were applied to forecast demand, evaluate material trends, and estimate adoption rates of inkjet, electrophotography, and thermal transfer technologies across packaging formats. USDAnalytics synthesizes these findings into a structured, SEO-optimized analysis tailored to industry professionals, highlighting historical insights, production-level capabilities, and projections from 2025 to 2034.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.