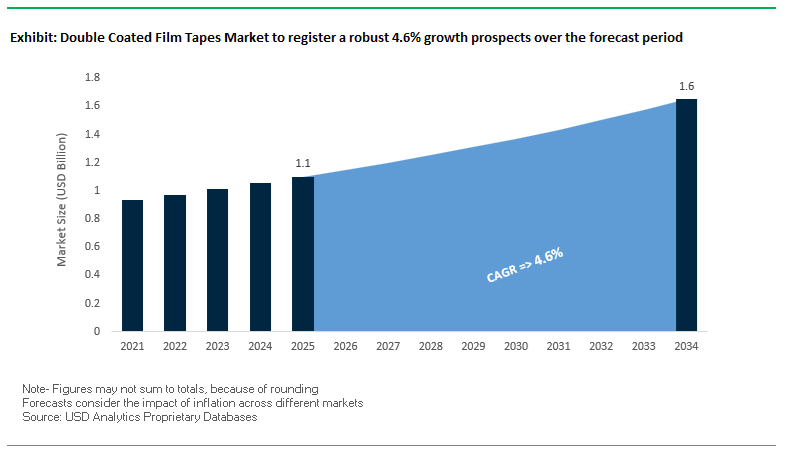

The global double coated film tapes market is being redefined by its strategic role as an engineered bonding medium in precision assembly environments. Market growth from USD 1.1 billion in 2025 to USD 1.6 billion by 2034 (CAGR 4.6%) reflects demand from electronics assembly, automotive interior bonding, flexible displays, and industrial laminations where joint reliability, thermal endurance, and chemical resistance are integral to product performance. Double coated film tapes are increasingly specified in OEM design standards to replace mechanical fasteners and liquid adhesives in applications that demand predictable peel strength, controlled shear performance, and dimensional stability across broad temperature regimes.

OEMs and tier suppliers have elevated expectations for dual-adhesive constructions tailored to substrate chemistry and process conditions. For example, 3M’s double coated tapes—such as the 9731 series combining high-performance acrylic with silicone PSA on a thin PET film—are engineered for bonding silicone elastomers and foams while maintaining dimensional stability under thermal and chemical stress, facilitating reliable gasketing and filter applications in industrial and fluid handling systems. The polyester carrier’s rigidity ensures consistent die-cut accuracy and automated handling—a prerequisite in high-volume electronics and module assembly lines. Similarly, 3M formulations incorporating 300LSE acrylic adhesives are optimized for bonding to low surface energy (LSE) plastics such as polypropylene and powder-coated substrates, aligning with automotive and appliance OEM requirements where secure adhesion to difficult plastics directly affects assembly yield and lifecycle performance.

Leading manufacturers have diversified adhesive chemistries and carrier technologies to address process-specific constraints. Nitto Denko’s double coated systems are engineered for strong cohesive strength and tack on foams and plastics, including challenging LSE substrates, ensuring stable bond lines in automated mounting and appliance manufacturing. Tesa SE and Avery Dennison offer differential designs—such as Avery’s FT 5295—with controlled lower bond strength on one side to support clean reworkability in electronics assembly without substrate damage, addressing OEM needs for serviceability in high-value devices. Lohmann’s portfolio is supported by advanced coating and die-cutting capability with a decades-long patent foundation in bonding technology, enabling custom film backing and adhesive combinations that meet automotive interior bonding standards and low-VOC performance goals, aligning with REACH and sustainability criteria. These material innovations—spanning acrylic, silicone, and hybrid PSA systems on PET or specialized film carriers—are replacing bulk adhesives and mechanical fastening in applications where bonded joints contribute to overall system integrity, thermal management, and weight reduction.

Across segments, the shift toward solvent-free and low-VOC production aligns with tightening global environmental compliance while preserving high performance under stress and temperature extremes. For OEMs, this results in improved manufacturing throughput, reduced rework and warranty costs, and greater design flexibility for lightweighting and miniaturization. As Asia-Pacific expands electronics and semiconductor assembly capacity, and as automotive platforms integrate more plastics and composite substrates, double coated film tapes will play an increasing role as engineered structural elements in bonded assembly flows rather than ancillary consumables.

The double coated film tapes industry is undergoing a transformation led by technological innovation, sustainability mandates, and regional manufacturing expansion. Key developments underscore the market’s dynamic progression toward advanced bonding materials, circular economy models, and REACH-compliant formulations.

In August 2025, a leading global manufacturer unveiled a 100μm thin acrylic tape engineered for EV interior trim applications, meeting stringent low-VOC and anti-fogging standards demanded by top OEMs. This launch reflects the shift toward lightweight, odor-free, and thermally stable adhesives critical for next-generation electric vehicles. In July 2025, a European adhesive tape specialist strengthened its foothold in high-tech applications through the acquisition of a North American coating technology firm, integrating UV-curable systems to enhance optically clear adhesive (OCA) production for premium displays and foldable electronics.

The sustainability focus continued in May 2025, when a leading tape producer introduced the first bio-based double-sided film tape containing 30% renewable carbon content in its carrier layer, alongside solvent-free adhesive chemistries. This eco-driven shift supports carbon footprint reduction (PCF) initiatives in the electronics and packaging industries. Similarly, in April 2025, a global adhesive brand partnered with a medical device leader to co-develop breathable and skin-friendly film tapes for wearable sensors—an emerging niche in medical-grade double coated film adhesives.

Meanwhile, technological advancements are enabling greater production efficiency and recyclability. In March 2025, an adhesive technology pioneer introduced an instant “Bond & Detach” system, allowing reworkable, high-strength bonds that can be easily released with controlled heat or chemical activation—a key development supporting device repairability and circular manufacturing in the electronics sector. By February 2025, several manufacturers had announced REACH-compliant product portfolios, emphasizing the elimination of hazardous chemicals from acrylic film tapes to meet tightening European regulations.

From a manufacturing perspective, Asia-Pacific investments continue to drive capacity and competitiveness. In June 2025, a global materials company allocated $50 million to expand PSA production in Southeast Asia, catering to the surge in smartphone, display, and FMCG packaging demand. Complementing this, in November 2024, a $30 million ISO Class 7 cleanroom facility was established in North America to produce optically clear film tapes for OLED and LCD screens, reinforcing the trend toward precision adhesive coating environments.

Double Coated Film Tapes Market Share Insights, 2025-2034

Thin double coated film tapes dominate the global double coated film tapes industry, accounting for an estimated 43.6% share in 2025. Their dominance stems from their adaptability across a wide range of industrial and commercial applications where high bonding strength, optical clarity, and flexibility are required without adding excessive bulk. These tapes, typically made from PET, PP, or PE carriers, are extensively used in automotive trim mounting, electronics assembly, and appliance manufacturing, providing reliable adhesion while maintaining low thickness profiles for aesthetic and functional integration. They deliver an ideal balance between adhesive strength, conformability, and temperature stability, making them compatible with both smooth and textured surfaces. Additionally, the proliferation of lightweight materials and compact electronic devices has increased demand for thin-film constructions that provide high-performance bonds in limited spaces.

Standard thickness double coated film tapes remain a core segment in the global adhesive tape market, primarily due to their robust adhesion strength and balanced mechanical stability. These tapes are widely used in construction, packaging, automotive interiors, and industrial equipment assembly, where moderate gap filling and cushioning properties are advantageous. Their balanced bond line ensures uniform stress distribution, enhancing joint longevity in applications subject to mechanical vibration or thermal cycling. In building envelope sealing, HVAC ducting, and packaging splicing, these tapes deliver dependable adhesion over a wide temperature range. Their continued relevance also stems from their cost-effectiveness and versatility, making them the preferred option for medium-performance, general-purpose tasks where ultra-thin or high-performance variants are unnecessary. As sustainability becomes a key differentiator, manufacturers are increasingly shifting toward solvent-free, water-based, and recyclable carrier systems, expanding the eco-friendly potential of this segment across global industrial supply chains.

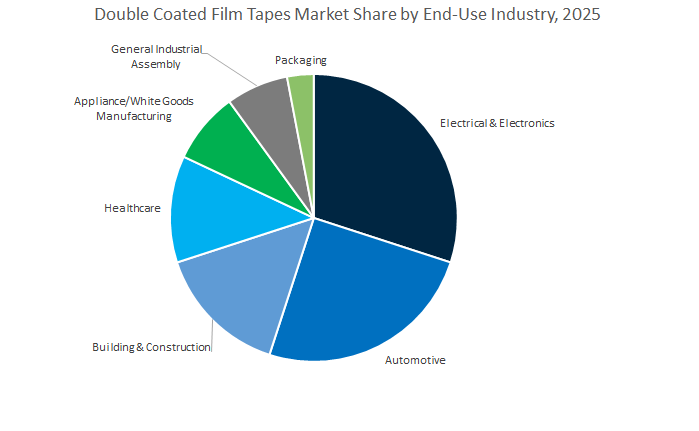

The electrical and electronics sector accounts for the largest share of the global double coated film tapes market, representing 32.1% of global demand in 2025. These tapes are indispensable in smartphones, tablets, LED modules, and display assemblies, where precise bonding, minimal residue, and high dielectric stability are required. As devices become thinner, lighter, and more integrated, double coated film tapes replace mechanical fasteners and liquid adhesives to deliver cleanroom-compatible, high-performance bonding solutions. They are extensively used in touch panel lamination, EMI shielding, and internal component assembly—providing permanent yet reworkable adhesion that supports efficient automated production. The segment also benefits from the accelerating transition to flexible electronics and foldable displays, where ultra-thin PET- and acrylic-based tapes ensure uniform stress distribution and dimensional stability under bending. With the growth of semiconductor packaging and 5G-enabled devices, demand for precision-engineered, thermally stable film tapes with low outgassing and contamination resistance continues to surge globally.

The automotive industry is the second-largest consumer of double coated film tapes, commanding approximately 23.6% of the market share. The segment’s strength lies in its extensive use across interior and exterior mounting applications, including emblems, trim, nameplates, and sensors, where these tapes provide durable, weather-resistant bonding without mechanical fasteners. As automakers accelerate the shift to lightweight materials and electric mobility, double coated film tapes are increasingly employed to bond composite panels, battery modules, wire harnesses, and NVH damping materials. Their combination of temperature resistance, shock absorption, and chemical stability makes them integral to modern vehicle design. Additionally, the move toward autonomous and connected vehicles is expanding the use of specialty tapes for securing radar, camera, and LiDAR systems. OEMs and Tier-1 suppliers are favoring acrylic foam-based and high-adhesion PET carrier tapes that balance long-term performance with ease of automation. This sector’s ongoing transition to adhesive-based assembly for lightweight and modular design ensures its position as a key growth engine within the global market.

The double coated film tapes market is defined by a handful of global leaders known for precision coating expertise, material integration, and sustainability-led innovation. Companies such as 3M, Tesa SE, Nitto Denko Corporation, Lohmann GmbH, and Avery Dennison Corporation are continuously developing high-performance, reworkable, and thermally stable tapes to meet the evolving requirements of automotive, display, electronics, and medical device manufacturers. Their strategies focus on expanding UV-curable technologies, VOC-free manufacturing, and LSE substrate bonding performance.

3M dominates the double coated film tapes market with its 300LSE acrylic adhesive platform, engineered to deliver superior adhesion to LSE substrates like polypropylene and powder-coated surfaces. The company’s 93015LE polyester carrier tape is widely approved across automotive OEM specifications for both interior and exterior bonding. By pioneering solventless coating technologies, 3M supports industrial clients in achieving Scope 3 emission reduction goals. The firm also maintains global application engineering centers that assist in high-precision die-cutting and converting processes, reinforcing its leadership in industrial adhesive innovation.

Tesa SE is recognized for its Bond & Detach series, a reworkable tape technology enabling strong temporary bonding in electronics and display assembly while promoting repairability and recyclability. Its tesa® 88010 series, used in display lamination, ensures optical clarity and high bonding reliability in touch panels and flexible OLED modules. Tesa’s strategic investments target sustainable formulations and thinner carrier films to reduce environmental impact. Through its Customer Solution Centers, Tesa collaborates directly with clients to optimize automated integration and high-precision converting operations.

Nitto Denko Corporation leverages decades of expertise in precision materials engineering to provide high-reliability double coated tapes such as No. 5915 for FPC-to-stiffener bonding and TR-5310EX series for thermal management applications. Known for minimal adhesive volatilization and superior chemical resistance, these tapes are ideal for use in electronics manufacturing environments involving soldering and solvent cleaning. Nitto’s D9605 tape also showcases exceptional 180° peel adhesion, ensuring durability in high-demand industrial and consumer appliance applications.

Lohmann GmbH, widely known as “The Bonding Engineers,” offers full-scale integration from adhesive formulation to process automation. Its DuploCOLL® 3605.2 polyester tape, featuring pure acrylic adhesive, is designed for permanent, high-strength bonding in construction and industrial settings. Using its TwinMelt® solvent-free process, Lohmann enhances sustainability and process efficiency. The company also develops DuploTEC® SBF structural bonding films, showcasing expertise in reactive adhesive technologies that extend into lightweight construction and smart building applications.

Avery Dennison provides a diverse Core Series™ portfolio of double coated film tapes, offering tailored adhesive technologies from rubber-based to High-Performance Acrylic (HPA) systems. Their differential adhesive tapes, combining silicone and acrylic layers, deliver effective bonding between dissimilar substrates such as silicone sponge to metals. With a strong focus on VOC reduction and solvent-free adhesive chemistry, Avery Dennison is driving environmentally responsible innovation across graphic attachment, membrane switch, and high-temperature applications.

China’s double coated film tapes market continues to accelerate under the nation’s “Made in China 2025” industrial strategy, which prioritizes New Materials production and innovation in adhesive technology. The country’s focus on domestic self-sufficiency and sustainable industrial expansion has spurred extensive R&D investment and production capacity expansion for high-performance double coated film tapes used in electronics, EV components, and renewable energy.

China’s EV component manufacturing boom—driven by state and private investment—creates significant demand for battery thermal management tapes and lightweight structural bonding materials. The specialized double coated films provide vibration resistance, insulation, and long-term bonding integrity in electric powertrains. Simultaneously, the surge in smart manufacturing and flexible display assembly, aligned with the 14th Five-Year Plan, is fueling adoption of optically clear, ultra-thin, and high-durability double coated film tapes for wearables and foldable electronics.

With major domestic players scaling operations in Jiangsu and Guangdong, China is rapidly evolving into the largest production hub for high-performance double coated adhesive tapes, integrating AI-enabled quality control systems to ensure uniform thickness and adhesion strength across large-scale production lines.

The United States double coated film tapes industry is characterized by cutting-edge pressure-sensitive adhesive (PSA) technology development, particularly for high-reliability sectors such as aerospace, medical devices, and infrastructure. Major American manufacturers are investing in next-generation ultra-thin double coated tapes that combine high peel strength with excellent temperature and solvent resistance, catering to aerospace bonding and electronics assembly applications.

In the medical device fabrication segment, the market is experiencing strong growth due to the demand for skin-friendly acrylic and silicone adhesive films designed for wearable health monitors and wound care applications. The FDA’s regulatory clarity and rising adoption of biocompatible adhesive systems have encouraged continuous R&D in breathable, hypoallergenic, and sterilization-resistant film tapes.

Additionally, the U.S. infrastructure revitalization efforts under federal investment programs are stimulating demand for environmentally resistant, UV-stable double coated film tapes used in construction bonding, glazing, and insulation systems. Companies are also leveraging low-VOC and solvent-free adhesives to align with LEED and EPA sustainability standards, reinforcing the country’s leadership in high-value engineered adhesive films.

Germany is a leading innovation hub in the European double coated film tapes market, driven by its Industry 4.0 transformation and leadership in automotive lightweighting. The Plattform Industrie 4.0 initiative promotes the integration of digital and cyber-physical manufacturing systems, enabling robotic application of double coated tapes for precision assembly in industrial automation and automotive manufacturing.

German automotive OEMs are significantly increasing the use of foam-backed and transfer film tapes to address NVH (Noise, Vibration, and Harshness) reduction and interior panel bonding in both EV and conventional vehicles. Moreover, the market is witnessing major advancements in Optically Clear Adhesives (OCA) with bubble-free lamination, providing superior optical clarity and thermal stability (up to 105°C) for Human-Machine Interface (HMI) panels and automotive displays.

Companies such as BASF, Henkel, and tesa SE are spearheading sustainability by developing solvent-free and recyclable polymer-based tapes for industrial and consumer use. As Germany transitions towards circular economy goals, demand for eco-compliant, precision-engineered film adhesives continues to rise across automotive, electronics, and manufacturing sectors.

Japan remains a technological frontrunner in the global double coated film tapes industry, supported by world-leading companies such as Nitto Denko, Lintec, and 3M Japan. The country’s dominance in advanced electronics and Flat Panel Display (FPD) manufacturing drives high-volume consumption of ultra-thin, high-transparency adhesive tapes like the LUCIACS™ series, designed for bonding smartphone displays, OLED panels, and compact electronic assemblies.

Japanese R&D efforts emphasize thermally conductive and solvent-free double coated film tapes that enhance heat dissipation in power electronics, LEDs, and server components, ensuring durability under demanding operating conditions. Furthermore, Japan is investing heavily in green adhesive technologies, with a growing number of companies transitioning to bio-based and solvent-free film tapes aligned with national carbon neutrality targets.

The continuous innovation in material science and adhesive chemistry reinforces Japan’s global leadership in precision-engineered electronic bonding films, ensuring strong market positioning in FPD assembly, semiconductor packaging, and renewable energy applications.

South Korea’s double coated film tapes market is expanding rapidly due to its dominance in display technology, semiconductor packaging, and EV battery manufacturing. The country’s leading electronics and materials firms are introducing foldable display tapes with advanced elasticity and high reworkability to support flexible and foldable OLED device production.

The nation’s semiconductor manufacturing boom, supported by the KRW 622 trillion Mega Cluster initiative, has amplified demand for ultra-low-outgassing double coated film tapes that meet the stringent cleanliness and dimensional stability standards required in wafer processing and cleanroom assembly. Meanwhile, the expansion of EV battery gigafactories across Korea has increased the use of thermal interface bonding tapes for battery module and cell adhesion, ensuring stability and efficient heat management.

As the government prioritizes next-generation materials for the electronics and mobility sectors, South Korea is becoming a global innovation center for adhesive films engineered for extreme reliability, heat resistance, and micro-level precision.

India’s double coated film tapes industry is gaining momentum as the nation undergoes rapid urban infrastructure expansion and a surge in automotive and packaging production. The government’s Smart Cities Mission and Bharatmala project are fueling the demand for durable adhesive tapes used in building envelope sealing, glazing, HVAC installation, and panel bonding, particularly suited to the country’s diverse climatic conditions.

The automotive sector, driven by the “Make in India” initiative and EV production incentives, increasingly utilizes high-tack double coated film tapes for non-structural bonding, wiring harness bundling, and lightweight component mounting. Simultaneously, the e-commerce packaging boom is strengthening demand for tamper-evident and high-speed splicing tapes used in logistics and high-volume packaging lines.

India’s growing domestic adhesive manufacturing ecosystem, coupled with foreign investments, positions the country as a fast-emerging hub for industrial-grade and consumer double coated film tapes tailored for high-demand applications in construction, automotive, and packaging sectors.

Double Coated Film Tapes Market Report Scope

Double Coated Film Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.1 Billion

|

|

Market Size (2034)

|

$1.6 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Film Backing Material (Polyethylene Terephthalate, Polypropylene, Polyvinyl Chloride, Polyethylene, Polyimide, Polyester), By Adhesive Type (Acrylic Tapes, Synthetic Rubber Tapes, Silicone Adhesives, Hydrocolloid Adhesives, Hybrid Formulations), By Liner Type (Paper/Glassine Liner, Plastic Liner, Film Liner, PCK Liner), By Thickness (Ultra-Thin Film Tapes, Thin, Standard, Thick), By Application Function (Structural Bonding, Optically Clear Adhesives, Thermal Management Tapes, EMI/RFI Shielding Tapes, Permanent Mounting, Temporary Fixation, Splicing Tapes), By End-Use Industry (Automotive, Electrical & Electronics, Building & Construction, Healthcare, Packaging, Appliance/White Goods Manufacturing, General Industrial Assembly

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Nitto Denko Corporation, tesa SE, Avery Dennison Corporation, Lohmann GmbH & Co. KG, Lintec Corporation, DIC Corporation, H.B. Fuller Company, Intertape Polymer Group Inc., Saint-Gobain S.A., Sika AG, Berry Global Inc., Coroplast Fritz Müller GmbH & Co. KG, Scapa Group plc, Adchem Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Film Backing Material

- Polyethylene Terephthalate

- Polypropylene

- Polyvinyl Chloride

- Polyethylene

- Polyimide

- Polyester

By Adhesive Type

- Acrylic Tapes

- Synthetic Rubber Tapes

- Silicone Adhesives

- Hydrocolloid Adhesives

- Hybrid Formulations

By Liner Type

- Paper/Glassine Liner

- Plastic Liner

- Film Liner

- PCK Liner

By Thickness

- Ultra-Thin Film Tapes

- Thin

- Standard

- Thick

By Application Function

- Structural Bonding

- Optically Clear Adhesives

- Thermal Management Tapes

- EMI/RFI Shielding Tapes

- Permanent Mounting

- Temporary Fixation

- Splicing Tapes

By End-Use Industry

- Automotive

- Electrical & Electronics

- Building & Construction

- Healthcare

- Packaging

- Appliance/White Goods Manufacturing

- General Industrial Assembly

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- 3M Company

- Nitto Denko Corporation

- tesa SE

- Avery Dennison Corporation

- Lohmann GmbH & Co. KG

- Lintec Corporation

- DIC Corporation

- H.B. Fuller Company

- Intertape Polymer Group Inc.

- Saint-Gobain S.A.

- Sika AG

- Berry Global Inc.

- Coroplast Fritz Müller GmbH & Co. KG

- Scapa Group plc

- Adchem Corporation

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Double Coated Film Tapes Market with analysis reviews that benchmark adhesion systems for LSE plastics, thin-film carrier precision, reworkability, thermal stability, and cleanroom compatibility. It highlights breakthroughs in solvent-free coating, bio-based carriers, optically clear display laminates, and EV-ready bonding solutions, connecting product performance to line throughput, die-cut convertibility, and total cost of ownership. The study maps competitive moves across electronics, automotive, construction, healthcare, and packaging, details regulatory trajectories (VOC/REACH), and quantifies demand linked to miniaturization, lightweighting, and automation. For sourcing, process, and R&D leaders, this report is an essential resource for specification setting, supplier shortlisting, and risk-aware investment planning.

Scope Highlights

Segmentation:

- By Film Backing Material: Polyethylene Terephthalate (PET); Polypropylene (PP); Polyvinyl Chloride (PVC); Polyethylene (PE); Polyimide (PI); Polyester.

- By Adhesive Type: Acrylic Tapes; Synthetic Rubber Tapes; Silicone Adhesives; Hydrocolloid Adhesives; Hybrid Formulations.

- By Liner Type: Paper/Glassine Liner; Plastic Liner; Film Liner; PCK Liner.

- By Thickness: Ultra-Thin Film Tapes; Thin; Standard; Thick.

- By Application Function: Structural Bonding; Optically Clear Adhesives (OCA); Thermal Management Tapes; EMI/RFI Shielding Tapes; Permanent Mounting; Temporary Fixation; Splicing Tapes.

- By End-Use Industry: Automotive; Electrical & Electronics; Building & Construction; Healthcare; Packaging; Appliance/White Goods Manufacturing; General Industrial Assembly.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecasts 2025–2034.

Companies: 15+ company profiles/analyses covering portfolios, capacity moves, sustainability roadmaps, and channel strategies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.