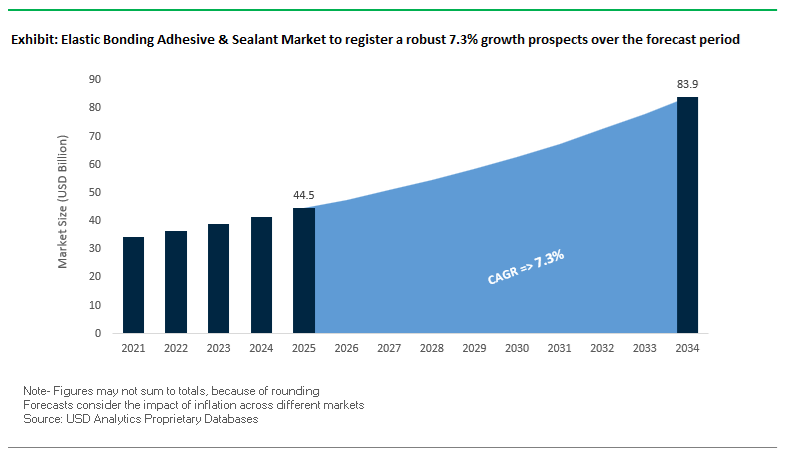

The Global Elastic Bonding Adhesive and Sealant Market is projected to rise from $44.5 billion in 2025 to $83.9 billion by 2034, registering a robust CAGR of 7.3%. Growth is driven by expanding applications in wind energy, EV assembly, and sustainable construction, where elastic bonding systems deliver high fatigue resistance, flexibility, and environmental compliance. As industries shift toward multi-material assembly and low-emission manufacturing, demand for next-generation polyurethane (PU), silane-modified polymer (SMP), and silicone-based bonding technologies is rapidly accelerating.

In renewable energy applications, particularly wind turbine manufacturing, elastic bonding adhesives are being engineered to withstand multi-axial fatigue loading with bond lines reaching up to 30 mm, enabling structural integrity in turbine blades under extreme stress. In construction, ultra-low modulus silicone elastomeric sealants—such as DOWSIL™ 790—are setting new performance benchmarks, providing unprimed adhesion to porous substrates and long-term resistance to environmental movement.

Regulatory developments like the EU REACH directive are reshaping polyurethane chemistry. Innovations such as Sika’s Purform® technology reduce monomeric diisocyanate content below 0.1%, ensuring worker safety compliance without sacrificing mechanical performance. The automotive industry continues to integrate elastic polyurethane adhesives to enable lightweight vehicle assembly, vibration damping, and thermal management—key for electric vehicle (EV) battery module production.

In addition, Mexico, Southeast Asia, and Central Europe are emerging as high-growth manufacturing zones, driven by nearshoring and demand from automotive, construction, and aerospace sectors. Elastic bonding solutions are being increasingly localized in these hubs to support agile, high-volume industrial assembly.

The elastic bonding adhesives and sealants industry is witnessing strong innovation momentum across mobility, construction, and renewable energy. Leading manufacturers are investing heavily in bio-based adhesives, high-strength silicones, and energy-efficient hot melts, reshaping both environmental and structural performance metrics.

In September 2025, Sonoco Products Company announced a $30 million production capacity expansion, adding 100 million units annually to reinforce its industrial adhesive and sealant supply for core customers. This aligns with the ongoing global push to stabilize supply chains through regionalized production. Meanwhile, in August 2025, Henkel AG & Co. KGaA unveiled bio-based LOCTITE engineered wood adhesives, reducing CO₂ emissions by over 60% compared to conventional chemistries—an important move in the growing mass timber construction market.

In July 2025, H.B. Fuller emphasized its sustainability-centric adhesive systems, targeting lower coat weights and reduced application temperatures to cut energy consumption in industrial lines. Dow Inc., in June 2025, introduced a high-design-strength silicone adhesive series tailored for EV battery packs, offering unmatched thermal cycling resistance and long-term stability under extreme load conditions.

Earlier, in May 2025, Sika AG completed a strategic acquisition in the Asia-Pacific region, expanding its expertise in hybrid polyurethane/silicone sealants for large infrastructure applications. Dow’s March 2025 launch of the Construction OnLine (COOL) platform further exemplifies industry digitalization, allowing engineers and architects to access real-time specifications for structural glazing sealants and facade systems.

Regulatory and material innovation continue to intersect. In January 2025, Henkel secured ISCC PLUS certification across multiple European sites, validating its bio-based and mass-balance PU formulations, while Sika’s December 2024 introduction of the SikaSeal® low-emission sealant range underscored the industry’s focus on healthy indoor air environments.

The demand for structural-grade hybrid polymers, particularly silane-terminated polymers (STP/MS Polymers), is transforming the industrial adhesives and sealants market. These advanced materials are replacing both rigid epoxy adhesives and traditional polyurethane sealants by offering exceptional elongation, tensile strength, and weatherability—qualities essential for bonding dissimilar materials in construction, transport, and manufacturing.

Technical data from leading manufacturers demonstrates that next-generation MS Polymer adhesives achieve elongation at break exceeding 380% while maintaining lap shear strength up to 8.6 MPa (1250 psi) in hybrid MS/Epoxy systems. The combination of high elasticity and structural integrity allows them to outperform conventional adhesives in high-stress environments involving thermal expansion, vibration, and dynamic loads.

R&D advancements are further enhancing their performance through bio-based additives. Incorporating lignin-derived molecular additives into MS Polymer sealants enhances UV and thermal stability, significantly extending the service life of façade systems and exterior assemblies. Additionally, two-component hybrid (2K MS/Epoxy) formulations deliver a rapid strength build-up exceeding 3 MPa within three hours, even without heating—making them ideal for high-throughput industrial assembly and prefabrication processes.

The tightening of global environmental and occupational safety regulations is catalyzing a decisive move toward low-VOC, solvent-free, and isocyanate-free adhesive technologies. The reformulation wave aligns with increasing consumer and industrial demand for products that meet indoor air quality (IAQ) and green building certifications such as LEED, EMICODE®, and Indoor Air Comfort Gold (IACG).

In North America, regulatory frameworks such as South Coast AQMD Rule 1168 are enforcing strict VOC limits, with certain adhesive categories capped at 250 grams per liter. Similarly, in the European Union, the EMICODE® EC1+ and French A+ VOC labeling standards mandate near-zero emission products. As a result, top manufacturers are reformulating their entire portfolios toward solvent-free and isocyanate-free chemistries, incorporating silane-modified and silyl-terminated polymers that deliver equivalent bonding performance with reduced health risks.

The industry-wide transition not only ensures regulatory compliance but also enhances worker safety and consumer health in enclosed spaces such as hospitals, schools, and residential complexes. The outcome is a new class of eco-friendly elastic adhesives and sealants that deliver exceptional durability, adhesion strength, and weather resistance while supporting global carbon reduction targets.

The Electric Vehicle (EV) revolution represents one of the most significant growth catalysts for the elastic bonding adhesive and sealant industry. As manufacturers scale up production of battery modules and enclosures, they require multi-functional adhesives that combine sealing, thermal management, and mechanical protection in a single material system.

Cutting-edge diisocyanate- and silicone-free thermal interface materials (TIMs) are emerging as integral components of EV battery assembly. These formulations are designed to provide high thermal conductivity, low pullout force, and easy removability—enabling efficient battery module repair, disassembly, and recycling, which are essential for building a circular EV ecosystem.

In addition, silyl-based sealant technologies are being optimized for battery pack case sealing, offering durable moisture barriers and long-term protection from contamination. These materials meet the thermal endurance, flame retardancy, and dielectric insulation requirements of modern EV safety standards. In large-scale EV manufacturing environments, these elastic adhesives not only improve production line throughput but also enhance vehicle reliability and safety across extended lifecycles.

The growing wave of urban infrastructure renewal is creating sustained demand for high-performance elastic bonding solutions tailored to building façade retrofits and window system refurbishments. With millions of post-war commercial and residential structures reaching obsolescence, the need for energy-efficient recladding and fenestration upgrades is fueling a lucrative aftermarket for advanced sealants and adhesives.

Technical assessments of aging high-rise buildings in Europe and Asia report that many existing sealant systems perform at Class 1 levels under EN 15651 standards—well below modern requirements for structural elasticity and durability. Consequently, engineers are specifying high-movement MS Polymer and polyurethane-based sealants that provide superior weatherability, UV stability, and adhesion longevity.

The aftermarket opportunity is amplified by the cost benefits of extended maintenance intervals. Field data confirm that re-cladding projects utilizing MS Polymer-based façade systems can extend the maintenance lifecycle by over a decade compared to conventional acrylic or polysulfide sealants. The results in lower operational costs, improved insulation performance, and enhanced façade aesthetics—making elastic bonding technology indispensable in the global drive toward sustainable building modernization.

Elastic Bonding Adhesive & Sealant Market Share Insights, 2025-2034

The one-component formulation segment holds the largest share of the global elastic bonding adhesive and sealant market, reflecting its unmatched convenience, reliability, and versatility. These systems—predominantly moisture-curing polyurethane (PU) and silicone-based adhesives and sealants—are widely adopted across construction, automotive, and general manufacturing sectors. Their single-package design eliminates the need for on-site mixing or ratio control, simplifying application and reducing labor time. This makes them the preferred choice for façade sealing, glazing, waterproofing, and flooring applications, where consistent performance and productivity are critical. Moreover, their ability to accommodate movement, resist UV and weathering, and bond diverse substrates (metal, concrete, plastic, and glass) reinforces their position as the global industry standard. Growing use in both professional and DIY/consumer markets, coupled with strong compliance to low-VOC and sustainable construction regulations, continues to strengthen this segment’s leadership. As global construction and infrastructure spending rise—particularly across Asia-Pacific and the Middle East—one-component elastic adhesives and sealants are expected to maintain their dominance due to their ease of application, environmental compliance, and long-term durability.

The two-component systems segment, though smaller in volume, represents the technological backbone of the high-performance elastic bonding industry. These formulations, typically based on epoxy, polyurethane, or hybrid reactive chemistries, are valued for their controlled curing behavior, superior mechanical strength, and faster cure times. They are indispensable in applications where structural integrity and precision curing are non-negotiable—such as automotive body assembly, wind turbine blade bonding, composite panel lamination, and heavy industrial assembly. Two-component systems allow for tailored mechanical properties, ensuring optimal elasticity, toughness, and chemical resistance even in extreme environmental conditions. As automation and advanced manufacturing processes expand globally, these adhesives are increasingly used in robotic dispensing and closed manufacturing environments, offering precise mixing and consistent performance. The shift toward lightweight structures, composite bonding, and modular industrial design—especially in transportation and renewable energy sectors—continues to fuel demand for high-strength, two-component elastic systems that deliver structural reliability without compromising flexibility.

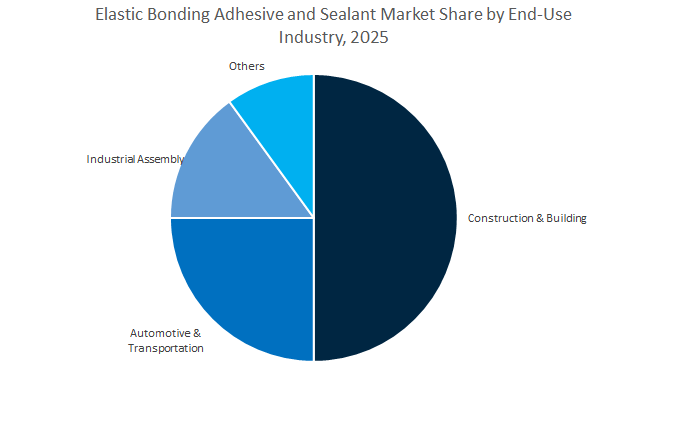

The construction and building segment remains the largest and most influential consumer of elastic bonding adhesives and sealants, accounting for nearly half of total market demand. These materials are essential for modern architecture and infrastructure projects, where long-lasting flexibility and environmental resilience are crucial. Applications such as structural glazing, curtain wall bonding, waterproofing, expansion joint sealing, and flooring systems depend on elastic adhesives to maintain integrity under dynamic stress and thermal movement. The surge in energy-efficient and green building initiatives—including LEED and BREEAM certifications—has further accelerated the adoption of low-VOC, solvent-free, and isocyanate-free elastic formulations. Additionally, the rapid expansion of urban housing, commercial complexes, and smart infrastructure in Asia-Pacific, coupled with ongoing renovation activity in North America and Europe, sustains robust global demand. As governments and developers emphasize sustainability, seismic performance, and longevity, elastic bonding products have become a cornerstone material category within the modern construction ecosystem.

The automotive and transportation industry is a major and rapidly evolving end-use sector for elastic bonding adhesives and sealants, driven by the industry-wide push toward lightweight vehicle design, electrification, and improved NVH (Noise, Vibration, and Harshness) performance. Elastic adhesives are replacing traditional mechanical fasteners and welds in critical applications like body panel bonding, direct glazing, seam sealing, and underbody protection, improving both performance and aesthetics. In electric vehicles (EVs), these materials are vital for battery module assembly, pack sealing, and structural integration, ensuring vibration damping, heat resistance, and moisture protection. The growing use of multi-material assemblies (aluminum, composites, glass, and plastics) in next-generation vehicles further amplifies the importance of flexible, high-strength bonding systems. As automotive OEMs shift toward modular manufacturing and automated assembly, reactive and hot melt elastic systems are gaining momentum due to their precision and durability. The segment’s innovation focus on lightweighting, noise reduction, and long-term performance will ensure continued growth for elastic bonding materials within the transportation value chain.

The global elastic bonding adhesive and sealant industry is dominated by multinational leaders—Henkel AG & Co. KGaA, Sika AG, Dow Inc., H.B. Fuller Company, Hexion Inc., and 3M Company—each leveraging chemistry innovation, vertical integration, and sustainability leadership to strengthen their competitive edge. These companies are converging on key growth areas: EV lightweighting, modular construction, renewable energy assembly, and VOC-free sealant technologies.

Henkel remains a global pioneer in polyurethane adhesives and industrial sealants, holding dominant positions across automotive, packaging, and electronics assembly. Its Teroson and LOCTITE brands define the benchmark for high-impact bonding and damping solutions, particularly in car manufacturing and flexible structural assembly. The company’s Adhesive Technologies division accounts for over half of global group revenues, illustrating its market influence. Henkel continues to advance solvent-free polyurethane formulations, aligning with tightening VOC and sustainability regulations worldwide.

Sika AG leads in construction and industrial bonding systems, with expertise in hybrid polyurethane and silicone technologies. Its Purform® platform represents a regulatory-compliant polyurethane generation with <0.1% monomeric diisocyanates, eliminating REACH training requirements. The SikaSeal® series delivers superior sag resistance for vertical facade joints, while Sika’s wind turbine adhesive systems manage multi-axial loading across thick bond lines. Sika’s full control over pre-polymer synthesis to formulation allows precision engineering for non-staining and non-cracking sealants, positioning it as a cornerstone brand in global infrastructure and renewable energy projects.

Dow Inc. continues to dominate the silicone elastomeric adhesive segment, particularly through its DOWSIL™ brand, which is integral to over 80% of China’s high-rise façade projects. The DOWSIL™ 3363 Insulating Glass Sealant is a top performer under hurricane-grade conditions, setting the standard in high-strength glazing adhesives. Dow’s carbon-neutral façade silicone program is an industry-first, underscoring its commitment to lifecycle sustainability. The company’s Building Science Connect platform enhances project design efficiency by providing digital adhesive selection and technical integration tools for architects and engineers.

H.B. Fuller excels in specialty adhesives and custom-engineered bonding solutions, catering to packaging, engineered wood, and consumer goods industries. Its Full-Care® and Swift® product lines target high-flexibility applications, while its low-temperature adhesive technologies contribute to energy savings and lower carbon output in production. The company actively invests in regional innovation centers, collaborating with OEMs to tailor elastic adhesive systems that improve processability and durability in industrial lines. H.B. Fuller’s focus on bio-based hot melts and circular packaging makes it a sustainability-driven market leader.

Hexion remains a key global supplier of epoxy and phenolic resin systems that form the foundation for flexible protective coatings and infrastructure adhesives. Its Versatic™ Monomer line enables ultra-high solids, waterborne resins catering to sustainable coating formulations. Hexion’s elastic epoxy resins are integral to marine, construction, and industrial corrosion-resistant coatings, where flexibility and toughness are critical. The company’s 12 facilities have been recognized under the American Chemistry Council’s Responsible Care® Awards, reinforcing its leadership in safety and environmental stewardship.

3M Company leads in tape-based bonding systems, with its VHB™ acrylic foam tapes replacing mechanical fasteners in transportation and aerospace assembly. These viscoelastic tapes provide superior stress dissipation and vibration damping while maintaining permanent elasticity under dynamic loads. In addition, 3M’s polyurethane and adhesive sealant range (e.g., Sealant 540 and 730 UV) offers high UV stability for outdoor applications. The firm continues to drive sustainability through its Pollution Prevention Pays (3P) initiative, while expanding into conductive and thermal adhesive systems for EV and electronic component assembly.

China continues to lead the Asia-Pacific elastic bonding adhesives and sealants market, primarily due to exponential growth in electric vehicle (EV) manufacturing and infrastructure construction. The 2022 launch of Dow’s VORATRON™ MA 8200S high-bonding adhesive has been pivotal in enhancing battery pack integrity, thermal stability, and lightweight assembly for top Chinese automakers such as SAIC, notably in its innovative “Magic Cube” battery system. The development supports structural integrity, vibration resistance, and extended life cycles, reinforcing Dow’s strategic positioning in the EV battery bonding segment.

China’s total battery cell manufacturing capacity for LFP and NMC chemistries increased by over 45% in 2023, driving parallel growth in elastic gap fillers, thermally conductive adhesives, and encapsulants. Moreover, Sika’s acquisition of Shenzhen Landun Holding further expanded its waterproofing and elastic sealant portfolio across China’s construction ecosystem. The rapid industrial expansion underscores China’s dominance in high-performance structural adhesives, EV thermal management adhesives, and advanced façade sealant bonding, supported by robust government-backed green infrastructure policies.

The United States remains a global innovation hub for eco-conscious elastic adhesives and sealants, driven by stringent VOC regulations, green building certifications, and expanding aerospace and industrial manufacturing sectors. Federal initiatives emphasizing energy-efficient and low-emission construction have led to a surge in waterborne and hot melt elastic adhesives, engineered to deliver superior bonding while complying with LEED and EPA standards.

In May 2024, H.B. Fuller acquired ND Industries and its Vibra-Tite brand, a move that strategically expanded its footprint in high-margin, high-growth industrial adhesives. Concurrently, Dow Inc. launched a water-borne silicone adhesive line in August 2025, designed for eco-conscious construction, offering rapid curing, high flexibility, and long-term bonding reliability. The advancements highlight the growing shift toward sustainable material transition and low-VOC waterborne adhesive systems that serve key North American industries, including aerospace, transportation, and commercial construction.

Germany: Europe’s Front-Runner in Bio-Based Polyurethane and Regulatory-Compliant Elastic Systems

Germany stands at the forefront of European elastic bonding adhesive innovation, particularly in bio-based polyurethane (PU) and silyl-terminated polymer (SMP) technologies. Pilot projects in mass-timber and Cross-Laminated Timber (CLT) construction employ second-generation bio-based polyurethane adhesives derived from soybean oil and castor beans, enabling primer-less adhesion to timber surfaces and contributing to sustainable elastic bonding. The innovations directly support Germany’s low-carbon infrastructure goals and circular economy strategy.

The German market is also undergoing a major regulatory transformation as the EU REACH diisocyanate regulations come into enforcement. The has accelerated the reformulation of polyurethane elastic adhesives and the rise of hybrid SMP adhesives, offering low-isocyanate alternatives with superior durability and environmental compliance. The transitions, supported by major chemical producers like Wacker Chemie and Henkel, are positioning Germany as the benchmark for sustainable adhesive chemistry in Europe’s automotive, construction, and renewable energy sectors.

Japan remains a technological leader in high-functionality elastic adhesives, leveraging its advanced R&D in hybrid polymer sealants and precision bonding technologies. In May 2025, the Japanese government implemented new regulations promoting eco-friendly and hybrid adhesive formulations, compelling manufacturers to comply with elevated safety, performance, and environmental standards. The regulatory clarity is accelerating product innovation across both construction and industrial manufacturing sectors.

The country’s robust automotive lightweighting initiatives continue to drive adoption of elastic structural adhesives engineered for bonding dissimilar materials such as carbon fiber, aluminum, and advanced composites. Japanese manufacturers are emphasizing energy-efficient, high-strength bonding that supports the shift toward next-generation electric and hybrid vehicles. The integration of The technologies into automotive assembly, aerospace, and rail underscores Japan’s precision-led approach to eco-sustainable, performance-driven adhesive innovation.

Switzerland continues to shape the global elastic adhesives and sealants landscape, largely through Sika AG’s market leadership and innovation. The company’s acquisition of Shenzhen Landun Holding has bolstered its dominance in Asia-Pacific’s waterproofing and construction sealant segments, enabling enhanced delivery of elastic roofing membranes and façade systems. The expansion exemplifies Sika’s strategy to strengthen its global presence and sustainable product ecosystem.

Technological advancements such as SikaForce thermal conductive adhesives and Sikagard fire-retardant coatings demonstrate the company’s pivotal role in e-mobility bonding, particularly for rail and electric bus applications, where thermal management and fire resistance are critical. The innovations align with Switzerland’s broader focus on sustainability and safety performance, ensuring long-term durability under extreme conditions. Through R&D and acquisitions, Switzerland solidifies its position as a center of excellence for high-performance, sustainable elastic bonding systems.

France plays a crucial role in the European elastic adhesive market, with the Arkema Group leading innovation in high-performance specialty chemicals for aerospace, automotive, and construction sectors. Arkema’s continued investment in advanced materials and sustainable polymer systems supports its global strategy for eco-resilient elastic bonding solutions that meet stringent aerospace durability and environmental standards.

French manufacturers are focusing on next-generation hybrid and solvent-free sealant systems designed to reduce VOC emissions while maintaining high mechanical flexibility and thermal resistance. The developments align with EU green manufacturing goals, positioning France as a pivotal hub for specialty elastic bonding adhesives that cater to premium industrial and architectural applications. The focus on advanced composites and lightweight assembly underscores France’s strategic influence in European adhesive technology ecosystems.

India’s elastic bonding adhesives and sealants industry is rapidly expanding, propelled by massive infrastructure investments and automotive sector modernization. Large-scale public initiatives such as the Smart Cities Mission and National Infrastructure Pipeline (NIP) are driving demand for high-durability construction sealants for façade glazing, HVAC sealing, and waterproofing in diverse climate conditions. The surge underscores India’s growing importance in the South Asia elastic sealants market.

Key multinational and domestic players are actively strengthening their presence. Dow’s collaboration with Glass Wall Systems brought advanced DOWSIL façade sealants to India’s skyscraper construction market, while Henkel Adhesive Technologies India expanded its automotive adhesive warehouse in Pune to serve OEMs with Just-in-Time (JIT) elastic supply systems. Local producers like Pidilite Industries are scaling up SMP and silicone-based elastic formulations to support both infrastructure and consumer product manufacturing. The diversification positions India as a critical hub for fast-setting, weather-resistant elastic adhesives.

Elastic Bonding Adhesive & Sealant Market Report Scope

Elastic Bonding Adhesive & Sealant Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$44.5 Billion

|

|

Market Size (2034)

|

$83.9 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Resin Type (Polyurethane, Silicone, Silyl-Modified Polymers, Others), By Product Type (One-Component, Two-Component, Hot Melt Systems), By End-Use Industry (Construction & Building, Automotive & Transportation, Industrial Assembly, Others

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, H.B. Fuller Company, Arkema Group, Dow Inc., Wacker Chemie AG, Huntsman Corporation, RPM International Inc., Avery Dennison Corporation, Illinois Tool Works Inc., Pidilite Industries Ltd., Jowat SE, DELO Industrial Adhesives, Toagosei Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type/Polymer Chemistry

- Polyurethane

- Silicone

- Silyl-Modified Polymers

- Others

By Product Type/Formulation

- One-Component

- Two-Component

- Hot Melt Systems

By End-Use Industry

- Construction & Building

- Automotive & Transportation

- Industrial Assembly

- Others

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- H.B. Fuller Company

- Arkema Group

- Dow Inc.

- Wacker Chemie AG

- Huntsman Corporation

- RPM International Inc.

- Avery Dennison Corporation

- Illinois Tool Works Inc.

- Pidilite Industries Ltd.

- Jowat SE

- DELO Industrial Adhesives

- Toagosei Group

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Elastic Bonding Adhesive and Sealant Market through a decision-focused lens on performance, compliance, and total cost-in-use across construction, transportation, renewable energy, and industrial assembly. It delivers analysis reviews spanning polymer innovations, application engineering, and supply-chain localization; highlights breakthroughs in REACH-compliant polyurethane platforms, hybrid MS/SMP systems, thermally stable silicones for EV battery integration, and high-movement façade weatherseals; and maps pricing, capacity, and specification trends to 2034. By synthesizing technology roadmaps with regulatory shifts and nearshoring dynamics, this report is an essential resource for materials strategists, R&D formulators, procurement leaders, converters, and OEM program managers seeking to de-risk sourcing, accelerate product qualification, and capture profitable niches in lightweighting and green construction.

Scope Highlights

Segmentation:

- By Resin Type/Polymer Chemistry: Polyurethane; Silicone; Silyl-Modified Polymers; Others.

- By Product Type/Formulation: One-Component; Two-Component; Hot Melt Systems.

- By End-Use Industry: Construction & Building; Automotive & Transportation; Industrial Assembly; Others.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecasts 2025–2034.

Companies: 15+ company analyses/profiles covering portfolios, pipeline innovations, sustainability pathways, and go-to-market strategies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.