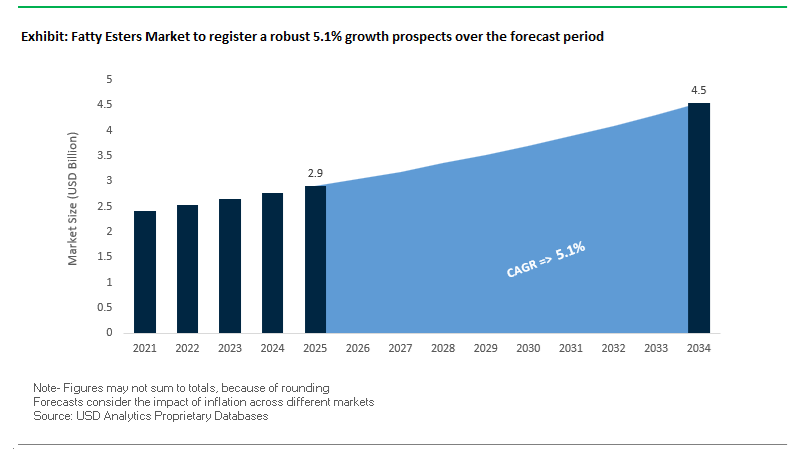

The Global Fatty Esters Market is projected to expand from USD 2.9 billion in 2025 to USD 4.5 billion by 2034, advancing at a CAGR of 5.1%, as fatty esters move decisively up the value chain from commodity oleochemicals to performance-defined, sustainability-qualified specialty ingredients. Demand growth is structurally anchored in bio-lubricants, personal care formulations, food emulsifiers, and surfactants, where OEMs and brand owners are actively replacing petrochemical derivatives with renewable, traceable alternatives. Leading oleochemical producers are aligning production assets with this shift by investing in enzymatic processing, advanced distillation, and feedstock traceability systems, allowing fatty esters to meet both functional specifications and tightening environmental disclosure requirements.

From a market-framing perspective, the critical change is not volume expansion but procurement behavior. Industrial buyers increasingly specify low-acid-value, high-purity esters to ensure formulation stability, oxidation resistance, and regulatory compliance across cosmetics, lubricants, and food-contact applications. This has pushed manufacturers to redesign refining stages and quality control protocols, particularly for esters derived from coconut, palm, soybean, and emerging waste-based feedstocks. The adoption of lipase-catalyzed esterification, deployed at commercial scale by multiple oleochemical and specialty ingredient producers, reflects a broader industry push toward lower energy intensity, higher conversion efficiency, and reduced byproduct formation, directly supporting corporate carbon-reduction targets without sacrificing output consistency.

Fatty esters used in Environmentally Acceptable Lubricants (EALs) increasingly require listing under frameworks such as LuSC, driving demand for polyol esters and diesters with verified biodegradability and aquatic safety profiles. In parallel, feedstock strategies are shifting rapidly toward RSPO-segregated or mass-balance certified palm derivatives, alongside used cooking oil (UCO)–based inputs, enabling producers to offer methyl esters and specialty esters with “low” or “ultra-low” carbon footprint classifications. As a result, fatty esters are no longer positioned merely as renewable substitutes, but as compliance-enabling chemical building blocks that directly influence downstream product approval, brand sustainability claims, and long-term supply chain resilience across personal care, lubricants, and food-grade applications.

The fatty esters industry is witnessing a wave of capacity expansions, bio-based innovation programs, and strategic partnerships to strengthen global production networks and sustainability credentials.

In September 2025, Croda International Plc announced a major expansion of its Super Refined™ facility in Leek, UK, to boost production of ultra-high-purity esters for biopharma applications, supporting the company’s growing role in drug delivery systems and specialty oleochemical derivatives. A few months earlier, in May 2025, Emery Oleochemicals showcased new ester base stocks for next-generation EV fluids at an industry conference, highlighting their technical superiority in thermal stability and biodegradability—two critical performance metrics in modern electric mobility fluids.

Bunge and Olleco’s joint venture, announced in June 2025, marked a major shift toward circular manufacturing. The partnership will manage the collection and reprocessing of used cooking oil (UCO) into feedstock for second-generation fatty esters, expanding renewable fuel and chemical production in Europe. Meanwhile, Mitsubishi Chemical Group’s March 2025 announcement of a new production line at its Kyushu Plant in Japan added 2,000 tons/year capacity for sugar ester emulsifiers, targeting surging demand in food-grade surfactants and beverages.

In August 2025, Emery Oleochemicals further strengthened its sustainability credentials by appointing a Global Sustainability Manager to accelerate ESG initiatives and expand its natural-based specialty esters portfolio, aligning operations with global decarbonization targets. Complementing this, Croda International launched a new pastillator facility (PS04) in Singapore in December 2024, increasing its solid-format fatty ester intermediates capacity by 4.6 kilotons, reinforcing Asia’s importance as a regional manufacturing hub.

Other notable developments include KLK OLEO’s establishment of an Indian subsidiary (Oct 2024) to deepen its presence in the South Asian oleochemical market, and Emery Oleochemicals’ launch of pelargonic acid-based green intermediates for high-stability saturated esters, underscoring the trend toward biobased and specialty ester production.

A major market-defining transformation is underway as leading oleochemical producers strategically transition away from palm oil–based raw materials toward diversified and deforestation-free feedstocks, including tallow, tropical oils, and secondary agricultural streams. The shift is propelled by tightening environmental regulations, global ESG mandates, and long-term supply chain resilience objectives.

In late 2024, a global oleochemical leader announced the expansion of its 100% bio-based portfolio to include pelargonic acid and specialty esters, signaling a decisive step toward non-palm, circular feedstocks. The strategy addresses consumer and regulatory concerns regarding palm-driven deforestation while ensuring certified traceability and renewable sourcing. The move drives a broader industry trend of prioritizing alternative lipid-based inputs such as waste tallow, coconut derivatives, and high-oleic tropical oils, ensuring consistent fatty acid availability for esterification processes.

The integration of enzymatic fat-splitting technology across European and Southeast Asian production facilities marks a significant sustainability leap. By replacing conventional high-pressure hydrolysis with biocatalytic processing, manufacturers report energy savings of up to 15%, while enabling the use of heterogeneous or low-grade feedstocks without compromising yield quality. The innovation aligns with global decarbonization targets and strengthens feedstock flexibility in volatile agricultural markets.

As Indonesia and Malaysia enforce moratoria on new palm plantations, the supply elasticity of lauric oils—including palm kernel and coconut oil—is tightening. With the combined production capacity plateauing over the past five years, ester producers are accelerating R&D into non-palm lipid routes, including microbial and algal oils, to safeguard long-term production scalability. The structural evolution reinforces the competitiveness of next-generation fatty ester derivatives for industrial, personal care, and lubricant markets.

As the electrification of mobility accelerates, the demand for high-stability, thermally conductive, and electrically insulating ester formulations is reshaping lubricant chemistry in EV powertrains, e-motors, and thermal management systems. Fatty esters are emerging as the preferred bio-lubricant base stocks for electric vehicle applications due to their dielectric stability, high viscosity index, and biodegradability.

At the 2025 STLE Annual Meeting, specialty chemical companies showcased new-generation synthetic esters engineered for direct-contact EV cooling fluids and high-speed e-motor lubrication. These materials deliver thermal conductivities exceeding 0.2 W/m·K and maintain electrical insulation across a wide voltage range, ensuring system safety under elevated load conditions. Their low volatility and oxidative stability make them ideal for EV inverter and transmission systems, where conventional mineral oils fail under electric field stress.

Research in EV transmission lubrication confirms that ester-based fluids maintain stable hydrodynamic film thickness even under high-speed, high-temperature conditions. The enables efficient friction reduction and heat dissipation in compact drivetrains. Esters’ inherent polarity ensures superior metal wetting and additive solubility, making them pivotal for long-drain, energy-efficient EV fluids.

Legacy chemical companies with oleochemical roots are repositioning their business toward EV fluid chemistry, leveraging their deep expertise in ester synthesis. Their focus on tallow- and vegetable-based bio-lubricant esters—noted for excellent friction and wear resistance in electric fields—has secured them premium market positioning as EV lubricant specialists. The segment’s anticipated CAGR of 8–10% through 2030 presents a high-margin opportunity for ester manufacturers capable of meeting e-mobility performance specifications.

Global regulatory reforms against persistent chemicals and microplastics are catalyzing the expansion of readily biodegradable surfactants derived from fatty ester chemistry, particularly in home care, detergents, and personal care applications. These renewable esters combine functional performance with rapid environmental degradation, aligning perfectly with eco-certification standards.

The European Union’s microplastic restriction under REACH and evolving wastewater discharge directives have elevated biodegradability as a key purchasing criterion. Studies confirm that sucrose laurate and fatty acid methyl esters (FAME)-based surfactants are classified as “readily biodegradable”, achieving near-complete degradation under aerobic conditions within days—far outperforming sulfonated synthetic surfactants.

With eco-labels like EU Ecolabel, Ecocert, and Nordic Swan influencing purchase decisions, leading consumer goods manufacturers are embedding fatty ester surfactants in their product formulations. These compounds, often derived from coconut and castor oils, exhibit excellent mildness, foaming, and wetting properties, driving their integration into green detergents, cosmetics, and baby care products.

The abundance of esterase enzymes in natural environments accelerates the biodegradation of ester-based surfactants. The enzymatic advantage allows for full mineralization into non-toxic by-products, enhancing regulatory compliance and consumer trust. The environmental advantage is expected to boost fatty ester surfactant demand by 40% in premium personal care by 2030.

The ongoing global phase-out of phthalate plasticizers in consumer and medical goods presents a transformative growth avenue for bio-based fatty ester plasticizers, especially in PVC, bioplastics, and flexible medical polymers. These sustainable alternatives meet regulatory safety standards while delivering mechanical and chemical properties superior to their petrochemical counterparts.

The European Chemicals Agency (ECHA) and the US Consumer Product Safety Commission (CPSC) have banned or restricted key ortho-phthalates such as DEHP and DBP in toys, medical tubing, and food-contact packaging. The regulatory vacuum has accelerated adoption of fatty ester–derived plasticizers like epoxidized fatty acid methyl esters (EFAME) and glyceryl esters, which are non-toxic, renewable, and compliant with REACH and FDA regulations.

Academic and industrial validation has shown that EFAME plasticizers offer superior migration resistance, thermal stability, and dielectric strength compared to DOP. When incorporated into biopolymer blends, they enhance flexibility and transparency while maintaining low extraction rates—an essential property for medical-grade and food-safe applications.

Patent literature highlights the growing focus on citrate and glyceryl ester plasticizers, which exhibit excellent compatibility with PVC and bio-PVC formulations. These plasticizers demonstrate enhanced solvent extraction resistance and aging stability, making them the preferred choice for bioplastic development and medical polymer engineering.

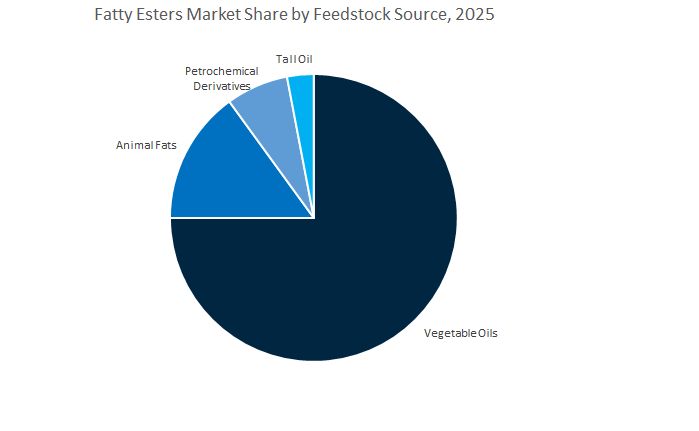

Fatty Esters Market Share Insights, 2025-2034

Vegetable oils dominate the global fatty esters industry, representing an estimated 72.1% share of total feedstock usage by 2025.

Their widespread availability, renewable origin, and diverse fatty acid composition make them the foundation of the global supply chain. Oils such as palm, soybean, rapeseed, and sunflower are key raw materials used for producing fatty acid methyl esters (FAME), fatty acid ethyl esters (FAEE), and complex esters, which serve as intermediates in personal care, lubricants, and food ingredients. The preference for vegetable oils aligns with global sustainability goals, as manufacturers increasingly transition toward bio-based and biodegradable alternatives to petrochemical-derived esters. Palm oil derivatives, in particular, offer a cost-effective and high-yield feedstock, giving developing markets in Southeast Asia and Latin America a competitive edge in global exports. Additionally, vegetable oil–based fatty esters are integral to the growth of green lubricants and low-toxicity surfactants, which are gaining regulatory support under environmental frameworks like REACH and EPA Safer Choice. The combination of cost-efficiency, renewable sourcing, and multifunctional performance has solidified vegetable oils as the undisputed leader in global fatty ester production.

While animal fats represent a smaller share of the market, they continue to serve important technical and industrial roles due to their distinctive fatty acid composition, particularly high saturated content. These fats are widely used in metalworking lubricants, bio-based fuels, and industrial greases, where oxidative stability and film strength are crucial. As industries adopt circular economy practices, the recovery of animal by-products from meat processing is gaining traction as a sustainable feedstock alternative, especially in Europe and North America. Tall oil—a by-product from kraft pulp and paper processing—is another renewable resource contributing to the fatty ester landscape. Its use in alkyd resins, coatings, and adhesives supports bio-based manufacturing initiatives while reducing waste from forest industries. Though smaller in scale, these feedstocks reinforce the diversification of raw material sourcing in the bio-lubricants and specialty chemicals sectors. Meanwhile, petrochemical-derived synthetic esters, while not renewable, remain indispensable for high-performance applications in aviation, electronics, and automotive lubricants, where thermal and oxidative stability far exceed natural alternatives.

The technical grade segment dominates the global fatty esters market, accounting for approximately 53.6% of total demand in 2025. This dominance stems from the extensive use of fatty esters as base fluids, plasticizers, and surfactants in a broad spectrum of industrial applications. Technical-grade esters derived from vegetable oils and animal fats are essential in metalworking fluids, automotive lubricants, agrochemical formulations, textile softeners, and polymer coatings. Their ability to provide lubricity, biodegradability, and film-forming properties has made them integral to industrial modernization and environmental compliance efforts. As sustainability regulations tighten globally, particularly in Europe and North America, industries are increasingly replacing mineral oil–based lubricants with bio-based ester formulations to meet biodegradability and toxicity standards. Additionally, the expansion of renewable diesel (biodiesel) production continues to boost demand for methyl esters, which are often classified within technical-grade use. The intersection of cost-efficiency, chemical flexibility, and environmental alignment positions this segment as the foundation of the global fatty ester supply chain.

The food-grade fatty esters segment holds a major share of the value-added market, underpinned by rising demand for emulsifiers, stabilizers, and texture modifiers in processed foods, baked goods, and dairy alternatives. Esters such as mono- and diglycerides (E471) are indispensable in maintaining the texture and shelf life of packaged foods while aligning with clean-label and plant-based product trends. The cosmetic-grade segment, on the other hand, is witnessing robust growth, fueled by the global boom in natural and sustainable personal care formulations. Fatty esters—such as isopropyl myristate, cetyl palmitate, and octyl stearate—serve as emollients, conditioners, and non-greasy carriers that enhance sensory appeal in lotions, creams, and makeup products. The preference for bio-based, non-irritating, and biodegradable ingredients has significantly increased the use of vegetable-derived esters in skincare and haircare lines, replacing synthetic silicones and petrochemical emollients.

The Global Fatty Esters Market is defined by a highly integrated network of multinational players combining oleochemical expertise, renewable feedstock sourcing, and advanced ester chemistry. Companies such as Croda International Plc, Emery Oleochemicals, KLK OLEO, and P&G Chemicals are leading the transformation by aligning product innovation with sustainability compliance, including RSPO, LuSC, and Net Zero frameworks.

Croda International Plc is a market leader in high-purity and functional fatty esters designed for personal care, healthcare, and biopharma applications. Its Super Refined™ technology platform delivers ultra-pure esters used in drug delivery and high-end cosmetics, ensuring superior stability and compatibility. With New and Protected Products (NPP) accounting for 35% of total sales in 2024, Croda demonstrates strong innovation throughput. The Zenakine™ active launch (September 2025) exemplifies how Croda integrates ester chemistry with biotechnology. The company also supports carbon footprint transparency by providing cradle-to-gate data for 2,000+ ingredients.

Emery Oleochemicals stands out for its natural-based specialty esters under the DEHYLUB® brand, catering to bio-lubricants, EV fluids, and metalworking applications. The company’s Cincinnati facility achieved ISO 50001 certification (June 2025), emphasizing energy efficiency and operational sustainability. Emery’s Green Polymer Additives division leverages LOXIOL® ester technology for advanced 3D printing filaments and binders, broadening the scope of ester applications. Many Emery products are LuSC-listed and NSF HX-1 certified, aligning with EAL and incidental food-contact regulations.

KLK OLEO leverages a fully integrated supply chain from palm plantations to downstream ester production, ensuring traceability and feedstock reliability. Its vast portfolio includes methyl esters, glycerine, surfactants, and bioactives, serving industries from home care to lubricants. Operating 16 global facilities across Asia and Europe, the company distributes to over 120 countries. In October 2024, KLK OLEO launched KLK OLEO India Pvt. Ltd., enhancing its reach across South Asia. Its strategic roadmap centers on bio-based polymer intermediates and bioplastics, reinforcing the role of fatty esters as precursors to renewable materials.

P&G Chemicals is a key global supplier of methyl esters, fatty alcohols, and fatty acids, essential precursors for fatty ester synthesis. The company’s “Ultra-Low” and “Low” carbon footprint variants enable carbon-neutral lubricant and agrochemical formulations, addressing Scope 3 emission reduction goals for downstream manufacturers. Its products are RSPO, Kosher, and Halal certified, ensuring ethical and traceable sourcing. P&G’s oleochemical building blocks are extensively used in pharmaceutical excipients, lubricant base oils, and food emulsifiers, maintaining its reputation as a high-volume, quality-driven feedstock provider.

The United States fatty esters market is undergoing rapid transformation, led by a strong emphasis on bio-based innovation, renewable fuel integration, and advanced chemical R&D. Consumer preference for natural and sustainable ingredients in personal care and cosmetics has significantly boosted the demand for non-toxic, plant-derived fatty esters as emollients, conditioners, and dispersing agents. The trend aligns with the U.S. chemical industry’s broader shift toward sustainable personal care solutions utilizing biodegradable fatty esters and non-petroleum feedstocks.

In the renewable energy domain, the adoption of Fatty Acid Methyl Esters (FAME) as a core component in biodiesel production continues to grow, supported by federal and state-level decarbonization mandates. North America’s rising biofuel infrastructure and sustainability awareness are positioning the U.S. as a leading hub for renewable energy biodiesel innovation. Concurrently, R&D facilities across major states are investing in high-performance synthetic esters and polyol esters used in pharmaceutical formulations, high-temperature lubricants, and specialty coatings. The developments reinforce the U.S. role as a technological leader in the bio-based fatty esters industry, bridging sustainable chemistry with next-generation industrial applications.

Germany stands at the forefront of Europe’s sustainable fatty esters and bio-lubricants market, supported by stringent environmental legislation and a national focus on renewable material substitution. The country’s shift toward bio-lubricant base oils—derived from vegetable oil feedstocks—has been accelerated by both industrial policy and consumer demand for environmentally responsible products. Major chemical producers are adopting advanced synthetic polyol ester technologies that deliver high oxidative stability and biodegradability for aviation, automotive, and industrial lubrication applications.

A defining example of German innovation is OQ Chemicals’ November 2024 launch of OxReduce L7-NPG, a bio-circular synthetic lubricant base oil developed to replace fossil-derived alternatives. The product highlights the transition toward closed-loop carbon-neutral lubricants within the fatty esters value chain. Moreover, compliance with the EU Ecolabel and LuSC (Lubricant Substance Classification List) has become a key driver for manufacturers seeking to align with European Green Deal goals. Supported by initiatives under Germany’s High-Tech Strategy 2025, domestic R&D efforts are increasingly geared toward EU Ecolabel-compliant esters and bio-circular lubricants, securing Germany’s position as the European innovation hub for sustainable fatty ester chemistry.

China remains the world’s largest producer and consumer of fatty esters, underpinned by extensive oleochemical infrastructure expansion and a robust focus on renewable energy and sustainable materials. In July 2024, KLK Oleo announced the expansion of its Zhangjiagang oleochemicals processing capacity to 500,000 tons per year, reflecting China’s growing role in the Asia-Pacific surfactants and specialty chemicals markets. The investment underscores the country’s long-term strategy to achieve vertical integration in fatty acid, alcohol, and ester production, enhancing supply chain efficiency and export competitiveness.

Parallel to its manufacturing growth, China’s clean energy transition is creating significant opportunities for palm-based methyl esters (FAME) in biodiesel blending. As the nation intensifies efforts to reduce carbon emissions, biodiesel adoption is becoming a critical pathway for the renewable fuel policy. Additionally, the expanding personal care and home care industries are driving demand for vegetable-based and natural fatty esters, particularly in cosmetics, detergents, and textile softeners. With policies aligning toward sustainability, China’s oleochemical and specialty fatty ester segments are poised for sustained growth in eco-friendly surfactants and green energy applications.

India’s fatty esters industry is entering a high-growth phase, driven by specialty chemical investments, expanding industrial applications, and government-led incentives. Jubilant Ingrevia Limited has significantly enhanced domestic ester production by commissioning a new high-value esters facility within its Diketene derivatives platform, adding approximately 2,000 TPA of specialty capacity. The marks a major step in the company’s diversification toward high-value specialty chemicals that cater to global pharmaceutical, agrochemical, and personal care markets.

In parallel, Klüber Lubrication’s EUR 15.6 million investment in its Mysore facility (May 2024) underscores India’s strengthening position in synthetic lubricant manufacturing, where fatty acid esters are integral to high-performance formulations. Government policies like the Production Linked Incentive (PLI) scheme and the Petroleum, Chemicals, and Petrochemicals Investment Region (PCPIR) policy continue to attract foreign investment and encourage R&D in sustainable chemical synthesis. As industrial demand and infrastructure scale up, India is quickly becoming a strategic manufacturing hub for bio-based fatty esters, synthetic lubricants, and specialty ester derivatives in the Asia-Pacific region.

Indonesia plays a pivotal role in the global fatty acid methyl esters (FAME) market, thanks to its extensive palm oil resources and strong renewable fuel policies. The government’s B40 biodiesel mandate, scheduled for gradual implementation beginning January 2025, aims to increase the mandatory palm oil content in biodiesel from 35% to 40%, positioning Indonesia as a leading producer of renewable palm-based fatty esters. The mandate directly drives capacity expansion for oleochemical and biodiesel producers, while simultaneously influencing global pricing dynamics in the renewable fuel and fatty esters value chain.

The country’s commitment to sustainable palm oil certification (RSPO) and downstream industrial investment is accelerating the transition from crude palm oil exports to high-value fatty ester and fatty alcohol derivatives. New processing plants focused on value-added oleochemicals ensure greater domestic retention of economic benefits while supporting international sustainability compliance. With its combination of policy-driven biodiesel expansion and industrial modernization, Indonesia is solidifying its status as a global hub for palm-based fatty esters and renewable oleochemicals.

South Korea’s fatty esters industry is distinguished by its technological sophistication and focus on high-performance specialty esters for advanced materials, coatings, and electronic applications. Major domestic producers such as Kukdo Chemical Co. Ltd. are developing high-purity fatty esters with exceptional thermal conductivity, dielectric stability, and surface performance, tailored for semiconductors, electronic fluids, and polymer coatings. The R&D efforts are supported by strong government initiatives in advanced material science, ensuring supply chain resilience and reducing dependence on imported intermediates.

The South Korean government continues to fund next-generation fatty ester research programs linked to lithium-ion battery components, coating formulations, and electronics encapsulants, reflecting the country’s strategic positioning in global supply chains. Additionally, industry collaborations between chemical conglomerates and research institutions are driving innovation in fatty acid-derived emollients and surfactants used in premium personal care and home care products. With a strong foundation in electronics-grade esters and advanced coatings, South Korea remains a vital player in the high-value specialty esters segment within the global fatty esters market.

Fatty Esters Market Report Scope

Fatty Esters Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.9 Billion

|

|

Market Size (2034)

|

$4.5 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Type (Glyceryl Esters, Polyol Esters, Fatty Acid Methyl Esters, Sucrose Esters, Isopropyl Esters, Glycol Esters, Phosphate Esters), By Application (Personal Care & Cosmetics, Lubricants, Food & Beverages, Surfactants & Detergents, Pharmaceuticals, Others), By Feedstock Source (Vegetable Oils, Animal Fats, Tall Oil, Petrochemical Derivatives), By Grade (Technical Grade, Food Grade, Pharmaceutical Grade, Cosmetic Grade

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

KLK Oleo, Evonik Industries AG, BASF SE, Cargill Incorporated, Wilmar International Ltd., DuPont, Emery Oleochemicals, Fine Organics, Oleon NV, Stepan Company, P&G Chemicals, Jubilant Ingrevia Limited, Arkema, Klüber Lubrication, Perstorp Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Type

- Glyceryl Esters

- Polyol Esters

- Fatty Acid Methyl Esters

- Sucrose Esters

- Isopropyl Esters

- Glycol Esters

- Phosphate Esters

By Application

- Personal Care & Cosmetics

- Lubricants

- Food & Beverages

- Surfactants & Detergents

- Pharmaceuticals

- Others

By Feedstock Source

- Vegetable Oils

- Animal Fats

- Tall Oil

- Petrochemical Derivatives

By Grade

- Technical Grade

- Food Grade

- Pharmaceutical Grade

- Cosmetic Grade

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- KLK Oleo

- Evonik Industries AG

- BASF SE

- Cargill Incorporated

- Wilmar International Ltd.

- DuPont

- Emery Oleochemicals

- Fine Organics

- Oleon NV

- Stepan Company

- P&G Chemicals

- Jubilant Ingrevia Limited

- Arkema

- Klüber Lubrication

- Perstorp Group

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Fatty Esters Market with a practitioner-first lens—linking process chemistry (esterification/transesterification, enzymatic catalysis), quality specs (acid value, iodine value, oxidation stability), and end-use performance (lubricity, sensory profile, biodegradability) to cost-in-use and compliance outcomes. It delivers analysis reviews of innovation pipelines and feedstock strategies, highlights breakthroughs in lipase-catalyzed, low-energy manufacturing, ultra-high-purity grades for life sciences, and next-gen ester base stocks for EV fluids, while mapping certification pathways (RSPO, LuSC/EAL) and carbon-intensity reporting. Integrating capacity moves, M&A, and regional policy drivers into dynamic market sizing and risk dashboards, this report is an essential resource for R&D leaders, sourcing and sustainability teams, and strategy executives who need decision-grade clarity on specialty versus commodity ester plays, resilience to feedstock volatility, and roadmaps for premiumization and decarbonization across lubricants, personal care, food, and surfactants.

Scope Highlights

Segmentation:

- By Type: Glyceryl Esters; Polyol Esters; Fatty Acid Methyl Esters; Sucrose Esters; Isopropyl Esters; Glycol Esters; Phosphate Esters.

- By Application: Personal Care & Cosmetics; Lubricants; Food & Beverages; Surfactants & Detergents; Pharmaceuticals; Others.

- By Feedstock Source: Vegetable Oils; Animal Fats; Tall Oil; Petrochemical Derivatives.

- By Grade: Technical; Food; Pharmaceutical; Cosmetic.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

Companies: 15+ company analysis/profiles covering strategies, portfolios, certifications, sustainability targets, and recent developments.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.