Market Overview: Transition Toward Sustainable and High-Performance Adhesive Technologies

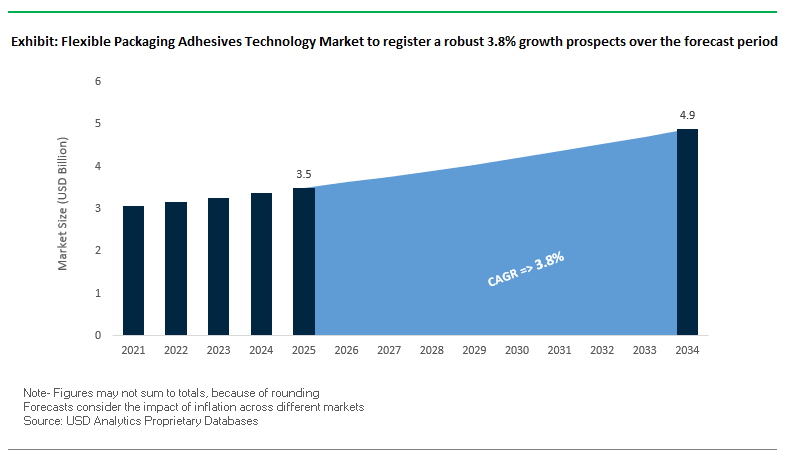

The Global Flexible Packaging Adhesives Technology Market is projected to expand from USD 3.5 billion in 2025 to USD 4.9 billion by 2034, growing at a CAGR of 3.8%. This industry plays a critical role in enabling lightweight, durable, and protective flexible packaging formats used across food, beverages, personal care, healthcare, and e-commerce applications. Adhesives technology ensures strong and reliable bonding of films, foils, and paper substrates, making it indispensable for high-performance packaging solutions.

The market is rapidly transitioning toward eco-friendly adhesive formulations, particularly water-based and solvent-free adhesives, as governments enforce stricter VOC regulations and brands prioritize sustainability goals. At the same time, the demand for laminating adhesives for retort pouches and barrier packaging continues to accelerate, driven by food safety requirements and the need to extend shelf life for convenience foods.

A key focus is the development of adhesives compatible with mono-material packaging structures, which enable recyclability while maintaining performance. Adhesive suppliers are investing heavily in bio-based, compostable, and solvent-free formulations to align with circular economy principles. Additionally, the boom in e-commerce and omnichannel distribution is creating demand for adhesives that can withstand vibration, humidity, and temperature fluctuations throughout global supply chains.

Key Insights for Industry Professionals:

- Market value rising from USD 3.5B (2025) → USD 4.9B (2034), CAGR 3.8%.

- Water-based and solvent-free adhesives are leading sustainability-driven growth.

- Retort pouches and food-grade laminations remain a major application driver.

- Mono-material compatibility is essential for recyclable packaging innovations.

- E-commerce logistics fueling adoption of fast-curing, high-tack adhesives.

Market Analysis: Recent Developments in Flexible Packaging Adhesives Technology

The Flexible Packaging Adhesives Technology Industry is highly dynamic, with innovation, partnerships, and consolidation reshaping its competitive environment.

In September 2025, Henkel Adhesive Technologies announced new recyclable and CO₂-reducing adhesive solutions at the FACHPACK 2025 exhibition, emphasizing the push toward sustainability. Earlier in July 2025, Henkel also launched Loctite Liofol LA 7837/LA 6265, a solvent-free adhesive system designed specifically for retort packaging, which combines high barrier performance with eco-friendly attributes.

The competitive landscape was further transformed in July 2025 when the Amcor–Berry Global merger closed, creating a packaging giant with greater leverage in flexibles, laminations, and sustainable innovation. Similarly, in April 2025, the Smurfit Kappa–WestRock merger reshaped the paper-based packaging market, indirectly boosting adhesives demand for fiber-based flexible formats.

Bostik (Arkema Group) has been at the center of expansion activities. In March 2025, it invested USD 27 million in its Middleton, MA plant to increase polyester production capacity, ensuring reliability and sustainability. Earlier, in December 2024, Bostik finalized the acquisition of Dow’s flexible packaging adhesives business, significantly strengthening its market position. In September 2024, Bostik partnered with Dow and Nordson to introduce Kizen™ LIME, a bio-based hot melt adhesive made from renewable materials for FMCG end-of-line packaging.

However, challenges persist. A report from August 2024 revealed that rising raw material costs linked to petrochemical volatility reduced adhesive production capacity by around 6%, emphasizing the importance of procurement optimization and supply chain resilience.

Cutting-Edge Trends and Strategic Opportunities Driving the Flexible Packaging Adhesives Technology Market

Commercialization of Non-Isocyanate Polyurethane (NIPU) Adhesives

The flexible packaging adhesives technology market is undergoing a significant technological transformation with the adoption of non-isocyanate polyurethane (NIPU) adhesives. Unlike conventional polyurethane adhesives, which rely on highly toxic isocyanate chemistry, NIPU alternatives enhance worker safety and reduce the risk of chemical migration into food products while maintaining superior bonding strength and flexibility. This trend is propelled by stringent regulatory pressures and increasing brand owner demands for safe, high-performance adhesives. Research into tannin-based NIPU adhesives, leveraging industrial wood waste, exemplifies industry efforts to combine safety, sustainability, and high performance. The commercialization of NIPU adhesives not only mitigates health risks but also streamlines production processes by reducing curing time, creating a high-value growth avenue in the global market. Moreover, this trend is reshaping the supply chain, demanding closer collaboration among raw material suppliers, adhesive manufacturers, and packaging converters to deliver seamless, compliant solutions.

Development of Recycling-Compatible Functional Adhesives

Adhesive technology in flexible packaging is evolving from a passive bonding agent to an active, recycling-compatible component. The focus is on adhesives that support both mechanical and advanced recycling processes, either by breaking down cleanly, avoiding contamination of polymer streams, or enhancing barrier properties in mono-material structures. Companies like Henkel and Bostik have developed adhesive lines recognized by RecyClass for compatibility with polyethylene (PE) recycling streams, demonstrating the growing industry commitment to sustainability. This trend addresses the critical need for high-quality recycling and strengthens the circular economy for flexible packaging. Adhesives engineered for recycling compatibility provide a significant growth opportunity, especially in the food and beverage sector, where brands are under pressure to meet sustainability targets without compromising product performance. The shift is fundamentally transforming the value chain, necessitating integrated collaboration among suppliers, manufacturers, and converters to achieve seamless, eco-friendly solutions.

Bio-Based Adhesives Derived from Non-Food Competing Feedstocks

A major opportunity in the flexible packaging adhesives technology market lies in the development of bio-based adhesives sourced from second-generation feedstocks, such as agricultural residues or industrial side streams like lignin from biofuel production. These adhesives offer a sustainable, non-food-competing alternative to petroleum-based products while enhancing lifecycle performance. Research demonstrates that lignin- and crop-residue-derived adhesives can improve mechanical properties, reduce curing temperatures, and provide a credible path for carbon reduction. Companies actively investing in this technology are creating functional, eco-friendly adhesives that appeal to environmentally conscious brands and consumers, offering a compelling value proposition. The adoption of bio-based adhesives fosters new cross-industry collaborations and strengthens the end-to-end circularity of the supply chain, positioning manufacturers as leaders in sustainable innovation.

UV-Curable and Electron-Beam (EB) Adhesive Technologies for Sustainable Manufacturing

UV and EB-curable adhesives present a transformative opportunity for sustainable, high-efficiency manufacturing. These 100% solid systems cure instantly under light or electron beams, eliminating solvents and VOC emissions while reducing energy consumption by removing large drying ovens. They also enable faster production speeds, thinner adhesive layers, and lightweight packaging solutions, contributing to material efficiency. This technology is highly relevant for direct-to-consumer (D2C) and short-run packaging, providing just-in-time production capabilities while minimizing waste. Widespread adoption, exemplified by HP’s global flexible packaging presses, underscores the commercial potential of UV/EB-curable adhesives. The combination of sustainability, efficiency, and performance makes this a high-value growth avenue, enabling brands and manufacturers to meet environmental regulations, improve worker safety, and accelerate time-to-market for new products.

Competitive Landscape: Strategies of Leading Flexible Packaging Adhesive Players

The Global Flexible Packaging Adhesives Technology Market is led by multinational players who combine material science, sustainability initiatives, and acquisitions to strengthen their positions.

Henkel AG & Co. KGaA focuses on solvent-free adhesive systems

Henkel is a global leader in adhesives, known for its Loctite® brand and broad portfolio covering water-based, solvent-based, and polyurethane adhesives. In July 2025, it launched Loctite Liofol LA 7837/LA 6265, a solvent-free system for retort packaging. Henkel’s Packaging RecycLab supports recyclability testing, reinforcing its strategy of sustainability, VOC reduction, and innovation-driven growth.

H.B. Fuller enhances recyclable and compostable adhesives portfolio

H.B. Fuller leverages its Flextra® brand to supply solvent-free and solvent-based laminating adhesives, many of which are RecyClass-approved. The company is investing in compostable adhesive solutions that decompose fully without leaving microplastics or toxins. Its strategic focus is growth through innovation and acquisitions, providing tailored solutions for packaging, automotive, and electronics markets.

Arkema (Bostik) strengthens position through acquisitions and bio-based innovation

Arkema, via its subsidiary Bostik, significantly expanded in December 2024 by acquiring Dow’s flexible packaging adhesives unit. In March 2025, Bostik invested USD 27M to expand polyester adhesive capacity. Its Kizen™ LIME hot melt adhesive, developed with Dow and Nordson, uses 80% renewable ingredients, showcasing Arkema’s leadership in bio-based, solvent-free adhesives.

The Dow Chemical Company pivots toward circular economy materials

Dow continues to focus on materials science and partnerships. Although it divested its adhesives business to Arkema in December 2024, Dow remains active through polyolefin elastomers for mono-material structures and collaborations like the September 2024 Kizen™ LIME project. Its strategy emphasizes innovation in recyclable packaging, advanced materials, and electronics-focused adhesives.

3M Company applies material science expertise to packaging adhesives

3M brings its expertise in pressure-sensitive adhesive films and transfer tapes to the packaging sector. While not a dominant laminating adhesives player, its OCAs (optically clear adhesives) for electronics demonstrate its cross-industry innovation. 3M’s focus is on sustainable design, advanced electronics, and niche high-performance bonding applications within the packaging industry.

Flexible Packaging Adhesives Technology Market Share Insights

Solvent-less Technology Leads Market Share by Adhesive Technology

In 2025, solvent-less adhesives dominate the flexible packaging adhesives technology market with a 40% share, reflecting the industry’s shift toward high-speed, sustainable solutions that eliminate volatile organic compounds (VOCs). Their ability to support rapid lamination without the need for energy-intensive drying ovens makes them the preferred choice for large-scale food and beverage packaging. Water-based adhesives follow with 25% share, benefitting from their eco-friendly and safer profile, though limited by slower processing and lower resistance. Solvent-based systems, once industry mainstays, are gradually losing ground due to VOC regulations and higher energy costs, yet they remain vital in applications requiring extreme chemical and heat resistance, particularly in industrial and pharmaceutical packaging. Meanwhile, hot-melt and other adhesive types retain niche roles, valued for instant setting and specific applications such as case sealing and technical laminates. Collectively, the adhesive technology landscape reflects a clear transition toward sustainability and compliance, with solvent-less leading innovation and solvent-based holding a defensive but critical niche.

Food and Beverage Packaging Dominates Adhesives Market Share by Application

The food and beverage sector holds a commanding 65% share of adhesive demand, positioning it as the undisputed growth engine of the flexible packaging adhesives industry. Driven by rising global demand for packaged snacks, ready-to-eat meals, and beverages, this segment requires advanced multi-layer laminates with excellent barrier properties to preserve freshness, extend shelf life, and meet stringent food safety regulations. Solvent-less adhesives are particularly favored due to their compatibility with food-contact requirements and ability to support high-volume production. In contrast, personal care and pharmaceutical applications, though smaller in scale, are high-value segments demanding tailored adhesives with superior resistance to oils, fragrances, and pharmaceutical-grade purity standards set by the FDA and EMA. Industrial packaging adds another layer of complexity, requiring extreme durability for chemicals, fertilizers, and paints, where solvent-based systems remain relevant despite sustainability concerns. This segmentation highlights how food and beverages anchor volume growth, while pharmaceuticals, personal care, and industrial packaging shape innovation in performance-specific adhesives.

United States Flexible Packaging Adhesives Market Accelerated by Low-VOC Innovations and Sustainability Trends

The U.S. flexible packaging adhesives technology market is navigating a fragmented regulatory landscape, with new EPA regulations targeting reductions in volatile organic compound (VOC) emissions. This shift has accelerated the adoption of water-based and other low-VOC adhesive technologies, driving innovation across the industry. Recent developments include solvent-free, aliphatic adhesive systems tailored for high-thermal stress applications, such as retort packaging. In September 2025, Advanced Flexible Packaging Solutions launched a new adhesive specifically for medical applications, offering superior bonding while maintaining biocompatibility.

Corporate investments are bolstering market growth, with Sonoco Products Co. committing $30 million to expand sustainable adhesive packaging production by 100 million units, focusing on flexible formats for the food industry. Key applications include food and beverage, pharmaceutical, and e-commerce sectors, driven by rising demand for lightweight, convenient packaging and tamper-evident seals. Sustainability remains central, with eco-friendly materials, bio-based polymers, and circular solutions—like Avery Dennison’s recyclable RFID labels—enhancing the environmental footprint of flexible packaging adhesives.

Germany Flexible Packaging Adhesives Market Shaped by Circular Economy Leadership and Regulatory Compliance

Germany’s flexible packaging adhesives technology market operates under strict European Union regulations, including the Packaging and Packaging Waste Regulation (PPWR), which mandates reduced packaging waste through reuse and recycling while phasing out chemicals such as PFAS. Technological innovations, such as machinery capable of handling sustainable materials and digital product passports, are enabling better material transparency and recycling efficiency.

Germany’s Extended Producer Responsibility (EPR) system encourages companies to design adhesives and packaging that are easier to recycle through modulated fees. Strategic partnerships between film producers and brand owners are fostering high-performance, customized flexible packaging solutions. Key applications include the food, beverage, and personal care sectors, where premium adhesives and high-barrier films enhance shelf life while meeting consumer expectations for sustainable, high-quality packaging.

China Flexible Packaging Adhesives Market Expanded by Green Policies and Domestic Manufacturing Initiatives

China’s flexible packaging adhesives technology market is strongly influenced by the government’s “dual carbon” goal and the March 2024 Action Plan for Large-Scale Equipment Updates and Consumer Goods Replacement, which promote recycling and sustainable materials adoption. Regulatory reforms, including the National Food Safety Standard for Adhesives in Food Contact Materials (GB 4806.15-2024), enforce strict migration limits to ensure food safety.

Technological advancements, including AI, 5G-enabled industrial internet integration, and automation, are improving production efficiency and flexible manufacturing capacity. A domestic focus on substituting imported technology is driving local production expansion. The market’s growth is fueled by rapid e-commerce, automotive, and electronics sectors, with high-volume demand for packaging and digital printing applications for high-end cosmetics and electronic product boxes.

India Flexible Packaging Adhesives Market Driven by Circular Economy Initiatives and Local Manufacturing Growth

India’s flexible packaging adhesives market is benefiting from government initiatives promoting a circular economy, including the Food Safety and Standards (Packaging) Regulations, 2018, which mandate food-grade material usage while prohibiting recycled plastics for food contact. Technological adoption is rising, with companies developing automated and solvent-free solutions. Brilliant Polymers achieved 72% solvent-free sales in 2025 and introduced five new solvent-free adhesive innovations for foil lamination and bulk packaging.

Corporate investments are strengthening market capacity, with UFlex operating over 100,000 TPA and investing in four R&D laboratories approved by the Ministry of Industries. Key applications include the food and beverage and personal care sectors, driven by growing e-commerce and the shift toward sustainable solutions. The “Make in India” initiative further encourages domestic production and technological development, reinforcing India’s role as a major player in flexible packaging adhesives.

Japan Flexible Packaging Adhesives Market Leading with Advanced High-Performance Films and Circularity Initiatives

Japan’s flexible packaging adhesives technology market leverages advanced precision manufacturing and sustainability-focused innovations. In September 2024, Toppan Inc., in collaboration with RM Tohcello Co. Ltd. and Mitsui Chemicals Inc., developed recycled BOPP film suitable for flexible packaging adhesives, exemplifying a push toward circularity. Regulatory guidance under the Plastic Resource Circulation Act (April 2022) promotes environmental design and reduces single-use plastics, targeting 2 million tonnes per year of bio-based plastics by 2030, influencing adhesives for these materials.

High-performance films with superior barrier properties, IoT-enabled tracking, and digital printing for sensor placement are transforming functionality in flexible packaging adhesives. Innovations such as easy-open tear notches and resealable closures cater to aging populations and single-person households, enhancing usability. Strategic mergers and acquisitions, like Sika AG’s acquisition of Hamatite from Yokohama Rubber Co., have strengthened market capabilities, particularly in automotive and construction segments, solidifying Japan’s position as a technology leader in flexible packaging adhesives.

Flexible Packaging Adhesives Technology Market Report Scope

Flexible Packaging Adhesives Technology Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.5 Billion

|

|

Market Size (2034)

|

$4.9 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Adhesive Technology (Solvent-Based, Water-Based, Hot-Melt, Solvent-less, Others), By Application (Food & Beverage Packaging, Pharmaceutical Packaging, Personal Care & Hygiene Packaging, Industrial Packaging, Others), By Material (Polyethylene, Polypropylene, PET, Polyamide, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Dow Inc., Arkema S.A., 3M Company, Sika AG, DIC Corporation, Toyochem Co., Ltd., Bostik S.A., Ashland Inc., Dymax Corporation, Delo Industrial Adhesives, Mactac Americas, Jowat SE, Lord Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flexible Packaging Adhesives Technology Market Segmentation

By Adhesive Technology

- Solvent-Based

- Water-Based

- Hot-Melt

- Solvent-less

- Others

By Application

- Food & Beverage Packaging

- Pharmaceutical Packaging

- Personal Care & Hygiene Packaging

- Industrial Packaging

- Others

By Material

- Polyethylene

- Polypropylene

- PET

- Polyamide

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Flexible Packaging Adhesives Technology Market

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Dow Inc.

- Arkema S.A.

- 3M Company

- Sika AG

- DIC Corporation

- Toyochem Co., Ltd.

- Bostik S.A.

- Ashland Inc.

- Dymax Corporation

- Delo Industrial Adhesives

- Mactac Americas

- Jowat SE

- Lord Corporation

* List Not Exhaustive

Methodology

USDAnalytics employed a rigorous, multi-dimensional research methodology to deliver a comprehensive analysis of the Global Flexible Packaging Adhesives Technology Market. Our approach combined primary research through interviews with adhesive manufacturers, packaging converters, regulatory authorities, and sustainability experts, alongside secondary research involving corporate reports, trade publications, patent databases, and regional regulatory frameworks. The methodology assessed market growth across adhesive technologies—including solvent-less, water-based, hot-melt, and UV/EB-curable systems—applications, and materials, with particular focus on sustainability trends such as non-isocyanate polyurethane (NIPU) adhesives, bio-based formulations, and mono-material compatibility for recyclable packaging. Regional insights were derived from regulatory mandates like the EU’s VOC and EPR policies, U.S. EPA regulations, China’s dual carbon initiatives, and Japan’s Plastic Resource Circulation Act. USDAnalytics also analyzed recent mergers, acquisitions, product innovations, and technological advancements, integrating market sizing, CAGR forecasts, competitive landscape mapping, and trend tracking to provide actionable, professional-grade insights for industry stakeholders seeking strategic, sustainable, and technologically advanced adhesive solutions in flexible packaging.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.