Market Overview: Folding Carton Packaging Market to Reach $322.8 Billion by 2034 at 5.5% CAGR

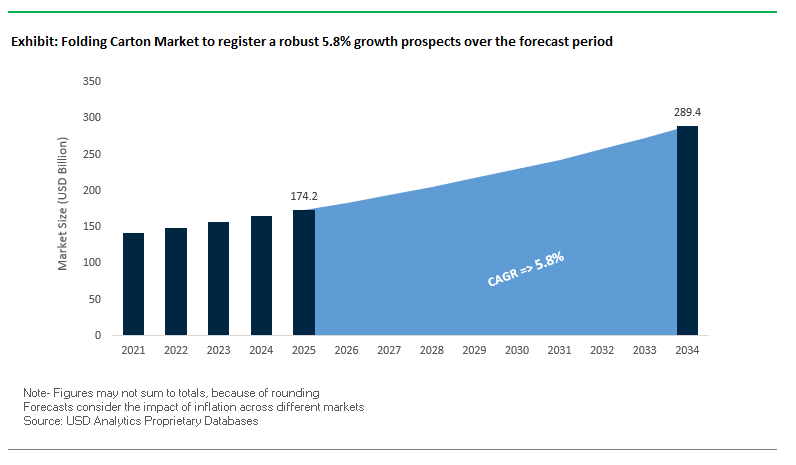

The global folding carton packaging market is projected to expand from $199.4 billion in 2025 to $322.8 billion by 2034, growing at a CAGR of 5.5%. This steady growth is underpinned by rising demand from food & beverage, personal care, and e-commerce sectors, alongside a strong push toward sustainable fiber-based packaging solutions. Folding cartons combine structural integrity, lightweighting, and superior printability, making them a preferred choice for brands looking to balance functionality, safety, and premium aesthetics. For industry professionals and buyers, the key considerations are: Which innovations in barrier coatings and material science will dominate the next decade? How are luxury and e-commerce packaging requirements shaping design priorities? And how are mergers and acquisitions redefining the global competitive landscape?

Key Insights for stakeholders:

- Virgin Fiberboard Demand: Premium brands in food & beverage and personal care are increasingly choosing virgin fiberboard for superior strength, brightness, and brand presentation.

- E-commerce Optimization: Cartons are being redesigned with cube efficiency and durability, enabling cost-effective logistics and improved unboxing experiences.

- Luxury Packaging Growth: The cosmetics sector is driving adoption of advanced printing techniques like cold foil, embossing, and textured finishes for high-value retail visibility.

- Sustainability Innovation: Development of water-based dispersion barriers and renewable materials is making folding cartons more recyclable and compostable, reducing reliance on plastic coatings.

Market Analysis: Recent Developments in the Folding Carton Packaging Industry

The folding carton packaging sector is witnessing consolidation, sustainability-driven product launches, and material breakthroughs, reshaping global supply dynamics.

In August 2025, a landmark event occurred when Smurfit Kappa and WestRock completed their merger, forming Smurfit WestRock, a packaging powerhouse with unmatched production capacity and a strong presence across North America, Europe, and Latin America. That same month, International Paper announced the $1.5 billion sale of its Global Cellulose Fibers business to American Industrial Partners, streamlining its focus on high-margin packaging solutions. Earlier in July 2025, International Paper also finalized its $9.9 billion acquisition of DS Smith, significantly enhancing its European footprint and establishing itself as a leading force in sustainable fiber-based packaging.

Sustainability remains the defining theme in material innovation. In June 2025, Mondi partnered with Saga Nutrition to introduce recyclable, paper-based pet food packaging, underscoring paper’s growing role in FMCG applications. In April 2025, WestRock collaborated with Recipe Unlimited to supply recyclable paperboard packaging, expected to prevent 31 million plastic containers from entering Canadian landfills. Also in April, Billerud launched a formable fiber-based material capable of replacing plastics in packaging, marking a significant advance in material science.

Investment in R&D has accelerated. In March 2025, DS Smith opened its R&D and innovation center near Birmingham, UK, designed to fast-track next-generation packaging technologies. Finally, in February 2025, Graphic Packaging International acquired Americraft Carton Inc., adding seven converting plants in North America and strengthening its leadership in folding carton solutions. Together, these developments signal an industry moving toward sustainability-first strategies, global consolidation, and material innovation leadership.

Trends and Opportunities Reshaping the Folding Carton Packaging Market

Regulatory Pressure for Recyclability and Waste Reduction Mandating Material Science Innovation

The folding carton packaging market is undergoing a compliance-driven transformation, where regulatory mandates on recyclability, waste reduction, and circular economy adoption are directly shaping material science innovation. The European Union’s Packaging and Packaging Waste Regulation (PPWR), effective from 2025, requires all packaging sold in the EU to be recyclable in an economically viable way by 2030, while also mandating a 5% reduction in packaging volume. This directly impacts carton design, forcing manufacturers to engineer solutions that minimize void space while maintaining strength and product protection.

Corporates are responding with accelerated material redesign commitments. Mars and Nestlé, in their 2025 sustainability reports, confirmed increased investments in mono-material paperboard solutions that can be recycled in standard paper streams, reducing reliance on plastic laminates. This is not merely substitution but a fundamental structural redesign of folding cartons to meet future compliance benchmarks. Simultaneously, paper mills and recyclers are expanding their capacity to process coated carton waste, ensuring high-quality fiber recovery. This surge in infrastructure investment underlines how regulatory frameworks are reshaping the entire folding carton value chain from design to recovery.

E-commerce Logistics Demanding Performance-Engineered Cartons

The rapid growth of e-commerce logistics is redefining performance requirements for folding cartons. Unlike retail packaging that emphasizes aesthetics and shelf presence, e-commerce-ready cartons must endure automated sortation systems, multiple handling points, and last-mile delivery stress. Automated fulfillment hubs, operated by companies like Amazon and FedEx, require durable cartons capable of withstanding high-speed sorting processes. Industry reports highlight that packaging durability has become a core determinant of logistics efficiency, directly influencing damage rates and consumer satisfaction.

Beyond durability, regulatory mandates on right-sizing are also reshaping carton design. The EU’s PPWR requires e-commerce packaging to maintain a maximum 50% empty space ratio, pushing companies to adopt intelligent automated packaging systems that tailor each carton’s size to the product. This not only reduces material consumption but also lowers shipping costs and carbon emissions. The folding carton market is thus shifting towards performance-engineered solutions that integrate strength, sustainability, and smart right-sizing to support the e-commerce economy.

Development of Functional Barrier Coatings Without Plastic

One of the most significant opportunities for the folding carton packaging market lies in the development of plastic-free barrier coatings that enable cartons to replace multi-material laminates in food, frozen, and liquid applications. Traditional plastic films used for grease, moisture, or oxygen resistance contaminate recycling streams, but new bio-based coatings are unlocking functional yet recyclable solutions. For example, H.B. Fuller’s bio-based and water-based coatings are now commercially available, offering oil, grease, and water resistance while remaining repulpable and compostable.

Industry leaders are moving aggressively in this direction. Tetra Pak’s paper-based barrier technology, which replaces aluminum foil layers with ultra-thin coatings while increasing paper content to 80%, demonstrates the scalability of plastic-free innovation. These coatings also comply with global food-contact safety regulations such as FDA 21 CFR 176.170 in the U.S. and BfR standards in Europe, enabling safe adoption in regulated food sectors. As regulators, consumers, and corporations converge on plastic-free circular packaging, companies pioneering recyclable barrier-coated cartons will capture significant growth.

Integrated Digital Printing for Hyper-Personalization and Agile Supply Chains

The rise of high-speed digital printing for folding cartons presents another transformative growth opportunity, combining supply chain efficiency with consumer engagement. Digital presses, such as those developed by Koenig & Bauer Durst, enable short-run, variable-data printing that reduces material waste by up to 90% compared to traditional methods, eliminating the need for printing plates and excess inventory. This makes folding cartons ideal for on-demand production and mass customization.

Competitive Landscape: Global Leaders Driving Folding Carton Packaging Innovation

The folding carton packaging market is shaped by large multinational corporations and specialized converters, each leveraging scale, innovation, and sustainability commitments to secure market share.

Smurfit Kappa Group (Now Smurfit WestRock) — Merger Creates a Global Packaging Giant

Smurfit Kappa, now part of Smurfit WestRock, is a leading force in paper-based packaging. The merger with WestRock in August 2025 creates one of the largest global players with unparalleled geographic reach and operational synergies. The company has pioneered multi-pack carriers and recyclable void-fill paper solutions that replace plastics, while leveraging its 350+ production sites worldwide to offer integrated supply chain control.

International Paper — Expanding European Leadership with DS Smith Acquisition

International Paper remains one of the strongest global players in corrugated and paperboard packaging, key components of folding carton production. In July 2025, it finalized the $9.9 billion acquisition of DS Smith, boosting its European market share. A $250 million investment at its Riverdale mill to produce containerboard further aligns with e-commerce packaging needs. By divesting its cellulose fibers business in August 2025, International Paper sharpened its focus on higher-margin, sustainable packaging solutions.

Graphic Packaging International — Scaling North American Folding Carton Capabilities

Graphic Packaging International (GPI) specializes in folding carton solutions for food, beverage, and consumer goods markets. Its February 2025 acquisition of Americraft Carton Inc., which added seven converting plants, significantly expanded its North American capacity. GPI is also innovating with PaperSeal™, a recyclable barrier-lined paperboard tray, and KeelClip™, a paperboard multi-pack solution replacing shrink film and plastic rings. Its integrated supply chain and proprietary machinery systems allow cost-efficient, high-quality production at scale.

WestRock Company (Now Smurfit WestRock) — Driving E-commerce and Fiber Packaging Expansion

WestRock, now merged with Smurfit Kappa, remains a pivotal player in fiber-based packaging solutions. Before the merger, it invested $47 million in its Claremont, North Carolina facility, boosting sustainable packaging capacity and creating 50 new jobs. Its portfolio includes CanCollar® and Meta® Systems, innovations that improve strength, flexibility, and cost-efficiency in consumer packaging. Post-merger, its expertise enhances the combined entity’s global reach and product diversity.

Mondi plc — Advancing Circular Packaging Through MAP2030 Roadmap

Mondi is a pioneer in sustainable packaging and paper solutions, driven by its MAP2030 roadmap that emphasizes “sustainable by design” principles. It recently introduced Ad/Vantage Smooth Brown Semi Extensible paper and is scaling FunctionalBarrier Paper Ultimate, a recyclable high-barrier solution for FMCG applications. Mondi’s vertically integrated operations—from forest management to finished cartons—enable strong supply chain reliability while supporting its ambition to be a leader in circular economy packaging.

Folding Carton Packaging Market Share Insights

Solid Bleached Sulfate Dominates Market Share by Material in Folding Cartons

In the folding carton packaging market, solid bleached sulfate (SBS) accounts for 40% of material share in 2025, reflecting its leadership as the premium-quality substrate for cosmetics, pharmaceuticals, and luxury goods. Its smooth, white surface delivers unmatched printability and visual impact, making it indispensable for high-end retail categories where packaging appearance drives consumer choice. Folding boxboard (FBB) holds 35%, valued for its cost-to-rigidity ratio and widespread use in cereals, toys, and electronics packaging. Coated unbleached kraft (CUK) is growing steadily as the sustainable, natural-look option, favored by eco-conscious brands and durable-goods packaging. White lined chipboard (WLC) continues to serve cost-sensitive applications with recycled content, though it faces pressure as brands upgrade to higher-grade boards. Material-type distribution underscores how aesthetic performance, cost efficiency, and sustainability cues dictate market share, with SBS anchoring the premium end and FBB dominating versatile everyday applications.

Food & Beverages Lead Market Share by Application in Folding Carton Packaging

By application, food and beverages hold the largest share at 45% of the folding carton market in 2025, as high-volume products such as confectionery, frozen foods, and beverage multipacks rely heavily on cartons for both protection and branding. This segment’s scale makes it the foundation of folding carton demand, while innovations in grease- and moisture-resistant coatings extend functionality for ready meals and frozen goods. Healthcare and pharmaceuticals, at 25%, represent a high-value and regulation-driven segment where SBS cartons ensure compliance, tamper evidence, and patient safety. Personal care and cosmetics use high-end cartons to create premium unboxing experiences with foiling and embossing, while consumer electronics leverage intricate die-cut structures to enhance product perception. Tobacco, once a major carton user, is in structural decline due to plain-packaging regulations and falling consumption. Overall, application-level share highlights food as the anchor of volume growth, pharmaceuticals as the compliance core, and cosmetics/electronics as the premium-value drivers of folding carton packaging.

United States: Sustainable and Smart Folding Cartons Driving FMCG Packaging Innovation

The U.S. folding carton packaging market is experiencing a major shift toward sustainable materials, with brands adopting paper-based cartons to meet increasing environmental regulations and consumer demand for green packaging. Companies are prioritizing eco-friendly solutions to reduce plastic use while enhancing recyclability, particularly in the food, beverage, and personal care sectors.

Technological integration is also transforming the market. Anti-counterfeit technologies, including embedded barcodes and RFID tags, are being used to improve product security, while QR codes and augmented reality (AR) enhance consumer engagement and traceability. The booming e-commerce sector is a significant driver, pushing demand for durable, custom, and on-demand packaging that protects products during transit and elevates the unboxing experience. Additionally, adoption of AI-driven production, robotics, and automated folding and gluing systems is enabling high-volume efficiency, cost reduction, and consistent quality in the U.S. folding carton industry.

Germany: Circular Economy Leadership and Premiumization in Folding Cartons

Germany’s folding carton packaging market is a European leader in the circular economy, driven by the German Packaging Act (VerpackG) and the forthcoming EU Packaging and Packaging Waste Regulation (PPWR). Companies are focusing on high-recycling-rate materials and designing packaging for maximum sustainability.

The market also emphasizes premiumization, with brands using tactile coatings, multi-panel storytelling, and high-quality digital printing to enhance the consumer experience and justify higher price points. Strategic investments in automation, including automated die-cutters and folder gluers, are enabling manufacturers to meet the increasing variety of products and demand for short-run customization while maintaining high production efficiency and quality.

China: Regulatory Compliance and E-commerce Driving Folding Carton Demand

China’s folding carton packaging market is being shaped by government regulations targeting sustainability, including policies to curb plastic pollution and improve recycling infrastructure. Standards for degradable and flushable materials are influencing packaging design, driving adoption of fiber-based alternatives.

The country’s massive e-commerce sector is a primary driver, demanding lightweight, durable, and cost-effective cartons for safe shipping. Advanced digital printing technologies allow for short-run customization to cater to diverse and rapidly changing consumer preferences. These developments highlight China’s position as both a major domestic market and global manufacturing hub for folding carton solutions.

India: Make in India Initiative and Technological Investments Shaping Growth

India’s folding carton packaging industry is experiencing rapid growth, fueled by the Make in India initiative, rising middle-class consumption, and low per capita packaging usage, which underscores its high growth potential.

Companies are investing in automated offset presses, die-cutters, and folder gluers to enhance production efficiency and quality, critical for competing in a cost-sensitive market. The sector is also seeing an increased focus on hygiene and shelf impact, as folding cartons provide sanitary barriers for food and personal care products, while high-quality printing enhances branding and marketing effectiveness.

Brazil: Regulatory Support and Barrier Innovations Advancing Folding Cartons

The Brazilian folding carton packaging market benefits from a regulatory push against single-use plastics, encouraging a transition toward fiber-based alternatives. This regulatory environment is driving sustainable packaging adoption across multiple industries.

Innovation in barrier coatings, including water-based and grease-proof treatments, is enabling paperboard to replace traditional plastic-laminated packaging, particularly in the food and beverage sector. Rapid e-commerce growth is another major driver, creating demand for cartons that reduce over-packaging, protect goods in transit, and enhance the consumer unboxing experience.

Japan: High-Quality Aesthetics and Circular Economy Initiatives Leading Folding Carton Trends

Japan’s folding carton packaging market is defined by premium design, high-quality materials, and functional innovations. Brands prioritize aesthetic appeal through decorative printing and premium paperboard, meeting consumer expectations for quality and luxury.

Innovations such as the S-Lock Tray for fruits demonstrate the market’s focus on material reduction while improving workability. The industry is also committed to a circular economy, with companies like Rengo designing packaging for easy recycling and exploring strategies to minimize environmental impact, reflecting Japan’s leadership in sustainable and eco-friendly folding carton solutions.

Folding Carton Packaging Market Report Scope

Folding Carton Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$199.4 Billion

|

|

Market Size (2034)

|

$322.8 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Material Type (Folding Boxboard, Solid Bleached Sulfate, Coated Unbleached Kraft, White Lined Chipboard), By Application (Food & Beverages, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, Consumer Electronics, Tobacco, Other Applications), By Printing Technology (Offset Lithography, Digital Printing, Flexography, Rotogravure), By End-Use (Retail, E-commerce, Industrial)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, Graphic Packaging Holding Company, WestRock Company, Smurfit Kappa Group plc, Mondi Group, DS Smith Plc, Huhtamaki Oyj, Amcor plc, Rengo Co., Ltd., Sonoco Products Company, Oji Holdings Corporation, Clearwater Paper Corporation, BillerudKorsnäs AB, TC Transcontinental Inc., Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Folding Carton Packaging Market Segmentation

By Material Type

- Folding Boxboard

- Solid Bleached Sulfate

- Coated Unbleached Kraft

- White Lined Chipboard

By Application

- Food & Beverages

- Personal Care & Cosmetics

- Healthcare & Pharmaceuticals

- Consumer Electronics

- Tobacco

- Other Applications

By Printing Technology

- Offset Lithography

- Digital Printing

- Flexography

- Rotogravure

By End-Use

- Retail

- E-commerce

- Industrial

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Folding Carton Packaging Market

- International Paper Company

- Graphic Packaging Holding Company

- WestRock Company

- Smurfit Kappa Group plc

- Mondi Group

- DS Smith Plc

- Huhtamaki Oyj

- Amcor plc

- Rengo Co., Ltd.

- Sonoco Products Company

- Oji Holdings Corporation

- Clearwater Paper Corporation

- BillerudKorsnäs AB

- TC Transcontinental Inc.

- Greif, Inc.

*List not Exhaustive

Research Coverage

This USDAnalytics report investigates the global folding carton packaging market, providing an in-depth analysis of breakthroughs in sustainable fiber-based materials, high-performance barrier coatings, and digital printing technologies that are reshaping design, functionality, and brand engagement. The analysis reviews recent mergers, strategic acquisitions, and technological innovations, highlighting how companies are optimizing cartons for e-commerce logistics, luxury branding, and circular economy compliance. This report is an essential resource for packaging engineers, brand managers, supply chain professionals, and industry investors seeking actionable insights into material science innovations, regulatory impacts, and competitive dynamics. It also highlights emerging trends such as plastic-free barrier solutions, mono-material designs, and high-speed digital printing for hyper-personalization. USDAnalytics combines historical data from 2021 to 2024 with forecasts from 2025 to 2034, delivering a comprehensive view of market growth drivers, competitive strategies, and regional opportunities across North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa.

Scope Highlights:

- Segmentation: By Material Type (Folding Boxboard, Solid Bleached Sulfate, Coated Unbleached Kraft, White Lined Chipboard), By Application (Food & Beverages, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, Consumer Electronics, Tobacco, Other Applications), By Printing Technology (Offset Lithography, Digital Printing, Flexography, Rotogravure), By End-Use (Retail, E-commerce, Industrial)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historical data from 2021 to 2024; forecast data from 2025 to 2034

- Companies: Profiles and analysis of 15+ companies including International Paper, Graphic Packaging Holding, WestRock, Smurfit Kappa, Mondi, DS Smith, Huhtamaki, Amcor, Rengo, Sonoco, Oji Holdings, Clearwater Paper, BillerudKorsnäs, TC Transcontinental, and Greif

Methodology

The study applies a rigorous research methodology combining primary interviews, expert consultations, and secondary data analysis to ensure comprehensive insights into the folding carton packaging market. USDAnalytics conducted discussions with packaging professionals, brand managers, regulatory experts, and material scientists to evaluate sustainability initiatives, e-commerce optimization, barrier coating innovations, and digital printing adoption. Secondary sources, including corporate filings, industry journals, regulatory databases, and historical market reports, were analyzed to capture trends from 2021 to 2024. A combination of top-down and bottom-up approaches was used to quantify market size by material type, application, printing technology, and end-use. Competitive benchmarking, scenario modeling, and regulatory impact assessment were integrated to evaluate market opportunities and risks. This methodology ensures highly accurate, actionable, and forward-looking insights for decision-makers and professionals across FMCG, retail, and industrial packaging sectors.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.