Global Food and Beverage Metal Cans Market Overview: Sustainability and Innovation Driving Growth

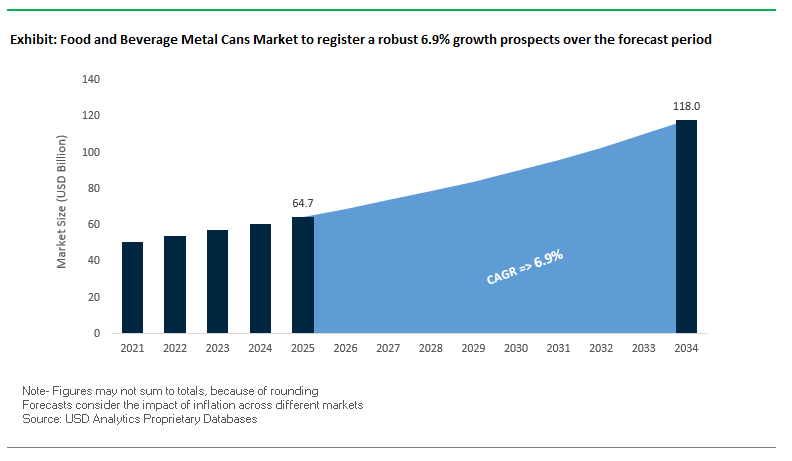

The global food and beverage metal cans market is forecasted to reach USD 64.7 billion in 2025 and expand to USD 118 billion by 2034, registering a steady CAGR of 6.9%. Industry professionals recognize metal cans as a cornerstone of the sustainable packaging revolution, thanks to their unparalleled recyclability, safety, and adaptability across both food and beverage applications. For buyers, the market answers pressing questions on sustainability performance, packaging efficiency, and cost optimization in supply chains under increasing regulatory and consumer pressure.

The market’s strength lies in its synergy between convenience, durability, and environmental responsibility. With aluminum and steel leading the charge in circular economy initiatives, food and beverage companies are increasingly aligning their packaging strategies with ambitious recycling and decarbonization targets. Lightweighting innovations and new manufacturing alloys are reinforcing the competitive position of metal cans against plastic and glass, while automation and smart labeling are unlocking new efficiencies and consumer engagement.

Key Insights for Industry Stakeholders

- High Recycled Content Advantage: Aluminum beverage cans in the U.S. contain 71% recycled content, outperforming glass (23%) and plastic (3–10%).

- Recycling Speed: Used cans can be recycled and back on store shelves in as little as 60 days, showcasing unmatched supply chain efficiency.

- Lightweighting Breakthroughs: Beverage cans are now over 40% lighter than in the 1970s, with wall thickness as thin as a human hair.

- Global Recycling Targets: The aluminum industry aims for 80% global recycling rates by 2030 and near 100% by 2050, reinforcing metal cans’ long-term sustainability role.

Market Analysis: Strategic Developments Reshaping the Metal Can Industry

The food and beverage metal cans industry has seen a surge in mergers, technological innovation, and sustainability-focused initiatives in recent years. In January 2024, Visy Industries, a leading Australian food can supplier, acquired Advanced Circular Polymers (ACP) to strengthen plastics recycling capabilities and reinforce its circular economy approach. This was followed by November 2024, when Sonoco expanded its Asia-Pacific footprint by acquiring the composite can operations of Amcor Packaging, including two manufacturing facilities.

In December 2024, industry associations highlighted the U.S. aluminum can consumer recycling rate at 43%, still significantly higher than competing materials. The drive for efficiency extended into February 2025, when new can-making alloys were introduced to streamline production by allowing the same alloy to be used for both body and lid. However, in March 2025, new U.S. tariffs on imported steel and aluminum began to weigh heavily on producers, raising costs and forcing some brands to explore alternative packaging formats.

Meanwhile, innovation in product design accelerated with Ball Corporation’s April 2025 launch of sustainable retort aluminum cans for milkshakes in partnership with CavinKare. The innovation curve continued in July 2025, with the unveiling of temperature-sensitive labels for beverage cans, enhancing consumer experience by signaling ideal drinking temperature. By August 2025, automation breakthroughs enabled equipment manufacturers to achieve production rates of over 2,000 cans per minute, more than doubling historical averages, further reinforcing the market’s efficiency trajectory.

Emerging Trends and Opportunities Redefining the Food and Beverage Metal Cans Market

Strategic Investment in Capacity Expansion and Facility Modernization

The food and beverage metal cans market is undergoing a significant transformation as leading manufacturers execute large-scale investments to modernize operations and expand global capacity. These commitments signal confidence in long-term demand for canned food and beverages, which remain essential to both mature and emerging markets. For example, Crown Holdings allocated $403 million in capital expenditure in 2024 as part of a multi-year expansion program, with an additional $450 million planned for 2025. These investments are primarily focused on the beverage can segment, which accounts for nearly two-thirds of Crown’s total revenue. Reinforcing this momentum, Crown recently launched a new two-line plant in Peterborough, United Kingdom, to meet Europe’s growing demand, while its North American facilities in Martinsville, Virginia, and Mesquite, Nevada, continue to surpass production expectations. Strategic restructuring is also shaping the landscape—Ball Corporation’s divestment of a 41% stake in its Saudi Arabian joint venture for $70 million reflects a disciplined approach to capital allocation, allowing the company to reinvest in high-growth, core packaging operations. Together, these moves underscore how modernization, facility launches, and geographic restructuring are central to strengthening competitiveness and meeting surging global demand.

Accelerated Adoption of Specific Sustainable Technologies

Sustainability in the metal cans industry has moved beyond broad recycling initiatives to the deployment of targeted, measurable technologies that reshape manufacturing practices. Crown Holdings’ 2024 Annual Report reveals that the company is already 46% of the way toward achieving its 2030 target of sourcing 75% renewable electricity, having reduced Scope 1 and 2 emissions by 16% in the same year. This demonstrates a clear commitment to science-based decarbonization. Similarly, Ball Corporation is spearheading circular economy solutions through the Global Beverage Can Circularity Alliance (GBCCA), aiming to establish a fully circular aluminum packaging loop. Weight reduction remains another pillar of sustainability progress. Coca-Cola HBC’s lightweighting initiatives have eliminated over 50,000 tonnes of packaging annually since 2010, while carton-based multipack solutions have avoided 2,300 tonnes of shrink film in 2023 alone. These advancements demonstrate how renewable energy integration, true circularity, and lightweighting initiatives are not only reducing environmental impact but also enhancing the competitiveness of metal cans in a global packaging market under increasing regulatory and consumer scrutiny.

Capitalizing on the Revival of Home Cooking and Pantry Stocking

Post-pandemic consumer behavior has created enduring opportunities for canned food products as households continue to embrace pantry stocking and convenient meal preparation. According to the USDA’s Economic Research Service, U.S. households maintain higher-than-pre-2020 levels of food stockpiles, driven by a desire for food security and reduced shopping frequency. This behavioral shift benefits shelf-stable canned goods, which provide long shelf life and versatility. Supporting this trend, the AHDB’s 2024 consumer insight report reveals that average preparation time for evening meals has dropped to 31 minutes, pushing consumers toward quick, convenient solutions where canned vegetables, fruits, and proteins play a central role. Industry data shows that sales of canned pantry staples remain elevated above pre-pandemic levels, suggesting that this trend is not temporary but a long-term driver of market growth. For food and beverage brands, this presents a sustained opportunity to align product innovation and marketing with the lifestyle needs of modern, convenience-driven households.

Penetration into New and High-Growth Beverage Categories

Metal cans are rapidly gaining ground in premium and emerging beverage segments, far beyond their traditional dominance in beer and carbonated soft drinks. Their lightweight, portable, and highly recyclable attributes position them as the preferred format for new-generation beverages. The explosive growth of hard seltzers and RTD cocktails underscores this shift, with metal cans delivering key advantages such as rapid chilling and easy stackability. Expanding into functional drinks, The Coca-Cola Company launched its Glaceau Smartwater in 12-ounce aluminum cans in the U.S., highlighting how cans are now being leveraged to elevate the image of wellness-oriented beverages. Furthermore, Crown Holdings reports that approximately 75% of all new beverage launches in North America now appear in cans, more than doubling in just five years. This surge reflects how brand owners view cans as an essential packaging solution that combines sustainability with premium shelf appeal. As beverage innovation accelerates, the penetration of cans into these new categories will remain a critical growth engine for the global food and beverage metal cans market.

Competitive Landscape: Global Leaders Shaping the Future of Metal Cans

The global food and beverage metal cans industry is highly consolidated, with major players leveraging technological expertise, geographic expansion, and strong sustainability commitments. These companies are not only expanding capacity but also investing in advanced alloys, decorative finishes, and smart packaging features to secure market leadership.

Ball Corporation drives lightweighting and circularity initiatives

Ball Corporation (USA) leads the global market with a strong focus on sustainability and lightweighting. Its latest innovation, the STARcan, is 8% lighter than standard cans, reducing raw material usage and lowering carbon emissions. The company is expanding production facilities worldwide to meet rising demand for aluminum beverage packaging, while also targeting emerging categories such as canned water and wine.

Crown Holdings strengthens premium branding through decorative cans

Crown Holdings, Inc. (USA) differentiates itself with advanced decorative printing and premium branding capabilities. By working closely with global food and beverage brands, Crown helps products achieve high shelf appeal. The company is expanding its manufacturing footprint in Asia and Europe and supports brand transitions from plastics and glass to sustainable metal packaging through integrated design and production services.

Ardagh Group promotes net-zero ambitions with diverse can portfolio

Ardagh Group S.A. (Luxembourg) operates across both beverage and food metal can markets, specializing in airtight, durable packaging that preserves product freshness and nutrition. The company is committed to 2050 net-zero goals and is a signatory of industry-wide climate initiatives. Ardagh’s portfolio includes popular single-serve wine cans, gaining traction for their portability and protection against light and oxygen.

Silgan Holdings delivers consumer convenience with innovative can ends

Silgan Holdings Inc. (USA) is a leading supplier of food cans in North America and Europe, offering packaging for fruits, vegetables, meat, and seafood. Its focus is on developing easy-open and resealable can ends, boosting consumer convenience and product accessibility. Silgan’s strong partnerships with leading food brands ensure consistent demand and highlight its role in ensuring food safety and shelf stability.

Trivium Packaging pioneers lightweight seafood cans and circularity

Trivium Packaging (Netherlands) is a sustainability-driven packaging leader recognized for producing the world’s lightest aluminum seafood can. With a sharp focus on recycled content and lightweighting, the company supports global brands in food, beverages, and personal care with customizable, decorative, and circular economy solutions. Trivium continues to push the boundaries of design and environmental efficiency in the metal can segment.

Food and Beverage Metal Cans Market Share Insights

Market Share by Can Size in the Food and Beverage Metal Cans Market

The 12 oz. (355 ml) can dominates the global food and beverage metal cans market with a 58% share in 2025, underscoring its position as the industry’s standard. Its dominance is anchored in decades of consumer familiarity, standardized production lines, and economies of scale that make it the most cost-effective format for beverage manufacturers. It is the default packaging for carbonated soft drinks (CSDs) and traditional beers, categories that still represent enormous global volume. This entrenched position has made the 12 oz. format nearly irreplaceable, despite innovation in can designs and size variations. Meanwhile, the 16 oz. (473 ml) can—holding 22% share—is the fastest-growing format, often referred to as “pounders.” Its growth is directly tied to shifting consumption trends in craft beer, hard seltzers, and ready-to-drink (RTD) cocktails, where consumers perceive value in larger volumes without overcommitment. Beverage brands are aggressively adopting this format to differentiate premium offerings, signaling a clear link between the rise of 16 oz. cans and the expansion of high-margin beverage categories. On the other hand, the 8 oz. (237 ml) and other sizes serve more specialized but strategically vital niches. The 8 oz. format is critical in energy shots, mixers, and kids’ drinks, while “other sizes” extend versatility across food packaging covering formats from 4 oz. tomato paste cans to 24–32 oz. iced tea and juice containers. This long-tail variety demonstrates the adaptability of metal cans in meeting both single-serve convenience and bulk storage needs, reinforcing their indispensability across applications.

Market Share by Application in the Food and Beverage Metal Cans Market

The beverage segment dominates the food and beverage metal cans market with a commanding 72% share in 2025, reflecting the unparalleled reliance of the global beverage industry on metal cans. This dominance is tied to their superior protection against light and oxygen, ability to chill rapidly, and strength as a marketing canvas through high-resolution graphics and customization. Single-serve and on-the-go consumption trends continue to drive enormous demand in categories such as CSDs, beers, energy drinks, and emerging RTDs, ensuring that beverages remain the backbone of the industry. In contrast, the food segment holds 28% of the market, representing a smaller but highly stable and resilient application area. Food cans play a critical role in long-shelf-life preservation of vegetables, soups, pet food, fish, and ready meals, where the airtight seal and sterilization capabilities of metal cans are unmatched. While less influenced by branding and marketing compared to beverages, the food segment is sensitive to raw material costs (aluminum and steel) and consumer health concerns around BPA liners, driving ongoing innovation in BPA-free coatings and lightweighting. Divergent growth drivers distinguish these two segments: beverages rely on marketing, new product launches, and premiumization, while food can growth is tied to population growth, food security concerns, and the demand for shelf-stable, convenient meal solutions. This divergence highlights the dual nature of the industry—one driven by consumer lifestyle trends, the other by essential functionality.

United States: Investments, Recycling Partnerships, and Sustainable Innovations in Metal Can Packaging

The U.S. food and beverage metal cans market is experiencing robust growth, fueled by heavy investments from major players like Ball Corporation in expanding production capacity. New manufacturing lines and upgraded facilities are being established to meet surging demand for aluminum beverage cans, particularly as consumption of carbonated soft drinks, seltzers, and ready-to-drink (RTD) cocktails continues to rise. Technological advancements in coatings are another major driver, with companies accelerating the shift toward BPA-free linings. This aligns with regulatory pressures and consumer preference for food-safe, sustainable packaging.

Innovation in can formats is also shaping the U.S. market, with slender cans designed for low-calorie seltzers and premium aluminum bottles providing differentiation for alcoholic and non-alcoholic beverages. Recycling partnerships between can manufacturers, industry organizations, and government bodies are enhancing aluminum circularity by improving the collection and processing of used beverage cans (UBCs). Furthermore, lightweighting technologies are reducing material usage and lowering carbon footprints, positioning metal cans as both a sustainable and high-performance packaging solution for the American beverage industry.

China: Urbanization, Policy Support, and High-Speed Production Drive Can Market Expansion

China’s food and beverage metal cans market is thriving, driven by rapid urbanization, rising disposable incomes, and shifting consumer lifestyles toward convenient, ready-to-eat packaged foods and beverages. The country’s massive beer and soft drink markets rely heavily on aluminum cans, while expanding food processing facilities are increasing demand for metal cans in both domestic and export-oriented production.

The Chinese government’s policy framework promoting eco-friendly and recyclable packaging provides further momentum, positioning metal cans as a sustainable alternative to single-use plastics. On the supply side, manufacturers are investing in automation and high-speed production lines to improve operational efficiency and meet high-volume requirements. Beyond aluminum, lightweight steel cans are gaining traction in the food sector, offering durability while optimizing transportation costs. These combined trends cement China’s role as one of the fastest-growing hubs for food and beverage metal can packaging.

Germany & France: EU Regulations, Premium Can Design, and Circular Economy Leadership

Germany and France are at the forefront of Europe’s food and beverage metal cans market, where sustainability regulations and consumer demand converge. The EU’s Single-Use Plastics Directive is a pivotal factor, compelling beverage and food brands to transition toward recyclable, long-life alternatives like aluminum and steel cans. This regulatory push is reinforced by well-established deposit-return systems and high recycling rates, making these countries leaders in circular economy practices for metal packaging.

Innovation in can aesthetics and consumer engagement is also significant. Digital printing technologies are being widely adopted to produce visually appealing, customized designs for craft beverages, premium sodas, and specialty food products. In addition, European regulators and consumers are strongly advocating for BPA-NI (Bisphenol-A non-intent) coatings, accelerating research and commercialization of safer linings. Strategic investments by global canmakers in production facilities across Europe are focused not only on expanding capacity but also on improving energy and water efficiency, reinforcing Germany and France as innovation hubs for sustainable metal can packaging.

India: Rising Packaged Food Consumption and Strategic Partnerships Fuel Market Growth

India’s food and beverage metal cans market is witnessing rapid expansion, primarily driven by the growing consumption of packaged foods and beverages in urban centers. Rising disposable incomes and evolving dietary preferences are boosting demand for ready-to-eat meals, dairy-based beverages, and convenience products—categories well-suited for preservation in metal cans. Government support for food processing initiatives has created a favorable investment environment, encouraging modernization in packaging infrastructure.

Global and domestic players are expanding their footprint, with notable collaborations such as Ball Corporation’s partnership with CavinKare to introduce two-piece aluminum cans for milkshakes. This move reflects India’s rising interest in sustainable dairy and beverage packaging. Technological innovations, including improved coatings and adherence to FSSAI’s proposed stricter food safety guidelines, are strengthening consumer confidence in canned products. Coupled with rising awareness of sustainability and the recyclability benefits of aluminum cans, India is becoming a strategically important growth market for the global metal cans industry.

Brazil: Expanding Beverage Industry and Raw Material Availability Strengthen Can Adoption

Brazil is one of Latin America’s most dynamic food and beverage metal cans markets, with metal packaging firmly entrenched in its beer and soft drink sectors. The transition from returnable glass bottles to lightweight aluminum cans is accelerating, reflecting changing consumer habits and industry efficiency goals. Crown Holdings and other global manufacturers are making significant investments, including new can facilities with annual capacities exceeding billions of units, to cater to growing domestic and export markets.

Rising consumption of energy drinks, specialty juices, and RTD alcoholic beverages is further boosting demand for aluminum cans, particularly among the country’s expanding middle class. Economic and environmental factors also contribute to the shift, as cans offer a lightweight and recyclable solution that reduces logistics costs in Brazil’s geographically vast market. These combined drivers highlight Brazil’s importance as both a consumption and production hub for food and beverage metal can packaging in Latin America.

Japan: Recycling Leadership and Material Efficiency Innovations Define Market Dynamics

Japan’s food and beverage metal cans market is globally recognized for its exceptionally high recycling rates and efficient waste management systems. This infrastructure underpins the country’s circular economy strategy, ensuring that aluminum and steel cans remain among the most sustainable packaging options. Beverage manufacturers and canmakers benefit from this established system, which enhances consumer confidence in metal cans as an environmentally responsible choice.

Innovation remains a cornerstone of Japan’s industry, with companies like Toyo Seikan developing cutting-edge solutions such as can lids incorporating higher levels of recycled material. Lightweighting technologies are also advancing, reducing material consumption while preserving can strength and functionality. Japanese companies are deeply committed to the “Eco Action Plan 2030,” which emphasizes reducing finite resource usage and creating a resource-circulating society. With infinite recyclability and continuous improvements in material efficiency, metal cans are positioned as a central pillar of Japan’s sustainable food and beverage packaging market.

Food and Beverage Metal Cans Market Report Scope

Food and Beverage Metal Cans Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$64.7 Billion

|

|

Market Size (2034)

|

$118 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Material (Aluminum, Steel), By Product Type (2-Piece Cans, 3-Piece Cans), By Can Size (12 Oz., 16 Oz., 8 Oz., Other Sizes), By Application (Beverages, Food)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ball Corporation, Ardagh Group S.A., Crown Holdings, Inc., CAN-PACK S.A., Silgan Holdings Inc., Toyo Seikan Group Holdings, Ltd., Hindustan Tin Works Ltd., Envases Group, Nampak Ltd., Mauser Packaging Solutions, Sonoco Products Company, Kaira Can Company Limited, Visakha Metal Industries, Anheuser-Busch InBev (Metal Container Corporation)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Food and Beverage Metal Cans Market Segmentation

By Material

By Product Type

- 2-Piece Cans

- 3-Piece Cans

By Can Size

- 12 Oz.

- 16 Oz.

- 8 Oz.

- Other Sizes

By Application

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Food and Beverage Metal Cans Market

- Ball Corporation

- Ardagh Group S.A.

- Crown Holdings, Inc.

- CAN-PACK S.A.

- Silgan Holdings Inc.

- Toyo Seikan Group Holdings, Ltd.

- Hindustan Tin Works Ltd.

- Envases Group

- Nampak Ltd.

- Mauser Packaging Solutions

- Sonoco Products Company

- Kaira Can Company Limited

- Visakha Metal Industries

- Anheuser-Busch InBev (Metal Container Corporation)

* List Not Exhaustive

Research Coverage

This report investigates the global Food and Beverage Metal Cans Market with a sharp focus on sustainability-led innovations, manufacturing breakthroughs, and commercial strategies reshaping packaging value chains; it synthesizes competitive developments, regulatory drivers, and material-technology intersections so readers can rapidly assess risk and opportunity. The analysis reviews recent capital investments, lightweighting and alloy advances, circularity initiatives, and commercial use-cases (from RTD beverages to retortable cans) that are altering cost structures and go-to-market strategies. Case studies and technology deep-dives highlight breakthroughs in production automation, smart labelling, and coating alternatives—while scenario-based forecasts quantify outcomes under varied raw-material and policy regimes—making this report an essential resource for C-suite strategists, packaging engineers, sustainability leads, and investors. USDAnalytics combines proprietary modelling with industry-sourced intelligence to deliver actionable recommendations and priority investment themes for stakeholders seeking to align product portfolios with decarbonization, recyclability, and consumer-preference imperatives.

Scope Highlights

- Segmentation: By Material (Aluminum, Steel); By Product Type (2-Piece Cans, 3-Piece Cans); By Can Size (12 oz., 16 oz., 8 oz., Other Sizes); By Application (Beverages, Food).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic data (2021–2024) and forecast horizon (2025–2034).

- Companies: In-depth analysis and profiles of 15+ leading players and innovators (manufacturers, alloy suppliers, and technology licensors).

Methodology

This report adopts a blended primary-and-secondary research methodology: primary inputs were collected via structured interviews with packaging OEMs, brand procurement leads, recycling and materials experts, and plant managers across target regions; secondary research synthesised annual reports, trade association data, regulatory filings, patent disclosures, trade press, and supplier technical papers. Market sizing and forecasting use a hybrid top-down/bottom-up approach—triangulating production capacity, historical shipment data, consumption patterns by application, and macro drivers such as urbanization and retail channel shifts—while sensitivity analysis models price shocks (aluminum/steel tariffs) and policy scenarios (deposit-return systems, single-use plastic bans). All inputs were validated through cross-checks with company CAPEX announcements, observed plant startups, and technology licensing activity to ensure robust, investment-grade conclusions.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.