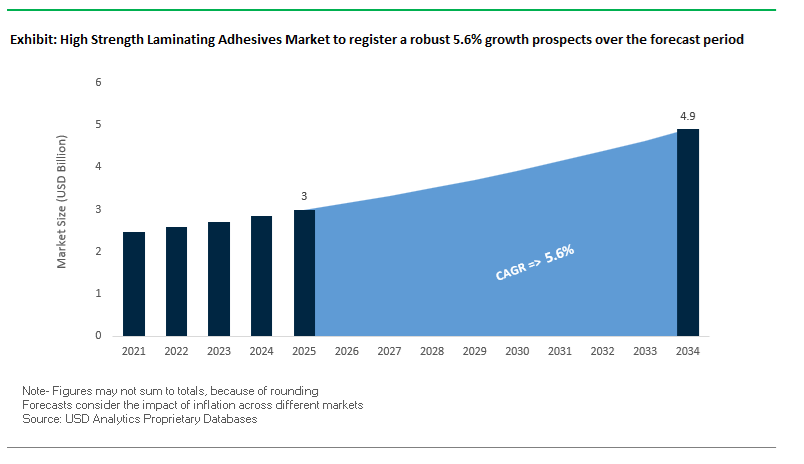

The Global High Strength Laminating Adhesives Market is projected to grow from USD 3.0 billion in 2025 to USD 4.9 billion by 2034, registering a CAGR of 5.6%. This growth trajectory is powered by the ongoing material transformation toward solvent-free, water-based, and ultra-low monomer polyurethane (PU) adhesive systems, meeting both performance durability and global sustainability mandates. The market is increasingly characterized by a dual demand — adhesives that can withstand extreme processing temperatures while also complying with stringent food-contact and environmental safety standards.

Advanced high-strength laminating adhesives are mission-critical across retort food packaging, medical flexible films, industrial composites, and structural laminates. In food and pet care packaging, retort-grade laminating adhesives have evolved to endure autoclave sterilization at up to 134°C while maintaining bond integrity and delamination resistance. Meanwhile, the broader transition toward solvent-free polyurethane (PU) and water-based dispersions has eliminated the energy-intensive drying phase, reducing CO₂ emissions by 25–30% per laminated product unit and improving plant safety and cost efficiency.

The market is also observing a significant regulatory-driven shift toward ultra-low monomer systems (<0.1% free diisocyanate) to comply with REACH and FDA 21 CFR standards for food safety. Further, the T-Peel Test (ASTM D1876) continues to be a defining benchmark for adhesion strength in high-performance flexible-to-flexible laminations, ensuring consistent reliability under deep-freeze or hot-fill stress conditions. Parallel advancements in epoxy-based laminating adhesives for composites in wind energy and automotive further indicate diversification beyond packaging applications.

In July 2025, Henkel Adhesive Technologies announced a breakthrough in high-performance packaging adhesives with the launch of Loctite Liofol LA 7837/LA 6265, a solvent-free, aliphatic polyurethane adhesive system designed for retort pet food applications. Capable of withstanding thermal sterilization up to 134°C, it delivers both high adhesion and food-contact compliance, marking a pivotal move toward energy-efficient, low-VOC adhesive processing.

In December 2024, Arkema (Bostik) finalized the $150 million acquisition of Dow’s flexible packaging laminating adhesives business, significantly broadening its portfolio of solvent-free and high-performance PU adhesives. This acquisition includes five global manufacturing sites and positions Arkema as a key global player in flexible packaging adhesives. The integration is expected to yield $30 million in EBITDA synergies within five years, boosting market competitiveness in Asia-Pacific and Europe.

Earlier, in May 2024, Dow Inc. announced the divestiture of its non-core flexible packaging laminating adhesives business to Arkema, signaling a strategic pivot toward “Decarbonize & Grow” and advanced materials innovation, while retaining its MOR-FREE™ and ADCOTE™ solvent-free systems. This realignment underscores Dow’s intent to lead in circular polymer innovation and sustainable materials rather than compete in commodity adhesive lines.

By early 2025, BASF SE expanded its Epotal® and Luphen® water-based adhesive lines to address recyclable and compostable packaging. These products, compatible with PLA and paper substrates, align with the EU Green Deal and Ellen MacArthur Foundation circular economy objectives, setting a sustainability benchmark for waterborne adhesives.

In June 2024, Sika AG reinforced its Purform® polyurethane platform, lowering free monomer content below 0.1%, complying with the upcoming REACH Annex XVII regulation. The innovation significantly reduces end-user safety requirements without compromising adhesion performance, strengthening its position in automotive, construction, and laminating sectors.

Meanwhile, Sun Chemical (Q3 2025) expanded its SunLam™ range of solvent-free laminating adhesives, designed for industrial compostable films and home-compostable packaging, responding to rising demand from FMCG and sustainable packaging converters. Concurrently, regional converters in China and India ramped up investments in solvent-free laminating lines, reflecting a decisive industry-wide migration toward sustainable adhesives.

Additionally, the global focus on epoxy-silane-free adhesive systems — led by innovators such as Toyo-Morton — indicates a growing preference for non-toxic, migration-safe chemistry that supports food contact regulation harmonization across the EU and Asia-Pacific.

A defining trend in the high-performance laminating adhesives market is the rapid industry shift from solvent-based formulations to 100% solids, solvent-free polyurethane and acrylic systems. The transition is not only a response to tightening VOC emission regulations but also a direct reflection of global brands’ sustainability goals and carbon reduction commitments. Modern solvent-free adhesives deliver equivalent or even superior performance compared to traditional solvent-based counterparts—without compromising production efficiency or adhesive strength.

The productivity advantage of solventless laminating systems is clearly validated by industry benchmarks. Advanced formulations from leading suppliers like Bostik are engineered for high-speed lamination processes, achieving line speeds of up to 1,300 feet per minute, representing a paradigm shift in flexible packaging operations that previously sacrificed speed for environmental compliance. These innovations demonstrate that green adhesive technology can compete head-to-head with conventional solvent-based adhesives in both performance and throughput.

From a sustainability perspective, major chemical producers such as Henkel and Dow are integrating low-carbon feedstocks and renewable electricity into their manufacturing processes, targeting a 20%–40% reduction in the Product Carbon Footprint (PCF) for hot melt and laminating adhesive lines. The decarbonization strategy is directly aligned with the industry’s migration toward cleaner production methods and ESG-compliant supply chains.

Further, testing on water-based acrylic/urethane hybrid systems in PET/PE laminates has yielded seal strength levels of approximately 37.6 ± 3.9 N/15mm, demonstrating performance parity with solvent-based urethane adhesives. These findings validate that next-generation solvent-free and waterborne adhesives are capable of maintaining the high cohesive strength, flexibility, and durability required for premium flexible packaging applications—marking a decisive step toward the elimination of solvent emissions in industrial lamination processes.

As global food safety and sterilization standards tighten, the need for high-barrier, retortable laminating adhesives has become critical to maintaining package integrity under extreme processing conditions. In retort applications, where packages undergo temperatures exceeding 121°C and elevated pressure during sterilization, conventional laminates often experience degradation in oxygen and moisture barrier performance.

Technical studies confirm that even SiOx-coated high-barrier polyester films suffer from increased Oxygen Transmission Rates (OTR) and Water Vapor Transmission Rates (WVTR) after the retort process, underscoring the importance of specialized cross-linked polyurethane and polyester adhesives capable of protecting barrier integrity. These adhesives act as structural reinforcements that prevent delamination and film deformation, ensuring product stability, safety, and shelf-life consistency in demanding food and medical packaging applications.

Equally important is the precision of adhesive formulation and mixing, particularly in two-component retort systems. Technical documentation from TAPPI highlights that improper mix ratios can cause dramatic reductions in bond strength, chemical resistance, and heat tolerance, resulting in failed laminations. Hence, process optimization and quality assurance are integral to realizing the full potential of high-performance retort adhesives in large-scale packaging lines.

The expansion of high-barrier flexible packaging across shelf-stable foods, pharmaceutical sachets, and sterilized medical pouches continues to drive R&D toward adhesives with enhanced chemical resistance and thermal endurance, positioning the segment as a key growth engine for the global High Strength Laminating Adhesives Market.

The global movement toward circular economy and packaging recyclability presents a transformative growth opportunity for high-strength laminating adhesives compatible with mono-material packaging structures, such as all-polyethylene (PE) laminates. Traditional multi-layer laminates—often composed of dissimilar plastics like PET, PE, and aluminum—pose major challenges for mechanical recycling. Hence, adhesives that allow seamless bonding between similar polymer substrates while maintaining performance integrity are vital for achieving a truly recyclable packaging ecosystem.

According to 2023 data, over 71% of multinational FMCG companies announced active Mono-Material Packaging Strategies aimed at meeting recyclability goals by 2025. The corporate commitment is creating a powerful demand pull for recycling-friendly adhesive solutions. Industry validation from the Association of Plastic Recyclers (APR) further strengthens the transition—Dow’s PACACEL™ Solventless Adhesive systems received official APR recognition for compatibility with PE recycling, marking a key milestone in adhesive innovation for sustainable flexible packaging.

The opportunity aligns directly with regulatory frameworks promoting Extended Producer Responsibility (EPR), where packaging producers must ensure that materials are recoverable within established waste management systems. Adhesives engineered for chemical compatibility and easy delamination form a critical component of recyclable packaging design, ensuring high-strength bonding during use and clean separation during recycling—a technological balance crucial to circular material economics.

The surge in consumer demand for eco-friendly and bio-based packaging materials offers a major growth frontier for adhesive manufacturers investing in renewable raw materials and biodegradable chemistry. As leading CPG brands commit to reducing their dependency on fossil-derived components, bio-based laminating adhesives derived from plant oils, starches, and other renewable feedstocks are gaining traction as viable high-performance alternatives.

Academic research and industrial R&D initiatives are converging on the use of vegetable oil–derived polyols (e.g., from castor and palm oils) in the synthesis of bio-based polyurethane laminating adhesives. These formulations demonstrate mechanical and thermal performance characteristics comparable to petroleum-based counterparts while offering superior sustainability credentials.

Commercially, companies like Henkel have set an early precedent in the domain by launching hot melt adhesives with 49% renewable content that also reduce operational temperatures by up to 40°C, translating to lower CO₂ emissions and reduced energy consumption in manufacturing. The dual sustainability benefit—through renewable sourcing and process efficiency—illustrates how bio-based adhesives can deliver both environmental and economic performance advantages for flexible packaging converters.

As sustainable packaging adoption accelerates, the shift toward biodegradable, compostable, and renewable laminating adhesive systems is expected to gain rapid momentum. These advancements will not only support brand owners’ net-zero objectives but also redefine adhesive chemistry in the context of green manufacturing, carbon reduction, and sustainable packaging circularity.

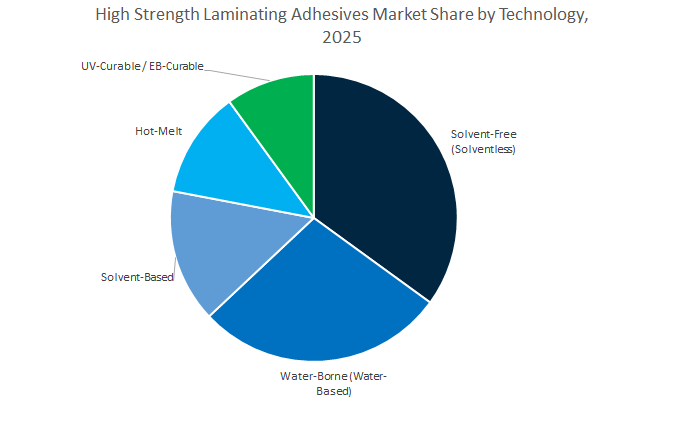

High Strength Laminating Adhesives Market Share Insights, 2025-2034

Solvent-free (solvent-less) laminating adhesives lead with a projected 33.6% share in 2025, reflecting converters’ pivot toward food-contact compliance, low VOCs, and total cost of ownership improvements in high-speed lamination. Their excellent heat/chemical resistance, rapid cure, and low residuals align with brand owners’ sustainability KPIs and global packaging regulations, making them the default in flexible packaging for food, pharma, and personal care. Water-borne systems retain a strong position as plants standardize on environmentally compliant lines for films, foils, and paper, aided by improved blocking resistance and wet-out on multi-substrate stacks. Solvent-based chemistries continue a managed decline, preserved in niche SKUs where extreme adhesion to low-surface-energy films, cold-seal resistance, or long open times are non-negotiable. Meanwhile, hot-melt and UV/EB-curable laminating adhesives expand in fast-cycle and in-line processes, where instant green strength, energy-efficient curing, and tight register control lift throughput and reduce scrap.

Packaging dominates at a projected 46.7% share in 2025, underpinned by flexible packaging growth, mono-material design, and barrier film innovation that demand high-strength, migration-safe bonds across PET/PE, OPP/PE, and foil structures. Performance needs—retort stability, aroma/barrier integrity, and puncture resistance—keep laminating adhesives central to food, pharmaceutical, and consumer goods value chains. Automotive & transportation gains momentum as battery modules, interior laminates, and lightweight composites require fatigue-resistant, temperature-stable bonds. Industrial uses remain resilient across technical textiles, performance tapes, and furniture laminates, where durability and shear retention at load drive selection. Electronics & electrical and building & construction represent specialized, specification-driven niches—optical clarity for displays, dielectric stability, insulation laminates, façade films—that favor precision cure and low shrinkage. Medical/healthcare, while smaller, prioritizes sterilizable packaging and wearables, elevating biocompatible, low-extractable formulations. Shares here closely track sustainability mandates, e-commerce packaging uptick, and lightweighting, anchoring packaging as the volume engine.

The global high-strength laminating adhesives industry is led by Henkel, H.B. Fuller, Arkema (Bostik), BASF, Sika, and Dow, each leveraging unique technologies in polyurethane chemistry, waterborne systems, and structural composites to address both performance and sustainability imperatives.

Henkel continues to lead with its Loctite Liofol range, offering solvent-based, solvent-free, and water-based PU adhesives tailored for food, retort, and peelable laminations. In July 2025, Henkel introduced Loctite Liofol LA 7837/LA 6265, a solvent-free, aliphatic system resistant up to 134°C, optimized for retort pet food packaging. With <0.1% free monomer content, it enables compliance with REACH and FDA standards while boosting production efficiency and sustainability credentials.

H.B. Fuller offers a comprehensive portfolio of PU, epoxy, and hybrid adhesives for flexible packaging and structural laminates. The company is actively expanding its presence in Asia-Pacific and Latin America, targeting industrial lamination, composites, and transportation sectors. Its formulations provide exceptional peel strength and shear resistance, addressing the requirements of durable laminates for automotive and composite panel bonding.

Following the December 2024 acquisition of Dow’s flexible packaging adhesives business, Bostik (Arkema) has become a powerhouse in multi-layer and solvent-free film lamination. The acquisition expands its reach across Europe, Asia, and North America, integrating five manufacturing sites. With its high-strength PU and SMP-based laminating systems, Bostik commands a leading position in food, medical, and industrial packaging adhesives.

BASF leads in Epotal® and Luphen® water-based adhesive systems, specifically engineered for recyclable and compostable packaging. Its recent focus on Epotal ECO 3702 highlights BASF’s commitment to bio-based and circular adhesive technologies. These dispersions are compatible with PLA films and paper, offering superior oxygen barrier and peel strength performance while aligning with EU Green Deal sustainability mandates.

Sika applies its expertise in SikaForce® 2C PU adhesives, Sikaflex® sealants, and SikaPower® epoxy systems to advanced laminating applications across construction, automotive, and industrial composites. Its Purform® polyurethane technology, achieving <0.1% monomeric diisocyanate, demonstrates regulatory foresight under EU REACH. The company’s SmartCore® toughening technology ensures impact durability in metal and composite bonding.

Post-divestiture in May 2024, Dow sharpened its strategic focus on waterborne and acrylic adhesive systems under its MOR-FREE™ and ADCOTE™ brands. These solvent-free laminating adhesives enable high-strength bonding for flexible packaging, labels, and multilayer films, while supporting Dow’s “Decarbonize & Grow” initiative. Its R&D emphasizes advanced polymer architectures and carbon-efficient laminating chemistries.

China holds the largest share of the Asia-Pacific laminating adhesives market, fueled by electric vehicle manufacturing, packaging modernization, and government sustainability policies. As the global hub for EV production—representing nearly 60% of global output in 2023—the country’s adhesive demand is heavily concentrated in battery pack assembly, flame-retardant laminates, and thermal management systems.

Henkel’s €120 million investment in its “Kunpeng” smart manufacturing facility in Yantai Chemical Industry Park exemplifies The industrial acceleration. The new facility focuses on high-strength polyurethane and acrylic-based laminating adhesives, designed for both automotive and electronics applications, and strengthens Henkel’s supply presence in the Chinese and wider Asian markets. Meanwhile, the Ministry of Industry and Information Technology (MIIT) has mandated that 95% of battery materials must be recoverable by 2025, driving R&D into debonding adhesives for easy disassembly and material recovery from EV batteries—an emerging high-value segment for domestic producers.

China’s adhesive manufacturers are also scaling thermally conductive and flame-retardant laminating systems used in battery modules and flexible packaging films, supporting a dual focus on safety and recyclability. The alignment with national carbon-neutrality goals, combined with rapid technological adoption, positions China as a global leader in sustainable, high-performance laminating adhesives across energy storage and packaging value chains.

The United States continues to shape the North American laminating adhesives industry through its deep integration of sustainability-driven innovation, decarbonization initiatives, and flexible packaging modernization. Major players are actively investing in low-carbon feedstock development, recyclable formulations, and compostable adhesive technologies to meet the surging demand from food packaging, automotive, and construction sectors.

Dow and Henkel’s 2025 partnership expansion marks a significant milestone in adhesive decarbonization—introducing renewable electricity and low-carbon inputs into manufacturing while exploring regional production hubs in North America. Similarly, H.B. Fuller launched the RecyClass-certified Flextra® SBA5250 + XA3350 system, a solvent-based laminating adhesive designed for mono-material flexible packaging that supports recyclability under European and U.S. packaging standards. The company also introduced industrially compostable, solventless, and water-based formulations, furthering the transition to a circular packaging economy.

On the R&D front, Henkel’s 70,000-square-foot Technology Center in Bridgewater, New Jersey, serves as a collaborative hub for innovation across 800+ industrial verticals. The facility is dedicated to next-generation laminating adhesives, advanced surface bonding systems, and digital manufacturing integration, accelerating innovation in both packaging and automotive adhesives.

Germany represents the European nucleus of high-performance laminating adhesive innovation, powered by stringent regulatory frameworks and its leadership in advanced packaging and construction materials. The nation’s manufacturers are at the forefront of non-isocyanate polyurethane (PU) and acrylic laminating adhesives that meet EU REACH, Green Deal, and CEFLEX recyclability guidelines.

The introduction of Bostik’s solvent-less SF-2KLF 760 / H330 laminating adhesive in October 2025 showcases Germany’s engineering excellence in high-temperature resistance adhesives for retort packaging applications—withstanding up to 135°C for one hour on demanding substrates like aluminum foil, SiOx, and AlOx-coated films. The innovation not only expands the application window for food packaging adhesives but also supports low-emission, high-durability lamination aligned with EU sustainability mandates.

Germany’s leadership is reinforced by value chain collaboration—exemplified by Bostik’s partnership with Nordmeccanica and Toyo Ink at K Fair 2025, unveiling a mono-material PP retortable pouch designed for circular economy compliance. With a national emphasis on VOC reduction, solvent-free systems, and advanced curing technologies, Germany continues to serve as the European benchmark for high-performance and environmentally compliant laminating adhesives.

Japan’s laminating adhesives market is characterized by its precision manufacturing standards, high-performance polymer chemistry, and focus on automotive and industrial innovation. Polyurethane (PU) adhesives, commanding roughly 26% of the Japanese market, remain dominant due to their superior adhesion strength (≈8.5 N/mm²), wide operating temperature range (−40°C to 100°C), and resilience to vibration and thermal cycling, making them ideal for automotive and electronics applications.

Simultaneously, epoxy-based laminating adhesives are emerging as a fast-growing segment due to their exceptional tensile strength (35–41 N/mm²) and chemical resistance, essential for electric vehicle lightweighting and structural bonding applications. Leading the innovation frontier, Toyo-Morton (Toyo Ink Group) unveiled its ECOAD solvent-free polyurethane laminating adhesives—a next-generation system optimized for industrial and food packaging applications across the Asian market.

Japan’s R&D environment, emphasizing precision bonding and energy efficiency, is increasingly focusing on advanced curing control and green formulations. The enables the country to sustain its reputation as a global technology hub for high-strength, durable, and environmentally responsible laminating adhesives catering to automotive, packaging, and electronics industries.

South Korea’s laminating adhesives industry is rapidly scaling with its EV manufacturing, advanced electronics production, and packaging modernization initiatives. The country’s KRW 63 trillion (USD 48 billion) investment by Hyundai Motor Group through 2025 exemplifies the national commitment to EV mass production, directly driving demand for high-strength polyurethane laminating adhesives used in battery systems, structural bonding, and component insulation.

The VAE/EVA laminating adhesives segment is among the fastest-growing, supported by increasing applications in food and medical packaging, as well as film-to-film lamination in healthcare disposables. The nation’s dominance in semiconductor and display technology further propels the use of optically clear adhesives (OCAs)—critical in smartphones, OLED panels, and flexible displays—demonstrating South Korea’s convergence of electronic miniaturization and material innovation.

The country’s export-driven industrial base, combined with robust R&D collaboration among conglomerates (LG Chem, SKC, Samsung SDI), underpins its transformation into a regional center for next-generation structural and laminating adhesive solutions. As Korea continues to expand its advanced materials and clean-energy manufacturing ecosystem, it solidifies its role as a global leader in performance adhesives tailored for EVs, electronics, and smart packaging.

High Strength Laminating Adhesives Market Report Scope

High Strength Laminating Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3 Billion

|

|

Market Size (2034)

|

$4.9 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Resin Type (Polyurethane, Acrylic, Epoxy, Ethylene-Vinyl Acetate, Polyolefin, Other Resin Chemistries), By Technology (Solvent-Based, Solvent-Free, Water-Borne, Hot-Melt, UV-Curable / EB-Curable), By End-User (Packaging, Automotive & Transportation, Industrial, Electronics & Electrical, Building & Construction, Medical/Healthcare

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, The Dow Chemical Company, Arkema, 3M Company, Toyo Ink Group, Sika AG, DIC Corporation, Ashland Global Holdings Inc., COIM Group, DuPont de Nemours, Inc., Mapei S.p.A., BASF SE, ThreeBond Holdings Co., Ltd., Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Polyurethane

- Acrylic

- Epoxy

- Ethylene-Vinyl Acetate

- Polyolefin

- Other Resin Chemistries

By Technology

- Solvent-Based

- Solvent-Free

- Water-Borne

- Hot-Melt

- UV-Curable / EB-Curable

By End-Use Industry

- Packaging

- Automotive & Transportation

- Industrial

- Electronics & Electrical

- Building & Construction

- Medical/Healthcare

By Packaging Application Subtype

- Food Packaging

- Beverage Packaging

- Medical Packaging

- Industrial Packaging

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- The Dow Chemical Company

- Arkema

- 3M Company

- Toyo Ink Group

- Sika AG

- DIC Corporation

- Ashland Global Holdings Inc.

- COIM Group

- DuPont de Nemours, Inc.

- Mapei S.p.A.

- BASF SE

- ThreeBond Holdings Co., Ltd.

- Huntsman Corporation

*- List not Exhaustive

Research Coverage

Developed for senior decision-makers, engineers, and sourcing leaders, this USDAnalytics study on the High Strength Laminating Adhesives Market delivers a single-source view that connects technology, regulations, and end-use adoption: this report investigates how solvent-free, water-borne, and ultra-low-monomer polyurethane (PU) platforms are reshaping retort packaging, medical films, industrial composites, and structural laminates; maps breakthroughs in retort-durable chemistry, high-barrier lamination, and fast-cure processing; analysis reviews competitive moves, portfolio realignments, and specification shifts (food-contact, REACH, FDA); and highlights productivity gains from oven-less processes, carbon-footprint reductions, and T-Peel (ASTM D1876) performance benchmarks across demanding thermal/cryogenic cycles. Built to support portfolio strategy, plant conversions, and qualification roadmaps, this report is an essential resource for packaging converters, CPG owners, film manufacturers, automotive and electronics integrators, and investors requiring evidence-based insights on durability, sterilization resistance, migration safety, and circular-ready laminate designs.

Scope Highlights

Segmentation

- By Resin Type: Polyurethane; Acrylic; Epoxy; Ethylene-Vinyl Acetate; Polyolefin; Other Resin Chemistries

- By Technology: Solvent-Based; Solvent-Free; Water-Borne; Hot-Melt; UV-Curable / EB-Curable

- By End-Use Industry: Packaging; Automotive & Transportation; Industrial; Electronics & Electrical; Building & Construction; Medical/Healthcare

- By Packaging Application Subtype: Food Packaging; Beverage Packaging; Medical Packaging; Industrial Packaging

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Time Horizon: Historic data 2021–2024; forecasts 2025–2034.

Companies: Analytical coverage and profiles of 15+ manufacturers and solution providers (list not exhaustive).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.