Market Overview: High Temperature Fibers Enabling Extreme-Performance Aerospace, Industrial & Thermal Systems

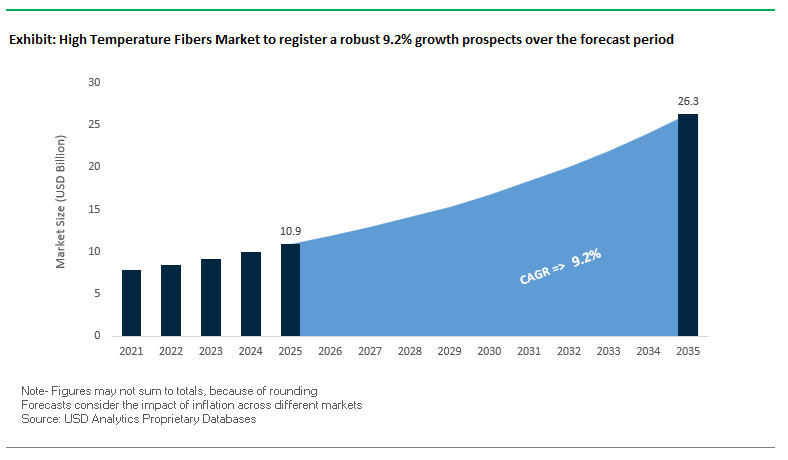

The High Temperature Fibers Market is projected to grow from USD 10.9 billion in 2025 to USD 26.3 billion by 2035, reflecting a strong CAGR of 9.2%. Market expansion is fueled by rising adoption of Ceramic Matrix Composites (CMCs), polyimide fibers, SiC fibers, alumina fibers, and carbon–carbon composites (C/C) in aerospace engines, industrial furnaces, automotive thermal protection systems, and high-temperature filtration. Manufacturers increasingly rely on ultra-high thermal stability, chemical resistance and low mass to meet next-generation engineering demands.

High-temperature fiber adoption is particularly strong in jet engine hot sections, where SiC-based CMC components now reliably operate above 1,300°C, enabling superior thrust-to-weight ratios and improved fuel efficiency. Meanwhile, advancements such as SiC-coated carbon fibers maintaining stability beyond 700°C in oxygen are expanding the market into mid-to-high temperature structural applications once dominated by metals and superalloys. In ultra-extreme environments—such as re-entry vehicles—C/C composites with UHTC coatings demonstrate ablation rates as low as 1.30 μm/s, setting new benchmarks for thermal protection systems.

Industries undergoing energy transitions—particularly metals, petrochemicals, cement and ceramics—are adopting High-Temperature Insulation Wools (HTIWs) at scale. These materials can reduce furnace lining weight by up to 80%, substantially cutting energy consumption and shortening thermal cycle times.

Key Insights for Manufacturers & Vendors

- SiC-CMC adoption accelerating: Aerospace engine makers are transitioning from superalloys to ceramic matrix composites for 1,300°C+ performance.

- Advanced oxidation-resistant fibers emerging: SiC-coated carbon fibers remain structurally intact at >700°C, unlocking new multi-material hybrid systems.

- Defense & space expansion: UHTC-coated C/C composites withstand extreme ablation environments, driving use in hypersonics and re-entry vehicles.

- Industrial insulation transformation: HTIW reduces furnace lining weight by 80%, driving energy efficiency initiatives globally.

Market Analysis: Strategic Expansions, Material Breakthroughs & Regulatory Shifts Reshaping High-Temperature Fiber Supply Chains

The High Temperature Fibers Industry continues to evolve through capacity expansions, research-driven material innovations, recycling advancements, and regulatory responses across North America, Europe and Asia. In September 2025, RATH Group opened a new joint venture plant in Visakhapatnam, India, expanding its ceramic fiber production base to meet rapidly rising Asian industrial furnace demand. This was complemented by June 2025’s launch of ALTRA FLEX®, Europe’s first oxide ceramic continuous fiber, strategically establishing RATH as a regionally independent supplier amid tightening supply security concerns. Similarly, in May 2025, RATH debuted ALTRA® 1500C, a non-classified polycrystalline insulation wool targeted at steel producers seeking lightweight, energy-optimized refractory solutions.

Breakthroughs in sustainable high-temperature materials are reshaping supply chains. In March 2025, researchers demonstrated carbothermal reduction as an effective route to produce uniform SiC coatings on recycled carbon fibers, unlocking cost-effective circular pathways for high-temperature composite applications. This development positions recycling as a future competitive differentiator, reducing both cost and carbon footprint in industries where fiber costs are traditionally high. Additionally, February 2025 marked growing aerospace adoption of Titanium Aluminide (TiAl) and advanced nickel superalloys reinforced with high-temperature fibers, solidifying their role in next-generation jet engine blades and high-efficiency propulsion systems.

Regulatory and safety-driven shifts are also influencing market direction. Throughout Q3 2024, North American and European producers significantly accelerated development and commercialization of Low Bio-Persistent (LBP) Ceramic Fibers in response to increasingly stringent worker exposure limits. Meanwhile, in November 2024, Honeywell reaffirmed strategic emphasis on its Spectra® UHMWPE fiber for non-flammable protective textiles and armor, signaling widening adoption of high-temperature-resistant ballistic and industrial safety materials.

Breakthrough Trends and Strategic Opportunities Reshaping the High-Temperature Fibers Market

Market Trend 1: Qualification of Alumina and Mullite Oxide Fibers for 1,150–1,200°C CMC Hot-Section Components in Next-Generation Jet Engines

A defining transformation in the high-temperature fibers market is the rapid qualification of oxide fibers—primarily alumina and mullite—as reinforcements for oxide–oxide ceramic matrix composites (O-CMCs) used in advanced aerospace propulsion systems. These fibers enable CMC hot-section components to operate at 1,150°C continuously and up to 1,200°C during short-term thermal spikes, exceeding the capability of air-cooled nickel-based superalloys that require heavy cooling schemes beyond 1,000°C.

O-CMCs exhibit exceptional oxidation resistance, maintaining chemical and structural stability even in high-humidity, oxygen-rich atmospheres, eliminating the need for complex Environmental Barrier Coatings (EBCs) required by SiC/SiC counterparts. Their quasi-ductile damage behavior—reflected in strain-to-failure values up to 0.6% versus <0.1% for monolithic ceramics—prevents catastrophic failure modes and dramatically improves in-engine safety margins. With densities one-third that of high-temperature steels and superalloys, oxide-fiber-reinforced CMCs enable turbine manufacturers to achieve significant engine weight reduction, enhance thrust-to-weight ratio, and improve mission fuel efficiency. These combined material attributes make oxide fibers a central pillar in the development of next-generation civil and military propulsion systems with higher firing temperatures and reduced cooling penalties.

Market Trend 2: Adoption of Silica and High-Silica Fibers for Thermal Runaway Propagation (TRP) Mitigation in Lithium-Ion Battery Modules

As energy storage systems become more power-dense, silica-based high-temperature fibers are emerging as essential thermal barriers for EV batteries, stationary ESS modules, and aerospace lithium-ion packs. Reinforced silica aerogels and high-silica fiber composites maintain extremely low thermal conductivity—below 0.116 W/(m·K)—even when exposed to 900°C cell-to-cell heat flux. This allows insulating layers as thin as 1.5–3 mm to delay TR propagation from under 1 minute to up to 26.4 minutes, fundamentally reshaping pack-level safety strategies.

These materials retain structural integrity when exposed to thermal runaway temperatures up to 1,405°C, outperforming polymer or mica-based insulation. Cutting-edge silica composites are also engineered for dynamic adiabatic transition, shifting from a conductive state (1.33 W/(m·K)) to an insulating state (≈0.1 W/(m·K)) in just 30 seconds when heated to ~100°C. This adaptive behavior is critical for next-generation pack designs seeking automatic thermal isolation responses during abuse events. As regulators worldwide mandate stricter TRP limits, silica and high-silica fibers are being rapidly adopted across EVs, e-mobility, grid storage, and aerospace batteries.

Market Opportunity 1: Engineering of PBI and PBO High-Temperature Fibers for HT-PEM Fuel Cells Operating at 160–200°C

The shift toward higher-efficiency industrial, automotive, and aerospace fuel cells is generating strong demand for polybenzimidazole (PBI) and poly(p-phenylene-2,6-benzobisoxazole) (PBO) high-temperature fibers within HT-PEM fuel cell membranes, gaskets, and structural components. Phosphoric-acid-doped PBI membranes reach proton conductivity values of 0.13–0.25 S/cm at 160–180°C under anhydrous conditions—performance that meets or exceeds DOE criteria for next-generation HT-PEM systems.

Durability metrics also validate PBI’s suitability: thermally cured PBI membranes show a low voltage decay rate of 43 mV per 1,000 hours at 160°C, signaling long-term chemical stability. Their material robustness is rooted in a glass transition temperature >350°C and decomposition temperature >600°C, enabling full mechanical and structural compliance with the acidic, high-temperature fuel cell environment. PBI’s capacity to absorb phosphoric acid up to 2.5× its weight (≈5 H₃PO₄ molecules per repeating unit) directly correlates to enhanced ionic mobility, providing a technology pathway for durable, high-efficiency HT-PEM stacks used in heavy-duty mobility, aerospace APU systems, and industrial micro-CHP.

Market Opportunity 2: Valorization of Basalt Fiber as a Cost-Efficient, Non-Combustible Reinforcement for High-Temperature Infrastructure and Construction Composites

Basalt fiber presents one of the strongest opportunities for cost-effective high-temperature reinforcement across construction, transportation, and fire-critical infrastructure. With an operational range from –260°C to 600°C and short-term tolerance up to 1,000°C, basalt fibers outperform many synthetic fibers and provide a unique balance of cost, fire resistance, and thermal stability.

Mechanical integrity is retained at high temperatures—basalt fiber preserves 80% of its strength at 600°C and maintains ≈150 MPa residual tensile strength at that temperature, offering a safer stiffness–strength profile compared to traditional polymer-based fibers. In structural concretes, basalt reinforcement results in only 1.4% compressive strength loss after 400°C exposure and retains 73% strength at 600°C, enabling fire-resistant designs for tunnels, bridges, and high-rise construction.

Critically, basalt fiber is fully non-combustible, enabling composites to meet Fire Safety Class A1, the highest European non-combustibility rating. With no toxic gas evolution, molten dripping, or particulate emission during fire exposure, basalt fiber is rapidly emerging as a preferred sustainable alternative to glass fibers and steel meshes in fire-critical civil engineering applications.

High Temperature Fibers Market Share Analysis

Market Share by Fiber Type: Ceramic Fibers Lead Due to Their Dominance in Ultra-High-Temperature Insulation Applications

Ceramic fibers hold the largest share of the global high-temperature fibers market—approximately 40% in 2025—because they remain the backbone material for thermal insulation systems operating at temperatures far beyond the capabilities of polymeric or conventional inorganic fibers. Their ability to withstand continuous service temperatures of 1,000°C to over 1,430°C, combined with exceptionally low thermal conductivity, makes them indispensable in high-temperature industrial equipment such as reheating furnaces, rotary kilns, glass melting tanks, boilers, and petrochemical cracking units. Unlike dense refractory bricks, ceramic fibers offer dramatically lower heat storage and reduced thermal mass, enabling faster thermal cycling and significant operational energy savings—often 18–28% lower heat loss compared to legacy insulation materials. Their wide availability in high-volume formats such as blankets, felts, boards, vacuum-formed shapes, and modular linings ensures scalable adoption across diverse industries. Furthermore, regulatory and operational pressures to improve energy efficiency and reduce carbon emissions reinforce the shift from older refractory technologies toward advanced ceramic fiber solutions. As industries intensify their modernization efforts, ceramic fibers maintain their leadership position thanks to their mature manufacturing base, performance consistency, and indispensability in extreme-temperature environments where no alternative material class offers equivalent performance.

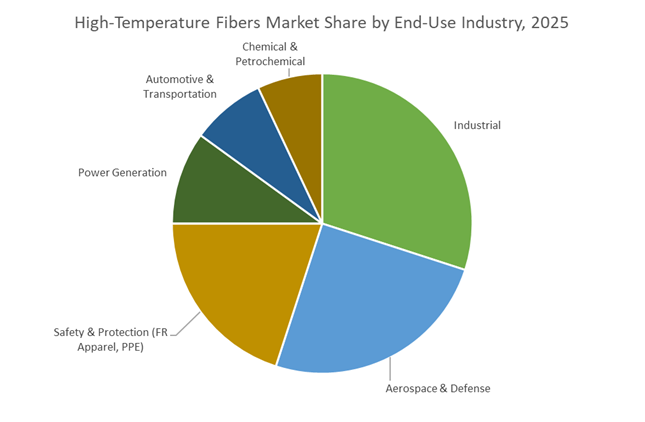

Market Share by End-Use: Industrial Sector Dominates Due to Its Heavy Dependence on High-Temperature Processing

The Industrial sector—encompassing iron and steel, petrochemicals, refining, cement production, non-ferrous metallurgy, and glass processing—holds the largest end-use share at around 30% in 2025, driven by its reliance on sustained, high-temperature operations central to global manufacturing. These industries operate continuous furnaces, reactors, reformers, ladles, and kilns that routinely exceed 1,000°C and therefore require reliable, high-performance thermal insulation to maintain operational efficiency and equipment life. The steel sector alone represents one of the largest consumers of ceramic fibers worldwide, with widespread deployment in tundishes, reheating furnaces, and ladle linings due to the need for ultra-high-temperature stability and rapid thermal response. Similarly, the refining and petrochemical industries use ceramic fibers extensively across radiant sections, process heaters, and thermal reactors to minimize heat loss, ensure chemical reaction stability, and meet strict emissions-reduction targets. As global decarbonization initiatives push energy-intensive sectors to modernize heat-management systems, ceramic fiber-based solutions are increasingly favored for their ability to reduce fuel consumption and improve thermal efficiency. The continuous maintenance cycles, periodic relining projects, and the global surge in capacity expansion ensure sustained, high-volume demand—cementing the Industrial sector’s position as the dominant end-use market for high-temperature fibers.

Country Analysis: Global High Temperature Fibers Hotspots Anchoring Aerospace, Industrial Insulation, and Extreme-Temperature Material Innovation

United States: SiC Fiber Leadership, CMC Expansion, and Next-Gen Polyimide Development for Extreme Heat Applications

The United States remains the global epicenter for high-temperature aviation materials, driven by unmatched commercial aerospace investments and continuous military modernization programs. The country leads in advancing Silicon Carbide (SiC) fibers and Ceramic Matrix Composites (CMCs)—materials that now replace heavy nickel superalloys in the LEAP and GE9X engine platforms, enabling unprecedented thermal resistance and fuel efficiency. GE Aerospace’s continued integration of SiC fiber-reinforced CMCs into hot-section components sets a global benchmark, positioning the U.S. as the foremost innovator in engine-grade HTF applications. Simultaneously, major materials companies such as 3M are expanding their high-temperature portfolio, prominently featuring the Nextel™ polycrystalline ceramic fiber line, capable of handling up to 2,372°F (1,300°C) for firewall, gasket, and aerospace insulation applications.

Defense priorities further amplify U.S. HTF demand. The Department of Defense continues to fund advanced polyimide (PI), PBI, and PBO fibers for astronaut suits, thermal protective systems in armored vehicles, and heat-shield components in hypersonic programs due to their exceptional flame and chemical resistance. The U.S. Department of Energy also plays a fundamental role, directing R&D investment toward scalable, cost-efficient SiC fiber manufacturing to support next-generation nuclear reactor designs, including fusion concepts. Beyond aerospace and defense, the rapid expansion of the U.S. Electric Vehicle (EV) industry drives strong growth in high-temperature glass fibers and meta-aramids used in battery fire shields, separators, and thermal runaway mitigation systems—solidifying the U.S. as a diversified powerhouse in high-temperature fiber technology.

Japan: Global Leader in SiC Fiber Engineering, Advanced Aramid Innovations, and Ultra-High-Performance Industrial HTF Materials

Japan maintains a commanding global leadership position in Silicon Carbide (SiC) fiber production, specialty aramid innovation, and advanced polymeric fibers engineered for extreme thermal environments. Companies such as UBE Corporation continue expanding SiC fiber production capacity to meet sharply rising global demand from aerospace engine manufacturers and gas turbine OEMs. These fibers, prized for exceptional creep resistance at ultra-high temperatures, remain central to Japan’s dominance in high-temperature composite systems. In the high-performance aramid space, Teijin Limited advances the HTF market with new variants of its Teijinconex® meta-aramid designed to withstand high temperature and high-pressure industrial filtration environments, strengthening Japan’s footprint in specialized PPE, flue-gas filtration, and heavy industrial applications.

Japan’s material ecosystem is deeply supported by strong academic–industry collaboration. Research institutions across the country are developing high-purity alumina fibers capable of functioning beyond 3,000°F (1,650°C) in vacuum furnaces and semiconductor thermal processing systems—critical technologies for Japan’s world-leading semiconductor supply chain. Furthermore, Japanese producers are innovating high-temperature variants of polyketone (PK) and polyphenylene sulfide (PPS) fibers to meet rising demand for chemical-resistant HTF products used in incineration plants, power generation, and industrial boilers. Japan’s integrated approach—from fiber precursor engineering to finished thermal insulation fabrics—positions it as a global benchmark for ultra-high-performance HTF technology.

China: Massive Scale-Up in Refractory Ceramic Fiber (RCF), Biosoluble Fiber, and Industrial Thermal Protection Materials

China is undergoing one of the world’s fastest expansions in refractory ceramic fiber (RCF) and Low Biopersistent (LBP) biosoluble fiber production, driven by its enormous steel, cement, glass, and ceramics industries. Domestic manufacturers have invested heavily in scaling output of ceramic fiber blankets, boards, and modules to meet furnace lining and industrial insulation demand—sectors undergoing aggressive modernization supported by national energy-efficiency mandates. This industrial push aligns with China’s policy to replace outdated refractory materials with high-performance ceramic fibers that offer superior insulating efficiency, lower emissions, and reduced operational costs.

The Chinese government’s strong emphasis on environmentally responsible industrial materials is also accelerating the transition toward biosoluble LBP fibers, manufactured using calcium–magnesium–silicate chemistries that comply with international occupational health standards. As Chinese industries shift toward cleaner technologies, demand is rising for high-temperature fabrics, woven tapes, and insulation wraps across the automotive, machinery, and heavy equipment sectors. This surge supports the country’s growing focus on thermal protection solutions for exhaust systems, turbocharger insulation, industrial gaskets, and high-temperature machinery reinforcement—reinforcing China’s status as the global production engine for industrial-grade HTFs.

Germany: European Center for Low-Bio-Persistence Fibers, Automotive High-Temperature Composites, and Advanced Industrial Thermal Insulation

Germany stands as the European Union’s leading hub for industrial thermal management materials, specializing in Low Bio-Persistence (LBP) ceramic fibers, high-silica thermal textiles, and advanced high-temperature glass fiber systems. German manufacturers are global leaders in biosoluble ceramic fiber production, benefiting from stringent EU worker-safety and carcinogenicity regulations that require high-performance yet environmentally compliant HTFs in industrial furnaces, chemical plants, and petrochemical refineries. This regulatory environment has catalyzed rapid adoption of next-generation ceramic insulation products across European heavy industry.

The German automotive sector is a major consumer of high-temperature fibers, integrating high-silica fiber mats, high-temperature glass fibers, and ceramic-based insulation into under-the-hood thermal barriers for ICE and hybrid vehicles. Federal and industrial R&D consortia are further advancing the HTF landscape through the development of silica aerogels and high-purity alumina fibers designed for compact electric motor insulation, battery fire protection layers, and lightweight EV thermal systems. Germany’s strong composite recycling initiatives and its long-standing industrial fiber expertise make it a central player in shaping the future of European HTF demand.

South Korea: Expanding Polymeric HTF Capacity for Electrical Insulation, Protective Apparel, and Defense Applications

South Korea’s High Temperature Fibers Market is rapidly evolving due to strategic expansion in meta-aramid and para-aramid fiber production, led by manufacturers such as Kolon Industries. The country is investing heavily in developing aramid fibers with improved UV resistance, dyeability, and mechanical stability to meet stringent performance requirements across industrial PPE, aerospace insulation, and high-heat filtration environments. South Korea’s robust electronics manufacturing sector creates a parallel surge in demand for aramid paper, polyimide films, and high-temperature electrical insulation materials, essential for motors, transformers, and printed circuit boards.

Defense modernization also plays a pivotal role in shaping Korea’s HTF trajectory. The shipbuilding, naval systems, and ballistic protection sectors require high-modulus aramid fibers and thermally resistant polymers to produce flame-resistant apparel, high-heat cable insulation, and advanced armor composites. This dual industrial–defense demand underpins Korea’s strategy to reduce import dependence and establish itself as a regional leader in polymeric high-temperature fibers.

India: Government-Led Expansion in Technical Textiles and High-Temperature Fiber Self-Reliance

India is rapidly strengthening its domestic ecosystem for high-performance technical textiles, propelled by strong central government initiatives aimed at reducing dependency on imported high-temperature fibers. The Production Linked Incentive (PLI) Scheme for Technical Textiles incentivizes the development of high-performance MMF-based products, including industrial filtration fibers, flame-resistant textiles, and protective apparel materials. This policy framework is accelerating capital investment and technology absorption across Indian fiber and textile manufacturing.

Strategic procurement initiatives from Indian defense agencies are reinforcing demand for indigenized aramid fibers used in ballistic helmets, bulletproof jackets, and armored vehicle composites—sectors previously dependent on imported HTFs. Meanwhile, India’s infrastructure megaprojects under the GATI SHAKTI program are fueling significant consumption of high-temperature glass fibers and high-silica textiles for fire protection systems, civil engineering reinforcement, and thermal insulation in industrial installations. These combined forces position India as a rising, strategically aligned contributor to the global HTF supply chain.

Competitive Landscape: Global Leaders Advancing Ceramic, Polyimide & Ultra-High-Temperature Fiber Technologies

The competitive landscape of the High Temperature Fibers Market is defined by a mix of ceramic fiber specialists, refractory technology leaders, advanced composite suppliers and insulation innovators. Companies differentiate through material purity, temperature capability, regulatory compliance, and integrated supply chain solutions. Many are expanding capabilities into 1,300–1,800°C applications, aerospace-grade composites, and next-generation industrial thermal systems.

Morgan Advanced Materials – Leadership in Low Bio-Persistent Ceramic Fiber Solutions

Morgan Advanced Materials is a pioneer in Low Bio-Persistent (LBP) fibers, primarily through its Superwool® product line, which meets strict European and North American occupational health regulations while offering operating temperatures up to 1,300°C. The company also produces Kaowool® ceramic fibers, supplying high-temperature thermal management systems to metals, power generation and petrochemical industries. Morgan’s emphasis on regulatory-compliant, energy-efficient insulation systems strengthens its role as a preferred vendor for industrial safety and sustainability-focused clients.

RATH Group – Establishing European Self-Sufficiency in Oxide Ceramic Continuous Fibers

RATH Group has emerged as a strategic force in European high-temperature fiber production with the launch of ALTRA FLEX®, the region’s first domestically produced oxide ceramic continuous fiber. This reduces reliance on Asian imports for critical composite reinforcement materials. Additionally, its ALTRA® high-temperature insulation wool and vertically integrated refractory systems support industrial applications up to 1,800°C. With new production capacity added in Visakhapatnam, India, RATH is expanding its footprint across Asia while strengthening its position as a specialized refractory-solutions provider.

3M Company – High-Temperature Ceramic Oxide Fibers for Aerospace & Defense

3M’s Nextel™ ceramic oxide fibers are engineered for applications requiring prolonged thermal stability at up to 1,600°C, making them core materials in aerospace exhaust systems, thermal protection layers and fire barriers. 3M also converts these fibers into fabricated textile forms such as woven cloth and sleeving, enabling flexible design integration for advanced insulation and reinforcement. Its leadership in high-temperature textile engineering secures strong demand across defense, aerospace and industrial high-heat environments.

Toray Industries – Polyimide & Carbon Fiber Composite Leadership for High-Temperature Structures

Toray Industries leverages its global carbon fiber leadership to deliver advanced polyimide-based fibers (TOYOBO K-6®) and high-temperature CFRP solutions using PI and BMI matrices. These materials enable structural integrity in demanding environments such as aerospace filtration, high-temperature protective apparel and elevated-temperature composite structures. Toray’s integrated composite value chain—from precursor production to high-performance laminate manufacturing—positions it as a leading supplier for next-generation thermal and structural applications.

Unifrax (Lydall/Unifrax) – High-Purity Alumina & Advanced Industrial Insulation Solutions

Unifrax offers a broad portfolio of High-Temperature Insulation Wool (HTIW), including Fiberfrax®, Isofrax® (LBP fiber), and Saffil® alumina fiber, which is designed for extreme conditions nearing 1,600°C. These materials are widely deployed in catalytic converters, high-temperature filtration, metal processing, and industrial furnace insulation. With its expansive global manufacturing footprint, Unifrax ensures high supply reliability for large-scale industrial customers requiring consistent, high-performance thermal insulation systems.

High Temperature Fibers Market Report Scope

High Temperature Fibers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.9 Billion

|

|

Market Size (2035)

|

$26.3 Billion

|

|

Market Growth Rate

|

9.2%

|

|

Segments

|

By Fiber Type (Ceramic Fibers, Silicon Carbide Fibers, Aramid Fibers, High-Temperature Polymer Fibers, High-Temperature Inorganic Fibers), By Form (Blankets & Boards, Textiles, Yarns & Roving, Modules & Papers), By End-Use Application (Aerospace & Defense, Automotive & Transportation, Industrial, Chemical & Petrochemical, Power Generation, Safety & Protection)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M, DuPont, Morgan Advanced Materials, Teijin, Toray, Unifrax, UBE, Vesuvius, Kolon Industries, Ahlstrom, COI Ceramics, Isolite Insulating Products, Yantai Tayho, Mitsubishi Chemical Group, Evonik

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High Temperature Fibers Market Segmentation

By Fiber Type

- Ceramic Fibers

- Silicon Carbide (SiC) Fibers

- Aramid Fibers

- High-Temperature Polymer Fibers

- High-Temperature Inorganic Fibers

By Form

- Blankets & Boards

- Textiles

- Yarns & Roving

- Modules & Papers

By End-Use Industry

- Aerospace & Defense

- Automotive & Transportation

- Industrial

- Chemical & Petrochemical

- Power Generation

- Safety & Protection (Fire-Resistant Apparel, PPE)

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in High Temperature Fibers Market

- 3M

- DuPont

- Morgan Advanced Materials

- Teijin

- Toray

- Unifrax

- UBE

- Vesuvius

- Kolon Industries

- Ahlstrom

- COI Ceramics

- Isolite Insulating Products

- Yantai Tayho

- Mitsubishi Chemical Group

- Evonik.

*- List not Exhaustive

Research Coverage: High Temperature Fibers Market

The latest High Temperature Fibers Market study from USDAnalytics provides an end-to-end strategic view of how ceramic fibers, SiC fibers, aramids, high-temperature polymer fibers and inorganic fibers are reshaping extreme-temperature aerospace, industrial and energy systems. Drawing on detailed quantitative modeling and qualitative insights, this report investigates the shift from conventional refractories and superalloys toward CMCs, HTIWs, oxide fibers and advanced thermal barriers in jet engines, industrial furnaces, EV battery safety, hypersonics and fuel cells. It examines technology breakthroughs such as oxide–oxide CMCs operating beyond 1,150–1,200°C, SiC-coated carbon fibers for hybrid composites, silica fiber TRP barriers for lithium-ion packs, and emerging PBI/PBO solutions for HT-PEM stacks, while assessing their cost, manufacturability, and regulatory compliance. The study’s analysis reviews capacity expansions in ceramic and biosoluble fibers, recycling routes for SiC-coated recycled carbon fibers, and the pivot toward Low Bio-Persistent (LBP) products under tightening occupational exposure limits. It further highlights regional hot spots across the U.S., Japan, China, Germany, South Korea and India, maps capex, and benchmarks leading players in ceramic fibers, oxide continuous fibers, HT polymer fibers and alumina systems on temperature capability, form factors and target verticals. With integrated coverage of demand by fiber type, form, and end-use, alongside policy, safety and decarbonization impacts, this report is an essential resource for materials strategists, R&D leaders, procurement heads, and investors looking to position competitively in the global High Temperature Fibers Market through 2034.

Scope Highlights

- Segmentation:

By Fiber Type – Ceramic Fibers, Silicon Carbide (SiC) Fibers, Aramid Fibers, High-Temperature Polymer Fibers, High-Temperature Inorganic Fibers

By Form – Blankets & Boards, Textiles, Yarns & Roving, Modules & Papers

By End-Use Industry – Aerospace & Defense, Automotive & Transportation, Industrial, Chemical & Petrochemical, Power Generation, Safety & Protection (Fire-Resistant Apparel, PPE)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, capturing region-specific regulations, industrial structures, and capex in high-temperature processing and aerospace programs.

- Time Frame: Includes historic data from 2021 to 2025 and forecast data from 2026 to 2034, enabling long-range planning for engine platforms, furnace relining cycles, and next-generation thermal protection initiatives.

- Companies Covered: In-depth analysis/profiles of 15+ companies, including ceramic fiber specialists, oxide fiber innovators, HT polymer leaders and CMC integrators, covering product portfolios, temperature ranges, recent investments, and strategic positioning.