Industrial and Institutional Cleaning Chemicals Market to Reach $162.6 Billion by 2034 at 7.5% CAGR Driven by Water Circularity, Green Surfactants, and Institutional Hygiene Innovation

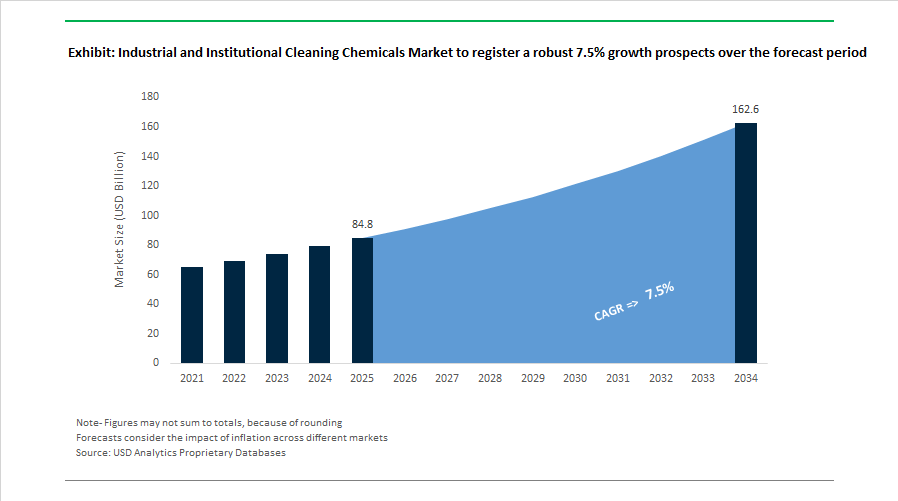

The Industrial and Institutional (I&I) Cleaning Chemicals Market is projected to grow from $84.8 billion in 2025 to $162.6 billion by 2034, registering a strong CAGR of 7.5%. Expansion is being fueled by heightened hygiene protocols across healthcare, hospitality, food processing, manufacturing, and commercial facilities, alongside structural shifts toward biodegradable surfactants, low-temperature enzymatic cleaning, and digital water management solutions. The market increasingly integrates specialty surfactants, liquid enzymes, disinfectants, degreasers, alkoxylates, alpha olefin sulfonates (AOS), and concentrated pod technologies designed to reduce carbon footprint and packaging waste.

In June 2024, Solenis acquired Aqua ChemPacs, a specialist in dissolvable, pre-portioned cleaning pods that enable on-site dilution and significantly reduce plastic packaging and freight emissions. In the first half of 2025, Stepan Company operationalized its new alkoxylation facility in Pasadena, Texas, strengthening North American surfactant supply for industrial degreasers and commercial laundry formulations. In June 2025, Stepan further expanded capacity with a 25% increase in Alpha Olefin Sulfonates production, supporting demand for high-foaming, biodegradable surfactants used in vehicle wash systems and institutional detergents. In July 2025, BASF launched three new liquid enzymes—Lavergy L Pace, Lavergy C Care, and Lavergy A Star—engineered to deliver effective stain removal at low wash temperatures, aligning with decarbonization goals in commercial laundries and food-service kitchens. In September 2025, CloroxPro introduced Screen+ Sanitizing Wipes, addressing the hygiene gap in tech-heavy workplaces by enabling residue-free disinfection of sensitive electronic screens.

Strategic consolidation accelerated in late 2025. On November 3, 2025, Solenis finalized its merger with NCH Corporation, expanding its industrial water treatment and maintenance chemical footprint to more than 160 countries with approximately 23,000 employees. In November 2025, Ecolab expanded its professional-grade cleaning portfolio into The Home Depot Canada, targeting contractors and mid-sized institutional buyers. During the same month, BASF hosted its Care 360 Sustainability Days, focusing on Product Carbon Footprint transparency and high-biodegradability formulations for I&I detergents and degreasers. In late 2025, Ecolab completed its acquisition of Ovivo Electronics, and by February 2026 confirmed that the transaction doubled the size of its Global High-Tech division, creating a closed-loop water circularity platform for semiconductor and microelectronics manufacturing.

Sustainability leadership and digital benchmarking became central differentiators entering 2026. In January 2026, Ecolab partnered with CDP to establish water performance benchmarking standards for food processing, hospitality, and other water-intensive industries. In February 2026, Henkel received the American Cleaning Institute Sustainability Spotlight Award, highlighting progress toward a 30% Scope 3 emissions reduction target by 2030. The industrial and institutional cleaning chemicals market is increasingly defined by integrated water management systems, enzyme-enabled low-energy cleaning, green surfactant capacity expansion, dissolvable concentrate technologies, and sustainability-driven procurement standards across global institutional supply chains.

Industrial and Institutional Cleaning Chemicals Market Trends and Opportunities

Migration to Cost-per-Clean Models Through Closed-Loop Dispensing Systems

The industrial and institutional cleaning chemicals market is undergoing a structural shift from volume-driven sales toward performance-based procurement models. Large institutional buyers across hospitality, healthcare, food processing, and contract cleaning are increasingly standardizing on cost-per-clean metrics enabled by closed-loop, automated dispensing systems. This transition is directly linked to corporate decarbonization strategies and Science Based Targets initiative alignment, as chemical overuse and inefficient dilution are now recognized as material Scope 3 emission contributors.

In 2025, multinational buyers reported that ultra-concentrated I&I cleaning formulations paired with precision dosing reduced packaging waste by up to 80% while cutting transportation emissions by roughly 40% per unit of active chemistry delivered. The shift toward monolayer polyethylene refill pouches has further improved recyclability, helping major suppliers raise recycled plastic content to more than 20% of total packaging portfolios. From an operational standpoint, IoT-enabled dispensing platforms are delivering measurable efficiency gains. Audits conducted in institutional kitchens and hospitals show that automated dosing eliminates 15 to 25% of chemical wastage typically caused by manual dilution, translating directly into lower total cost of ownership and improved compliance with internal sustainability KPIs.

Regulatory Substitution of Quaternary Ammonium Compounds With Oxidative Chemistries

Regulatory scrutiny of quaternary ammonium compounds is accelerating a second major inflection point in the I&I cleaning chemicals market. Environmental persistence concerns and growing evidence of respiratory sensitization have triggered intensified evaluations of widely used actives such as benzalkonium chloride and DADMAC, particularly in North America and the European Union. As of 2025, this has translated into a rapid substitution cycle favoring oxidative chemistries with more favorable toxicological and environmental profiles.

Healthcare and public facilities in regulated jurisdictions are increasingly transitioning toward peracetic acid, accelerated hydrogen peroxide, citric acid, and lactic acid based formulations. In California alone, state-level oversight drove a reported 35% increase in the adoption of peroxide and peracid disinfectants across hospitals and long-term care facilities. Parallel developments in Europe, aligned with evolving biocidal and persistent pollutant frameworks, are reinforcing this shift by prioritizing active ingredients listed under safer chemistry programs.

Operational data from 2025 indicate that facilities replacing quats with stabilized oxidative systems achieved a 20% reduction in reported skin and respiratory irritation incidents among cleaning staff. This health and safety dimension is becoming a decisive procurement criterion, particularly in labor-constrained healthcare and food service environments where worker retention and compliance risk carry significant cost implications.

Specialized Clean-in-Place Chemistries for Precision Fermentation and Alternative Proteins

The rapid commercialization of alternative protein production is opening a high-margin opportunity for specialized clean-in-place cleaning chemistries. Precision fermentation facilities generate complex proteinaceous and lipid-based residues that are fundamentally different from conventional dairy or meat soils. Standard alkaline and acid CIP programs are often insufficient, creating demand for enzyme-driven and bio-compatible cleaning systems tailored to sensitive bioreactor environments.

Industry projections indicate that alternative proteins could contribute more than €900 billion to global economic output by mid-century, with fermentation infrastructure scaling identified as a key bottleneck. In response, I&I chemical suppliers are developing validation-ready CIP solutions capable of supporting regulatory audits and rapid batch changeovers. Enzymatic cleaners introduced in 2025 operate at temperatures 10 to 15 degrees Celsius lower than traditional caustic systems, enabling energy savings of approximately 12% per cleaning cycle while maintaining high soil removal efficiency.

As facilities move from pilot to commercial scale, contamination control is emerging as a critical risk factor. This is driving adoption of pH-neutral, stainless-steel-safe formulations that deliver 99.99% residue removal without compromising bioreactor longevity. Suppliers that can combine cleaning efficacy with material protection and process validation support are positioned to secure long-term contracts in this fast-scaling segment.

Hypochlorous Acid Hardware-as-a-Service Models in Healthcare

On-site generation of hypochlorous acid is evolving from a niche solution into a strategic growth platform within healthcare cleaning and disinfection. Hospitals and clinical networks are increasingly adopting hardware-as-a-service models in which I&I providers install and maintain electrolyzed water systems that generate HOCl on demand using salt, water, and electricity. This approach addresses multiple pain points simultaneously, including chemical transport risk, storage hazards, and residue management.

By 2025, small-scale electrolysis systems had become a core component of hospital hygiene programs, supported by evidence that hypochlorous acid delivers significantly higher antimicrobial efficacy than traditional bleach at a fraction of the concentration. Clinical pilots demonstrated that residue-free HOCl disinfection reduced operating room turnover times by an average of eight minutes per procedure, directly improving asset utilization in high-demand surgical environments.

From a risk management perspective, on-site generation materially reduces hazardous chemical inventories. Public procurement data from late 2025 show that hospitals deploying HOCl generation systems cut hazardous chemical storage volumes by approximately 60%, leading to lower insurance premiums and simplified regulatory compliance. This positions HOCl hardware-as-a-service as a durable, recurring revenue opportunity for I&I suppliers capable of integrating chemistry, equipment, maintenance, and compliance reporting into a single service offering.

Industrial and Institutional Cleaning Chemicals Market Share and Segmentation Insights

Surfactants Lead Industrial and Institutional Cleaning Chemical Formulations Through Core Soil Removal Performance

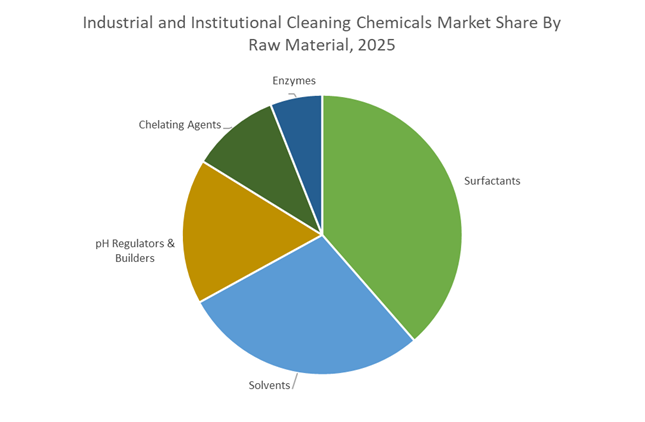

Surfactants accounted for 38.6% of the Industrial and Institutional Cleaning Chemicals Market share in 2025, establishing them as the most important raw material in professional cleaning formulations. Surfactants function as the primary active agents responsible for reducing surface tension, emulsifying oils, dispersing particulate soils, and improving wetting and penetration on surfaces, making them indispensable across nearly all industrial and institutional cleaning products. These chemicals are widely incorporated into general-purpose cleaners, floor care solutions, industrial degreasers, laundry detergents, dishwashing formulations, and vehicle wash chemicals, where consistent cleaning performance is required in demanding environments. In 2025, a major transformation in the market is the transition toward bio-based and renewable surfactants, driven by sustainability commitments from facility management companies, hospitality groups, and food service operators. Cleaning product manufacturers increasingly utilize alkyl polyglycosides, plant-derived surfactants, and biosurfactant technologies that provide improved biodegradability and lower environmental impact while maintaining the high cleaning efficiency required in commercial and industrial sanitation programs.

Commercial Facilities Drive the Largest Demand for Industrial and Institutional Cleaning Chemicals

Commercial facilities represented 48.6% of the Industrial and Institutional Cleaning Chemicals Market share in 2025, making them the largest end-use sector for professional cleaning products. Commercial environments such as office buildings, hotels, restaurants, retail centers, healthcare facilities, and entertainment venues require continuous cleaning and sanitation to maintain hygiene standards and provide safe environments for employees, customers, and visitors. These facilities consume large volumes of surface disinfectants, floor cleaners, restroom sanitation chemicals, kitchen degreasers, and laundry detergents, creating consistent demand for industrial-grade cleaning formulations. The hospitality and food service sectors represent particularly significant users of cleaning chemicals because of strict sanitation regulations governing commercial kitchens, food preparation areas, and dining environments. In 2025, a major market driver is the permanent elevation of hygiene and sanitation standards following the COVID-19 pandemic, which has reshaped cleaning protocols across commercial buildings. Businesses now maintain more frequent disinfection schedules and visible sanitation practices, especially in healthcare, hospitality, transportation hubs, and high-traffic retail locations, sustaining higher baseline consumption of industrial and institutional cleaning chemicals compared with pre-pandemic levels.

Competitive Landscape in Industrial and Institutional Cleaning Chemicals Market

Ecolab Expands Digital Water Circularity Platform

Ecolab Inc. reported record 2025 sales of $15.3 billion, with 2026 guidance projecting 12%–15% adjusted EPS growth. In November 2025, it completed the acquisition of Ovivo Electronics, doubling its Global High-Tech segment and strengthening its end-to-end water circularity offerings for semiconductor customers. The company’s 3D TRASAR™ digital monitoring platform now exceeds 47,000 installations globally, enabling real-time chemical dosing optimization and predictive system analytics. Through its “One Ecolab” productivity program, annualized savings are expected to reach $325 million by 2027. Strategic emphasis is placed on high-tech water treatment, digital hygiene systems, and pest elimination—segments delivering double-digit growth. The company is increasingly positioning cleaning chemicals within a broader total-value proposition combining water stewardship, infection prevention, and data-enabled performance guarantees.

Solenis Integrates Water and Hygiene Through Consolidation

Solenis, strengthened by its 2023 merger with Diversey and the November 2025 acquisition of NCH Corporation, now operates as a globally diversified water and hygiene solutions provider across 160 countries with 78 manufacturing facilities. The integration enables a “360-degree” approach combining water treatment chemistries with institutional hygiene platforms. In 2026, Solenis reported that 74% of revenue stems from sustainability-supporting solutions, with 91% of active innovation initiatives aligned to circularity. The opening of a new Global Research Center in Delaware reinforces its R&D focus on next-generation disinfection, closed-loop water reuse, and industrial hygiene chemistries. The NCH acquisition significantly strengthens its middle-market industrial footprint, expanding technical field service capabilities across manufacturing and energy sectors.

Henkel Aligns Consumer and Industrial Cleaning Strategy

Henkel AG & Co. KGaA finalized the integration of its Laundry & Home Care and Beauty Care units into the unified Consumer Brands division by end-2025. For 2026, it projects 1.5%–3.5% organic sales growth, with adjusted return on sales targeted between 13.5% and 15.0%. While maintaining consumer leadership, Henkel continues expanding industrial applications, illustrated by the January 2026 launch of Loctite STYCAST US 8000 A/B for harsh-environment electronics. Its decarbonization efforts include launching India’s first mid-haul re-powered electric truck operations in late 2025, reducing logistics-related emissions. In the I&I space, Henkel is leveraging formulation expertise, adhesives, and specialty chemistries to target industrial sanitation, surface preparation, and equipment maintenance markets.

BASF Leverages Verbund Integration for Asian Growth

BASF SE is utilizing its “Winning Ways” strategy to strengthen its cleaning and care portfolio while managing cost pressures in Europe. Major startups at its Zhanjiang Verbund site in China during 2025–2026 position Asia as a primary growth engine for care chemicals and surfactants. The company targets a €2.3 billion annual cost reduction run rate by end-2026. For 2026, BASF forecasts Group EBITDA before special items between €6.2 billion and €7.0 billion, with Nutrition & Care and Chemicals segments expected to drive earnings growth. Projected CO2 emissions for 2026 are estimated at 17.2–18.2 million metric tons, reflecting simultaneous site expansions and energy-efficiency measures. BASF’s integration model provides raw material cost advantages and supply reliability in surfactants, solvents, and performance additives used in institutional cleaning formulations.

Clariant Accelerates Innovation and Digital Services

Clariant reported a 17.8% EBITDA margin for FY 2025, improving 180 basis points year-on-year. Its innovation sales—products launched within the past five years—account for 18.8% of total revenue, reflecting a rapid commercialization pipeline in care chemicals. The CLARITY™ digital platform nearly doubled its global user base in 2025, supporting performance tracking and catalyst/additive optimization across 38 countries. For 2026, Clariant anticipates stable sales in a challenging macro environment while maintaining a 42% free cash flow conversion target. The company continues prioritizing high-margin, sustainability-driven chemistries with strong safety performance metrics (DART rate of 0.13), positioning itself as a premium specialty supplier within institutional cleaning and surface-care segments.

Evonik Scales Biosurfactant Production

Evonik Industries AG is advancing bio-based surfactants as a structural shift in industrial cleaning. The company successfully scaled production at the world’s first industrial-scale rhamnolipid biosurfactant facility in Slovakia, offering biodegradable alternatives to petrochemical-derived surfactants. In March 2025, Evonik entered an exclusive U.S. distribution agreement with Sea-Land Chemical Company to streamline North American market access. Through its “Evonik Tailor Made” restructuring program, the company aims to reduce hierarchies and eliminate approximately 2,000 positions by end-2026 to enhance competitiveness. For 2026, Evonik forecasts adjusted EBITDA between €1.7 billion and €2.0 billion under a revised dividend policy targeting 40%–60% of adjusted net income. Its biosurfactant platform positions it at the forefront of regulatory-driven demand for low-toxicity, biodegradable cleaning chemistries across industrial and institutional markets.

United States Industrial and Institutional Cleaning Chemicals Market: AI-Driven Hygiene, Concentration Logistics, and Regulatory Tightening

The United States industrial and institutional cleaning chemicals market is shifting toward digitally optimized hygiene, ultra-concentrated formats, and evidence-based antimicrobial compliance. In September 2025, Ecolab launched CIP IQ at Drinktec 2025, embedding AI-powered clean-in-place intelligence into food and beverage operations. The platform applies fluid fingerprinting with proprietary 4T2 Sensors to adjust cleaning cycles in real time, delivering verified gains in operational efficiency and materially lowering water use. This deployment reflects a broader U.S. trend toward data-validated sanitation outcomes in regulated manufacturing environments where uptime, traceability, and audit readiness are critical.

Concentration and logistics innovation is advancing in parallel. In November 2025, Ecolab introduced the Fill & Clean Series, a mobile dispensing system that converts a single concentrate into the equivalent of 16 ready-to-use bottles via a just-add-water design. The approach materially reduces transport-related emissions and on-site storage complexity for commercial facilities. Aviation maintenance is also seeing step-change innovation. In October 2025, Henkel released Bonderite C-AK DW 805 AERO, a non-flammable dry-wash aircraft cleaner that eliminates water rinsing, reduces maintenance downtime, and aligns with FAA-supported sustainability objectives for 2026. Regulatory expectations are tightening as well. From January 2026, updated EPA List N efficacy standards require manufacturers to submit data on long-term residual antimicrobial performance for high-traffic institutional settings such as airports and schools. Complementing these shifts, Evonik finalized an exclusive U.S. distribution agreement with Sea-Land Chemical in March 2025 to scale rhamnolipid-based biosurfactants, accelerating substitution away from petroleum-derived surfactants across institutional applications.

China Industrial and Institutional Cleaning Chemicals Market: Phase-Out Mandates, Localization, and Digital Traceability

China’s industrial and institutional cleaning chemicals sector is being reshaped by hard regulatory deadlines, localization targets for critical intermediates, and mandatory digital oversight. Effective July 1, 2026, the Ministry of Ecology and Environment will prohibit the use of hydrochlorofluorocarbons as cleaning agents, forcing a nationwide transition toward hydrofluoroethers and water-based aqueous cleaners in metal finishing and electronics cleaning. This mandate materially accelerates reformulation timelines and capital allocation toward compliant chemistries.

Industrial policy is reinforcing the shift. Under the 2025–2026 Steady Growth Plan jointly issued by MIIT and seven ministries, the chemical sector is guided toward sustained value growth with a clear priority on localizing high-end surfactant and chelating agent intermediates. The stated objective is to reach approximately 90% domestic self-sufficiency by 2026, reducing exposure to imported inputs in mission-critical cleaning formulations. Compliance pressures extend to coatings removal. From June 2026, SAMR will enforce GB 30981.1-2025, imposing stricter VOC and hazardous substance limits on industrial protective coatings and the specialized strippers used to remove them. In parallel, the 2026 Digital Empowerment mandate is driving I&I chemical plants to integrate blockchain-based traceability systems that track hazardous cleaning agents from production through industrial waste treatment, elevating accountability across the lifecycle.

Germany Industrial and Institutional Cleaning Chemicals Market: Enzyme Scale-Up, Green Deal Alignment, and Portfolio Refocus

Germany’s I&I cleaning chemicals market is advancing through enzyme technology scale-up, biodegradable chelation, and strategic portfolio rationalization aligned with EU sustainability policy. In October 2025, BASF and International Flavors & Fragrances announced a collaboration to develop the Designed Enzymatic Biomaterials platform, targeting high-performance industrial degreasing and fabric care. The initiative focuses on scaling next-generation enzymes that deliver efficacy at lower temperatures and reduced chemical load, directly supporting energy efficiency targets in industrial laundering and processing.

Product commercialization is already reflecting this direction. In April 2025, BASF deployed Trilon G, a GLDA-based biodegradable chelating agent containing approximately 56% renewable carbon, positioned to replace EDTA in industrial dishwashing and laundry formulations to meet 2026 EU Green Deal requirements. Portfolio decarbonization is also evident. Clariant reported a reduction in Scope 3 emissions in late 2025 by increasing the share of bio-based raw materials within its Care Chemicals division serving the European I&I market. Strategic focus sharpened further when BASF confirmed the divestment of its optical brightening agent business to Catexel, part of International Chemical Investors Group, in early 2026, signaling a move away from commoditized laundry additives toward specialized I&I solutions.

India Industrial and Institutional Cleaning Chemicals Market: Incentivized Specialty Production and Environmental Enforcement

India’s I&I cleaning chemicals market is being propelled by targeted production incentives, stricter waste governance, and infrastructure-led capacity creation. For 2025–2026, the government expanded allocations under the Production-Linked Incentive scheme to prioritize sunrise sectors, including high-purity specialty chemicals used in hospital-grade disinfectants and electronics cleaning. This policy support is accelerating domestic capability development in formulations that require tight impurity control and consistent antimicrobial performance.

Environmental oversight is intensifying alongside capacity build-out. In March 2025, the Central Pollution Control Board introduced the Ninth Amendment to the Hazardous and Other Wastes Rules, strengthening controls on the disposal of industrial surfactants and chemical residues, particularly across manufacturing belts in Gujarat and Maharashtra. Looking ahead, the Aatmanirbhar Bharat roadmap for 2026 includes the establishment of integrated chemical hubs with advanced waste-management infrastructure to support enzyme-based cleaning agent production. This alignment of incentives and enforcement is reshaping India’s I&I landscape toward compliant, export-ready specialty chemistries.

Singapore Industrial and Institutional Cleaning Chemicals Market: Waste Reduction Formats and Automated Dosing at Scale

Singapore’s I&I cleaning chemicals market emphasizes compact formats, dosing automation, and food safety assurance within dense urban operations. In July 2025, Ecolab introduced the ReadyDose program for Southeast Asian foodservice, featuring tablet-based, non-phosphate formulations that dissolve rapidly and cut packaging waste by up to 90% versus traditional liquid containers. The program directly addresses storage constraints and waste reduction mandates common in hospitality-heavy environments.

Partnership-led deployment is accelerating adoption. Ecolab partnered with Sia Huat to integrate automated dosing systems across hospitality hubs in Singapore and Malaysia, with a stated objective to eliminate manual chemical handling by 2026. This approach elevates consistency, worker safety, and compliance, reinforcing Singapore’s role as a regional reference market for precision dosing and low-waste I&I cleaning systems.

Industrial and Institutional Cleaning Chemicals: Country-Level Strategic Summary

Industrial and Institutional Cleaning Chemicals Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Core Technology or Policy Lever

|

Market Direction

|

|

United States

|

AI-enabled hygiene and evidence-based antimicrobials

|

CIP IQ, EPA List N residual efficacy

|

Data-validated, low-water, low-emission solutions

|

|

China

|

Regulatory phase-outs and localization

|

HCFC ban, GB 30981.1-2025, blockchain traceability

|

Rapid reformulation and domestic supply security

|

|

Germany

|

Enzyme scale-up and EU Green Deal alignment

|

GLDA chelation, enzymatic biomaterials

|

Shift to high-performance, low-carbon I&I chemistry

|

|

India

|

Incentives plus enforcement

|

PLI expansion, hazardous waste amendments

|

Domestic specialty capacity with compliance focus

|

|

Singapore

|

Waste reduction and dosing automation

|

Tablet-based formats, automated dispensing

|

Compact, safe, and highly controlled deployment

|

Industrial and Institutional Cleaning Chemicals Market Report Scope

Industrial and Institutional Cleaning Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$84.8 Billion

|

|

Market Size (2034)

|

$162.6 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Raw Material (Surfactants, Solvents, Chelating Agents, pH Regulators & Builders, Enzymes), By Product Type (General Purpose Cleaners, Disinfectants and Sanitizers, Laundry Care Products, Vehicle Wash Products, Clean-in-Place Chemicals, Floor & Carpet Care), By End-Use Sector (Commercial, Institutional, Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc., BASF SE, Henkel AG & Co. KGaA, Diversey, Procter & Gamble, Clariant AG, Solvay S.A., Dow Inc., Evonik Industries AG, Reckitt Benckiser Group plc, Stepan Company, The Clorox Company, 3M Company, Kimberly-Clark Corporation, AkzoNobel N.V.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial and Institutional Cleaning Chemicals Market Segmentation

By Raw Material

By Product Type

- General Purpose Cleaners

- Disinfectants and Sanitizers

- Laundry Care Products

- Vehicle Wash Products

- Clean-in--Place Chemicals

- Floor & Carpet Care

By End-Use Sector

- Commercial

- Institutional

- Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Industrial and Institutional Cleaning Chemicals Industry

- Ecolab Inc.

- BASF SE

- Henkel AG & Co. KGaA

- Diversey

- Procter & Gamble

- Clariant AG

- Solvay S.A.

- Dow Inc.

- Evonik Industries AG

- Reckitt Benckiser Group plc

- Stepan Company

- The Clorox Company

- 3M Company

- Kimberly-Clark Corporation

- AkzoNobel N.V.

*- List not Exhaustive