Market Overview: Infant Formula Packaging to Reach $4.9 Billion by 2034 on Premium, Tamper-Evident, and Bio-Based Formats

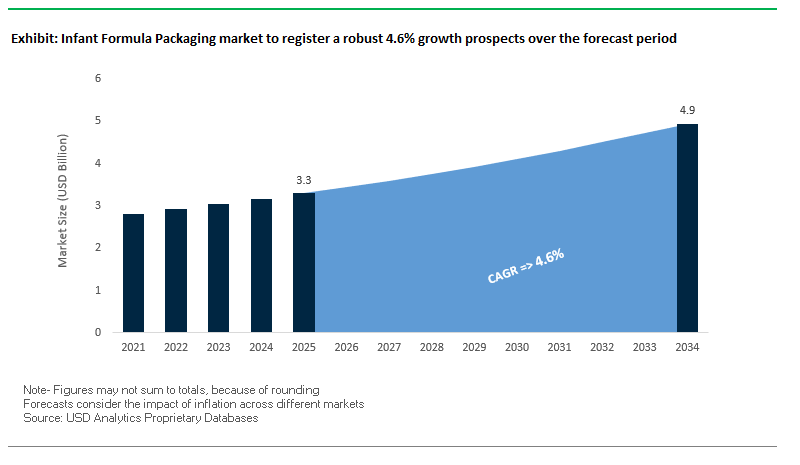

The global infant formula packaging market is valued at $3.3 billion in 2025 and is projected to reach $4.9 billion by 2034, registering a CAGR of 4.6%. Unlike mainstream food packs, infant nutrition demands ultra-reliable barrier performance, tamper evidence, and convenience features that simplify safe preparation for caregivers. The competitive edge is shifting toward premium plastic tubs with built-in scoops and snap-shut lids, tamper-evident closures, and mono-material or bio-based components that lower carbon footprints without compromising shelf life. While glass retains niche prestige in organic/premium SKUs, lightweight, shatter-resistant plastics are expanding share by reducing logistics emissions and breakage risk.

Key Insights for Industry Stakeholders

- Premium convenience drives format shifts: Plastic tubs with scoop holders and snap-shut lids are displacing composite cans on ease-of-use and hygiene.

- Security is non-negotiable: Tamper-evident seals/closures are critical to consumer trust and retail compliance.

- Sustainable materials accelerate: Brands deploy bio-based lids/scoops (e.g., sugar-cane derived) and recycle-ready pouch structures.

- Weight and safety advantages: Move from glass to plastic reduces CO₂ per shipment and eliminates shatter risk while maintaining product integrity.

Market Analysis: 2024–2025 Developments Emphasize Sustainability Credentials and Portfolio Scale-Ups

Industry momentum centers on sustainability milestones, capacity expansions, and format innovation supporting infant nutrition and adjacent baby food lines. In August 2025, Amcor expanded its healthcare packaging network in Costa Rica, boosting access to high-value medical-grade solutions relevant to infant nutrition hygiene standards. Also in August 2025, Amcor reported strong Q4 FY2025 results (+43% YoY net sales), reflecting contributions from its April 2025 acquisition of Berry Global, deepening capability in rigid bottles, closures, tubs, and specialty films used across infant categories.

Sustainability proof points gained prominence. Tetra Pak achieved EcoVadis Platinum (July 2025) and Huhtamaki earned EcoVadis Gold (July 2025), signaling strong governance for buyers prioritizing verified ESG in supplier selection. Brand-side material transitions accelerated: Nestlé (March 2025) launched bio-based lids and scoops (sugar-cane) across infant and children’s nutrition, while Huhtamaki (March 2025) showcased paper cups and lids for spreads, underlining capabilities in high-barrier fiber solutions transferrable to baby categories. Flexible packaging advanced via Amcor & Mespack’s 2L AmPrima stand-up bag (November 2024) and Amcor’s recyclable baby food pouches (October 2024) mono-material structures designed to simplify recycling and appeal to eco-conscious parents.

Trends and Opportunities Reshaping the Infant Formula Packaging Market

Strategic Investment in Aseptic Packaging and Filling Capacity

The infant formula packaging market is undergoing a major structural shift as manufacturers strategically invest in aseptic filling lines to expand production capacity. This trend is fueled by the surging popularity of ready-to-feed (RTF) liquid infant formula, which delivers unmatched convenience for caregivers. Unlike traditional powder formats that require scooping and mixing, RTF aseptic cartons and bottles eliminate preparation, catering to parents’ need for speed and safety during late-night feedings or travel.

Beyond convenience, aseptic packaging provides superior sterility assurance a critical differentiator following recent product recalls linked to bacterial contamination. By extending shelf life without preservatives or refrigeration, aseptic formats build consumer trust and strengthen brand positioning. This strategic advantage comes at a cost: a single integrated aseptic carton line may exceed $18 million in investment, underscoring the capital intensity of this packaging evolution. Industry leaders such as Tetra Pak and Scholle IPN are enabling this transformation with cutting-edge equipment designed to meet both safety and scalability requirements.

As premiumization drives parents to pay more for liquid infant nutrition solutions, aseptic packaging is becoming the growth engine for formula brands. Companies that invest early in aseptic infrastructure are positioning themselves to capture long-term market share in high-value segments.

Enhanced Integration of Anti-Counterfeit and Traceability Features

Another defining trend is the accelerated integration of track-and-trace and anti-counterfeit technologies directly into infant formula packaging. Regulators and brand owners are prioritizing these innovations to safeguard consumer trust and ensure product integrity amid global counterfeiting risks.

In the U.S., the FDA and FTC investigations into formula shortages and contamination crises emphasized the urgent need for traceability solutions. This has prompted packaging suppliers to adopt unique digital identifiers (UIDs), QR codes, and covert features that enable instant product authentication. For instance, KURZ SCRIBOS has developed copy-proof QR codes that allow parents to confirm authenticity using their smartphones, turning packaging into a direct consumer trust tool.

Globally, the urgency is reinforced by operations like Interpol’s OPSON initiative, which has uncovered counterfeit baby milk powder in multiple markets. This underscores why brands are embedding authentication systems that work seamlessly across geographies. Beyond consumer verification, these smart packaging features enable rapid recall execution, ensuring regulators and manufacturers can trace defective batches instantly. Together, they elevate infant formula packaging from passive containment to a central pillar of food safety and consumer security.

Development of Sustainable Packaging Formats Without Compromising Barrier Properties

Sustainability is both a challenge and an opportunity in the infant formula packaging market. The product’s sensitivity to oxygen, light, and moisture necessitates high-barrier packaging traditionally reliant on complex laminates and plastics that are difficult to recycle. The unmet need lies in developing eco-friendly formats that reduce environmental impact without sacrificing protection.

Companies like Amcor are addressing this gap with solutions such as AmLite HeatFlex, a metal-free, high-barrier retort pack that cuts the carbon footprint by up to 40% compared to standard alternatives. Innovations are also emerging in bag-in-box (BIB) packaging, where a multi-layer plastic bag within a corrugated box provides both structural protection and lower material intensity than rigid containers.

Pressure from major infant nutrition companies like Nestlé and Danone, both committed to reducing virgin plastic and increasing recycled content, is accelerating innovation in this area. The winning solutions will be those that balance sustainability with sterility, proving that eco-friendly design and product safety can coexist. For suppliers, this represents a lucrative opportunity to lead in next-generation sustainable infant formula packaging.

Packaging Innovation for Improved Accessibility and Usability

Beyond sustainability and safety, the usability of infant formula packaging is an emerging frontier. Packaging design is increasingly being optimized for caregiver convenience, accessibility, and ergonomics, recognizing that parents often prepare formula in stressful or time-sensitive situations.

One example is Chadwicks’ “Spoon-in-lid” solution, developed with a plastic engineering specialist, which resolves the long-standing frustration of scoops being buried within powder cans. By embedding the scoop in the lid, the design improves hygiene and reduces preparation stress. Similarly, clear and prominent labeling with nutritional claims such as “organic,” “fortified with iron,” or “no artificial additives” helps parents make faster, more confident purchase decisions, especially in high-pressure shopping environments.

Ergonomic enhancements, including re-sealable lids, pour spouts, and easy-grip handles, further reduce contamination risk and mess during feeding. These design elements elevate the overall user experience, ensuring packaging becomes not just a protective medium but also a value-adding tool for caregiver confidence and brand loyalty.

Competitive Landscape: High-Barrier Science, Tamper Evidence, and Recycle-Ready Systems Differentiate Leaders

The infant formula packaging market blends global converters, dispensing specialists, and aseptic leaders. Winners pair regulatory-grade barriers with parent-friendly ergonomics and credible sustainability (bio-based, mono-material, PCR pathways). Below is an expert-focused cut of leading participants.

Amcor Recycle-ready pouches and tubs scaled by Berry integration

Amcor supplies multi-layer pouches, thermoformed cups, rigid tubs, and SlimFlex™ stickpacks for powdered beverages including infant formula. The Berry Global acquisition (April 2025) expanded rigid and closure depth; network expansion in Costa Rica (August 2025) adds medical-grade rigor. AmPrima® Plus recycle-ready solutions target mono-material designs with high oxygen/moisture barrier. Amcor’s global R&D + materials science underpin safety, freshness, and shelf-life core to infant nutrition compliance.

Aptar Tamper-evident, hygienic closures and renewable-feedstock options

Aptar delivers closures, flip-top pour spouts, and custom scoops engineered for hygienic prep and precise dosing. Its Neo closure (first launched September 2021) is available in food-grade renewable feedstock material, and the portfolio emphasizes tamper-evidence and easy one-hand use. Integration across tubs and pouches streamlines parent experience, differentiating premium SKUs on convenience and safety.

Sonoco Rigid paper cans with high barrier and recyclable options

Sonoco serves powdered formula with rigid paper containers and Sealed Safe® membrane ends engineered against oxygen, moisture, and aroma ingress. The Eviosys acquisition (December 2024) strengthens metal packaging know-how for ends and specialty components. Under EnviroSense™, Sonoco advances paperboard cans with paper ends to enhance recyclability while preserving the stacking durability required across complex distribution.

Huhtamaki High-barrier flexible laminates with verified sustainability

Huhtamaki provides laminates, stand-up pouches, and specialty films that protect sensitive powders from oxygen and moisture. Its EcoVadis Gold (July 2025) underscores reliable ESG performance. The company’s expansion in fiber-based packaging complements flexibles, offering brands paper-forward options where barrier and machinability permit aligning infant nutrition with plastic reduction roadmaps.

Tetra Pak Aseptic cartons for ready-to-drink infant formula

Tetra Pak leads liquid RTD infant formula packaging via aseptic cartons (e.g., Tetra Brik Aseptic), enabling ambient-shelf-life without refrigeration. EcoVadis Platinum (July 2025) bolsters sustainability credentials. Core value lies in separate sterilization of product and package, then aseptic sealing, ensuring light/oxygen barrier and logistics efficiency for portion packs and hospital channels.

Sealed Air Protective barrier films and automated form-fill-seal systems

Sealed Air (CRYOVAC®) offers barrier bags/films that extend shelf life and protect against oxygen and moisture; its systems integrate with form-fill-seal equipment to safeguard product integrity at speed. While broadly known in food and protective packaging, its barrier portfolio and automation expertise are applicable to infant formula supply chains where waste reduction and seal reliability are paramount.

Infant Formula Packaging Market Share Insights

Rigid Packaging Dominates Infant Formula Packaging Market Share by Type

In the infant formula sector, rigid packaging holds an overwhelming 85% market share in 2025, underscoring its absolute dominance as the global standard for safety and quality. Metal cans and high-grade plastic tubs provide superior barrier properties against moisture, oxygen, and light, ensuring formula stability and nutritional integrity factors that are non-negotiable for parental trust and regulatory compliance. Their structural resilience also prevents damage during transport, safeguarding product quality across global supply chains. Flexible packaging plays only a niche role, primarily in single-serve sachets or as inner liners, but it lacks the protective capabilities and consumer trust of rigid formats. This clear imbalance highlights how rigid packaging’s functional superiority and symbolic role as a “trust signal” for parents sustains its dominance against lightweight alternatives.

Powdered Formulas Command Infant Formula Packaging Market Share by Application

Powdered formulas account for 80% of infant formula packaging applications in 2025, reinforcing their role as the undisputed mainstay of the industry. Their dominance is attributed to long shelf life, cost efficiency, and logistical advantages, which make powdered formats the most practical and trusted option for households worldwide. Packaging is primarily in high-barrier rigid metal cans or plastic tubs engineered for moisture protection, underscoring the segment’s reliance on robust solutions. Ready-to-use (RTU) formulas occupy a smaller but premium niche, packaged in sterile bottles and liquid cartons that appeal to convenience-focused parents and healthcare facilities. Concentrated liquid formulas remain the smallest, declining segment, squeezed by RTU’s superior convenience and powder’s cost efficiency. This segmentation makes clear that powdered formulas and rigid cans define the industry’s baseline, while RTU products carve out a premium, high-value niche.

United States: Regulatory Reforms and Sustainable Packaging Driving Market Transformation

The U.S. infant formula packaging market is undergoing a significant transformation driven by regulatory initiatives, sustainability demands, and packaging innovations. The Department of Health and Human Services’ Operation Stork Speed (OSS) is a major catalyst, with the FDA reviewing formula standards for the first time in nearly three decades. This regulatory push is promoting innovation in both product formulation and packaging to support functional health outcomes. Companies like Abbott Laboratories are investing heavily in domestic manufacturing, with a $500 million plant to bolster supply chain resilience. Sustainability is a key driver, with firms such as Trivium Packaging focusing on 100% infinitely recyclable infant formula cans and implementing lightweighting solutions to reduce environmental impact and transportation costs. Additionally, advancements in packaging technology, including bag-in-box formats, are improving convenience, extending shelf life, and reducing carbon footprints, highlighting the market’s response to consumer and environmental expectations.

Germany: Circular Economy and Eco-Friendly Materials Leading Industry Growth

Germany’s infant formula packaging market is heavily influenced by stringent regulations and sustainability initiatives. The EU Packaging and Packaging Waste Regulation (PPWR) and the German Packaging Act (VerpackG) enforce high standards for recyclable and environmentally friendly materials. German companies are deeply invested in the circular economy, prioritizing packaging designed for recyclability and incorporating high percentages of recycled content. Innovations in eco-friendly materials, such as bio-based plastics, recyclable cartons, and compostable pouches, are increasingly adopted to reduce non-recyclable waste. The market’s focus on sustainable packaging solutions positions Germany as a leader in eco-conscious infant formula packaging in Europe, meeting both consumer expectations and regulatory mandates.

China: E-Commerce Growth and Premiumization Driving Packaging Innovation

China’s infant formula packaging industry is shaped by stringent regulatory compliance, rapid e-commerce expansion, and rising consumer demand for premium products. All products must be registered with the National Medical Products Administration (NMPA), ensuring safety, traceability, and adherence to the Food Safety Law. The growing middle class is driving premiumization, with high-end packaging featuring advanced finishing, unique shapes, and high-quality printing to differentiate products. The surge in e-commerce has increased demand for secure, tamper-evident, and durable packaging capable of withstanding long-distance shipping. Furthermore, the government’s focus on traceability has prompted the widespread use of QR codes and digital technologies on packaging, providing consumers with authenticity verification and safety information while combating counterfeiting.

India: Technological Advancements and Rural Market Expansion Enhancing Packaging Adoption

India’s infant formula packaging market is benefiting from rapid technological advancements, evolving family dynamics, and regulatory oversight. Innovations such as resealable pouches and single-use sachets are gaining popularity, providing convenience and product safety for a growing consumer base. The rise of nuclear families and working mothers is driving demand for ready-to-use packaging formats. The Food Safety and Standards (Foods for Infant Nutrition) Regulations, 2019, enforce strict labeling requirements, including prohibitions on pictures of infants or women and mandatory warning statements. With a large rural population, demand for smaller, affordable, and convenient packaging formats is growing, allowing brands to expand market reach while complying with regulatory standards.

Brazil: Regulatory Oversight and E-Commerce Growth Strengthening Packaging Market

The Brazilian infant formula packaging market is strongly influenced by government regulation, safety standards, and e-commerce growth. The Brazilian Health Regulatory Agency (Anvisa) has implemented stringent frameworks, including restrictions on advertising, to ensure purchasing decisions are guided by healthcare advice rather than marketing. Regulatory updates for food contact materials emphasize high-quality and safe packaging that meets international standards. The rapid growth of Brazil’s e-commerce sector has created strong demand for secure and efficient packaging solutions for infant formula. These factors collectively reinforce a market environment that prioritizes safety, quality, and sustainable innovation.

Japan: Regulatory Reforms and Convenience-Driven Packaging Innovations

Japan’s infant formula packaging market has been significantly influenced by regulatory changes, demographic trends, and consumer convenience demands. The introduction of standards for liquid infant formula under the Food Sanitation Act in 2018 enabled domestic production and sale, creating new packaging opportunities. Strict regulations ensure that hygiene, safety, and product integrity are maintained, prompting manufacturers to adopt highly reliable packaging solutions. The growing number of single-person households and working parents has increased demand for convenient, ready-to-use packaging formats, including pre-measured liquid formulas. These trends highlight Japan’s focus on quality, safety, and user-friendly packaging solutions in the infant formula sector.

Infant Formula Packaging Market Report Scope

Infant Formula Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.3 Billion

|

|

Market Size (2034)

|

$4.9 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Material Type (Metal, Plastics, Glass, Paper & Paperboard, Flexible Packaging), By Packaging Type (Rigid Packaging, Flexible Packaging), By Application (Ready-to-use Formulas, Powdered Formulas, Concentrated Liquid Formulas)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Ardagh Group S.A., Trivium Packaging, AptarGroup, Inc., DS Smith Plc, Gerresheimer AG, Mondi Group, Huhtamaki Oyj, Sonoco Products Company, Silgan Holdings Inc., Bormioli Rocco, Crown Holdings Inc., WestRock Company, Ball Corporation, Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Infant Formula Packaging Market Segmentation

By Material Type

- Metal

- Plastics

- Glass

- Paper & Paperboard

- Flexible Packaging

By Packaging Type

- Rigid Packaging

- Flexible Packaging

By Application

- Ready-to-use Formulas

- Powdered Formulas

- Concentrated Liquid Formulas

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Infant Formula Packaging Market

- Amcor plc

- Ardagh Group S.A.

- Trivium Packaging

- AptarGroup, Inc.

- DS Smith Plc

- Gerresheimer AG

- Mondi Group

- Huhtamaki Oyj

- Sonoco Products Company

- Silgan Holdings Inc.

- Bormioli Rocco

- Crown Holdings Inc.

- WestRock Company

- Ball Corporation

- Greiner Packaging International GmbH

*List not Exhaustive

Research Coverage

This report investigates the global infant formula packaging market, providing an in-depth exploration of market dynamics, innovations, and competitive strategies shaping the sector through 2034. USDAnalytics’ analysis reviews breakthroughs in aseptic packaging, tamper-evident systems, and sustainable, bio-based materials, highlighting how these advancements enhance infant formula safety, shelf life, and caregiver convenience. The report emphasizes premiumization trends, including high-barrier rigid tubs, mono-material structures, and ready-to-feed liquid formats, while evaluating eco-conscious packaging initiatives, digital authentication, and traceability solutions. This report is an essential resource for packaging engineers, FMCG executives, sustainability officers, and regulatory specialists seeking to understand evolving market forces, strategic investment opportunities, and emerging consumer preferences. Additionally, it assesses regional market developments across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, offering a comprehensive view of technological adoption, policy influence, and premium product trends. By profiling key players and highlighting their capacity expansions, mergers, and sustainability commitments, USDAnalytics provides actionable insights to inform business strategy, R&D focus, and supply chain decisions.

Scope Highlights

- Segmentation: By Material Type (Metal, Plastics, Glass, Paper & Paperboard, Flexible Packaging), By Packaging Type (Rigid Packaging, Flexible Packaging), By Application (Ready-to-use Formulas, Powdered Formulas, Concentrated Liquid Formulas)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historical & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Analysis/profiles of 15+ companies, including Amcor plc, AptarGroup, Trivium Packaging, Huhtamaki Oyj, Sonoco Products Company, Tetra Pak, Gerresheimer AG, Mondi Group, DS Smith Plc, and others.

Methodology

The research methodology for this report combines primary and secondary data collection, expert interviews, and proprietary analytical models to deliver highly reliable insights for industry stakeholders. USDAnalytics leveraged quantitative data from company financials, regulatory filings, trade associations, and industry reports, coupled with qualitative insights from packaging engineers, R&D directors, and supply chain managers. Market sizing and forecasting utilized a bottom-up approach, integrating historical shipment volumes, material consumption trends, and capacity expansions to project revenues through 2034. Competitive benchmarking focused on sustainability initiatives, barrier technologies, tamper-evident mechanisms, and digital authentication solutions. Additionally, regional analyses incorporated macroeconomic indicators, e-commerce growth, and regulatory frameworks to contextualize adoption rates and premiumization trends. The methodology ensures robust, actionable intelligence tailored for well-experienced professionals seeking to optimize investments, product design, and supply chain strategy in infant formula packaging.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.