Labelling Services Market Overview: Key Industry Statistics

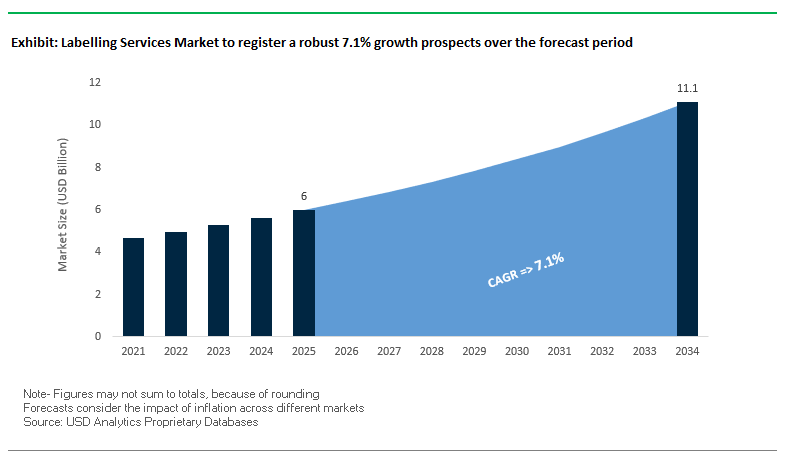

The Labelling Services Market is projected to grow from USD 6.0 billion in 2025 to USD 11.1 billion by 2034, expanding at a CAGR of 7.1%. This market is central to the global packaging and logistics ecosystem, ensuring accuracy, compliance, and efficiency in product identification across sectors such as food & beverages, pharmaceuticals, consumer goods, and industrial products. With sustainability, automation, and digitalization reshaping the industry, labelling services are evolving into a critical enabler of smart supply chains.

Key Insights for Industry Professionals

- Automation as Standard: High-volume industries such as food and pharma are rapidly shifting to automatic labelling systems for speed, consistency, and accuracy.

- Digital Printing Surge: Growth in digital label presses supports flexible, on-demand customization, reducing changeover times for brands with diverse SKUs.

- Smart Labelling & Traceability: Increasing adoption of QR codes, UDIs, and RFID-based labels enables enhanced product transparency and compliance with global traceability regulations.

- Sustainability Imperative: Rising demand for biodegradable and recyclable labelling materials is driving partnerships with providers offering eco-friendly solutions.

- Regulatory Alignment: Industries increasingly rely on professional labelling services to ensure compliance with complex international standards.

Market Analysis: Recent Developments in Global Labelling Services Industry

The global labelling services market is undergoing rapid transformation, driven by digital printing adoption, sustainability initiatives, and strategic consolidations. In September 2025, Domino Printing Sciences launched the N410 digital LED inkjet press at Labelexpo Europe, expanding access to digital printing for converters of all scales. Similarly, in July 2025, Comexi showcased its new D4 digital press and a flexo press, reinforcing the shift toward faster, more sustainable label production.

Mergers and acquisitions are shaping industry dynamics. In August 2025, Avery Dennison announced the acquisition of Meridian Adhesives Group’s flooring adhesives business, expanding its specialty adhesives portfolio. In the same month, Siegwerk acquired Dutch coating specialist Allinova, strengthening its coating capabilities for packaging and labelling. Additionally, Accenture acquired NeuraFlash in August 2025 to enhance its Salesforce and AI-led supply chain solutions, underscoring the growing role of digitalization in labelling services.

Rebranding and recognition also marked key milestones. In June 2025, UPM Raflatac transitioned to UPM Adhesive Materials, signaling a broader focus beyond label materials into specialty tapes and graphics. In July 2025, the National Association of Container Distributors (NACD) recognized MRP Solutions as Supplier of the Year, highlighting leadership in packaging excellence. Furthermore, Wonnda spotlighted labelling as central to automation and integrated logistics in May 2025, confirming the sector’s critical role in the packaging value chain.

Key Trends and Emerging Opportunities in the Labelling Services Market

Surging Investment in Digital Label Management and Integration Platforms

The labelling services market is witnessing a robust shift toward cloud-based, integrated label management systems, driven by the need for enhanced supply chain agility, version control, and regulatory compliance. Enterprises across industrial and consumer sectors are investing heavily in digital solutions to modernize labeling operations. According to PwC, 54% of industrial products companies and 53% of consumer goods companies found cloud-based technologies highly effective in creating operational value. Strategic acquisitions, such as LTIMindtree leveraging AI and digital expertise, enable enterprises to accelerate transformation and implement intelligent, data-driven label management platforms. Cloud-based Intelligent Label Management Systems (ILMS) offer scalability, accessibility, and enhanced collaboration, essential for global enterprises managing labeling across multiple sites. The integration of real-time data and automation ensures traceability and accuracy, while compliance pressures and the drive for supply chain efficiency make ILMS adoption a critical growth driver.

Increased Outsourcing Driven by Complex Global Regulatory Compliance

Global regulatory complexity is propelling brands to outsource labelling services to specialized providers capable of navigating multi-regional compliance requirements. Outsourcing mitigates the risk of costly product recalls, legal penalties, and reputational damage caused by non-compliance, as highlighted by Global Resources Direct. Enterprise Labeling and Artwork Management solutions, like those offered by Loftware, help companies manage regional variations efficiently, ensuring accurate labeling for traceability, nutritional information, or localized claims. Outsourcing also delivers operational efficiency, reducing repetitive in-house tasks while leveraging third-party expertise, as demonstrated by SGS DIGICOMPLY. Specialized service providers, such as NSF International, enable businesses in life sciences and regulated industries to meet complex requirements for 510(k) submissions, CE marking, and ongoing compliance. This trend positions outsourcing as a strategic pathway to reduce risk, improve efficiency, and ensure global compliance.

Service Expansion for ESG and Sustainability Labelling Verification

The increasing focus on ESG compliance and sustainability claims presents labelling service providers with a high-value opportunity to offer verification and auditing services. As “greenwashing” concerns grow, third-party verification adds credibility and consumer trust, with providers like QIMA highlighting the importance of validated sustainability claims. Partnerships with certification bodies, including NSF, allow service providers to deliver rigorous data verification, gap assessments, and secure ESG label issuance. Regulatory initiatives such as the UK’s Sustainability Disclosure and Labelling (SDR) framework are driving mandatory ESG compliance, creating demand for verification services that ensure accuracy and regulatory alignment. By transforming label printing into a comprehensive ESG verification service, providers can create a recurring revenue model while delivering high-value solutions that reinforce transparency and accountability.

On-Demand, Localized Label Printing as a Supply Chain Resiliency Service

Global supply chain disruptions have highlighted the need for decentralized and on-demand label printing, creating a strategic opportunity for service providers to enhance operational resilience. Regional digital print hubs or enterprise-grade software allow companies to print compliant labels locally, reducing reliance on centralized production. Decentralization improves supply chain resilience by distributing printing capacity across manufacturing, distribution, and retail locations, as noted by Propel Apps. Cloud-based label management systems, exemplified by Loftware, provide centralized control over templates and jobs while enabling local execution, minimizing logistical delays. On-demand printing eliminates the need to ship pre-printed labels globally, reducing costs and enabling rapid response to regulatory changes or sudden market demand. Offering these capabilities via a SaaS model provides recurring revenue for providers while granting clients flexibility, control, and agility in labeling operations.

Competitive Landscape: Top Companies in Global Labelling Services Industry

The competitive environment in labelling services is defined by global leaders in adhesives, materials science, and printing technologies, all investing in sustainability, automation, and smart labelling innovations.

Avery Dennison Corporation: Expanding Specialty Adhesives Portfolio

Avery Dennison stands as a leader in label materials and RFID-based smart labelling. In August 2025, it acquired Meridian Adhesives Group’s flooring adhesives unit, broadening its product scope. The company emphasizes linerless and recyclable labels, digital identification, and RFID technologies to meet sustainability and traceability demands. With its global footprint and innovation-driven strategy, Avery Dennison remains a front-runner in eco-friendly and high-performance labelling solutions.

CCL Industries Inc.: Strengthening Specialty Packaging and Intelligent Labels

CCL Industries is a top global player in specialty packaging and labelling, serving consumer goods, healthcare, and home care markets. In August 2025, it reported strong Q2 results driven by its CCL, Checkpoint, and Innovia divisions. CCL’s portfolio includes pressure-sensitive and in-mould labels, alongside RFID and anti-theft technologies. Its focus on digital transformation and automation ensures growth in intelligent labelling solutions that enhance supply chain security and product integrity.

3M Company: Innovating with Durable and Sustainable Label Materials

3M’s portfolio spans industrial adhesives, films, and durable label materials engineered for extreme conditions. The company continues to innovate, with its Versatile Print Label Material offering compatibility with multiple inks and printing systems. Its commitment to sustainability and high-performance adhesives aligns with customer needs across logistics, healthcare, and manufacturing. 3M’s global R&D ecosystem strengthens its ability to deliver tailored, next-generation label solutions.

UPM Adhesive Materials (Formerly UPM Raflatac): Rebranding for Growth Beyond Labels

Rebranded in June 2025, UPM Adhesive Materials reflects a broadened strategy beyond traditional label materials into graphics solutions and specialty tapes. Its product range supports food, beverage, and personal care industries with sustainable, recyclable label solutions. UPM’s vertically integrated model, from forests to finished products, ensures supply chain reliability. The company’s commitment to a fossil-free future reinforces its leadership in eco-conscious labelling services.

Lintec Corporation: Innovating with Eco-Friendly Labelstock

Lintec Corporation, a Japanese leader in adhesive products, specializes in pressure-sensitive materials for industrial and consumer labelling. The company is investing in eco-friendly labelstock compatible with digital printers, designed to enhance recyclability and container reuse. With a strong emphasis on sustainability, product safety, and continuous innovation, Lintec positions itself as a reliable global provider of advanced labelling solutions tailored to evolving regulatory and customer needs.

Labelling Services Market Share Insights

Digital Labeling Dominates Market Share by Service Type in the Labelling Services Industry

Digital labeling leads the labelling services industry with around 35% share in 2025, driven by its unmatched agility in handling short runs, variable data printing (VDP), and mass customization requirements. Unlike conventional print methods, digital labeling eliminates costly setup processes, enabling faster turnaround and cost-effective prototyping for industries facing frequent design updates or regulatory changes. This dominance is further reinforced by the growth of limited-edition products, personalized packaging campaigns, and just-in-time supply chains across food, beverage, and personal care industries. While physical labeling and printing services remain essential in high-volume production lines, digital labeling secures leadership as it meets the demand for flexibility, premium aesthetics, and compliance in dynamic global markets.

Product Labeling Retains the Largest Market Share by Application in the Labelling Services Industry

Product labeling represents the largest application segment, holding 30% of the labelling services industry in 2025, as it encompasses the foundational need for branding, ingredient information, and consumer communication across virtually all packaged goods. This segment is essential in consumer markets such as food and beverages, healthcare, cosmetics, and industrial goods, where labeling not only delivers mandatory product data but also enhances shelf appeal and consumer trust. The reliance on professional services for design, compliance, and large-scale execution underpins the size of this category. Barcoding and RFID labeling also account for a significant share, fueled by the rapid rise of e-commerce and omnichannel logistics requiring accurate, real-time tracking. Regulatory and compliance labeling remains non-negotiable, particularly in pharmaceuticals and chemicals, making it a high-value, risk-averse driver. Together, these applications highlight how product labeling secures volume leadership while compliance and traceability solutions enhance strategic value across industries.

United States Labelling Services Market Driven by Cybersecurity Initiatives and Food Safety Programs

The U.S. labelling services market is witnessing robust growth driven by government-led initiatives and rising consumer demand for product transparency. The Cyber Trust Mark, launched by the White House in early 2025, functions as an “Energy Star for cybersecurity” and is creating a specialized segment for cybersecurity labeling in consumer electronics. Simultaneously, the U.S. Environmental Protection Agency (EPA) has introduced a new labeling program for climate-friendly construction materials, backed by a $100 million investment under the Inflation Reduction Act, boosting demand for compliance and verification labeling services.

Market demand is further reinforced by a growing focus on food and product safety, which is increasing the adoption of smart labels, QR codes, and traceable labels providing real-time expiration dates, recall information, and product origin details. The Government Service Delivery Improvement Act of 2025 emphasizes clearer information dissemination across federal agencies, highlighting the broader governmental trend toward standardized labeling practices, which supports the growth of labelling service providers.

European Union Labelling Services Market Expands Through Packaging Regulations and Chemical Compliance

The EU labelling services market is primarily driven by regulatory compliance and sustainability initiatives. The Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandates standardized labeling on all packaging to guide consumers in proper waste sorting, specifying material composition and disposal methods. The Regulation (EU) 2024/2865, effective December 2024, amends the CLP Regulation, requiring precise font sizes, colors, and layouts to improve readability, creating opportunities for specialized printing and design services.

The same regulation allows fold-out labels and the inclusion of digital label formats by July 2026, enhancing flexibility for packaging companies. REACH regulations continue to impose stricter limits on hazardous substances, increasing the demand for updated compliant labels for industrial and consumer chemicals. These regulatory drivers are fueling growth in high-quality, value-added labelling services across the European Union.

China Labelling Services Market Fueled by Digital Transformation and Anti-Counterfeiting Measures

China’s labelling services market is undergoing rapid transformation under the “14th Five-Year Plan”, which emphasizes digital and intelligent manufacturing. Automation and smart technologies are becoming widespread, particularly in e-commerce and high-value sectors such as consumer electronics, pharmaceuticals, and luxury products. Anti-counterfeiting and security labels are gaining traction to protect premium goods and ensure product authenticity.

Chinese manufacturers are also innovating in sealing and labeling machinery to enhance operational efficiency and precision. The e-commerce boom has further increased the demand for variable data labels, including barcodes and QR codes, to improve inventory management, tracking, and logistics. The combined effect of digitalization, smart labeling, and anti-counterfeiting measures is positioning China as a leading hub for advanced labelling services in Asia.

India Labelling Services Market Boosted by PLI/DLI Schemes and Food Safety Regulations

India’s labelling services market is expanding rapidly due to government initiatives promoting domestic manufacturing and compliance. The Production Linked Incentive (PLI) and Design Linked Incentive (DLI) schemes are creating a robust ecosystem for domestic production, catering to both local and export markets. The Food Safety and Standards Authority of India (FSSAI) is driving food labeling standards, promoting QR code-based traceability systems to enhance transparency and combat food fraud.

The 2022 ban on certain single-use plastics has created new opportunities for eco-friendly and water-soluble packaging labels, while the Make in India initiative continues to expand the domestic manufacturing base across industries such as automotive, electronics, and consumer goods. These regulatory and policy-driven trends are significantly increasing demand for innovative, compliant, and sustainable labeling services across India.

Japan Labelling Services Market Advances with Profit-Oriented Strategy and Sustainability Focus

Japan’s labelling services market reached $4.3 billion in 2024, marking a 2.4% year-on-year growth the highest in five years. The industry is shifting from volume-based growth to profit-oriented strategies, emphasizing value-added features in pressure-sensitive labels. Regulatory initiatives, including the Plastic Resource Circulation Promotion Law (2025), encourage the reduction or redesign of single-use plastics, driving demand for reusable and compostable labels.

The food and beverage sector is a key growth driver, with pressure-sensitive labels dominating packaging while non-adhesive formats, such as shrink labels, gain popularity in the beverage and alcohol industries. Japanese manufacturers are focusing on high-performance, functional labels, including self-sealing and durable formats, to meet diverse industry requirements and sustainability objectives.

Canada Labelling Services Market Driven by Food Transparency and Traceability Programs

Canada’s labelling services market is experiencing strong growth due to evolving food labeling regulations and consumer demand for transparency. The Food Labelling Modernization (FLM) initiative, overseen by the Canadian Food Inspection Agency (CFIA), mandates front-of-pack (FOP) labeling to indicate sodium, sugar, and saturated fat content, with the transition period ending on December 31, 2025.

Collaborations between the Retail Council of Canada (RCC), government, and industry stakeholders are further reinforcing accurate and clear labeling, including updated criteria for “Made in Canada” claims. Rising consumer interest in sustainability and traceability, along with initiatives like the “Boat-to-Plate” seafood traceability program, is creating demand for advanced labeling services and supply chain infrastructure, establishing Canada as a significant market for compliance and eco-friendly labelling solutions.

Labelling Services Market Report Scope

Labelling Services Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6 Billion

|

|

Market Size (2034)

|

$11.1 Billion

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Service Type (Digital Labeling, Physical Labeling, Data Labeling & Annotation, Consulting & Compliance Services, Printing & Finishing Services), By Application (Product Labeling, Barcoding & RFID, Brand & Security Labeling, Regulatory & Compliance Labeling, Information & Instructional Labeling), By End-Use Industry (Food & Beverages, Consumer Goods, Healthcare & Pharmaceuticals, Industrial, Automotive, Electronics, Cosmetics & Personal Care, Retail & E-commerce), By Technology (Pressure-Sensitive Labels, Shrink Sleeve Labels, In-Mold Labels, Wet-Glue Labels, Other Technologies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avery Dennison Corporation, CCL Industries Inc., 3M Company, RR Donnelley & Sons Company, All4Labels Group GmbH, Lintec Corporation, Avery Products Corporation, Sato Holdings Corporation, Quad/Graphics, Inc., WestRock Company, Sonoco Products Company, Multi-Color Corporation, Cenveo Worldwide Limited, Smyth Companies, LLC, Esko-Graphics

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Labelling Services Market Segmentation

By Service Type

- Digital Labeling

- Physical Labeling

- Data Labeling & Annotation

- Consulting & Compliance Services

- Printing & Finishing Services

By Application

- Product Labeling

- Barcoding & RFID

- Brand & Security Labeling

- Regulatory & Compliance Labeling

- Information & Instructional Labeling

By End-Use Industry

- Food & Beverages

- Consumer Goods

- Healthcare & Pharmaceuticals

- Industrial

- Automotive

- Electronics

- Cosmetics & Personal Care

- Retail & E-commerce

By Technology

- Pressure-Sensitive Labels

- Shrink Sleeve Labels

- In-Mold Labels

- Wet-Glue Labels

- Other Technologies

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Labelling Services Market

- Avery Dennison Corporation

- CCL Industries Inc.

- 3M Company

- RR Donnelley & Sons Company

- All4Labels Group GmbH

- Lintec Corporation

- Avery Products Corporation

- Sato Holdings Corporation

- Quad/Graphics, Inc.

- WestRock Company

- Sonoco Products Company

- Multi-Color Corporation

- Cenveo Worldwide Limited

- Smyth Companies, LLC

- Esko-Graphics

* List Not Exhaustive

Methodology

USDAnalytics applies a multi-layered research methodology to the Labelling Services Market, combining rigorous primary research structured interviews with C-level supply-chain managers, label converters, print-hub operators, regulatory affairs specialists and packaging technologists with exhaustive secondary research across company filings, industry reports, regulatory texts (PPWR, UDI/UDI rules), trade data and patent landscapes to validate technology adoption and service models. Market sizing and the CAGR projection (2025–2034) use a blended bottom-up approach (site capacities, digital press deployment, service contract volumes) cross-checked by top-down demand drivers (end-use sector growth, e-commerce penetration, regulatory mandates) while segmentation and share analysis incorporate deployment metrics for digital vs. conventional printing, RFID/barcode volumes and service-type revenue streams. Technology and trend validation leverages lab performance data, ILMS vendor benchmarks, and pilot-client case studies for cloud-based label management, automated applicators and smart-labelling integrations; competitive positioning is informed by M&A tracking, vendor capability matrices and pricing elasticity models. Finally, scenario modeling tests regulatory shocks (accelerated EPR rollouts, expanded traceability mandates), supply-chain disruptions, and digital decentralization (on-demand local print hubs) to generate risk-aware, actionable recommendations for procurement, operations and sustainability teams.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.