Market Overview: Key Industry Statistics

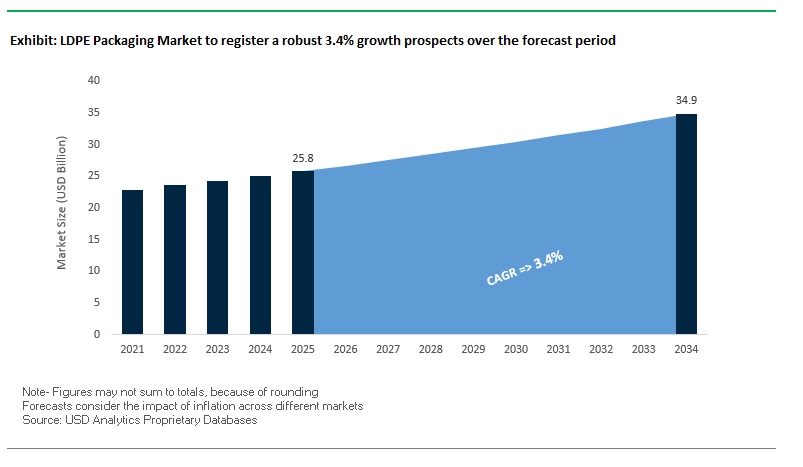

The Global LDPE Packaging Market is expected to expand from USD 25.8 billion in 2025 to USD 34.9 billion by 2034, registering a CAGR of 3.4%. Low-Density Polyethylene (LDPE) remains one of the most widely used packaging materials due to its flexibility, moisture resistance, and cost-effectiveness. The market is undergoing a critical transformation as sustainability, food safety, and performance-based innovation reshape procurement and investment decisions.

For industry professionals, the market addresses pressing questions about circular economy adoption, e-commerce growth, compliance standards, and material performance upgrades. The shift toward recycled LDPE (R-LDPE), accelerated by regulations like the EU PPWR, is at the center of procurement strategies. E-commerce has amplified the demand for lightweight and protective films, while advanced LDPE grades now deliver improved MVTR, puncture resistance, and tensile strength, ensuring durability for applications across food, healthcare, and consumer goods.

Key Insights for Buyers and Industry Leaders

- Circular economy imperative: R-LDPE adoption is accelerating under EU and U.S. regulations.

- E-commerce driver: Poly mailers and protective films are fueling LDPE demand in logistics.

- Performance innovation: New LDPE films enhance moisture, tear, and puncture resistance.

- Food safety compliance: LDPE remains FDA-approved for food contact, boosting adoption in regulated sectors.

Market Analysis: Recent Developments in LDPE Packaging

The LDPE packaging industry has seen a wave of strategic investments, acquisitions, and product launches, reflecting the dual push for sustainability and high-performance films. In August 2025, Mauser Packaging Solutions joined the Association of Plastic Recyclers (APR), reinforcing its commitment to circular economy goals and recyclability standards. In the same month, Mondi introduced Ad/Vantage Smooth Brown Semi Extensible kraft paper, highlighting cross-material innovations that complement LDPE’s role in flexible packaging. Graphic Packaging International, also in August 2025, launched a child-resistant paperboard detergent pod package, showing how paperization trends influence LDPE alternatives in specific applications.

Technological advances are being showcased at industry events. In July 2025, Comexi displayed new D4 digital and flexo presses at Labelexpo Europe, demonstrating the link between advanced printing technologies and high-quality flexible packaging, including LDPE. Strategic collaborations continue to emerge—SCHÜTZ GmbH & Co. KGaA’s May 2025 partnership in Saudi Arabia to produce ECOBULK IBCs shows the convergence of rigid and flexible solutions in food logistics, where LDPE liners are often critical. Similarly, Wonnda’s May 2025 report positioned LDPE as a central enabler of automation-ready, sustainable packaging, especially in e-commerce and food supply chains.

M&A activity remains a major driver. In November 2024, Amcor’s acquisition of Berry Global created the world’s largest resin buyer, reshaping global LDPE supply and pricing. The October 2024 merger of Smurfit Kappa and WestRock consolidated the fiber packaging industry but also influences LDPE integration in hybrid paper-plastic solutions.

Key Trends and Emerging Opportunities in the LDPE Packaging Market

Strategic Investment in Recycled Content Production and Advanced Recycling Integration

The LDPE packaging market is witnessing a strong push toward integrating post-consumer recycled (PCR) content into flexible packaging, driven by regulatory mandates, brand sustainability goals, and circular economy initiatives. Global petrochemical leaders are making significant capital investments to increase the production of food-grade recycled LDPE. ExxonMobil, for instance, plans to invest over $200 million to expand advanced recycling operations in Baytown and Beaumont, Texas, targeting a global recycling capacity of 1 billion pounds per year by 2027. Similarly, Repsol is investing €26 million to manufacture LDPE and HDPE plastics with 10%–80% recycled content, aligning with Europe’s 2030 recycled content targets. Strategic acquisitions, such as Dow’s purchase of Circulus in North America, ensure a stable supply of high-quality PCR for LDPE applications. Importantly, FDA approvals, like the Letter of Non-Objection for Circulus’ Ardmore facility, confirm the suitability of recycled LDPE for food-contact applications, overcoming a historical barrier to mechanical recycling. This trend underscores the convergence of regulatory compliance, corporate ESG initiatives, and technological advancement in recycled LDPE production.

Lightweighting and Downgauging Driven by EPR Cost Pressures

Extended Producer Responsibility (EPR) schemes are transforming the economics of LDPE packaging by linking regulatory fees to package weight and recyclability. This is accelerating the adoption of downgauging strategies, where packaging materials are optimized to minimize resin use while maintaining structural integrity. Advanced high-performance resins, such as ExxonMobil’s Exceed™ S, enable thinner films without compromising stiffness or toughness, crucial for transportation and storage applications. Investment in modern blown film lines ensures consistent production of downgauged films at scale. Beyond cost reduction, lightweighting reduces the carbon footprint associated with both production and logistics, aligning with corporate ESG objectives. This dual benefit reinforces lightweighting as a strategic response to both environmental and economic pressures in the LDPE packaging industry.

Development of High-Performance Mono-Material LDPE Packaging Solutions

The global focus on recyclability and circularity presents a significant opportunity to replace multi-material laminates with mono-material LDPE packaging. Mono-material structures ensure compatibility with single-stream recycling systems, enhancing the efficiency of post-consumer recycling. Innovations in barrier coatings and multi-layer LDPE film structures provide oxygen and moisture protection, critical for food and beverage applications, without compromising recyclability. Collaborations across the value chain, exemplified by Sabic and Mars’ closed-loop recycling project for KIND® snack bar wrappers, demonstrate how resin producers, converters, and brand owners can collectively deliver market-ready mono-material solutions. This opportunity not only addresses sustainability goals but also strengthens brand positioning by promoting eco-friendly packaging credentials.

LDPE Films for Agricultural Sustainability: Reducing Methane Emissions from Silage

Beyond traditional food packaging, LDPE films are finding applications in agriculture, particularly in silage coverage for livestock feed. High-barrier LDPE films help reduce dry matter losses and fermentation inefficiencies, directly lowering methane emissions from livestock. Scientific studies, including publications in the Journal of Dairy Science, validate the environmental benefits of these specialized films. The use of high-performance silage films enhances global food security by preserving feed quality while mitigating greenhouse gas emissions. This trend offers LDPE manufacturers a compelling value proposition, positioning their products as carbon-reduction tools in agriculture. Early adoption in livestock-intensive markets such as the U.S. and Ireland illustrates tangible success cases, establishing LDPE agricultural films as both an environmental and economic solution for sustainable farming practices.

Competitive Landscape: Top Companies in LDPE Packaging

The LDPE packaging sector is dominated by global packaging giants, polymer innovators, and protective packaging leaders who are reshaping the market through sustainability and product innovation.

Amcor plc: Leading with global scale and sustainability commitments

Amcor offers a broad portfolio of LDPE films, laminates, and specialty solutions across food, healthcare, and FMCG. Its 2024 acquisition of Berry Global positioned it as the world’s largest resin purchaser, creating unmatched buying power and supply chain leverage. With a strong focus on recyclable, reusable, and compostable packaging, Amcor continues to work closely with brand owners to introduce mono-material LDPE packaging aligned with circular economy targets.

Berry Global Group Inc.: Expanding sustainable packaging capacity

Berry Global is a leading manufacturer of LDPE films, bags, and pouches, with strong penetration in foodservice and consumer packaging. In 2025, it invested USD 110 million in North America to expand clear, sustainable foodservice packaging production. Its Sustane® brand highlights recycled LDPE solutions, reflecting its push toward low-carbon and circular packaging systems.

Sealed Air Corporation: Innovating for e-commerce and logistics

Sealed Air is renowned for protective LDPE packaging, particularly for e-commerce and industrial markets. Its AUTOBAG® automated bagging solutions use LDPE films optimized for high-speed operations. With a global focus on recycled-content materials and automation, Sealed Air is addressing growing demand for durability, sustainability, and supply chain efficiency.

Mondi Group: Diversifying sustainable packaging offerings

Mondi produces LDPE films and hybrid flexible packaging solutions, serving e-commerce, retail, and food sectors. Its recent innovations, like FunctionalBarrier papers, reflect its strategy to replace conventional plastics while still offering LDPE-based barrier films and laminates where performance is critical. Mondi’s pledge to make all packaging recyclable or compostable by 2025 places it at the forefront of regulatory compliance.

LyondellBasell Industries N.V.: Advancing recycled and bio-circular polymers

LyondellBasell is a leading supplier of LDPE resins under its Circulen brand, which focuses on recycled and bio-circular polymers. Its advanced recycling technologies allow the production of LDPE with lower carbon intensity, supporting global brand owners under pressure to meet scope 3 emission targets. Its expertise in polymer chemistry ensures continued leadership in low-impact, high-performance LDPE.

The Dow Chemical Company: Innovating with REVOLOOP™ resins

Dow is a global leader in polymer science, offering LDPE resins and films designed for food, healthcare, and industrial markets. Its REVOLOOP™ recycled plastics resins are designed to reduce carbon footprint while maintaining high mechanical properties. Dow is also investing in digital traceability and smart packaging solutions, making it a key partner for companies seeking both performance and sustainability in LDPE packaging.

LDPE Packaging Market Share Insights

Films & Wraps Dominate Market Share by Product Type in the LDPE Packaging Industry

Films and wraps represent the largest share of the LDPE packaging market, accounting for nearly 45% of total demand in 2025, due to their indispensable role in flexible packaging across multiple sectors. LDPE films are valued for their clarity, moisture resistance, and heat-sealing capability, making them essential for food wraps, stretch films, and as inner sealing layers in multi-layer pouches. Their cost-effectiveness and versatility ensure adoption in both consumer and industrial packaging applications. Bags and sacks follow closely, commanding a strong share because of their durability and widespread use in retail, agriculture, and industrial sectors. Meanwhile, LDPE bottles, droppers, and closures hold more specialized shares where flexibility, squeezability, and chemical resistance are required, such as in cosmetics, household chemicals, and pharmaceuticals. The product segmentation highlights how films and bags secure leadership through volume efficiency, while bottles and closures cater to specialized, high-value niches.

Food and Beverages Retain the Largest Market Share by Application in the LDPE Packaging Industry

The food and beverages sector dominates the LDPE packaging industry with 40% share in 2025, reflecting the material’s unmatched ability to maintain freshness, prevent moisture loss, and extend shelf life. LDPE films are extensively used in bread bags, frozen food packaging, fresh produce wrapping, and dairy liners, while stretch wraps secure pallets of food products during transport. Consumer goods and e-commerce also represent critical demand drivers, with LDPE providing durability for shopping bags, protective mailers, bubble wrap, and air pillows that safeguard items in logistics chains. Niche applications in personal care, pharmaceuticals, and electronics leverage LDPE’s flexibility and resistance to chemicals, though volumes are comparatively lower. Collectively, this segmentation underscores how food and beverages anchor LDPE demand, while e-commerce and consumer goods provide strong growth momentum.

United States LDPE Packaging Market Driven by Regulatory Reforms and E-Commerce Expansion

The U.S. LDPE packaging market is heavily shaped by a fragmented regulatory landscape, including state-level bans on single-use plastics and polystyrene foam containers. Recent laws in Delaware prohibiting plastic rings and shrink wraps for beverage containers are accelerating the adoption of sustainable LDPE packaging solutions. Technological innovations, such as recycling initiatives by Berry Global to enhance the Sustane line of recycled polymers, are further strengthening market growth.

Corporate investments are fueling expansion, with major players adopting advanced recycling technologies to improve the performance of recycled LDPE for high-demand applications. Key market segments include e-commerce, food and beverage, and pharmaceutical packaging, where the demand for flexible, lightweight, and durable LDPE films has surged due to the “Amazon Effect.” Sustainability is a core focus, with increasing adoption of bio-based LDPE derived from renewable feedstocks such as sugarcane, supporting carbon footprint reduction and eco-friendly packaging objectives.

Germany LDPE Packaging Market Propelled by Circular Economy and Food-Safe Innovations

Germany’s LDPE packaging industry is influenced by stringent regulations, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025, which mandates fully recyclable or reusable packaging by 2030. This regulatory framework is driving adoption of recycled and mono-material LDPE solutions, particularly in food-safe and high-performance applications.

Technological innovation is a key market driver. Products such as KP Flexivac multi-layer vacuum films from Dow and Klöckner Pentaplast demonstrate the shift towards 100% recyclable LDPE packaging for meat and poultry. The Packaging Act (VerpackG) further incentivizes sustainable design and recyclability, fostering growth in high-performance LDPE films. Corporate investments, including Berry Global’s expansion of recycling capacity in Steinfeld, Germany, support production of eco-friendly and high-quality LDPE packaging solutions for European markets.

China LDPE Packaging Market Accelerates with Green Policies and Smart Manufacturing

China’s LDPE packaging market is advancing under the “dual carbon” goal, emphasizing sustainable production and recycling. The Action Plan for Large-Scale Equipment Updates encourages eco-friendly materials across industries, while new national standards like GB/T 31268 and upcoming recycled plastics regulations enforce recyclable packaging design.

Technological advancements, including AI-enabled automation and 5G industrial internet integration, are optimizing production efficiency and flexible manufacturing capacity. Domestic manufacturing is expanding, with companies such as Sinopec producing high-performance LDPE for agricultural films and packaging. Growth in e-commerce, electronics, and automotive sectors is driving demand for innovative LDPE packaging with enhanced durability and sustainability features.

India LDPE Packaging Market Expands Through Circular Economy Initiatives and Industrial Growth

India’s LDPE packaging industry is benefiting from government initiatives like the Make in India program and the Smart Cities Mission, which drive demand for sustainable LDPE packaging in construction and infrastructure sectors. The circular economy focus creates opportunities for companies providing innovative and eco-friendly LDPE solutions.

Technological adoption is rising, with LDPE shrink films preferred for their strength and durability for heavier and larger items. Corporate investments are increasing, led by Reliance Industries Limited, a major domestic LDPE producer. Key applications include the food processing, cold chain, and pharmaceutical sectors, where exports are creating demand for high-performance LDPE packaging solutions that comply with international safety standards.

Japan LDPE Packaging Market Strengthened by Advanced Manufacturing and High-Performance Innovations

Japan’s LDPE packaging market leverages precision manufacturing and advanced material technologies. Regulatory support through the Plastic Resource Circulation Act guides the market toward sustainable design and reduced single-use plastics, while companies are shifting toward specialty LDPE products with superior barrier and self-sealing properties.

Market focus is on high-value applications, where Sumitomo Chemical and other players are enhancing LDPE production for specialty uses. The industry emphasizes high-performance, functional LDPE packaging to meet stringent quality standards in food, pharmaceutical, and industrial sectors. Innovation is driving growth in value-added packaging materials with enhanced durability and environmental compliance.

Brazil LDPE Packaging Market Grows with Bio-Based Solutions and Strategic Corporate Investments

Brazil’s LDPE packaging market is evolving under sustainable waste management policies such as the National Solid Waste Policy and trade measures like provisional antidumping duties on PE imports, creating opportunities for domestic production. Bio-based LDPE, such as Braskem’s “I’m green” sugarcane-derived products, is gaining traction in the market.

Technological advancements include innovative sustainable LDPE films for food, beverage, and agricultural applications, supporting ready-to-eat and processed food packaging. Corporate investments, including Braskem’s partnerships with Nestlé, are driving the development of eco-friendly, high-performance LDPE solutions, positioning Brazil as a key player in the Latin American LDPE packaging industry.

LDPE Packaging Market Report Scope

LDPE Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.8 Billion

|

|

Market Size (2034)

|

$34.9 Billion

|

|

Market Growth Rate

|

3.4%

|

|

Segments

|

By Product Type (Films & Wraps, Bags & Sacks, Bottles & Droppers, Caps & Closures, Others), By Application (Food & Beverages, Personal Care & Cosmetics, Electrical & Electronics, Consumer Goods, Pharmaceuticals, E-commerce, Other Applications), By Technology (Blown Film Extrusion, Cast Film Extrusion, Injection Molding, Blow Molding, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mondi plc, Amcor plc, Berry Global Inc., Sealed Air Corporation, Dow Inc., Chevron Phillips Chemical Company LLC, ExxonMobil Chemical Company, LyondellBasell Industries Holdings B.V., Braskem S.A., Borealis AG, SABIC, Westlake Chemical Corporation, Reliance Industries Limited, Sumitomo Chemical Co., Ltd., China Petrochemical Corporation (Sinopec)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

LDPE Packaging Market Segmentation

By Product Type

- Films & Wraps

- Bags & Sacks

- Bottles & Droppers

- Caps & Closures

- Others

By Application

- Food & Beverages

- Personal Care & Cosmetics

- Electrical & Electronics

- Consumer Goods

- Pharmaceuticals

- E-commerce

- Other Applications

By Technology

- Blown Film Extrusion

- Cast Film Extrusion

- Injection Molding

- Blow Molding

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in LDPE Packaging Market

- Mondi plc

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- Dow Inc.

- Chevron Phillips Chemical Company LLC

- ExxonMobil Chemical Company

- LyondellBasell Industries Holdings B.V.

- Braskem S.A.

- Borealis AG

- SABIC

- Westlake Chemical Corporation

- Reliance Industries Limited

- Sumitomo Chemical Co., Ltd.

- China Petrochemical Corporation (Sinopec)

* List Not Exhaustive

Methodology

USDAnalytics applies a comprehensive and multi-source research methodology to deliver accurate and reliable insights into the Global LDPE Packaging Market. The study integrates primary and secondary research techniques to ensure data precision and relevance. Primary research consisted of in-depth interviews and surveys with key stakeholders, including polymer scientists, packaging manufacturers, sustainability officers, and regulatory experts across major markets such as the U.S., Germany, China, India, Japan, and Brazil. Secondary research drew upon company annual reports, industry white papers, trade association publications, government databases, patent repositories, and peer-reviewed journals to validate market intelligence. Advanced data triangulation techniques were used to confirm market sizing, share distribution, and CAGR estimations, incorporating macroeconomic indicators, resin pricing trends, and technology adoption rates. Both top-down and bottom-up forecasting models were applied to assess future market performance, while regional dynamics were analyzed in the context of evolving circular economy policies, recycling infrastructure, and consumer sustainability trends. This layered approach allows USDAnalytics to produce fact-based, actionable insights that reflect real-world industry behavior and guide strategic decisions for packaging manufacturers, investors, and policymakers worldwide.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.