Metal Food Cans Market Overview: Size, Growth, and Key Insights

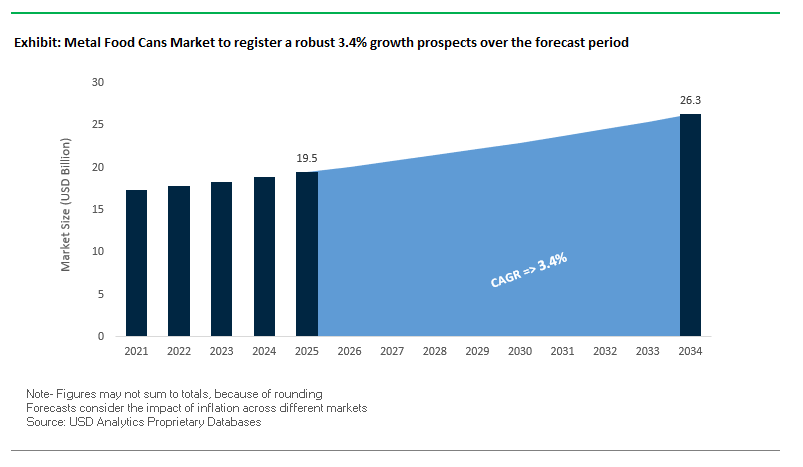

The global Metal Food Cans Market is projected to reach $19.5 billion in 2025 and is expected to expand to $26.3 billion by 2034, registering a CAGR of 3.4% over the forecast period. This growth reflects a balance between sustainability imperatives, food safety needs, and consumer convenience trends. Metal cans continue to dominate the food packaging sector due to their ability to preserve food for extended periods without refrigeration, which positions them as a reliable solution for both developed and emerging markets. The market’s resilience is reinforced by innovations in lightweighting and eco-design, where manufacturers are reducing resource consumption while maintaining structural integrity.

For industry professionals, the core questions revolve around how sustainability is reshaping supply chains, whether innovations in can formats are improving consumer acceptance, and how regulatory and corporate commitments to carbon reduction will influence production costs. Another critical dimension is the shifting consumer behavior toward on-the-go consumption and single-serve packaging, which is reshaping demand patterns globally.

Key Insights Driving Market Growth:

- Sustainability leadership: Aluminum and steel cans are 100% recyclable and can be reused infinitely without quality loss, supporting circular economy targets.

- Superior shelf-life advantage: Metal cans act as a robust barrier against oxygen, light, and moisture, ensuring food safety and nutritional value retention.

- Lightweighting trend: Thinner walls and material efficiency are lowering costs and reducing carbon footprints across supply chains.

- Consumer convenience: The rise of easy-open lids and varied can sizes aligns with the demand for ready-to-eat meals and portable food solutions.

Market Analysis: Developments Reshaping the Metal Food Cans Industry

The metal food cans industry has witnessed significant strategic and sustainability-driven developments over the past 18 months. These developments highlight the dual priorities of strengthening financial positions and deepening sustainability commitments.

In August 2025, Ball Corporation divested a major ownership stake in its Saudi joint venture to sharpen focus on its core businesses, while Crown Holdings secured SBTi validation for its net-zero target, demonstrating strong momentum in corporate decarbonization goals. Around the same period, Ardagh Group announced a sweeping recapitalization initiative to reduce debt burdens, a move designed to stabilize operations and fuel future growth. Meanwhile, Silgan Holdings reported strong second-quarter 2025 results, reinforcing its reputation as a consistent player in rigid packaging.

Earlier in the year, Crown Holdings announced the addition of a new high-speed production line in Brazil (May 2025), signaling capacity expansion in growth regions, while Trivium Packaging’s April 2025 sustainability report confirmed a tangible 2% reduction in Scope 1 and 2 emissions. In January 2025, CPMC Holdings was delisted from the Hong Kong Exchange following a compulsory acquisition, marking a key restructuring within the Asian market. Looking back to May 2024, Sonoco Products Company’s acquisition of Eviosys was a defining deal that positioned Sonoco as a global leader in food cans and aerosol packaging.

Transformative Trends and Strategic Opportunities in the Metal Food Cans Market

Mandatory Transition to Non-BPA and Next-Generation Sustainable Linings

The metal food cans market is undergoing a regulatory-driven transformation, with governments mandating the replacement of Bisphenol A (BPA) and other substances of concern in internal coatings. The European Commission Regulation (EU) 2024/3190, effective January 2025, enforces a complete ban on BPA in food contact coatings, with compliance deadlines extending to July 2026. This marks a shift from voluntary adoption to mandatory compliance, compelling canmakers to invest in new coating chemistries.

Leading manufacturers are responding proactively. Trivium Packaging announced in late 2024 that it is fully prepared to transition the majority of its product portfolio to BPA non-intent (BPA-NI) lacquers, encouraging customers to make early conversions. Similarly, PPG expanded its non-BPA portfolio with the launch of PPG Hoba Pro 2848, engineered for aluminum bottles and compliant with new safety standards, earning recognition at the 2025 ADF Innovation Awards. Beyond BPA, the industry is moving toward coatings free of formaldehyde, styrene, and other NIAS, to avoid “regrettable substitutions” and future-proof compliance.

While the U.S. has not introduced a universal BPA ban, FDA restrictions on infant-related packaging and consumer-driven demand have accelerated adoption. By 2020, the Can Manufacturers Institute reported that 95% of food cans in the U.S. were BPA-free, underscoring how market forces and global regulation are aligning to create a new standard of safety and sustainability for food packaging worldwide.

Strategic Reshoring and Supply Chain Securement for National Food Security

Geopolitical tensions, pandemic disruptions, and trade conflicts have reshaped priorities for governments and corporations, making domestic can manufacturing capacity a critical pillar of food security. The U.S. government, through the National Institute of Standards and Technology (NIST), is promoting reshoring initiatives to reduce reliance on foreign supply chains and safeguard essential food packaging availability.

Large food processors are following suit, investing in regional canning infrastructure to shorten lead times and secure capacity. For example, a major U.S. food company announced in mid-2025 the expansion of its domestic manufacturing footprint, adding new canning lines dedicated to soups and vegetables. Policymakers view local food packaging capability as a matter of national security, ensuring uninterrupted access to essentials like infant formula and canned goods during crises. This strategic reshoring trend is positioning the metal food cans market as a critical enabler of resilient and self-sufficient food supply chains.

Development of Advanced Easy-Open Ends for Senior and Accessibility Markets

An aging global population is creating strong demand for senior-friendly and accessible can ends. According to the World Health Organization (WHO), the number of people aged 60 and above will double by 2050, many of whom face mobility and dexterity challenges. This demographic shift is encouraging canmakers to redesign easy-open ends with reduced pull force, improved ergonomics, and enhanced safety.

Innovations include Trivium Packaging’s OptiLift® easy-open end, which features enhanced finger access and requires significantly less effort to open. Other advancements focus on smoother edges and wider pull tabs to prevent injuries and make cans easier to handle for seniors. Packaging design firms note that modifications in scoring patterns and pivot mechanisms can further lower resistance, making cans safer and more user-friendly. As consumer brands increasingly prioritize inclusivity, easy-open ends tailored for seniors represent a high-value niche opportunity with global growth potential.

Integration of Digital Watermarking for Precision Recycling and Circular Economy

The transition to a circular economy is accelerating innovation in recycling technologies, with digital watermarking emerging as a breakthrough enabler for precision sorting. The EU Packaging and Packaging Waste Regulation (PPWR), approved in December 2024, sets strict recycled content and design-for-recycling mandates, creating strong financial incentives for adoption.

The HolyGrail 2.0 initiative has demonstrated that embedding invisible digital watermarks on cans enables high-speed recognition by optical sorting systems, reaching speeds of 3 meters per second. This allows recyclers to separate packaging types with unprecedented precision, ensuring cleaner metal streams and higher yields of high-quality recycled content. Pilot projects across Europe have validated the technical and commercial feasibility of digital watermarking. For canmakers, this technology not only ensures compliance with EU regulations but also strengthens their role in enabling brand owners to meet sustainability pledges and recycled content targets. As the industry embraces the circular economy, digital watermarking will emerge as a cornerstone innovation for the future of sustainable metal food cans.

Competitive Landscape of the Global Metal Food Cans Industry

The global metal food cans industry is dominated by multinational packaging leaders with deep expertise in recyclable materials, food safety technologies, and sustainability programs. These companies are actively reshaping the competitive landscape through financial restructuring, acquisitions, and environmental strategies. Below is an overview of key players driving innovation and growth.

Trivium Packaging: Sustainability at the Core of Strategy

Trivium Packaging has positioned itself as a global leader in infinitely recyclable metal packaging solutions, catering to food segments such as soups, seafood, and vegetables. In September 2024, the SBTi validated its near-term emissions reduction targets, strengthening its credibility as a climate-conscious leader. Almost half of Trivium’s revenue comes from eco-designed products, demonstrating a deep alignment with circular economy principles. Additionally, its technical design and integration services enable food brands to align product launches with sustainability goals, making Trivium a preferred partner for eco-conscious clients.

Silgan Holdings Inc.: Consistent Value Creation and Market Leadership

Silgan Holdings stands out in the North American and European food can market, producing a diverse range of containers for human and pet food. In August 2025, the company announced its 21st consecutive year of dividend increases, underscoring financial stability and shareholder value creation. Its acquisition of Gateway Plastics in September 2021 expanded its closures portfolio, highlighting its focus on innovation and growth. With strengths in both regulatory compliance and product diversity, Silgan remains a dominant force in food and pet packaging markets.

Crown Holdings, Inc.: Driving Net-Zero Packaging Futures

Crown Holdings continues to demonstrate leadership in metal food can technology with a strong focus on decarbonization. In August 2025, it secured SBTi validation for its net-zero target and posted strong financial results, with a 19% YoY increase in adjusted diluted EPS. Its flagship Twentyby30 program reflects a commitment to ESG initiatives across its global footprint. Crown’s advanced coatings and linings also provide critical protection against corrosion and food degradation, making its cans the benchmark for food safety and quality.

Ardagh Group: Strengthening Finances to Fuel Innovation

Ardagh Group is a major supplier of recyclable glass and metal packaging, with a strong footprint in food cans. In July 2025, the company launched a recapitalization strategy to deleverage its operations, fortifying its financial resilience. Its strategy emphasizes sustainability and innovation, focusing on material efficiency and reduced energy consumption. With a global manufacturing presence, Ardagh leverages best practices across markets, ensuring high-quality and sustainable solutions for its food industry clients.

Ball Corporation: Innovating Beyond Beverage Cans

While traditionally associated with beverage packaging, Ball Corporation has a strong stake in the food can market, particularly with aluminum-based solutions. Its April 2024 partnership with CavinKare to launch retort aluminum cans for milkshakes demonstrates its adaptability in expanding applications. Ball is aggressively pursuing a decarbonization pathway, aiming for a 16% reduction in value chain emissions by 2030 and 100% renewable electricity across operations. Its expertise in lightweight and durable packaging makes it a strong innovator in the evolving food can segment.

Metal Food Cans Market Share Insights

Steel Maintains Majority Market Share by Material in the Metal Food Cans Industry

Steel commands 62% of the global metal food cans market, cementing its position as the backbone of long-shelf-life food preservation. Its superior mechanical strength enables the safe packaging of low-acid foods such as vegetables, soups, and meats, which require intense high-temperature retort sterilization that would deform weaker materials. Steel cans are also favored for large-volume formats—notably in pet food and institutional catering—where durability, vacuum resistance, and stackability are critical for distribution efficiency. Cost-effectiveness further reinforces its dominance, as steel provides robust packaging at scale while meeting recyclability targets in both mature and emerging markets. By contrast, aluminum continues to serve a critical niche for acidic foods like tomatoes and fruits, where corrosion resistance and lightweight handling enhance convenience. The material split reflects a balance of functional resilience, safety compliance, and application-specific performance, with steel remaining indispensable for high-volume global supply chains.

Fruits and Vegetables Retain the Largest Application Share in the Metal Food Cans Industry

The fruits and vegetables segment holds 25% of global demand, making it the cornerstone application for metal food cans. The category’s dominance is rooted in the canning process’s unique ability to preserve seasonal produce year-round, safeguarding food security and reducing waste across global supply chains. Tomatoes, corn, beans, peas, and peaches represent the highest-volume products, each relying on either steel or aluminum depending on acidity levels. The enduring consumer trust in canned vegetables and fruits as affordable, nutritious staples ensures stable baseline demand, while growth in developing economies continues to expand consumption. Beyond household consumption, institutional food services—including schools, hospitals, and military supply chains—also sustain volume. The segment is a prime beneficiary of sustainability regulations, as the high recyclability of cans offers governments and brands an environmentally responsible solution for essential food products.

United States: Sustainability and Innovation Driving the Metal Food Cans Market

The United States metal food cans market is shaped by stringent oversight from the Food and Drug Administration (FDA) and the Environmental Protection Agency (EPA), with a strong focus on consumer safety and environmental responsibility. Recent FDA initiatives, such as guidelines on BPA-free linings and foreign object detection, are pushing manufacturers toward safer coatings and advanced inspection technologies. At the same time, lightweighting strategies using thinner-walled aluminum and steel cans are gaining momentum, cutting production costs while minimizing transportation-related emissions. Ball Corporation’s investment in a new aluminum end manufacturing facility in Kentucky further highlights the focus on strengthening domestic supply chains and expanding capacity to meet growing demand.

Applications in ready-to-eat foods and pet food packaging are leading the way, supported by e-commerce growth and the demand for durable, shelf-stable solutions. Sustainability efforts are also central to the U.S. market, with initiatives like the Aerosol Recycling Initiative—spearheaded by the Can Manufacturers Institute (CMI) and Household & Commercial Products Association (HCPA)—setting ambitious targets to raise the national recycling rate to 85%. This combination of regulatory compliance, material innovation, and collaborative sustainability initiatives is positioning the U.S. as a global leader in metal food can advancements.

Germany: Circular Economy and Premium Packaging Fuel Market Growth

Germany’s metal food cans market operates within the strict regulatory environment of the European Union’s Packaging and Packaging Waste Regulation (PPWR), which enforces recyclability targets and promotes high-value material use. These rules are reinforcing the role of metal as a highly recyclable packaging solution compared to plastics. German manufacturers are leading the way in can contouring technologies, enabling asymmetrical and ergonomic shapes that improve brand differentiation while meeting consumer expectations for design and functionality.

With a deposit return system and a robust recycling infrastructure, Germany boasts some of the highest recycling rates in Europe, making it a global model of packaging sustainability. Demand is particularly strong in the premium food category, with canned soups, ready meals, and specialty vegetables driving innovation in both product quality and packaging appeal. The combination of circular economy leadership and a consumer market focused on premium convenience foods ensures Germany’s continued dominance in Europe’s metal food can sector.

China: Automation and Smart Packaging Transforming the Market

China’s metal food cans market is benefiting from strong government support for domestic manufacturing under the “dual-carbon” policy framework, which encourages sustainable and energy-efficient production. Regulatory reforms from the National Medical Products Administration (NMPA) are streamlining approvals for innovative products, accelerating the adoption of internationally competitive packaging solutions.

On the technological front, Chinese manufacturers are investing in automation and digital printing to enable on-demand, customized can production. Companies like ORG are pioneering the use of QR code-enabled smart packaging, applied directly to can surfaces and pull rings, offering traceability and enhanced consumer engagement. Multinational FMCG giants are also expanding production bases in China to shorten supply chains and meet rising domestic demand. Together, these advancements highlight how China is rapidly becoming a global hub for smart, sustainable, and scalable metal food can manufacturing.

India: Government Incentives and Rising Consumer Demand Fuel Expansion

India’s metal food can industry is being propelled by government-backed programs such as Make in India and the Production Linked Incentive (PLI) Scheme, both of which are boosting domestic manufacturing in food processing and packaging. These policies are encouraging investments in new facilities and industrial parks that create a favorable environment for large-scale growth.

On the technological side, the Indian market is increasingly adopting two-piece aluminum cans that combine lightweighting with enhanced safety features. A notable development was Ball Corporation’s collaboration with CavinKare in 2024, introducing retort two-piece aluminum cans for popular milkshake products. With rising disposable incomes and a rapidly growing middle-class population, demand for ready-to-eat meals and convenient food packaging is accelerating. India’s trajectory underscores its position as one of the fastest-growing markets for metal food cans in Asia, driven by both industrial policy support and demographic shifts.

Brazil: Regulatory Shifts and Domestic Investments Strengthen Market Outlook

Brazil’s metal food can market is being shaped by regulatory changes led by Anvisa, particularly the RDC #

429/2020 regulation requiring front-of-pack nutritional warnings. This has influenced can design and labeling, pushing manufacturers to prioritize compliance while enhancing consumer transparency. At the same time, technological innovation is centered on developing cans that withstand Brazil’s varied climate and logistics challenges, with steel cans gaining popularity for their durability and pressure resistance.

Corporate investments are fueling capacity expansion, with Crown Holdings announcing a new beverage can plant in Rio Verde as part of its strategy to scale up in South America. Applications are strongest in the food and beverage sector, where convenience, extended shelf life, and consumer preference for packaged goods are creating sustained demand. Brazil is emerging as a regional growth hub, with both local and global players increasing their footprint to capture opportunities in the expanding market.

Japan: Precision Manufacturing and Premium Cans Define Market Leadership

Japan’s metal food can industry is globally recognized for its expertise in precision manufacturing and advanced packaging technologies. Companies such as Toyo Seikan are at the forefront of producing high-quality tinplate and aluminum cans that meet stringent safety and performance benchmarks. Regulatory oversight from the Pharmaceuticals and Medical Devices Agency (PMDA) is also shaping the industry, with the May 2025 amendments to the Pharmaceuticals and Medical Devices Act strengthening supply stability for packaging in pharmaceutical aerosols—a move that has broader implications for the metal can sector.

The market is seeing increasing demand for high-performance and value-added products, including cans with thinner sidewalls, premium finishes, and consumer-friendly innovations like easy-open ends and peel-off lids. With its emphasis on functionality, quality, and design precision, Japan remains a leading innovator in the global metal food can market, particularly in premium food applications where durability and consumer convenience are critical.

Metal Food Cans Market Report Scope

Metal Food Cans Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$19.5 Billion

|

|

Market Size (2034)

|

$26.3 Billion

|

|

Market Growth Rate

|

3.4%

|

|

Segments

|

By Material (Aluminum, Steel), By Type (2-Piece Cans, 3-Piece Cans), By Application (Fruits & Vegetables, Meat & Seafood, Pet Food, Soups & Sauces, Ready-to-Eat Meals, Others), By End-User (Food & Beverage Companies, Pet Food Manufacturers, Pharmaceutical Companies, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ball Corporation, Crown Holdings, Inc., Trivium Packaging, Ardagh Group S.A., Silgan Holdings Inc., Toyo Seikan Group Holdings, Ltd., Can-Pack S.A., ORG Technology Co., Ltd., Sonoco Products Company, CPMC Holdings Limited, Nampak Ltd., Colep Packaging, DS Containers, Inc., Exal Corporation, Hindustan Tin Works Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metal Food Cans Market Segmentation

By Material

By Type

- 2-Piece Cans

- 3-Piece Cans

By Application

- Fruits & Vegetables

- Meat & Seafood

- Pet Food

- Soups & Sauces

- Ready-to-Eat Meals

- Others

By End-User

- Food & Beverage Companies

- Pet Food Manufacturers

- Pharmaceutical Companies

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Metal Food Cans Market

- Ball Corporation

- Crown Holdings, Inc.

- Trivium Packaging

- Ardagh Group S.A.

- Silgan Holdings Inc.

- Toyo Seikan Group Holdings, Ltd.

- Can-Pack S.A.

- ORG Technology Co., Ltd.

- Sonoco Products Company

- CPMC Holdings Limited

- Nampak Ltd.

- Colep Packaging

- DS Containers, Inc.

- Exal Corporation

- Hindustan Tin Works Ltd.

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and multi-layered methodology to develop insights for the global Metal Food Cans Market, combining both quantitative and qualitative research approaches. The process begins with an extensive collection of primary data from industry stakeholders, including manufacturers, distributors, and regulatory authorities, complemented by secondary research from verified sources such as corporate filings, sustainability reports, industry journals, and government databases. Key market drivers, such as sustainability adoption, BPA-free coating mandates, and innovations in lightweighting, are analyzed alongside macroeconomic and geopolitical factors influencing regional growth, such as reshoring initiatives in the U.S. and Make in India incentives. Advanced analytical models, including CAGR projections, market segmentation analysis, and material-based trend evaluation, are applied to forecast market size, revenue potential, and growth opportunities. USDAnalytics also monitors corporate developments, mergers and acquisitions, and regulatory shifts across leading players—including Ball Corporation, Crown Holdings, Trivium Packaging, and Silgan Holdings—to ensure an up-to-date competitive landscape assessment. Insights are further enriched by regional market evaluations covering the U.S., Europe, China, India, Brazil, and Japan, enabling a comprehensive view of emerging trends, technological adoption, and sustainability-driven innovations. This robust methodology ensures that our market intelligence is precise, actionable, and aligned with the strategic needs of industry professionals seeking to navigate the evolving metal food cans ecosystem.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.