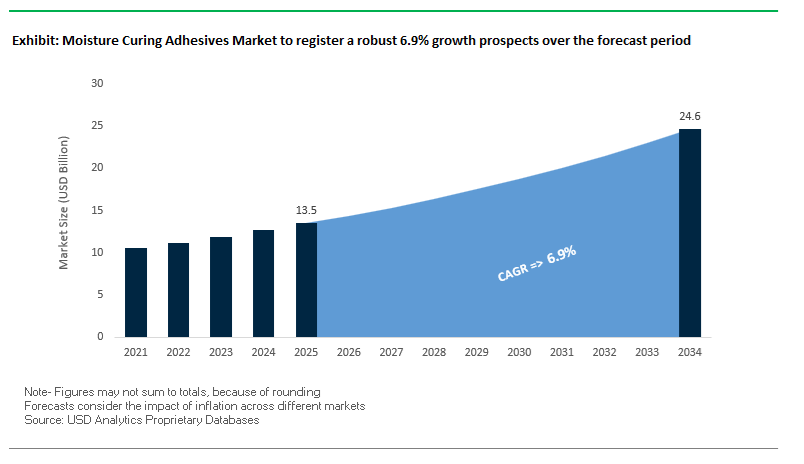

The Global Moisture Curing Adhesives Market is expected to expand from USD 13.5 billion in 2025 to USD 24.6 billion by 2034, advancing at a CAGR of 6.9%, as manufacturers increasingly prioritize ambient-curing reliability, substrate tolerance, and compliance-ready formulations across construction, transportation, electronics, and industrial assembly. Growth is being driven less by incremental chemistry changes and more by the ability of moisture-curing systems to deliver consistent bond performance without ovens, UV exposure, or tightly controlled process environments, making them particularly attractive in large-scale, decentralized, and mixed-material manufacturing.

Polyurethane (PU) adhesives continue to anchor the market due to their combination of high bond strength, elasticity, and long-term durability in moisture-exposed environments. In construction and woodworking, EN 204 D4–certified polyurethane systems are widely specified for exterior applications where joints must retain integrity under repeated wet–dry cycling. Automotive and transportation OEMs are increasingly relying on moisture-curing PU formulations to support lightweighting strategies, particularly for bonding aluminum, coated steels, and fiber-reinforced composites, where mechanical fastening introduces corrosion risk or stress concentration. Suppliers such as Sika, Henkel, and Bostik have expanded moisture-curing PU portfolios to meet these multi-material and durability requirements while aligning with evolving VOC limits.

Silyl-modified polymer (SMP) adhesives are gaining preference in parallel, particularly where low emissions, indoor air quality, and application flexibility influence material selection. Solvent-free, low-VOC SMP formulations are increasingly specified in building interiors, flooring, and panel assembly to meet LEED and A+ indoor air quality standards, while still providing elastic bonding and moisture resistance. Unlike traditional polyurethanes, SMPs avoid isocyanates, which is gaining importance in procurement discussions as occupational exposure rules tighten across Europe and parts of Asia.

Innovation within the market is increasingly defined by hybridization rather than single-chemistry optimization. Manufacturers are developing hybrid curing systems that combine UV-triggered surface fixation with moisture-driven bulk curing, addressing long-standing “shadow cure” limitations in electronics, medical devices, and enclosed assemblies. This convergence between adhesive and sealant technologies is expanding end-use versatility, allowing a single material platform to perform structural bonding, sealing, and vibration damping functions while reducing overall production cycle times.

The global moisture curing adhesives industry has entered a pivotal phase characterized by consolidation, capacity expansion, and sustainability-focused innovation. Major industry leaders are executing acquisitions, launched hybrid formulations, and enhanced production capacities to address the surging demand for construction, EV, and industrial adhesives worldwide.

In May 2025, H.B. Fuller Company completed the acquisition of a specialty adhesives and fastener locking solutions provider, expanding its high-margin Engineering Adhesives business unit. This move reinforced Fuller’s position in cyanoacrylate and UV-curable technologies, strengthening its portfolio for industrial assembly and electronics manufacturing. Earlier in April 2025, Sika AG introduced a new one-component polyurethane sealant line tailored for modular construction, emphasizing fast skin-over time and robust adhesion on varied substrates — a critical advancement for prefabricated building applications.

In February 2025, Dow Inc. finalized a major production facility expansion in Asia-Pacific, targeting silicone-based sealants and adhesives for electronics and skyscraper construction. This regional investment underscores the strong demand in Asia’s infrastructure boom and the growing use of high-performance silicone systems in humid, high-temperature environments. Likewise, Henkel Adhesive Technologies unveiled a low-VOC, isocyanate-free moisture-curing series in December 2024, aligning with the industry’s move toward safer and sustainable production formulations.

Dymax Corporation, in November 2024, introduced a Hybrid Light-Curable (HLC) adhesive combining light and moisture curing mechanisms, specifically designed for medical device manufacturing. Its compliance with biocompatibility standards positions Dymax as a front-runner in medical-grade adhesive innovation. Meanwhile, Wacker Chemie AG confirmed in September 2024 its strategic investment in silane-modified polymer (SMP) technologies, responding to the global transition toward solvent-free and elastic bonding systems in roofing and flooring.

In July 2024, BASF SE advanced safety standards with a new PU prepolymer technology featuring reduced free monomer content, addressing occupational exposure concerns in industrial and automotive environments. Earlier, in May 2024, Master Bond Inc. launched MasterSil 711Med, an RTV silicone adhesive certified under ISO 10993-5 non-cytotoxicity standards, accelerating adoption in medical bonding and gasketing. Rounding out the trend, Arkema Group (Bostik) announced a European capacity expansion in March 2024 for its SMP-based adhesives, supporting the region’s green building movement through enhanced durability and elasticity.

Market Trend 1: Accelerated Reformulation to Eliminate Isocyanates and Reduce VOCs

A global regulatory and environmental shift is driving adhesive manufacturers to reformulate moisture-curing polyurethane and silicone systems toward safer, sustainable, and non-isocyanate polyurethane (NIPU) alternatives. Traditional isocyanate-based formulations, long favored for their strong adhesion and flexibility, are under scrutiny due to their classification as respiratory sensitizers and potential carcinogens under frameworks such as the EU CLP Regulation, US EPA air quality mandates, and Safe Work Australia occupational standards. The has placed pressure on producers to develop isocyanate-free and low-VOC moisture-curing adhesive systems that meet both regulatory compliance and performance expectations.

In cutting-edge R&D, researchers are advancing cyclic carbonate/polyamine-based NIPU chemistries that eliminate isocyanates while maintaining the durability and flexibility required for industrial applications. These next-generation systems, validated in demanding conditions such as military rain erosion testing, have demonstrated the ability to maintain tensile strength and elongation performance essential for high-stress coatings. Although early iterations faced challenges in matching the elongation benchmarks of isocyanate-based systems (e.g., >500% elongation), ongoing refinements are closing the performance gap, signaling a scalable pathway for isocyanate-free structural adhesives.

Leading chemical manufacturers are already commercializing such innovations. For example, a global specialty chemicals company introduced a VeoVa™ silane polymer technology, a non-isocyanate, low-VOC hybrid system that combines the flexibility of polyurethane with the chemical resistance of silicone. These polymers deliver exceptional hardness, pot life, and weathering resistance, outperforming conventional acrylic and epoxy-polysiloxane formulations in industrial coatings and adhesives. As regulatory deadlines tighten globally, the adoption of isocyanate-free, silane-modified polymer (SMP) adhesives is expected to accelerate, marking a pivotal trend in sustainable moisture-curing chemistry.

Market Trend 2: Emergence of Rapid-Cure and High-Humidity Formulations for Manufacturing Efficiency

Manufacturers across automotive, electronics, and industrial assembly sectors are demanding rapid-curing moisture adhesives capable of performing in low-temperature or high-humidity environments, where traditional curing processes struggle. These innovations directly support assembly line throughput, reduce production downtime, and expand the operational range of moisture-curing systems in diverse climatic conditions.

Recent studies on one-component polyurethane (1C-PUR) adhesives report optimized cure kinetics that maintain tensile shear strength even after exposure to low temperatures (0°C–10°C) and water immersion. Such performance characteristics are critical for outdoor assembly operations and high-speed industrial applications where environmental control is limited.

In parallel, leading adhesive producers are commercializing two-part, moisture-activated silicone materials engineered for battery sealing applications in electric vehicles. These advanced systems exhibit controlled viscosity and stable curing, maintaining bond integrity under variable humidity and temperature. Their consistent performance under non-climate-controlled conditions enhances production flexibility, enabling automakers to achieve uniform curing speeds and superior adhesion regardless of environmental fluctuations.

The industry’s focus is shifting toward low-temperature/high-humidity cure formulations that deliver high initial strength, faster fixture times, and minimal shrinkage, marking a new benchmark for manufacturing efficiency and reliability in moisture-curing adhesive technologies.

Market Opportunity 1: Electric Vehicle Battery Pack Sealing and Assembly Applications

The accelerating global transition toward electric mobility represents a major commercial opportunity for moisture-curing adhesives and sealants. EV battery packs require adhesives with high thermal stability, flexibility, and environmental resistance to ensure long-term ingress protection, thermal management, and vibration dampening. Leading manufacturers are responding with one-part silane-modified polymer (SMP) and polyurethane sealants specifically designed for EV battery modules and casings.

These moisture-curing sealants deliver a unique balance of elasticity and structural integrity, ensuring a durable barrier against moisture and corrosion. Their formulation enables thermal cycling resilience, preventing material fatigue and maintaining sealing strength over thousands of charge-discharge cycles.

Additionally, the adoption of dual-cure systems—which combine UV/Visible light curing for rapid surface bonding and moisture curing for complete depth polymerization—addresses complex geometries within EV batteries. The hybrid curing approach ensures complete encapsulation of sensitive components such as Battery Management Systems (BMS) and circuit boards, enhancing electronic protection and reliability.

As EV production volumes surge globally, demand for high-performance, flexible moisture-curing adhesives in battery assembly, module bonding, and potting applications is expected to escalate sharply, making it one of the most promising growth segments within the adhesive industry.

Market Opportunity 2: Growth Potential in Wind and Solar Energy Component Assembly

The worldwide expansion of renewable energy infrastructure—particularly wind and solar power—is creating sustained demand for durable, high-performance moisture-curing adhesives. These adhesives are vital in ensuring the structural integrity, weather resistance, and service life of renewable energy systems deployed in harsh environments.

In solar photovoltaic (PV) applications, high-quality silicone-based moisture-curing sealants are essential for module encapsulation, frame sealing, and junction box assembly. The use of these advanced sealants significantly enhances UV stability, ozone resistance, and temperature tolerance, contributing to the 25–30-year lifespan of modern solar panels. As the solar industry continues to scale under global decarbonization initiatives, reliable sealants with long-term weatherproofing and thermal cycling resilience are becoming indispensable.

Similarly, the wind energy sector—particularly offshore installations—relies on neutral-curing, medium-modulus silicone sealants for foundation sealing, blade assembly, and nacelle housing protection. These formulations exhibit high adhesion strength and flexibility, capable of withstanding extreme weather, vibration, and saltwater exposure. Moisture-curing sealants also play a key role in load-bearing grouting and structural reinforcement, enhancing the operational durability of wind turbines in coastal and high-wind regions.

With massive investments in renewable infrastructure and grid modernization, moisture-curing adhesives and sealants are set to become integral materials in sustainable energy construction and maintenance, offering exceptional long-term performance in UV-exposed, humid, and corrosive environments.

Moisture Curing Adhesives Market Share Insights, 2025-2034

Market Share by Product Type

The one-component (1K) adhesive segment dominates the global moisture curing adhesives market, commanding a projected 72.3% share in 2025, due to its ease of use, zero mixing requirement, and ambient moisture-activated curing process. These adhesives are widely favored in construction, woodworking, and industrial assembly applications, where simplicity, reliability, and long-term performance are essential. Their single-package convenience significantly reduces waste and setup time, making them ideal for on-site applications such as flooring, roofing membranes, façade systems, and joint sealing. Furthermore, their excellent adhesion to porous and non-porous substrates, combined with high flexibility and weather resistance, makes them indispensable in outdoor structural and façade bonding. Environmental regulations have also accelerated the adoption of 1K formulations, as they are solvent-free, low-VOC, and compliant with green building certifications. The increasing global demand for sustainable, energy-efficient construction materials continues to fuel the dominance of this segment, positioning 1K systems as a cornerstone technology for modern architectural and infrastructure development.

On the other hand, the two-component (2K) adhesive segment retains a strategic niche, primarily for applications requiring rapid curing, thicker bond lines, or controlled polymerization in low-humidity conditions. These systems are crucial in automotive assembly, composite manufacturing, and industrial bonding, where high mechanical performance and reduced cycle times are critical. The 2K segment’s value share is significant due to its specialized formulations tailored for demanding environments such as electric vehicle battery packs, industrial laminates, and aerospace structures. The coexistence of both systems—1K for convenience and 2K for performance—reflects the industry’s dual focus on user efficiency and engineering excellence, ensuring moisture curing adhesives remain versatile across multiple manufacturing and construction domains.

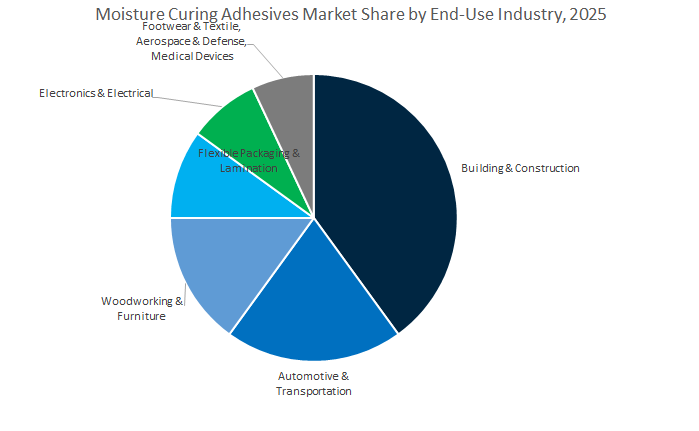

Market Share by End-Use Industry

The building and construction segment leads the global moisture curing adhesives market, with a projected 43.6% share in 2025, reflecting its critical role in infrastructure development, architectural finishing, and structural sealing applications. These adhesives are extensively used in flooring, roofing, panel bonding, cladding, and window installation, where their excellent weatherability, water resistance, and mechanical flexibility are indispensable. The growing shift toward green building materials and VOC-free bonding technologies has propelled the use of polyurethane- and silane-modified polymer-based moisture-curing adhesives, which deliver strong adhesion on diverse substrates like concrete, glass, metal, and composites. Rapid urbanization in Asia-Pacific and Middle Eastern economies, coupled with massive residential and commercial construction projects, continues to boost market demand. Additionally, renovation and retrofitting activities in developed regions sustain steady consumption of moisture-curing sealants and adhesives in waterproofing, insulation, and joint sealing applications.

The automotive and transportation segment demonstrates strong growth, fueled by rising EV adoption, lightweight material integration, and modular vehicle assembly trends. Moisture-curing adhesives are increasingly used for glass bonding, interior components, and body sealing, offering superior flexibility, vibration damping, and long-term durability under dynamic conditions. Woodworking and furniture applications maintain steady demand, particularly in edge banding, veneer lamination, and panel bonding, benefiting from 1K polyurethane systems that provide moisture resistance and strong adhesion to wood substrates. Meanwhile, flexible packaging, electronics, and electrical applications are expanding as manufacturers leverage moisture-curing systems for lamination, potting, and protective encapsulation. Smaller but specialized sectors such as footwear, aerospace, and medical devices rely on moisture-curing formulations for niche bonding tasks where elasticity and chemical resistance are key.

The Moisture Curing Adhesives Market is moderately consolidated, with global leaders such as Henkel, 3M, Sika AG, H.B. Fuller, Dow Inc., and Wacker Chemie AG commanding strong technological and regional positions. These companies are redefining the market through portfolio diversification, regional investments, and hybrid technology innovation, focusing on compliance, performance, and sustainability.

Henkel, through its Loctite brand, leads the global market for polyurethane and silicone moisture-curing adhesives. The company is pioneering the development of isocyanate-free PU prepolymers, aligning with evolving European chemical safety regulations. In 2024, Henkel launched electrically conductive moisture-cure adhesives for compact camera modules, expanding its reach into high-precision electronics. Its vertically integrated approach — combining adhesives with automated dispensing equipment — ensures superior consistency and performance for automotive and industrial applications.

3M leverages its deep material science expertise to produce Scotch-Weld and specialty moisture-curing polyurethane adhesives for extreme-condition environments. The company focuses on lightweighting and vibration-damping solutions in aerospace and heavy transportation, offering unmatched adhesion to low-surface-energy substrates. To stay ahead of regulatory trends, 3M continues to integrate non-VOC and UV-curable variants within its moisture-curing product lines, aligning with global sustainability goals.

Sika AG remains a dominant force through its Sikaflex polyurethane and SMP-based sealants, renowned for structural glazing, façade bonding, and elastic joint sealing. With a strategic presence in emerging markets, Sika tailors product formulations to meet localized climate demands and building codes. Its recent innovation in fast-curing SMP adhesives for roofing and flooring systems enhances weather resistance and efficiency in high-performance construction. Continuous investments in regional R&D centers further support its long-term leadership in green infrastructure bonding solutions.

H.B. Fuller focuses on engineering-grade moisture-curing adhesives, serving sectors like automotive, aerospace, and woodworking. Following its May 2025 acquisition of a specialty adhesives manufacturer, the company has significantly expanded its high-performance portfolio. Its emphasis on single-component, high-speed curing systems provides a cost-effective solution for high-volume assembly. Fuller’s D4-standard polyurethane adhesives continue to be the preferred choice in woodworking and millwork applications requiring long-term water resistance.

Dow Inc. integrates deep chemical expertise with End-Use Industry design, supplying polyols, isocyanates, and formulated adhesives through its Industrial and Consumer Solutions divisions. Its latest bio-based polyol technology enables more sustainable polyurethane systems for the green building and automotive sectors. Dow’s high-modulus window bonding adhesives are widely used to enhance vehicle rigidity and safety, while its global infrastructure projects benefit from cost-effective, moisture-curing sealant technologies that improve structural integrity and lifespan.

Wacker Chemie AG is globally recognized for its silicone and silyl-terminated polymer (STP/SMP) moisture-curing systems. The company’s advanced formulations exhibit high elasticity, UV stability, and non-foaming performance, making them ideal for architectural and sealing applications. Wacker’s commitment to low-emission, solvent-free systems ensures compliance with the world’s most stringent environmental and worker safety standards. Its hybrid adhesive technologies seamlessly blend silicone flexibility with polyurethane strength, reinforcing Wacker’s leadership in premium construction bonding solutions.

Country Analysis: Global Moisture Curing Adhesives Industry

United States: Low-VOC Innovation and Automotive Lightweighting Drive Market Expansion

The United States moisture-curing adhesives industry is advancing rapidly under stringent environmental regulations and an accelerating shift toward lightweight vehicle manufacturing. The U.S. Environmental Protection Agency (EPA) and multiple state-level agencies such as the California Air Resources Board (CARB) have implemented tightened VOC emission limits on construction sealants and adhesives, compelling the industry to transition toward low-isocyanate, solvent-free 1K polyurethane (PU) and silane-modified polymer (SMP) technologies. The regulatory pressure has catalyzed innovation among major domestic manufacturers, leading to the emergence of dual-cure PU adhesives—a hybrid formulation combining moisture and UV curing mechanisms.

The new-generation adhesives are particularly gaining traction across automotive and electronics manufacturing clusters in the Midwest and West Coast, where high-speed robotic assembly lines dominate production. The EV (Electric Vehicle) sector represents a critical growth frontier, as structural moisture-curing adhesives are increasingly used for battery enclosure sealing, crash-durable bonding, and body-in-white assembly. Major OEMs and Tier 1 suppliers are integrating The formulations to reduce weld points, improve durability, and meet lightweighting targets essential for enhanced vehicle performance and sustainability.

Germany: Bio-Based Adhesive Chemistry and Green Building Certifications Reinforce Market Leadership

Germany’s moisture-curing adhesives market remains a cornerstone of European innovation, propelled by bio-based polyurethane development and stringent environmental compliance. Leading German chemical giants have launched renewable polyol-based PU adhesive systems engineered for carbon-neutral construction and furniture manufacturing, directly supporting the European Union’s Green Deal and REACH compliance framework. The bio-based solutions are gaining traction among construction material suppliers striving for DGNB-certified green buildings, which demand adhesives with low monomer content and superior weatherability.

Industrial investment is also directed toward high-solids, reactive hot-melt polyurethane (HMPUR) systems, which are rapidly becoming the standard for wood lamination, flexible film packaging, and high-speed industrial assembly. The aligns with the country’s strong commitment to circular economy principles and reduced carbon emissions in manufacturing. With active participation in Horizon Europe’s sustainable materials cluster, Germany is spearheading research in eco-compliant moisture-curing sealants that combine long-term flexibility, recyclability, and high mechanical strength—ensuring the country’s continued leadership in advanced adhesive engineering across construction and industrial sectors.

China: Infrastructure Growth and Electronics Manufacturing Fuel Adhesive Demand

China’s moisture-curing adhesives industry is expanding at an accelerated pace, underpinned by large-scale infrastructure investment and industrial modernization initiatives. Both domestic and international adhesive producers are investing in R&D and local production hubs in Shanghai, Guangdong, and Jiangsu, enabling faster supply of advanced polyurethane and SMP formulations to serve the booming construction and new energy vehicle (NEV) markets. The dual demand from infrastructure and electronics is driving adoption of flexible, durable, and thermally stable adhesives used for structural bonding, panel sealing, and encapsulation.

China’s dominance in electronics manufacturing—spanning smartphones, LED displays, and PCB assembly—is spurring the need for moisture-curing encapsulants with superior heat, humidity, and chemical resistance. Moreover, with the country’s vast tropical and subtropical zones, adhesive R&D centers are prioritizing heat- and moisture-resistant 1K PU adhesives suitable for long-term performance under high humidity. The government’s infrastructure pipeline and green industrial policies further ensure a stable demand for low-VOC, solvent-free moisture-curing systems, positioning China as a high-volume, innovation-driven production hub for moisture-curing adhesives globally.

India: Infrastructure Expansion and Automotive Localization Stimulate Market Growth

India’s moisture-curing adhesives market is being reshaped by large-scale infrastructure projects and the localization of automotive production under government-backed programs. The National Infrastructure Pipeline (NIP) and the Production Linked Incentive (PLI) Scheme for Auto and Components—worth ₹25,938 crore—are catalyzing investment in structural bonding solutions for railways, commercial vehicles, and smart city developments. The national focus on modern construction and advanced manufacturing is fueling demand for high-strength, moisture-curing polyurethane adhesives capable of withstanding temperature and humidity variations.

Domestic adhesive producers are increasingly forming joint ventures with global leaders to enhance local production of Polyurethane Reactive (PUR) hot-melt adhesives, serving key sectors such as furniture, footwear, and textiles. Concurrently, metro-area construction authorities are enforcing low-VOC and solvent-free adhesive adoption to improve indoor air quality (IAQ), aligning with India’s National Clean Air Programme. The combination of policy support, infrastructure investment, and growing manufacturing capacity is positioning India as one of the fastest-growing regional markets for moisture-curing adhesives in Asia-Pacific.

Japan: Precision Manufacturing and Advanced Material Bonding

Japan’s moisture-curing adhesives industry is renowned for precision, reliability, and high-performance chemistry integration. The country’s adhesive manufacturers are global pioneers in non-acidic cyanoacrylate and SMP polymer development, offering ultra-clean, high-purity bonding agents tailored for sensitive electronic component assembly and thin-film encapsulation. The market’s high R&D intensity is driven by demand from semiconductor, display, and medical device sectors, where biocompatibility, low outgassing, and sterilization resistance are critical.

Additionally, Japanese R&D programs are investing heavily in self-healing moisture-curing polymer technologies aimed at extending the operational lifespan of products in aerospace, automotive, and high-speed rail. The polymers exhibit the ability to autonomously repair micro-cracks, reducing maintenance and improving material longevity. As Japan continues to advance precision electronics and smart device manufacturing, demand for high-purity silicone and moisture-curing adhesives will remain integral to sustaining the country’s position as a global leader in high-value material bonding technologies.

South Korea: EV Battery and Display Industry Catalyze High-Tech Adhesive Development

South Korea’s moisture-curing adhesives market is anchored in two core sectors: electric vehicle (EV) battery systems and flexible OLED display manufacturing. Domestic conglomerates such as LG Chem and Hanwha Solutions are investing heavily in R&D for moisture-curing thermal management adhesives to enhance battery safety, fire resistance, and thermal conductivity. The products are increasingly critical for battery pack assembly and gap filling in high-performance EVs, where weight reduction and temperature stability are key design priorities.

Simultaneously, South Korea’s leadership in consumer electronics is fueling large-scale consumption of 1K PU and silicone-based moisture-curing adhesives used for thin-layer lamination, flexible screen sealing, and optical bonding. The country’s robust shipbuilding and marine engineering sectors further contribute to demand for high water-resistant polyurethane structural adhesives. With national initiatives promoting green manufacturing and high-tech innovation, South Korea is emerging as a regional epicenter for advanced moisture-curing adhesive solutions catering to both heavy industry and precision electronics manufacturing.

Moisture Curing Adhesives Market Report Scope

Moisture Curing Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.5 Billion

|

|

Market Size (2034)

|

$24.6 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Product Type (Polyurethane, Silicone, Cyanoacrylate, Polyolefin, Hybrid, Others), By Application (Construction, Automotive, Woodworking/Wood Bonding, Electronics, Aerospace, Marine, Textile, Others), By Substrate (Metal, Plastics, Glass, Wood, Composite Materials,, Others), By Technology (Reactive Hot Melt, Solvent-Based, Water-Based

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, H.B. Fuller Company, Dow Inc, Bostik, BASF SE, Dymax Corporation, Jowat SE, Illbruck, Momentive Performance Materials Inc, Illinois Tool Works Inc. (ITW)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type / Chemistry

- Polyurethane

- Silicone

- Cyanoacrylate

- Polyolefin

- Hybrid

- Others

By Application

- Construction

- Automotive

- Woodworking/Wood Bonding

- Electronics

- Aerospace

- Marine

- Textile

- Others

By Substrate

- Metal

- Plastics

- Glass

- Wood

- Composite Materials,

- Others

By Formulation / Technology

- Reactive Hot Melt

- Solvent-Based

- Water-Based

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Moisture Curing Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- H.B. Fuller Company

- Dow Inc

- Bostik

- BASF SE

- Dymax Corporation

- Jowat SE

- Illbruck

- Momentive Performance Materials Inc

- Illinois Tool Works Inc. (ITW)

*- List not Exhaustive

Research Coverage

This report investigates the Moisture Curing Adhesives Market, delivering analysis reviews on demand catalysts such as polyurethane (PU) leadership, SMP hybrid innovation, low-VOC reformulation, and dual-cure (light + moisture) adoption across construction, automotive/EV, electronics, woodworking, and industrial assembly; it highlights technology breakthroughs in isocyanate-free chemistries, rapid-cure/high-humidity performance, and durability gains that extend service life in harsh environments; with comparative benchmarking of cure kinetics, elasticity, and long-term weatherability, competitive strategy mapping, regulatory-readiness assessment, and investment signals, USDAnalytics structures decision-grade insights for product managers, sourcing leads, and operations executives; this report is an essential resource for professionals seeking defensible forecasts, route-to-market clarity, and risk/opportunity framing in a rapidly evolving adhesives landscape.

Scope Highlights

Segmentation:

- By Product Type / Chemistry: Polyurethane; Silicone; Cyanoacrylate; Polyolefin; Hybrid; Others.

- By Application: Construction; Automotive; Woodworking/Wood Bonding; Electronics; Aerospace; Marine; Textile; Others.

- By Substrate: Metal; Plastics; Glass; Wood; Composite Materials; Others.

- By Formulation / Technology: Reactive Hot Melt; Solvent-Based; Water-Based.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecasts 2025–2034 with annual updates.

Companies: Analysis/profiles of 15+ companies including strategies, portfolios, and recent developments.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.