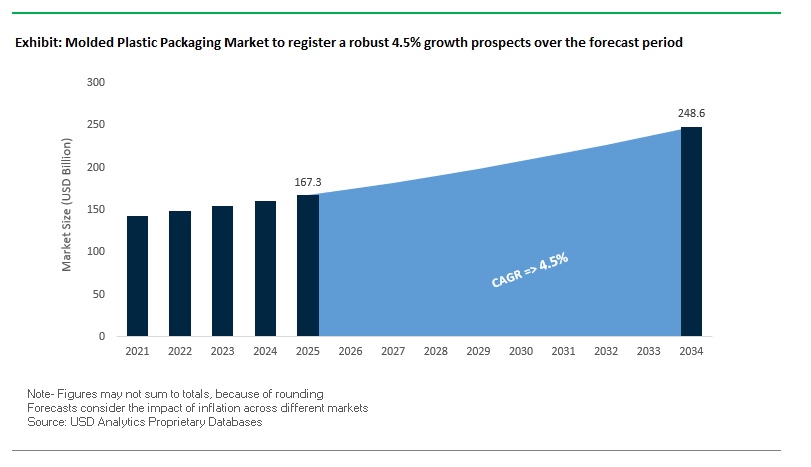

Molded Plastic Packaging Market to Reach $248.6 Billion by 2034 at 4.5% CAGR

The global molded plastic packaging market is projected to grow from $167.3 billion in 2025 to $248.6 billion by 2034, reflecting a CAGR of 4.5%. Growth is driven by e-commerce expansion, automation, AI integration, and sustainability initiatives, positioning molded plastic packaging as a critical solution for protective, lightweight, and durable product delivery. Its wide applicability across food and beverage, pharmaceuticals, personal care, and industrial goods ensures consistent demand, while advances in injection molding and recycled polymer usage reinforce its market dominance.

Key Insights for Industry Stakeholders

- Injection molding dominance: Automated processes reduce production costs, enhance efficiency, and minimize material waste.

- E-commerce impact: Growth in last-mile delivery has increased demand for molded packaging that protects products through multiple handling stages.

- Sustainable materials: Companies are adopting recycled polymers and closed-loop systems to reduce environmental impact and promote circular economy practices.

- AI and automation: AI-driven quality control and robotic automation improve production consistency, reduce downtime, and enhance productivity.

- Cross-industry application: Molded plastic packaging is widely used across automotive, electronics, food & beverage, and healthcare sectors, highlighting its versatility.

Market Analysis: Recent Industry Developments Driving Growth in Molded Plastic Packaging

The molded plastic packaging industry has experienced a series of strategic acquisitions, technological innovations, and infrastructure expansions that reinforce its global growth trajectory. In August 2025, Inteplast Group acquired Con-pearl and Perga in Germany, signaling a strategic expansion into European plastics and packaging markets. The same month, ProAmpac announced its acquisition of PAC Worldwide, creating a vertically integrated packaging solution provider capable of serving e-commerce, consumer goods, and industrial markets.

Regional growth is also significant. A July 2025 study highlighted the Asia-Pacific metallized film sector as a growth hotspot due to expanding food, beverage, and pharmaceutical manufacturing. Concurrently, the merger of WestRock and Smurfit Kappa in July 2025 formed Smurfit WestRock, strengthening its ability to serve the molded plastic packaging market with enhanced product offerings.

Investments in production capacity and sustainability have accelerated. In April 2025, C&J Industries expanded its facility by 25,000 square feet, including a 12,000-square-foot molding cleanroom. February 2025 saw PSI Molded Plastics invest $5 million in its Marion, South Carolina facility to increase production capabilities. Meanwhile, January 2025 featured Cirkla’s launch of molded fiber MAP trays, reducing plastic usage by 85% and showcasing the industry’s shift toward eco-friendly alternatives. Notably, Sonoco Products Company acquired Eviosys in November 2024, expanding its global packaging capabilities across consumer and industrial segments.

Trends and Opportunities Shaping the Molded Plastic Packaging Market

Accelerated Reshoring and Strategic Capacity Expansion in North America

The molded plastic packaging market is experiencing a strong trend toward reshoring production and expanding regional capacity, particularly in North America. Geopolitical risks, shipping disruptions, and rising overseas labor costs have heightened the importance of domestic manufacturing for essential packaging in medical, pharmaceutical, and high-value consumer goods.

Government backing is reinforcing this transition. In January 2022, the U.S. Department of Energy (DOE) allocated $13.4 million to projects targeting plastic waste reduction and next-generation resin development, indirectly supporting molded packaging resilience. While not specific to molded packaging, such investments strengthen the broader plastics ecosystem, including recycling infrastructure.

Corporate reshoring initiatives are equally notable. Several firms have announced expansions of regional molding facilities in North America to reduce lead times and ensure uninterrupted supply. The urgency for medical and pharmaceutical packaging security became evident during COVID-19, when shortages of molded vials, trays, and closures disrupted healthcare delivery. This has made localized molded packaging production a national priority, tying directly into supply chain resilience and food and drug security policies.

Mandated Adoption of Post-Consumer Recycled (PCR) Content

The second major trend is the mandated integration of post-consumer recycled (PCR) resins into molded plastic packaging. Regulatory frameworks and corporate sustainability goals are pushing the industry toward higher recycled content while maintaining product safety and performance.

The European Union’s PPWR (Packaging and Packaging Waste Regulation), effective from February 2025, requires 30% PCR content in PET contact-sensitive packaging and 35% in other plastics by 2030, with stricter thresholds planned for 2040. These rules are shaping packaging design choices, driving demand for high-quality PCR streams, and incentivizing closed-loop recycling systems.

Companies are already responding. In May 2025, a brand introduced a refillable packaging system in North America with PCR integrated into molded components. Another major player reported in its 2024 sustainability update that it is on track to reach 50% recycled content in packaging by 2030. This alignment between regulatory mandates and corporate pledges is transforming PCR adoption from a voluntary initiative to a structural industry standard.

Development of Advanced Mono-Material and Polymer-Blend Thermoformed Trays

A significant opportunity lies in replacing traditionally non-recyclable PET/PE laminated trays with mono-material or polymer-blend thermoformed alternatives. Advances in materials science are making it possible to achieve high barrier, clarity, and sealing performance using primarily one resin, ensuring compatibility with recycling systems.

Industry collaborations have already delivered prototypes. For example, a joint project between a raw material supplier and a packaging machine manufacturer created a 95% polyethylene (PE) thermoformed packaging structure that maintained barrier properties comparable to PA-based laminates. These innovations are not only technically feasible but also regulatory-driven. Under the PPWR recyclability grading system, by 2030 packaging must achieve a recyclability rate of at least 70% to qualify as “designed for recycling.

The move toward mono-material trays positions suppliers to meet recyclability benchmarks, avoid penalties, and future-proof their portfolios against non-compliance bans. This makes advanced polymer trays a key growth opportunity.

Integration of In-Mold Labeling (IML) with Digital Printing for Hyper-Personalization

The rising demand for personalized and limited-edition packaging creates a compelling opportunity through the integration of in-mold labeling (IML) with digital printing. This hybrid approach embeds high-resolution, variable graphics directly into molded packaging, eliminating secondary labeling while enabling mass customization at scale.

IML with digital printing offers operational benefits as well. A technical report notes that fusing labels into the mold streamlines the production process, reduces labor requirements, and eliminates post-mold labeling errors. From a marketing perspective, digital printing’s on-demand flexibility enables brands to deploy unique graphics, serializations, or personalized messages without costly tooling.

This combination of efficiency and marketing agility is particularly attractive for consumer electronics, cosmetics, and promotional packaging, where branding differentiation and consumer engagement are critical. By merging digital printing innovation with molded packaging, manufacturers can deliver both cost savings and value-added customization, cementing a competitive edge.

Competitive Landscape of Global Molded Plastic Packaging Market

The molded plastic packaging industry is highly competitive, dominated by companies leveraging technological innovation, sustainability initiatives, and global production networks. Leading firms differentiate themselves through advanced injection molding, integrated service offerings, and adoption of recycled materials, ensuring operational efficiency and environmental responsibility.

Amcor plc: Leading Global Innovator in Molded Plastic Packaging

Amcor is a global packaging leader, offering a comprehensive portfolio of molded plastic packaging solutions across food, beverage, pharmaceutical, medical, and personal care sectors. Following its merger with Berry Global, Amcor is redefining its core portfolio to solidify leadership in consumer and healthcare packaging. Its global footprint, emphasis on lightweighting, sustainable materials, and innovation, and services from design to logistics enable clients to optimize product launches and sustainability objectives.

Berry Global Inc.: Advancing Sustainable and High-Performance Packaging

Berry Global manufactures rigid containers, films, and trays for molded plastic applications. In August 2025, Berry completed its merger with Amcor plc, creating a global leader in consumer and healthcare packaging solutions. The company focuses on sustainable, recyclable, and high-performance products, investing in technologies that reduce environmental impact while meeting the demands of food, medical, and pharmaceutical sectors.

Sealed Air Corporation: Expert in Protective and Food Packaging Solutions

Sealed Air provides molded plastic solutions within its flexible packaging portfolio, designed to extend shelf life and reduce food waste. The company leverages materials science expertise to improve global food supply chain efficiency. Offering design, engineering, and technical support, Sealed Air helps customers optimize packaging, meet sustainability targets, and maintain a competitive advantage in global markets.

Sonoco Products Company: Expanding Global Packaging Capabilities

Sonoco specializes in paperboard, molded fiber, and plastic packaging products, essential in molded plastic packaging applications. Its November 2024 acquisition of Eviosys expanded its metal food can and aerosol packaging capabilities, strengthening its global presence. Sonoco emphasizes lightweight, durable, and recyclable solutions, serving diverse industries with innovative and sustainable packaging options.

WestRock Company (Smurfit WestRock): Providing Premium and Sustainable Packaging Solutions

WestRock, now Smurfit WestRock, offers a wide range of folding cartons and corrugated containers suitable for molded plastic packaging applications. The July 2025 merger with Smurfit Kappa created a global packaging leader, enhancing its portfolio and sustainability initiatives. Smurfit WestRock focuses on recycled and renewable materials, offering premium-quality solutions for shipping, logistics, and consumer packaging needs.

Molded Plastic Packaging Market Share Insights

Injection Molding Dominates Market Share by Technology in the Molded Plastic Packaging Industry

Injection molding secures the leading 35% market share in 2025, making it the cornerstone technology for molded plastic packaging. Its dominance stems from unmatched precision, consistency, and scalability, enabling the production of thin-walled containers, closures, and high-volume rigid tubs with uniform wall thickness. The technology’s compatibility with recycled resins such as rPET and rPP further strengthens its position as sustainability mandates reshape the industry. While blow molding follows closely with 30% share for hollow containers like bottles, and thermoforming captures 20% for trays and blisters, injection molding remains the most cost-efficient and versatile choice for packaging manufacturers targeting both mass-market and premium applications. Extrusion and niche methods such as rotational and foam molding play important but secondary roles, often serving as enabling technologies in upstream or specialized markets.

Food & Beverage Leads Market Share by End-User in the Molded Plastic Packaging Industry

The food & beverage sector dominates with 50% share, reflecting the indispensable role of molded plastic packaging in preserving freshness, ensuring safety, and enabling convenience. From beverage bottles and dairy tubs to ready-meal trays and fresh produce packaging, this segment consumes over half of global output. The ongoing shift to recycled content and mono-material packaging further reinforces molded plastic’s importance, as brands face growing regulatory and consumer pressure for sustainable solutions. Personal and household care, with 25% share, relies on molded plastics for bottles, tubes, and jars, while pharmaceuticals hold 15% share due to high-value requirements in drug safety and compliance. Industrial packaging accounts for 10%, emphasizing heavy-duty and reusable formats, but food & beverage remains the most volume-intensive and strategically critical end-user segment driving technological and material innovations.

United States: Smart Manufacturing and Circular Economy Initiatives Driving Molded Plastic Packaging

The United States molded plastic packaging market is being reshaped by state-level Extended Producer Responsibility (EPR) laws and initiatives such as the U.S. Plastics Pact, which aims to recycle or compost 50% of plastic packaging and achieve 30% recycled content by 2025. These regulatory measures are accelerating the adoption of recyclable and bio-based plastics, encouraging manufacturers to innovate sustainable packaging solutions.

Technological advancements are revolutionizing production, with AI-powered vision systems detecting defects at high speeds and IoT sensors enabling predictive maintenance on molding lines. Companies are actively investing to capture growth opportunities; for instance, Berry Global Inc. introduced an advanced micro tray packaging solution using bio-based polyethylene for food applications, while TransPak inaugurated a new 300,000-square-foot campus specializing in packaging for semiconductors. Key applications are concentrated in food and beverage packaging, including bottles, jars, and trays, along with pharmaceuticals and healthcare sectors requiring tamper-evident and sterile molded packaging solutions.

Germany: PPWR Compliance and Advanced Fiber-Based Molding Technologies Fuel Growth

Germany’s molded plastic packaging market is strongly influenced by the European Union’s Packaging and Packaging Waste Regulation (PPWR) 2025, which prioritizes recyclability and incorporation of recycled content. This framework compels manufacturers to adopt circular economy models, producing packaging that is sustainable, recyclable, and cost-effective.

Technological innovation is a key differentiator, with companies like BIO-LUTIONS pioneering dry molding technology to produce fiber-based, fully recyclable packaging as an alternative to single-use plastics. The country also maintains a robust R&D ecosystem, with 75 research institutes collaborating with industry to drive innovation across the plastics value chain. Borealis’ €100 million investment to expand its recyclable, foam-based polypropylene production highlights the push for lightweight yet durable materials suitable for automotive, consumer goods, and construction applications.

China: Government Support and Automation Drive High-Performance Molded Plastics

China’s molded plastic packaging market is expanding under supportive government initiatives targeting high-end manufacturing and policies such as the “Opinions on Further Strengthening the Control of Plastic Pollution”. These regulations promote innovative, lightweight, and sustainable plastics, aligning with the country’s environmental goals and dual-carbon strategy.

Technological advancements in automation and AI enhance production efficiency and quality control, ensuring high-precision molded parts. China’s booming automotive, electronics, and construction sectors are driving demand for lightweight molded plastics for vehicle components, sound insulation, and structural applications. Analysts forecast strong growth in the plastic extrusion molded parts market, fueled by the increasing demand for high-quality packaging solutions and lightweight materials.

India: Make in India and PLI Schemes Boost Sustainable Packaging Adoption

India’s molded plastic packaging market is being propelled by the Make in India initiative and the Production Linked Incentive (PLI) scheme, which encourage local manufacturing and investment in advanced packaging technologies. The country’s commitment to a circular economy is further reinforced by updates to the Plastics Waste Management Rules 2024, which broaden the definitions of manufacturers, producers, and importers while promoting recyclable and biodegradable plastics.

The market is seeing widespread adoption of advanced packaging solutions equipped with barcodes or QR codes for product traceability, as enabled by the 2025 amendment to the Plastic Waste Management Rules. Corporate investments are increasing, strengthening production capabilities and R&D. Molded plastics are finding applications in electronics packaging, food and beverage containers, and healthcare products, reflecting the country’s growing focus on sustainable, high-performance packaging.

Japan: Innovative Biodegradable Plastics and Recycled Material Programs Lead the Market

Japan’s regulatory environment is driving innovation with new rules for food containers and packaging effective June 2025, establishing a “positive list” for allowable synthetic materials. Japanese scientists have developed plastics that dissolve in seawater within hours, offering an eco-friendly solution to reduce oceanic plastic pollution.

The government is actively promoting recycled plastics for automotive applications, evidenced by the Industry-Government-Academia Consortium launched in 2024. Japanese manufacturers leverage microcellular and molded plastics for vehicle interiors and exteriors, including dashboards and bumpers, while prioritizing lightweighting strategies to improve fuel efficiency and comply with environmental regulations.

Brazil: Biodegradable Alternatives and National Solid Waste Policy Drive Market Expansion

Brazil’s molded plastic packaging market is influenced by Law No. 15,088 (2025), amending the National Solid Waste Policy to restrict imports of solid waste, including plastics, encouraging sustainable domestic production. The government is promoting biodegradable packaging alternatives as part of a shared responsibility model across manufacturers, importers, distributors, consumers, and waste management services.

Technological innovation in molded pulp packaging is gaining traction, offering enhanced durability, printability, and design versatility. Adoption is strongest in foodservice and consumer products, where renewable and compostable packaging is increasingly valued. This trend underscores Brazil’s growing market focus on eco-friendly molded packaging solutions that meet sustainability goals and regulatory requirements.

Molded Plastic Packaging Market Report Scope

Molded Plastic Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$167.3 Billion

|

|

Market Size (2034)

|

$248.6 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Material (PE, PET, PP, PS, EPS, PVC, Bio-based Plastics, Others), By Technology (Injection Molding, Extrusion, Blow Molding, Thermoforming, Others), By Application (Bottles & Jars, Cans, Trays & Containers, Caps & Closures, Others), By End-User (Food & Beverage, Industrial Packaging, Pharmaceuticals, Personal & Household Care)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Inc., Dow Inc., LyondellBasell Industries N.V., International Paper Company, WestRock Company, Sealed Air Corporation, Mondi Group, DS Smith, Sonoco Products Company, Graphic Packaging Holding Company, Huhtamaki Oyj, Avery Dennison Corporation, Crown Holdings, Inc., BASF SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Molded Plastic Packaging Market Segmentation

By Material

- PE

- PET

- PP

- PS

- EPS

- PVC

- Bio-based Plastics

- Others

By Technology

- Injection Molding

- Extrusion

- Blow Molding

- Thermoforming

- Others

By Application

- Bottles & Jars

- Cans

- Trays & Containers

- Caps & Closures

- Others

By End-User

- Food & Beverage

- Industrial Packaging

- Pharmaceuticals

- Personal & Household Care

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Molded Plastic Packaging Market

- Amcor plc

- Berry Global Inc.

- Dow Inc.

- LyondellBasell Industries N.V.

- International Paper Company

- WestRock Company

- Sealed Air Corporation

- Mondi Group

- DS Smith

- Sonoco Products Company

- Graphic Packaging Holding Company

- Huhtamaki Oyj

- Avery Dennison Corporation

- Crown Holdings, Inc.

- BASF SE

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and integrated research methodology to deliver precise insights into the global Molded Plastic Packaging market. Our approach combines extensive primary research, including interviews with packaging engineers, supply chain experts, sustainability officers, and industry stakeholders, with secondary research from corporate filings, regulatory documents, scientific publications, and trade reports. We analyze technological trends such as injection molding, thermoforming, blow molding, and AI-driven automation, alongside material innovations including recycled polymers, bio-based plastics, and mono-material trays. Quantitative forecasting incorporates historical market data, CAGR projections, regional growth drivers, and application-specific demand across food & beverage, pharmaceuticals, personal care, and industrial sectors. Competitive intelligence evaluates mergers, acquisitions, production expansions, and sustainability initiatives of leading players such as Amcor, Berry Global, Sealed Air, Sonoco, and Smurfit WestRock, with an emphasis on operational efficiency, recyclability, and product customization. This comprehensive methodology ensures USDAnalytics provides actionable, data-driven insights that empower industry professionals to optimize production, meet sustainability mandates, and capitalize on emerging opportunities in the rapidly evolving molded plastic packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.