Mono Cartons Market Overview: Growth Outlook

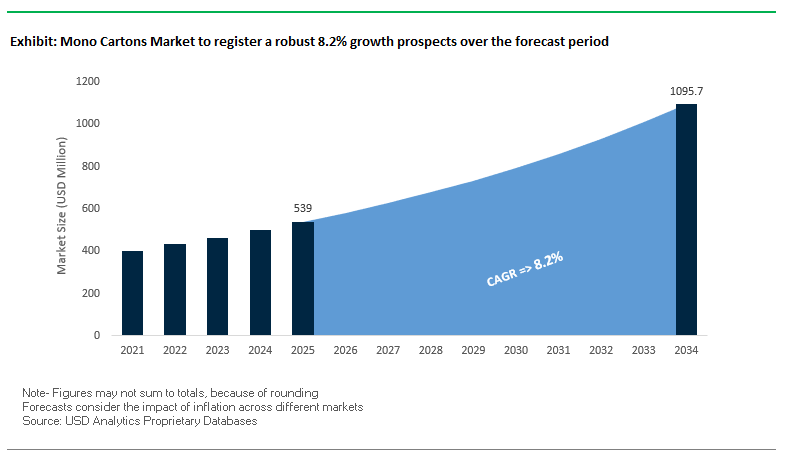

The global mono cartons market is projected to grow from $539 million in 2025 to $1,095.6 million by 2034, reflecting a CAGR of 8.2%. This growth is fueled by increasing demand for sustainable, recyclable packaging, the rise of e-commerce and direct-to-consumer (DTC) models, and innovations in smart and interactive packaging. Mono cartons, being single-layer paperboard solutions, provide a lightweight yet robust packaging option, helping brands reduce plastic usage while delivering premium shelf appeal.

Key Insights for Industry Stakeholders

- Sustainability driving adoption: Mono cartons leverage renewable and recyclable fibers, supporting circular economy goals and reducing environmental footprint.

- E-commerce influence: Strong strength-to-weight ratio ensures product protection during shipping while lowering transport costs.

- Digital and smart packaging integration: QR codes, RFID tags, and scannable features enhance supply chain transparency, anti-counterfeiting, and consumer engagement.

- Premium branding and aesthetics: Techniques such as litho-lamination, embossing, and foil stamping differentiate products on crowded retail shelves.

- Cross-industry adoption: Applicable across food & beverage, personal care, healthcare, and industrial segments, offering versatility in packaging solutions.

Market Analysis: Recent Industry Developments Highlighting Mono Cartons Innovation

The mono cartons industry has witnessed strategic innovations and mergers that reflect both sustainability focus and market expansion. In August 2025, Graphic Packaging International (GPI) launched its PaperSeal® Pressed MAP Tray, a mono carton-based solution that reduces plastic usage by up to 85%, demonstrating a commitment to eco-friendly packaging alternatives. The same month, GPI received four wins at the AmeriStar Awards, including recognition for its CleanClose™ child-resistant laundry detergent packaging, highlighting innovation in high-demand applications. Additionally, Amcor and Flügger introduced a paint container with 50% recycled material, signaling growing adoption of sustainable content in consumer-facing products.

July 2025 marked a significant structural change with WestRock merging with Smurfit Kappa to form Smurfit WestRock, strengthening its position as a global leader in paper-based packaging. In parallel, GPI partnered with Unilever to launch WHITE NOW oral care packaging, showcasing collaboration for sustainable product deployment. The company also published its 2024 Impact Report, demonstrating progress on its “Better by 2030” sustainability initiatives.

Investments in production capacity and alternative packaging continue to shape the industry. In May 2025, Mondi commissioned a €400 million paper machine at its Štětí mill, reinforcing leadership in sustainable paper-based packaging. In February 2025, Mondi partnered with Proquimia to launch a paper-based stand-up pouch for dishwashing tabs, while January 2025 saw PerfoTec develop laser micro-perforated bags extending produce shelf life up to three weeks, highlighting potential applications for mono cartons in food preservation.

Trends and Opportunities Transforming the Mono Cartons Market

Mandatory Design-for-Recycling Driven by Extended Producer Responsibility (EPR)

The mono cartons market is undergoing a structural shift as Extended Producer Responsibility (EPR) regulations reshape packaging design worldwide. Governments and regulators are forcing brands to eliminate non-paper components such as plastic windows, metallized laminates, and polyethylene coatings that complicate recycling. The move toward pure paperboard mono-material cartons ensures compatibility with standard paper recycling streams and aligns with circular economy objectives.

The European Union’s Packaging and Packaging Waste Regulation (PPWR), effective February 2025, sets a clear blueprint by requiring all packaging to achieve a recyclability score of at least 70% by 2030. Mono cartons naturally meet this criterion due to their ease of fiber recovery during repulping. In addition, new eco-modulated fee structures under EPR policies incentivize recyclable packaging: brands using mono cartons pay lower compliance fees compared to those still relying on non-recyclable formats.

The trend is not limited to Europe. By September 2025, six U.S. states, including Maine, Oregon, and California, had enacted EPR legislation, directly holding producers responsible for packaging collection and recycling. These measures are driving North American brands toward mono cartons to minimize regulatory risk and reduce financial liabilities tied to packaging waste management.

Adoption of Advanced Water-Based Barrier Coatings to Replace Plastic Liners

A second critical trend is the rapid adoption of water-based dispersion coatings as alternatives to traditional plastic liners. Historically, polyethylene (PE) coatings on paperboard created recyclability barriers, often leading to rejection by paper mills. Now, innovations in aqueous barrier coatings are solving this challenge by providing grease, moisture, and oil resistance while remaining fully repulpable.

Technical data from leading suppliers confirm that fiber recovery rates improve significantly when water-based coatings replace PE liners. These coatings maintain the required protective properties for frozen foods, fast food packaging, and dry goods while ensuring compliance with direct food contact regulations in both North America and Europe.

Industry collaboration is accelerating this transition. Packaging converters, chemical companies, and brand owners are piloting large-scale trials of these coatings across paper cups, frozen food boxes, and quick-service restaurant cartons. The dual benefit of functional performance and recyclability compatibility is making them the new standard for barrier-coated mono cartons.

Integration of Digital Printing for Mass Customization and Limited Editions

The rise of mono-material cartons presents a compelling opportunity to leverage digital printing technology for personalization and marketing agility. Digital presses enable cost-effective short runs, eliminating plate-making costs and setup time, making it feasible to deliver regional campaigns, limited editions, and personalized designs directly onto sustainable carton substrates.

Case studies demonstrate the business impact. For example, Momose Superfoods in Lithuania transitioned to digitally printed, recyclable packaging and reported both a sales uplift and stronger sustainable brand positioning. The global precedent set by the “Share a Coke” campaign highlights the scalability of personalization, where variable data printing can extend to mono cartons for promotions, seasonal events, or targeted demographics.

This opportunity allows packaging producers to position cartons not just as sustainable and recyclable but also as a dynamic marketing tool. By fusing sustainability with customization, brands can differentiate in crowded retail environments while appealing to eco-conscious consumers.

Development of Functional Inks and Coatings for Smart Packaging

Mono cartons also provide an ideal substrate for the integration of functional inks and coatings, enabling smart packaging solutions. The smooth, fiber-based surface supports the application of conductive inks, thermochromic coatings, and photochromic pigments that transform packaging into an interactive, information-rich medium.

Competitive Landscape of Global Mono Cartons Market

The mono cartons industry is highly competitive, driven by sustainability, innovation, and high-quality print capabilities. Leading companies differentiate themselves with fiber-based solutions, eco-friendly packaging innovations, and customized carton designs, ensuring strong market positioning and responsiveness to evolving consumer and regulatory demands.

Graphic Packaging International: Innovating Sustainable Mono Carton Solutions

GPI is a global leader in fiber-based packaging, offering folding cartons, rigid boxes, and specialty cartons across multiple industries. In August 2025, the company launched PaperSeal® Pressed MAP Tray to replace traditional plastic trays, while securing child-resistant certification for its CleanClose™ packaging. GPI’s “Better by 2030” commitments emphasize recyclable and fiber-based solutions that reduce plastic waste and elevate brand visibility. Innovative offerings like Boardio™ canisters and KeelClip™ clips underscore GPI’s focus on sustainable mono carton alternatives.

Smurfit WestRock: Leading High-Quality Folding Carton Solutions

Smurfit WestRock, formed from the July 2025 merger of WestRock and Smurfit Kappa, provides a comprehensive range of folding cartons and multipacks. Its strength lies in customization, high-quality printing, and brand-focused enhancements, including inks, coatings, and textured finishes. Smurfit WestRock’s products cater to food, healthcare, and beauty sectors, supporting both e-commerce shipping needs and retail shelf differentiation.

Amcor plc: Driving Recyclable and Specialty Carton Innovations

Amcor offers a diverse portfolio of folding and specialty cartons for food, beverage, and healthcare applications. In August 2025, Amcor and Flügger introduced 50% recycled paint containers, reflecting its commitment to sustainable packaging. With advanced printing capabilities like scented varnish and optical variable ink, Amcor focuses on enhancing consumer experience and brand differentiation while achieving its 2025 goal of fully recyclable or reusable packaging.

Smurfit Kappa: Sustainable and Circular Mono Carton Solutions

Before merging into Smurfit WestRock, Smurfit Kappa specialized in folding cartons and paper-based solutions containing 75% recycled fiber. With a CO2 reduction target of 40% by 2030, the company emphasizes sustainability and circular economy principles, offering packaging for consumer goods, e-commerce, and industrial applications, along with creative design and supply chain consultancy services.

Kotkamills Oy: Pioneering Virgin Fiber Mono Cartonboard

Kotkamills, a Finnish manufacturer of virgin fiber cartonboard, offers mono carton grades with water-based dispersion barriers suitable for food service and other demanding applications. In August 2025, the company ramped up production at its new mill to meet growing demand for sustainable, food-safe packaging. Its ALASKA® boards replace plastics in packaging while being fully recyclable, highlighting Kotkamills’ commitment to high-quality, eco-friendly mono carton solutions.

Mono Cartons Market Share Insights

Solid Bleached Sulfate (SBS) Retains the Largest Market Share by Board Type in the Mono Cartons Industry

Solid Bleached Sulfate (SBS) commands the largest share at 40% in 2025, reaffirming its premium positioning in industries where visual appeal, purity, and print performance are critical. Its superior surface brightness, rigidity, and ability to support complex finishing techniques make it the material of choice for cosmetics, pharmaceuticals, and high-end consumer goods. Recycled paperboard, however, follows closely with 35% share and is the fastest-growing segment, propelled by circular economy initiatives and recycled content mandates in food and beverage packaging. Coated Unbleached Kraft (CUK), with 20% share, appeals to brands seeking an “eco-premium” aesthetic that blends strength with sustainability. Specialty boards such as CCNB contribute the remaining 5%, mainly in cost-sensitive applications. SBS’s leadership reflects its ability to maintain a balance between performance, sustainability innovation, and premium branding needs in a competitive packaging environment.

Food & Beverage Dominates Market Share by End-Use Industry in the Mono Cartons Industry

The food & beverage industry secures the leading 45% share, underscoring its reliance on mono cartons as the primary packaging format for dry goods, frozen foods, and beverages. The sector’s dominance is reinforced by the global shift away from plastics, where recyclable cartons align with both regulatory mandates and consumer sustainability expectations. Pharmaceuticals and healthcare, with 20% share, represent the second-largest end-use, demanding high-rigidity, contamination-free SBS cartons with tamper-evidence features. Cosmetics and personal care claim 15%, driven by luxury packaging trends, while consumer goods hold 10%, increasingly replacing plastic clamshells with paperboard. Electronics & electricals (5%) and automotive (3%) use cartons for durability and protective secondary packaging. Collectively, food & beverage leads the industry by sheer volume, but the high-value growth drivers lie in healthcare and cosmetics, where stringent compliance and premium aesthetics make cartons indispensable.

United States: Regulatory Push and Innovative Packaging Driving Mono Carton Growth

The United States mono cartons market is being influenced by new state-level regulations and sustainability initiatives, including the U.S. Plastics Pact, which targets recycling or composting 50% of plastic packaging by 2025 and achieving 30% recycled content. Although primarily focused on plastics, these regulations are accelerating the shift toward eco-friendly paper-based packaging alternatives like mono cartons.

Technological advancements are transforming the market, with smart and sustainable packaging solutions emerging. Companies are leveraging recyclable, bio-based paperboard, combined with advanced printing technologies such as digital printing, embossing, and foil stamping to deliver high-quality, customizable packaging that enhances brand visibility. Corporate investments, such as International Paper’s strong growth in the mono carton segment in late 2024, reflect the increasing demand from the food and beverage, cosmetics, and personal care sectors. Mono cartons are particularly favored for e-commerce and retail packaging, offering lightweight yet sturdy protection while providing ample space for branding and product information.

Germany: Circular Economy and High-Performance Paperboard Drive Market Expansion

Germany’s mono cartons market is shaped by the European Union’s Packaging and Packaging Waste Regulation (PPWR) 2025, which mandates that all packaging in the EU be economically recyclable by 2030. This regulatory framework strongly favors mono-material, recyclable packaging solutions and supports the adoption of sustainable paperboard alternatives.

Technological innovation is at the forefront, with German manufacturers focusing on high-performance, lightweight, and recyclable paperboard materials. Advanced printing and finishing techniques enhance both functionality and aesthetics. The country’s robust recycling infrastructure and leadership in the circular economy further support eco-friendly packaging adoption. Key applications are concentrated in the food, pharmaceutical, and cosmetics sectors, where mono cartons are used for everything from cereals and frozen foods to over-the-counter medications.

China: Government Support and Automation Enable High-Efficiency Mono Carton Production

China’s mono cartons market is growing under supportive governmental initiatives promoting high-performance paperboard manufacturing and sustainable production practices aligned with dual-carbon targets. Policies encouraging sustainable manufacturing standards are driving investments in eco-friendly packaging solutions.

Technological advancements include automation and AI integration to improve production efficiency and quality control. For example, Qingdao Meiguang Machinery Co., Ltd. launched China’s first single corrugated laminating production line, offering high efficiency and lower labor costs. The market is driven by the country’s rapidly expanding e-commerce, electronics, and consumer goods sectors, with mono cartons being widely adopted for product packaging ranging from smartphones to personal care items. Government support and booming end-use industries indicate significant capital flow into the mono cartons segment.

India: Make in India and PLI Schemes Boost Sustainable Mono Carton Adoption

India’s mono cartons market is benefiting from initiatives like Make in India and the Production Linked Incentive (PLI) scheme, which encourage domestic manufacturing and investment in sustainable packaging solutions. The government’s push for a circular economy is further supported by regulations such as the CPCB’s Extended Producer Responsibility (EPR) registration, driving the shift from plastics to paper-based mono cartons.

Corporate initiatives highlight the market’s momentum. For instance, Diageo India announced in late 2024 the phase-out of mono cartons for premium Scotch brands like VAT 69 and Black & White, saving an estimated 10,000 tonnes of paper annually. Key applications span e-commerce, pharmaceuticals, and consumer goods, where mono cartons play a crucial role in brand presentation, product protection, and premium unboxing experiences.

Japan: Innovative Paperboard and Sustainability Guidelines Accelerate Market Growth

Japan’s mono cartons market is influenced by regulatory updates for food containers and packaging effective June 1, 2025, which introduce a positive list for synthetic materials. Japanese manufacturers are focusing on high-quality, functional, and aesthetically appealing paperboard packaging, using advanced coatings and finishes to enhance durability and consumer appeal.

Sustainability remains a priority, with companies like Nissui actively reducing plastic usage in packaging and integrating paper-based alternatives. The company’s Container/Packaging Selection Guidelines 2025 exemplify this trend. Key applications are prominent in the food and beverage, and electronics sectors, where high-quality packaging is integral to the brand experience and consumer perception.

Mono Cartons Market Report Scope

Mono Cartons Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$539 Million

|

|

Market Size (2034)

|

$1095.6 Million

|

|

Market Growth Rate

|

8.2%

|

|

Segments

|

By Material Type (Coated, Uncoated), By Board Type (SBS, CUK, Recycled Paperboard, Others), By End-Use Industry (Food & Beverage, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Electronics & Electricals, Consumer Goods, Automotive, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Graphic Packaging International, LLC, WestRock Company, International Paper Company, Oji Holdings Corporation, Stora Enso Oyj, Sonoco Products Company, Mondi Group, DS Smith Plc, Huhtamaki Oyj, AR Packaging Group AB, Parksons Packaging Ltd., Amcor Plc, Rengo Co., Ltd., Walki Group, Mayr-Melnhof Karton AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Mono Cartons Market Segmentation

By Material Type

By Board Type

- SBS

- CUK

- Recycled Paperboard

- Others

By End-Use Industry

- Food & Beverage

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Electronics & Electricals

- Consumer Goods

- Automotive

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Mono Cartons Market

- Graphic Packaging International, LLC

- WestRock Company

- International Paper Company

- Oji Holdings Corporation

- Stora Enso Oyj

- Sonoco Products Company

- Mondi Group

- DS Smith Plc

- Huhtamaki Oyj

- AR Packaging Group AB

- Parksons Packaging Ltd.

- Amcor Plc

- Rengo Co., Ltd.

- Walki Group

- Mayr-Melnhof Karton AG

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to provide actionable insights into the global Mono Cartons market. Our approach integrates primary research, including interviews with packaging engineers, sustainability officers, supply chain managers, and industry executives, with secondary research from regulatory filings, corporate reports, trade journals, and industry databases. We evaluate technological advancements in mono-carton production such as digital printing, litho-lamination, embossing, and water-based barrier coatings, alongside material innovations including Solid Bleached Sulfate (SBS), recycled paperboard, and Coated Unbleached Kraft (CUK). Market sizing and forecasting incorporate historical trends, CAGR projections, regional dynamics, and adoption rates across end-use industries including food & beverage, pharmaceuticals, cosmetics, and electronics. Competitive intelligence analyzes mergers, acquisitions, sustainability initiatives, and innovative product launches by leading players such as Graphic Packaging International, Smurfit WestRock, Amcor, Mondi, and Kotkamills, emphasizing operational efficiency, recyclability, and brand-focused packaging solutions. This methodology ensures USDAnalytics delivers data-driven, reliable insights that help industry professionals optimize production, comply with sustainability mandates, and capitalize on emerging opportunities in the rapidly growing mono cartons market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.